CHART OF THE WEEK

We focus on macro and technical data driving markets, so you can focus on the trends that matter the most.

MOST RECENT

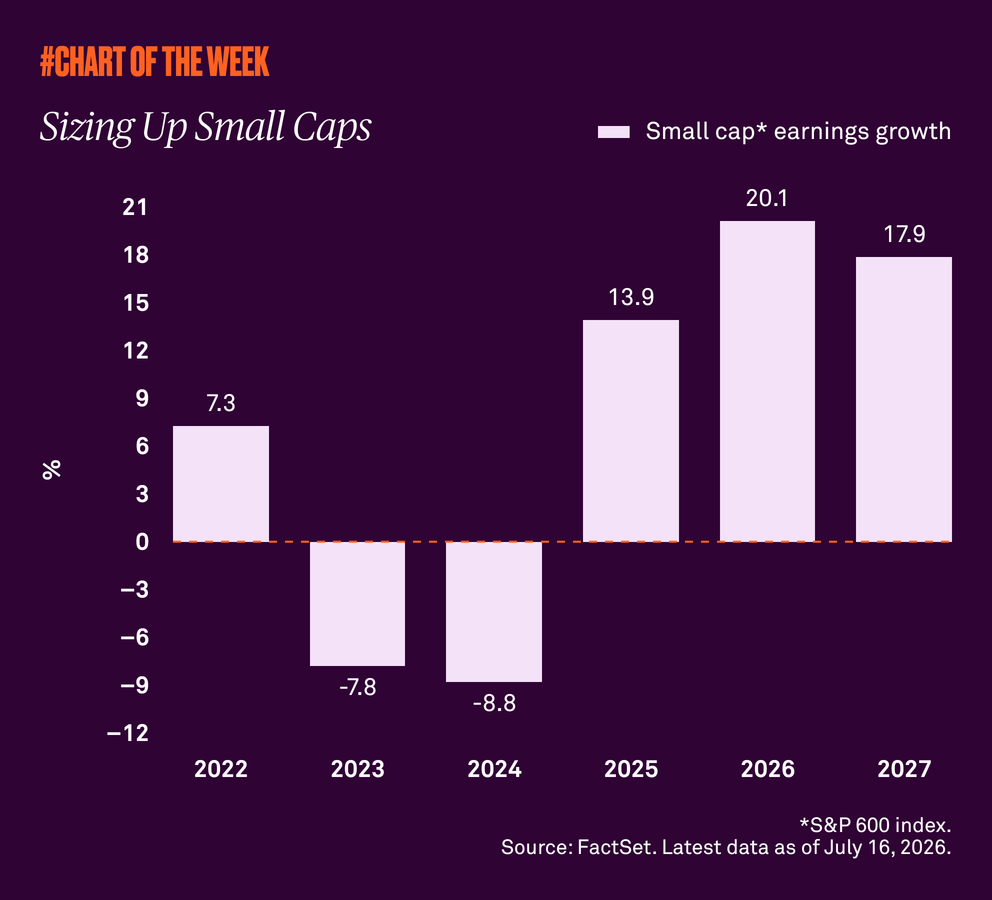

Sizing up small caps

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Previous Charts

Signs from sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

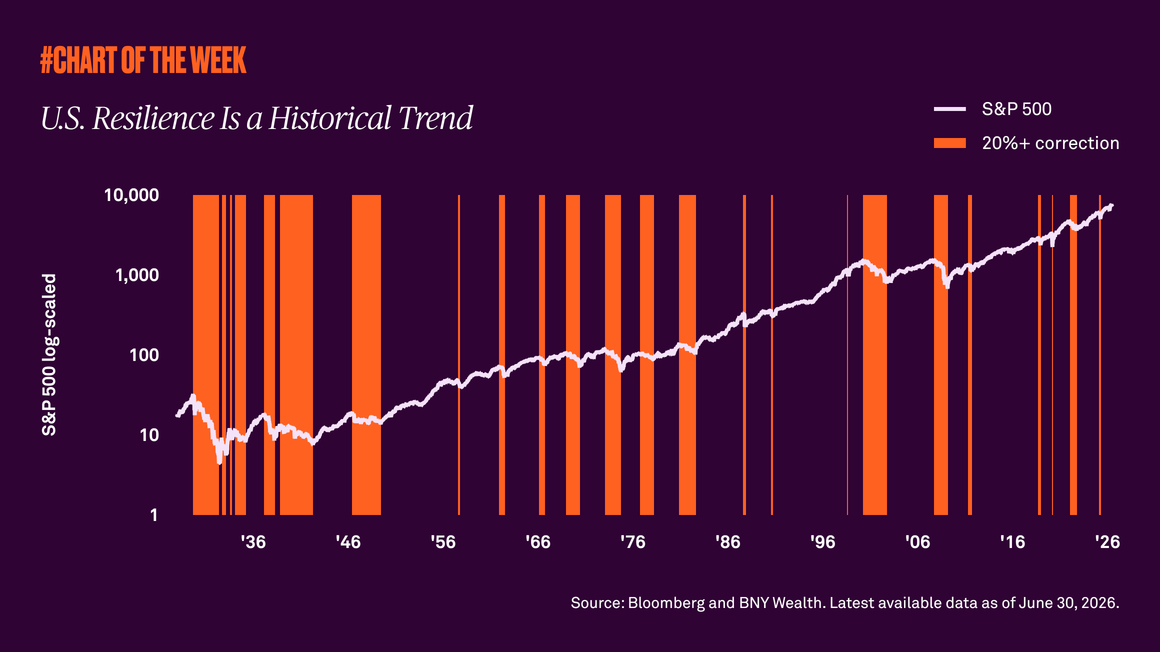

Resilience is a historical trend

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

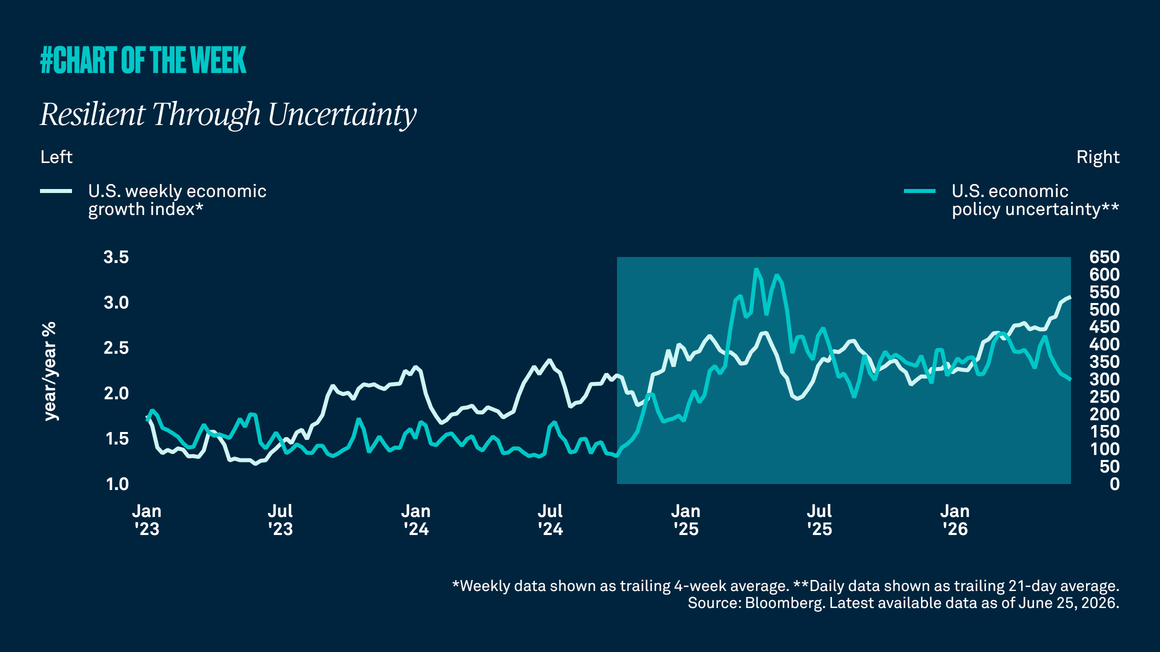

Resilient through uncertainty

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.

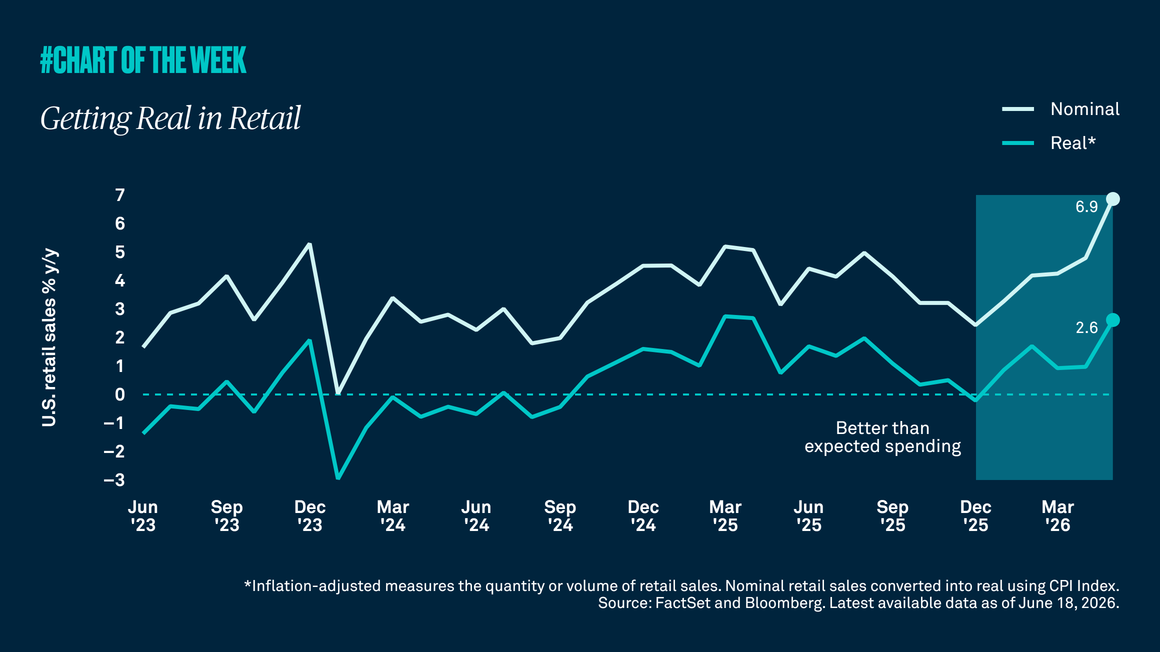

Getting real in retail

Despite persistent concerns that sticky inflation would erode purchasing power and drag consumer spending lower, the May retail sales data tells a different story. Spending is up not just in dollar terms, but in quantity, highlighting continued consumer resilience.

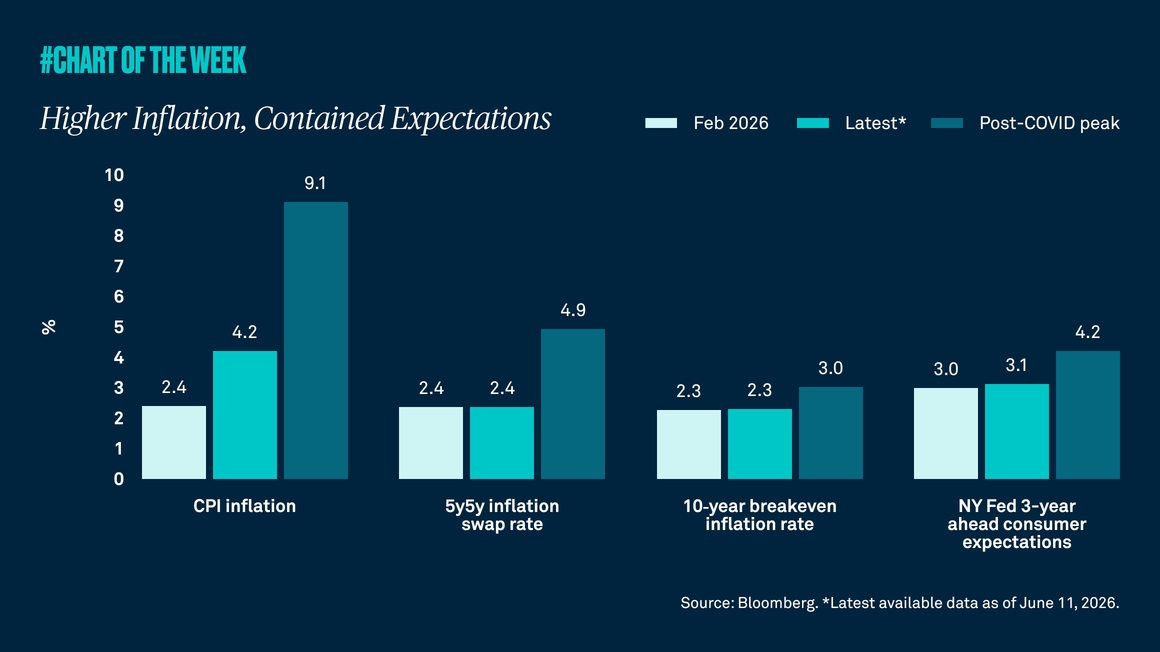

Higher inflation, contained expectations

Inflation has jumped since the Strait of Hormuz closed, squeezing consumers through higher gas and utility bills and pressuring businesses with higher freight and operating costs. Yet, longer-term inflation expectations remain contained, suggesting this looks more like a temporary energy shock than a lasting inflation upswing.

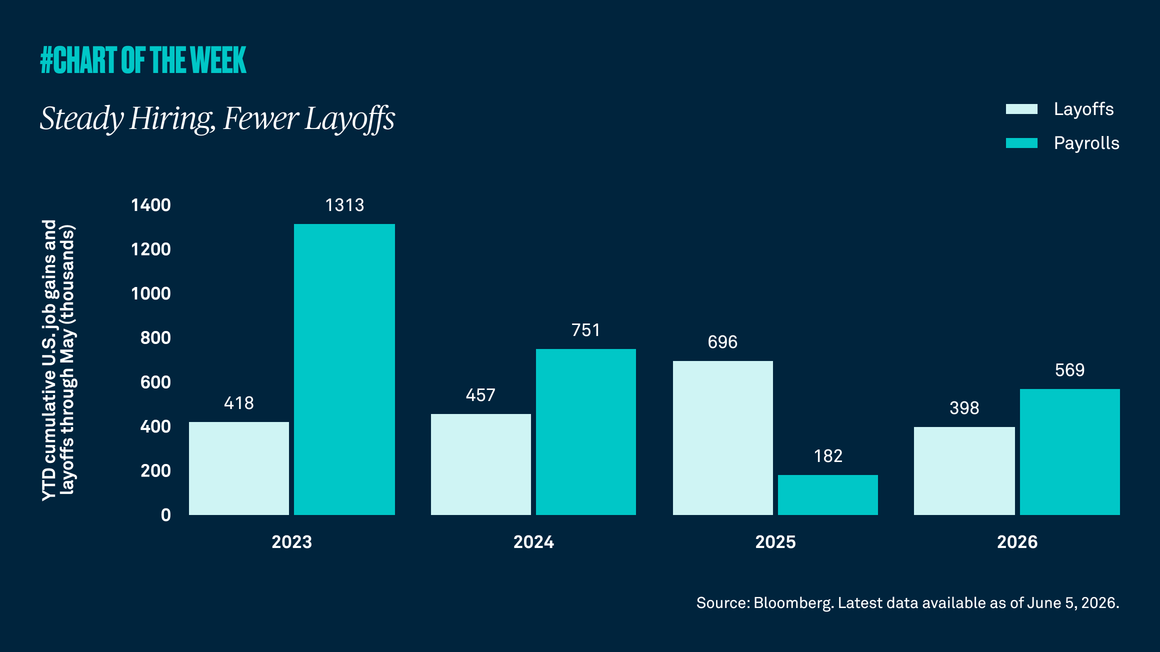

Steady hiring, fewer layoffs

May’s jobs report showed a labor market that is improving, with payroll growth exceeding expectations and layoffs down sharply from last year. Steady hiring and fewer layoffs should continue to support consumer spending and U.S. economic growth.

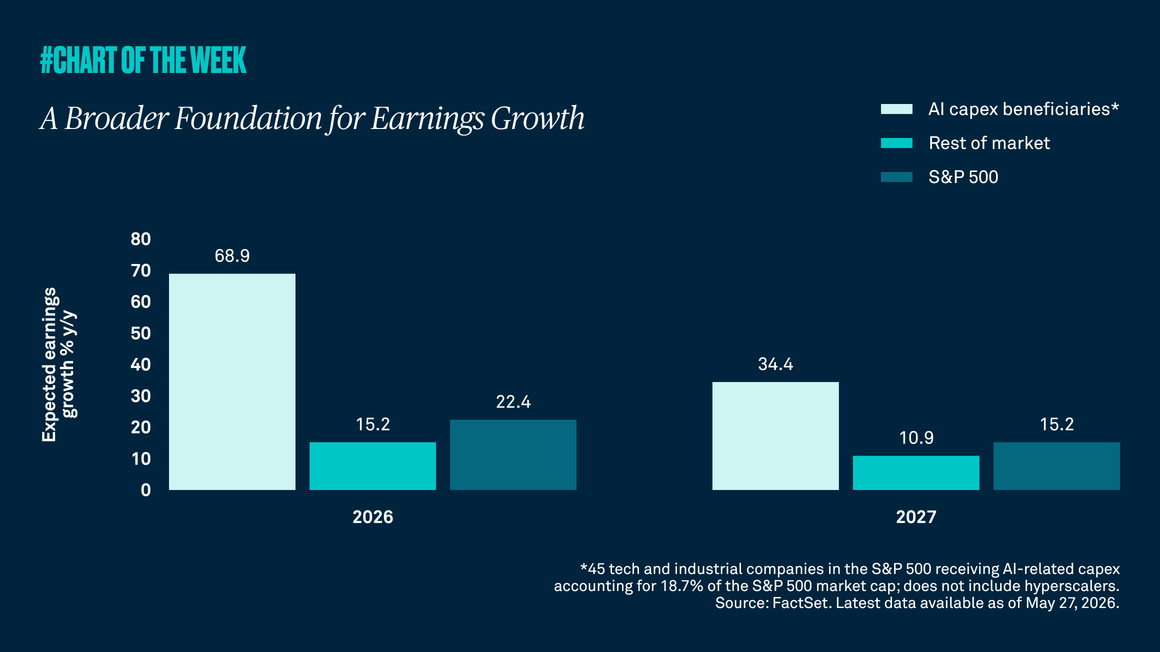

A broader foundation for earnings growth

Although companies benefiting most directly from AI-related capital spending are the main drivers of higher earnings, strength is no longer confined to that group. Earnings across the broader market remain solid and are expected to grow more than 10% this year and next, suggesting the risk of concentrated market leadership may not be founded.

Is the job market stabilizing?

After sluggish job growth in 2025, investors are looking for signs that the labor market may be stabilizing. With consumer spending driving 70% of economic activity, an improving labor market is essential to sustaining economic growth.

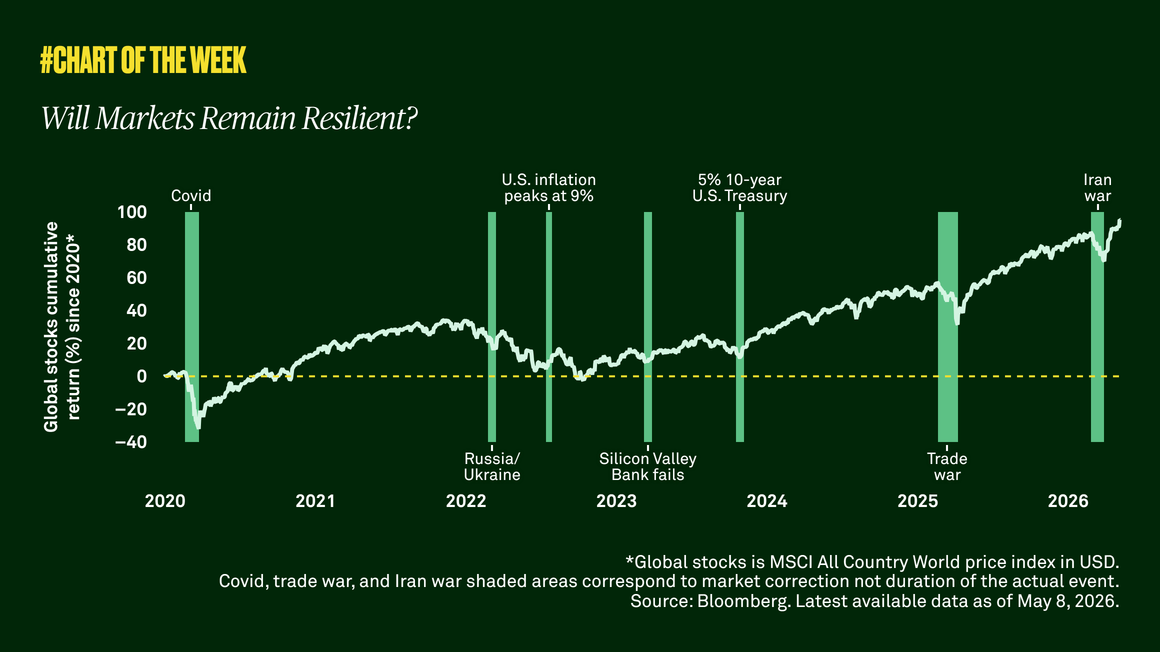

Will markets remain resilient?

Global equities have risen an annualized 11% since 2020 despite repeated shocks, as resilient growth and earnings have helped markets recover from periods of volatility. While the U.S.-Iran conflict poses near-term inflation and growth risks, markets remain constructive as earnings expectations continue to improve.

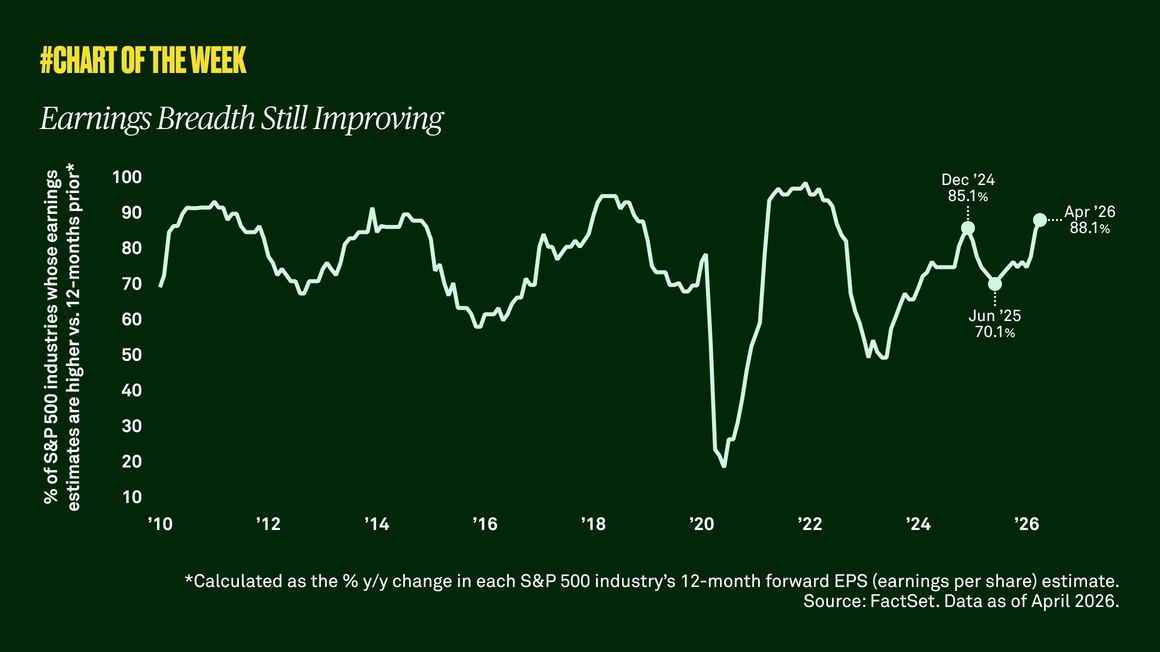

Earnings breadth still improving

Rising earnings estimates continue to support equities despite geopolitical and macroeconomic uncertainty. With profit growth broadening across S&P 500 industries, resilient corporate earnings underpin our constructive outlook for the stock market.

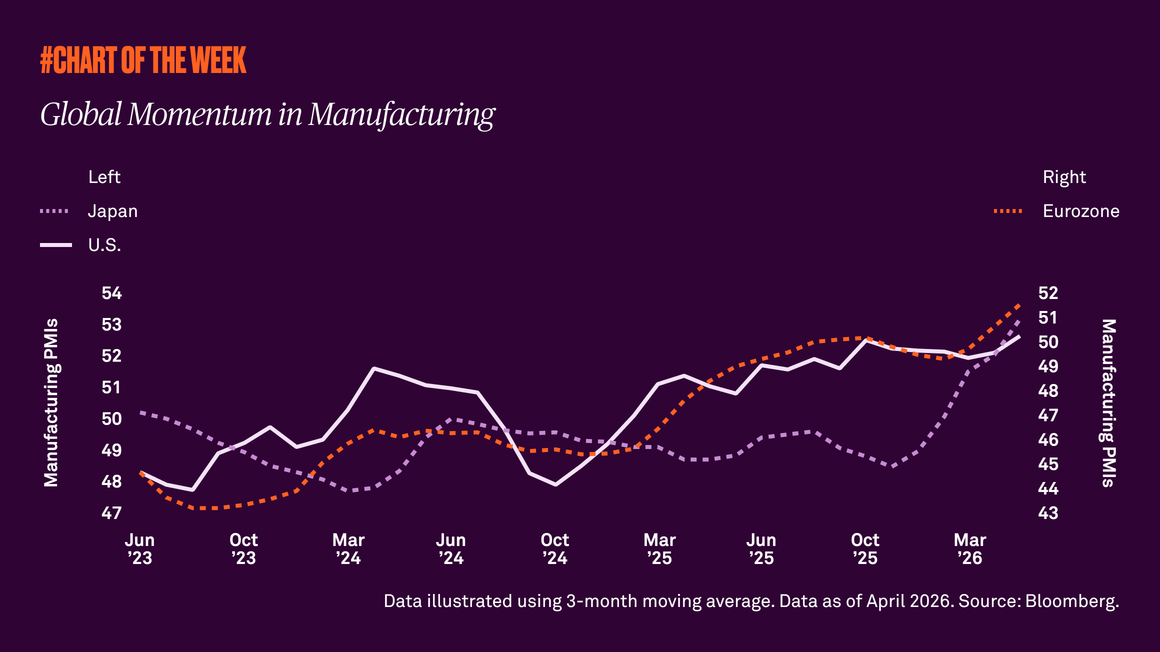

Global momentum in manufacturing

April PMIs (Purchasing Managers’ Indices) point to a meaningful improvement in global manufacturing momentum, with the U.S., Eurozone and Japan all posting stronger-than-expected and firmly expansionary results. The breadth of the rebound suggests improving global demand, supporting a constructive outlook for growth despite ongoing geopolitical tensions.

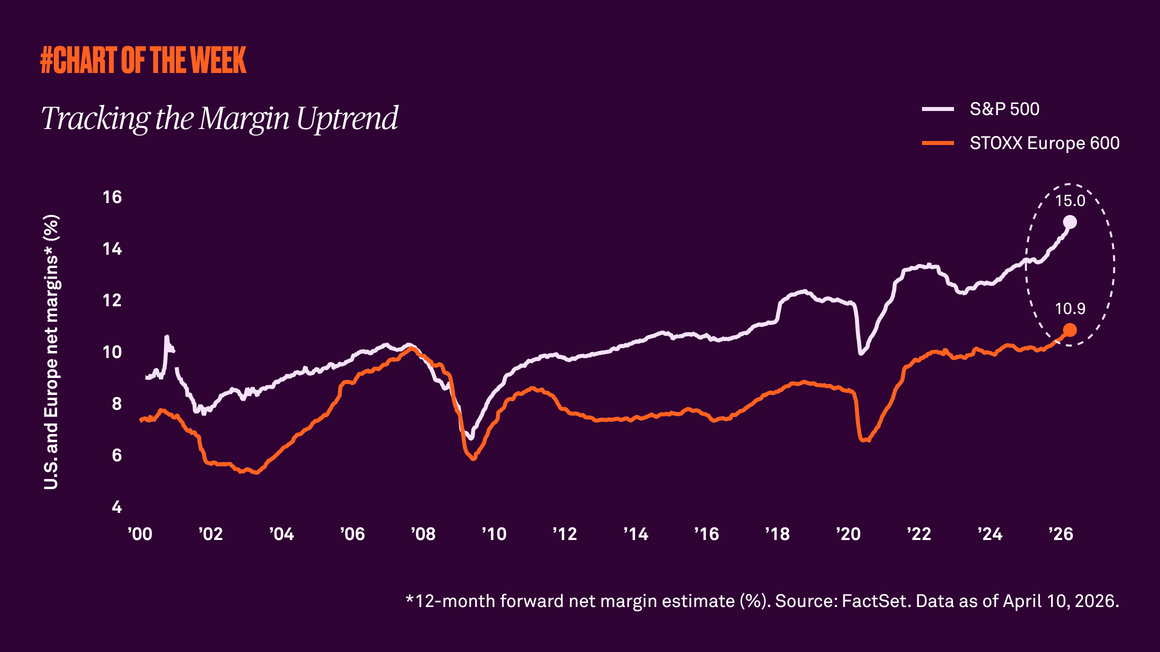

Tracking the margin uptrend

Rising margin expectations continue to support equities, underscoring the resilience of corporate profitability in the face of last year’s tariffs and this year’s Middle East war. The U.S. remains especially strong compared to peers, though first quarter earnings will be an important test.

Time to buy tech?

Technology valuations have meaningfully declined over the past year, but the sector continues to stand out for its strong earnings growth and relative resilience. While near-term uncertainty remains, tech still appears well positioned as a key driver of broader market growth.

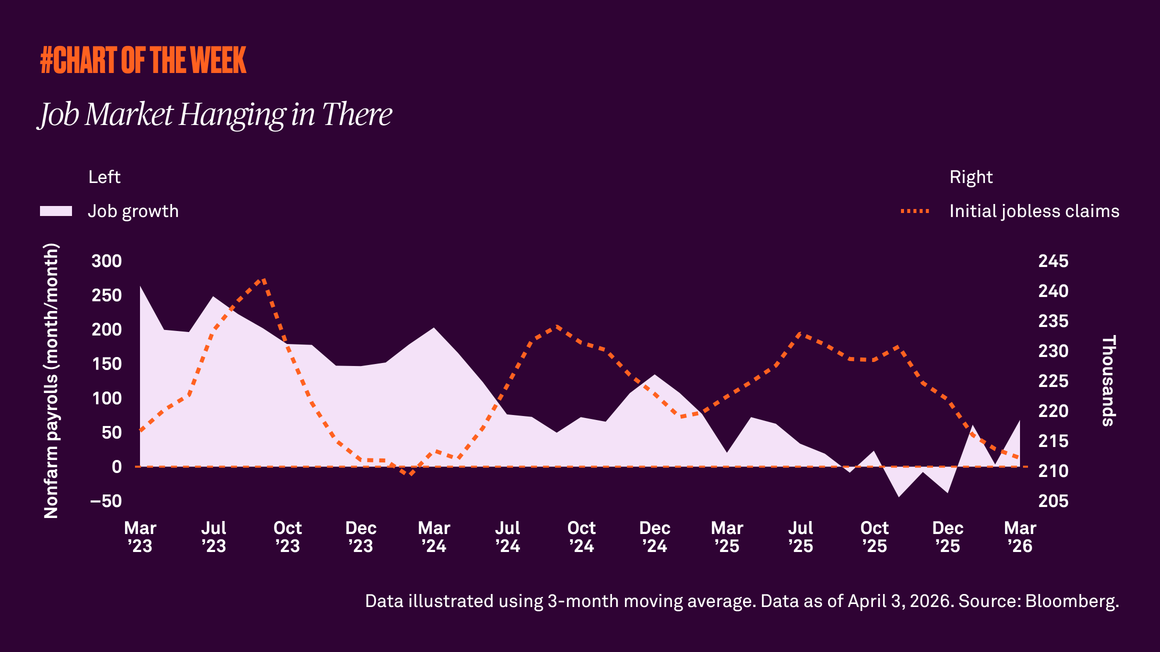

Job market hanging in there

Recent jobless claims data point to a resilient U.S. labor market, with both initial and continuing claims remaining low and signaling that unemployment is still contained. Although job growth has softened and remains subdued, March’s job growth of 178,000, the highest since 2024, is encouraging. Our constructive outlook still holds despite continued uncertainty related to the war in the Middle East.

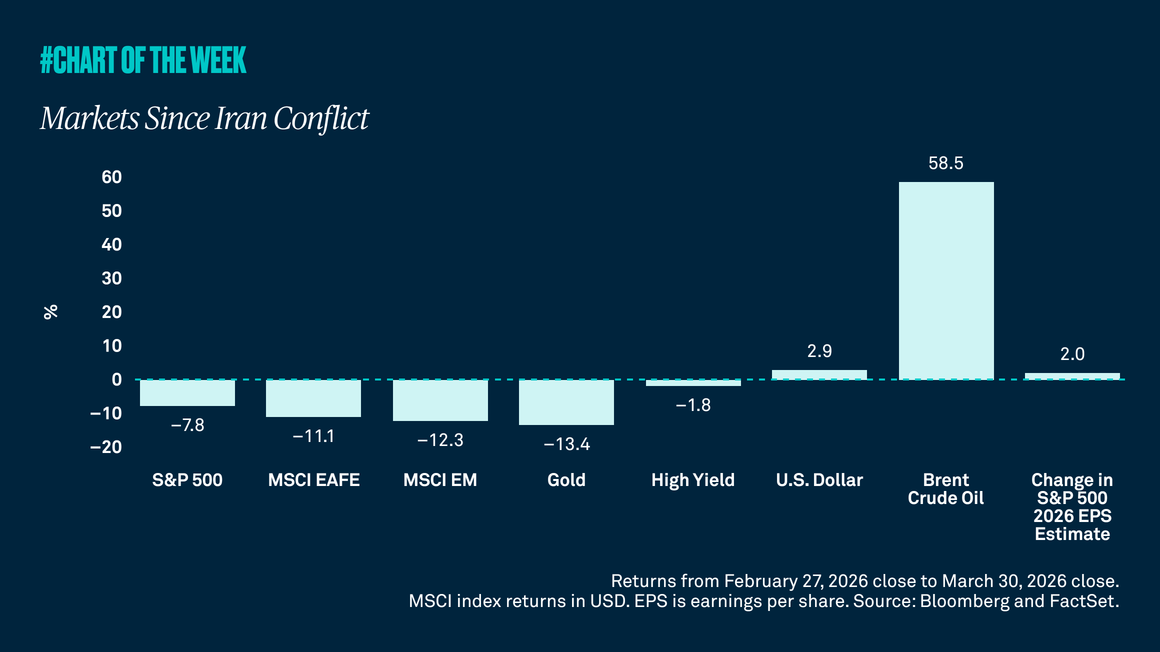

Markets since Iran conflict

Markets are reacting to the Middle East conflict with sharp moves across asset classes, signaling broad risk repricing and shifting safe‑haven behavior. While volatility is elevated, fundamentals like earnings growth continue to support our constructive outlook.

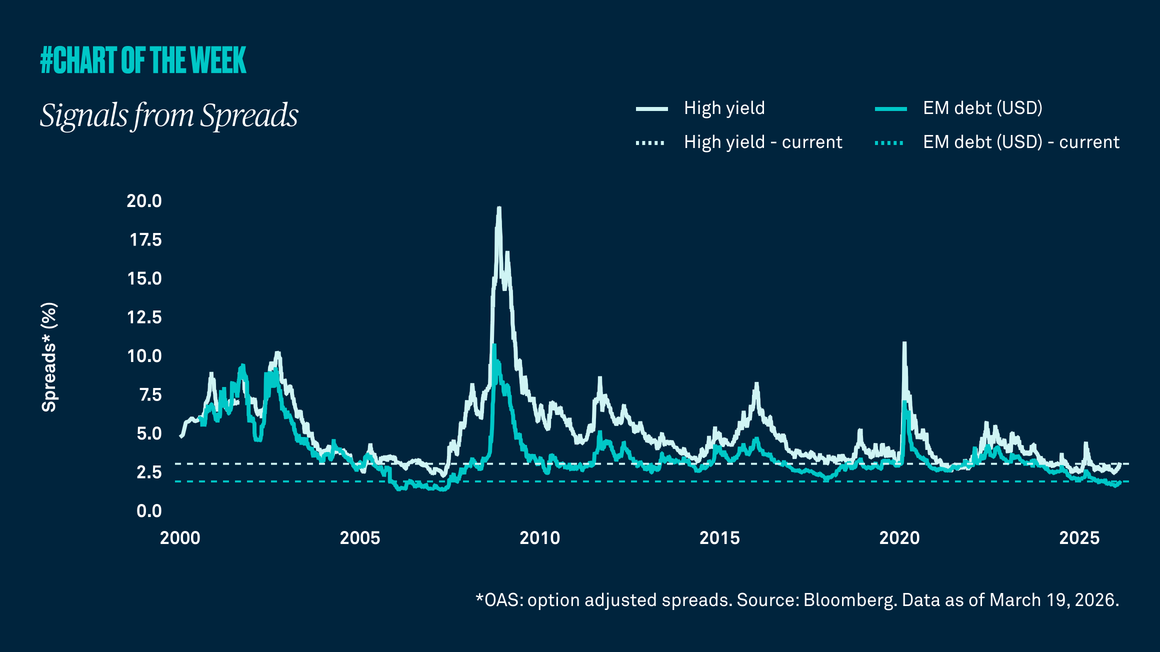

Signals from spreads

Credit spreads have risen yet remain historically low, reinforcing our view that the oil shock is likely temporary — not a driver of long-term growth concerns.

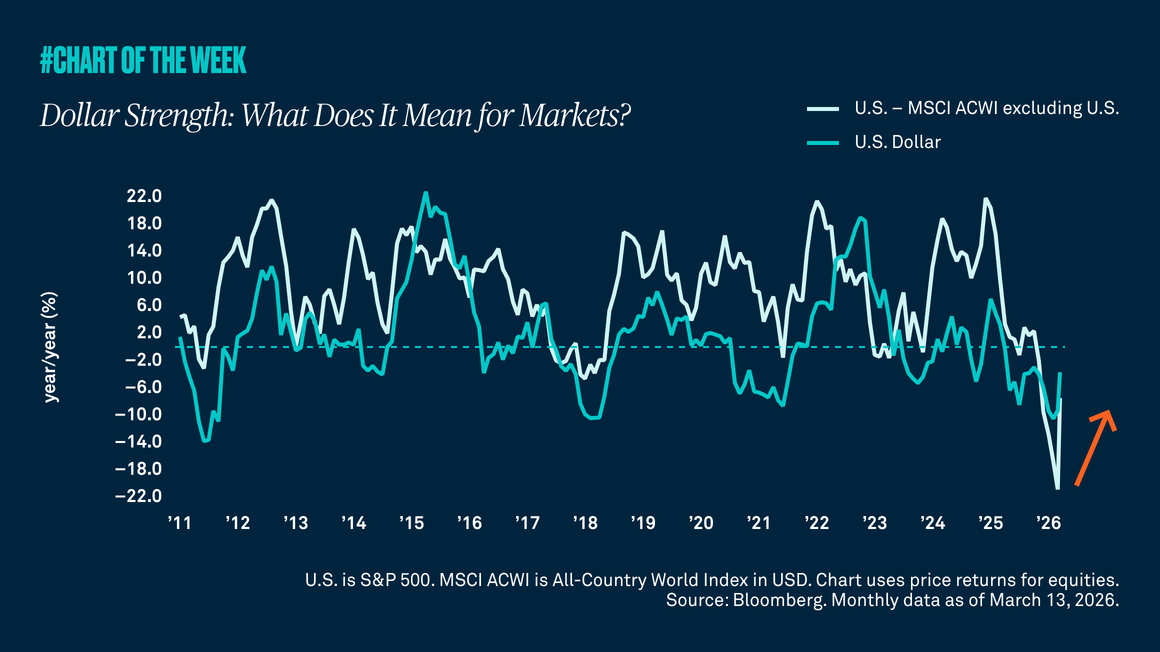

Dollar strength: what does it mean for markets?

Geopolitical tensions have lifted oil prices, sent U.S. stocks slightly lower and driven flows into the safety of the U.S. dollar, which has strengthened versus peers. While a weaker dollar previously supported international equity outperformance, dollar stabilization now suggests that tailwind is fading, underscoring the importance of diversification across regions and asset classes.

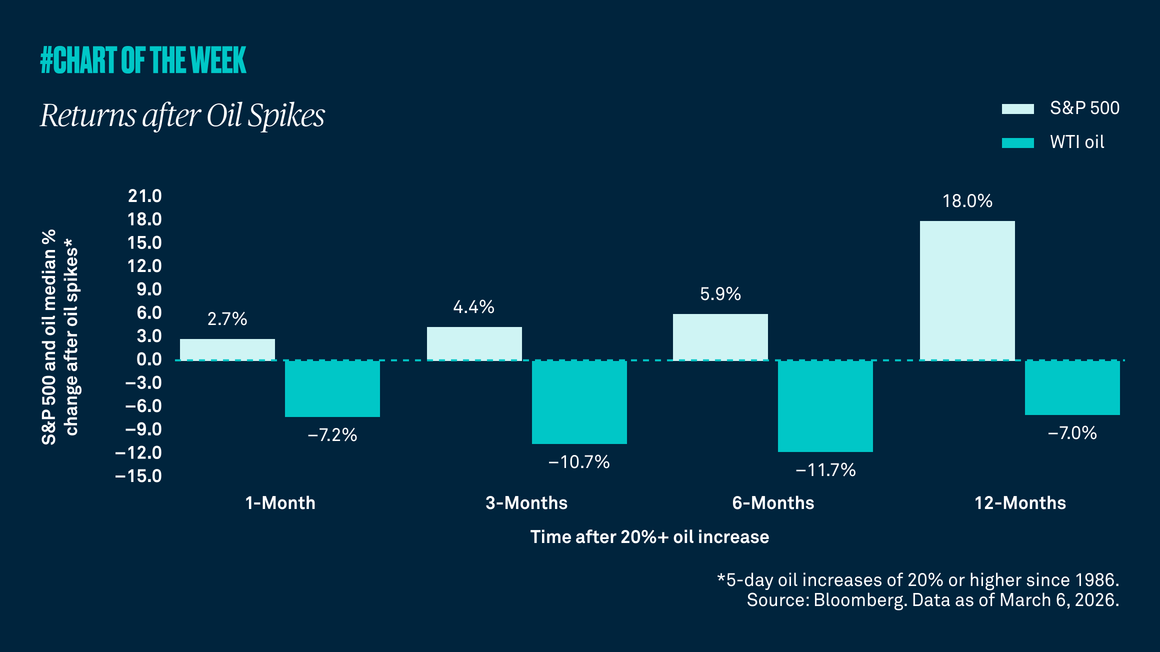

Returns after oil spikes

The Strait of Hormuz, which moves about 20% of global oil, has seen many ships that normally travel through it curtail their activity. Consequently, WTI oil was up over 36% in the five days after the oil supply shock began. Yet equities barely budged, signaling a temporary supply shock, not a larger crisis. Historically, after similar price spikes equities tend to move higher while oil prices decline — further evidence for avoiding emotion-driven investing.

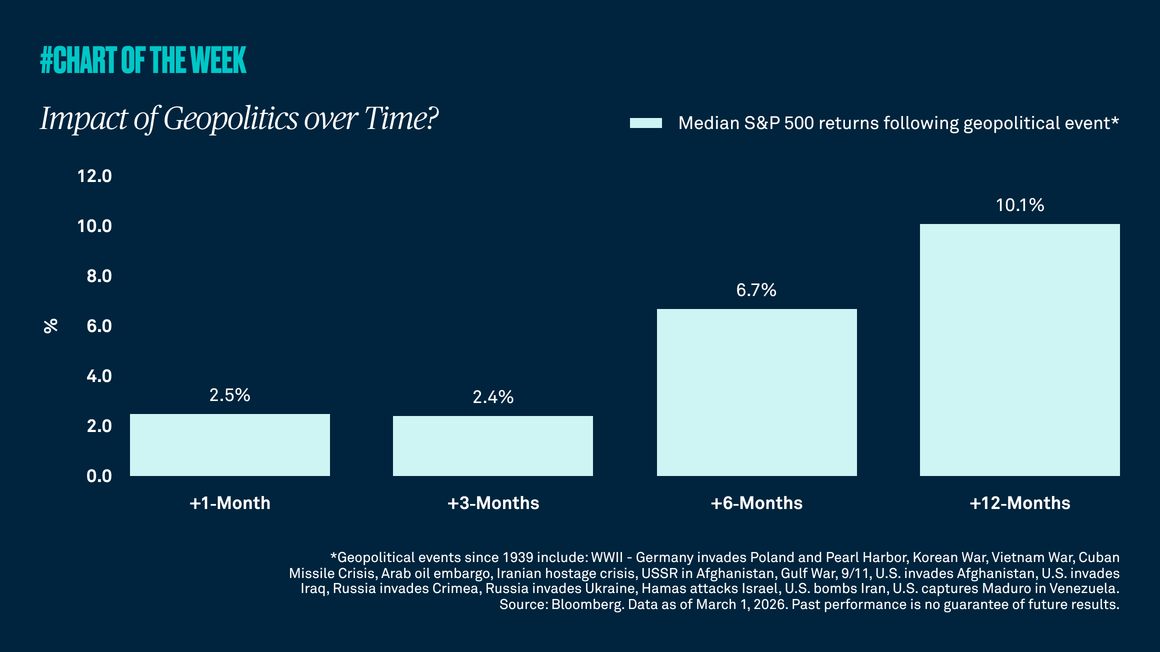

Impact of geopolitics over time?

Tensions between the U.S./Israel and Iran have recently boiled over into a military conflict, which has given many investors the jitters. However, our research shows that equity market pullbacks resulting from geopolitical events are often short lived with the S&P 500 typically higher in the months following these events.

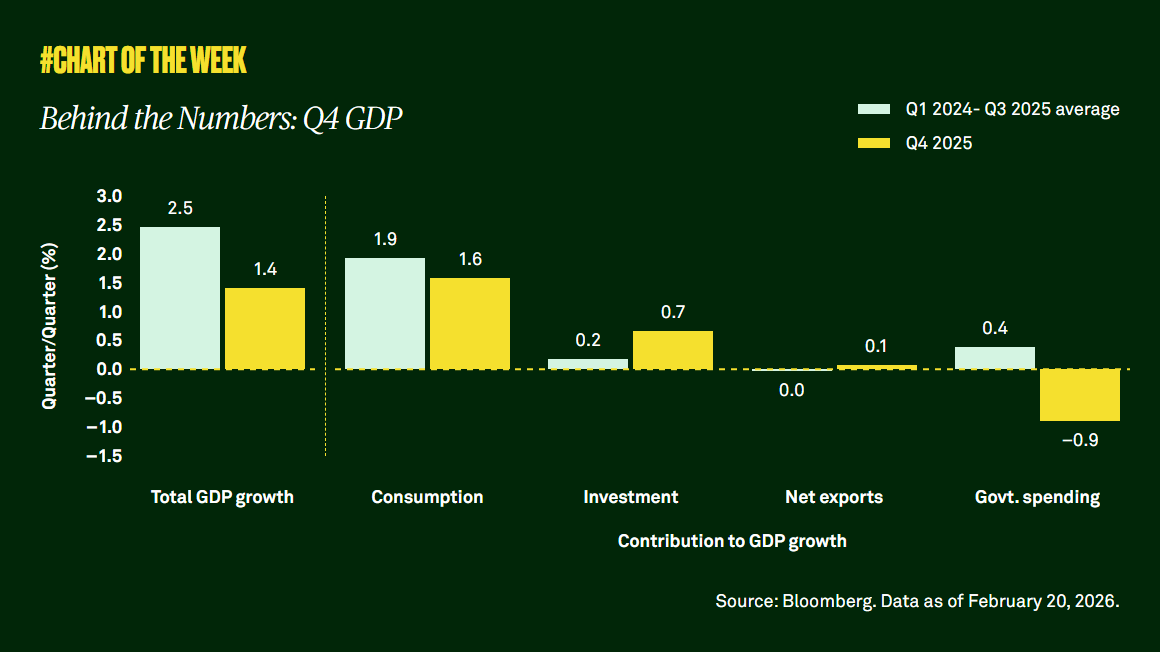

Behind the numbers: Q4 GDP

Gross domestic product undershot expectations last quarter, but the shortfall appears driven more by the temporary government shutdown than broad-based weakness. Consumer demand remains resilient, and with supportive fiscal policy, easing financial conditions and a steady labor market, the outlook points to a modest acceleration in economic activity this year.

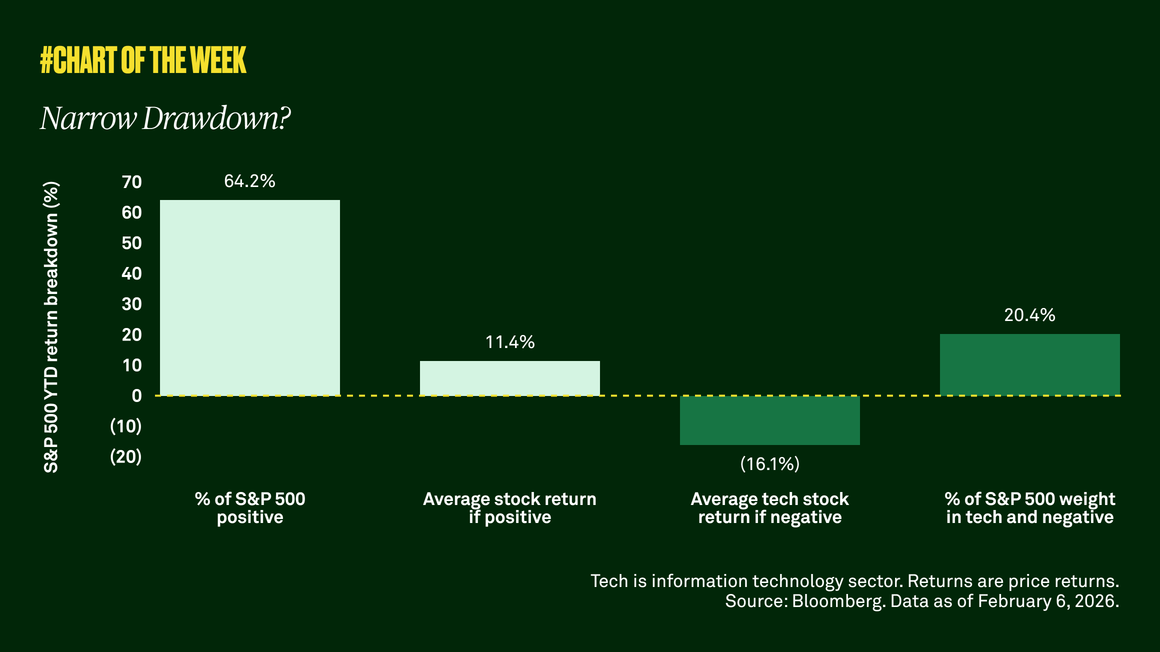

Narrow drawdown?

Equity volatility is rising, but all is not what it seems. The technology sector is weighing on the S&P 500 while value and cyclical stocks lead. A market rotation is underway as many investors begin to favor companies beyond tech.

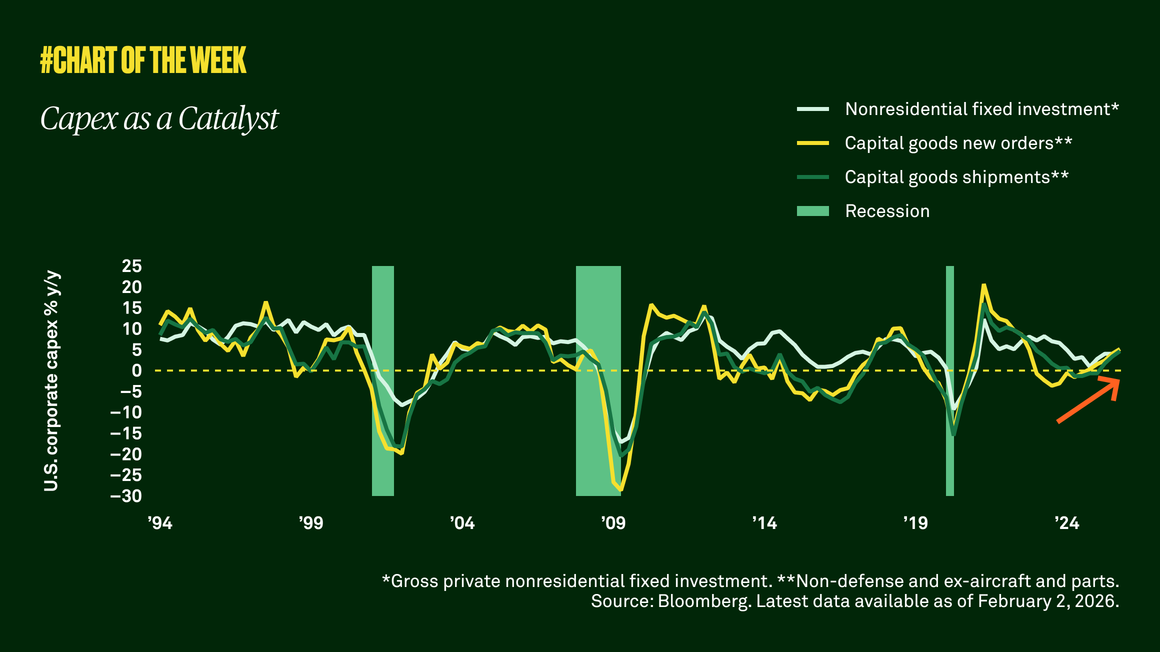

Capex as a catalyst

Improved business confidence and recent tax legislation are compelling corporations to reinvest their cash flows in their businesses. We believe this is a positive signal for economic growth.

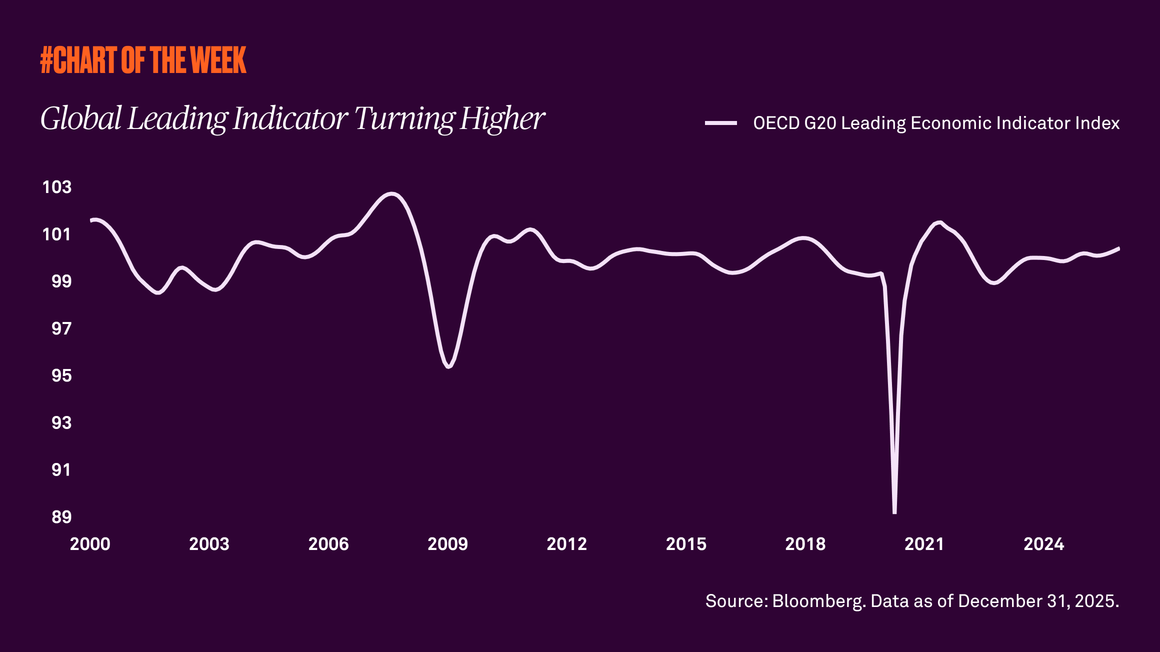

Global leading indicator turning higher

Headline volatility persists and yet the global growth outlook continues to improve. We examined a leading indicator, and why there is good cause to diversify equity holdings if you haven’t already.

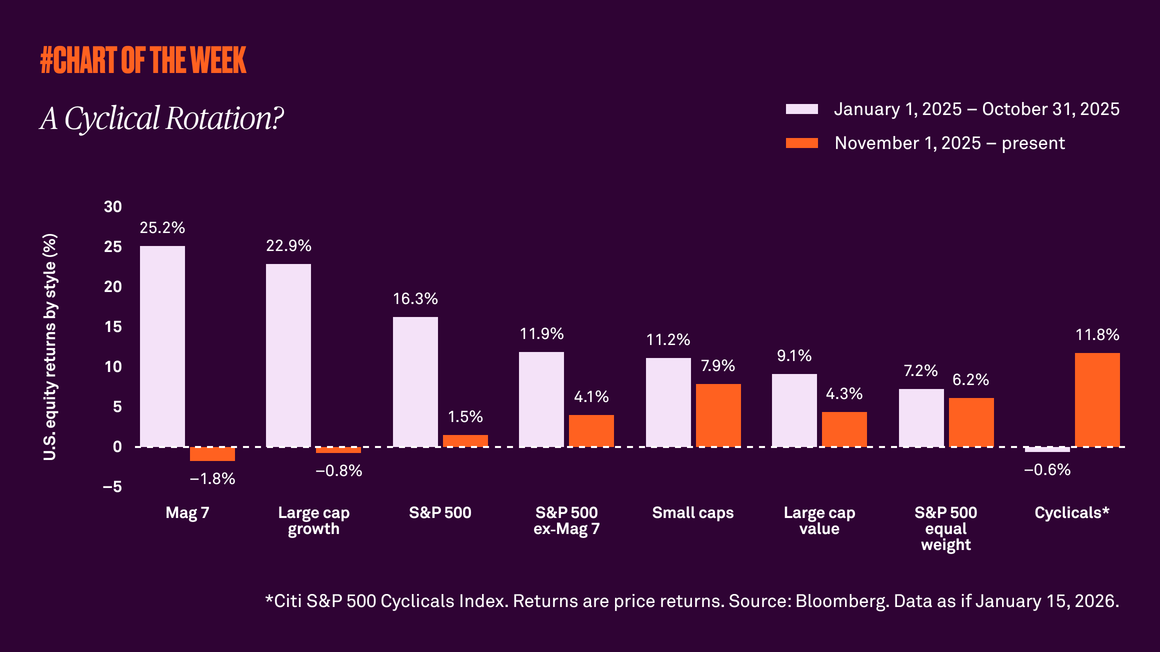

A cyclical rotation?

Stronger growth expectations are driving a global rotation out of growth-oriented and mega cap technology stocks, and into cyclical companies. At a time when geopolitical tensions and tariff discussions continue to simmer, we remind investors to stay invested despite the headline noise.

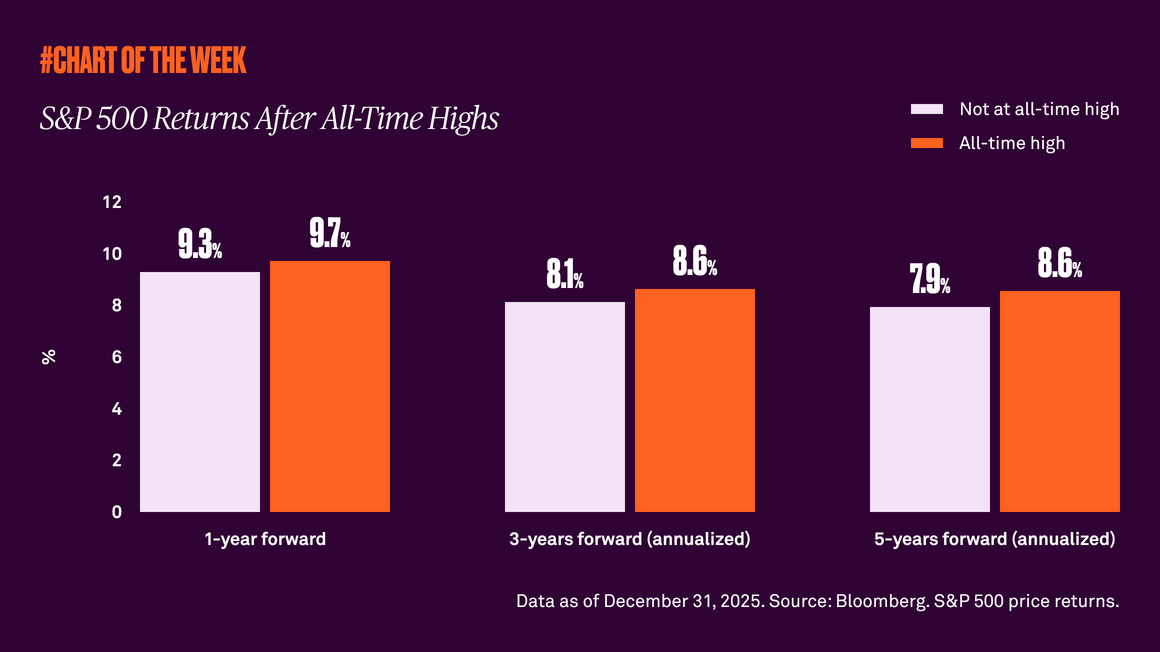

S&P 500 Returns After All-Time Highs

The S&P 500 recently hit a new all-time high after a notable year of peaks in 2025. Is now the time for caution? History tells us attractive performance often follows record highs.

Are earnings broadening beyond the magnificent 7?

Tech stocks have outperformed the rest of the S&P 500 for several years, and while we expect earnings growth among these companies to continue in 2026, we see another encouraging trend emerging. Earnings across the rest of the market are on an upward path too — and are set to contribute more to earnings growth for the S&P 500 Index in 2026 than the Magnificent 7.

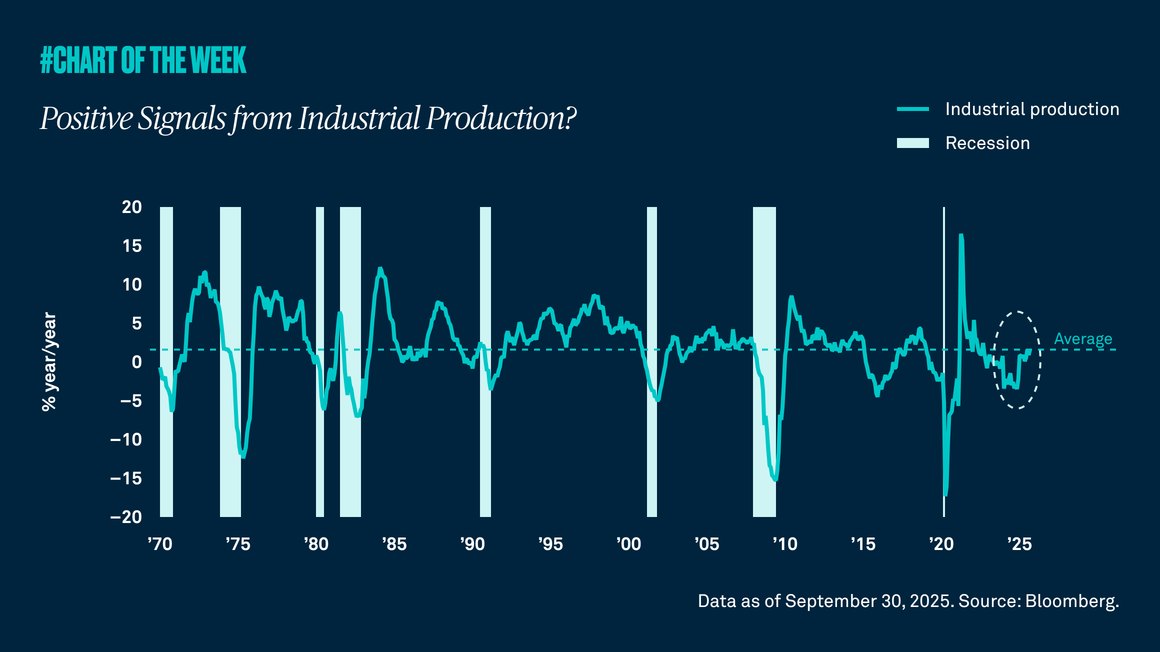

Positive signals from industrial production?

Industrial production is a proxy for the level of manufacturing in the economy, and last week’s report showed the highest growth rate in three years. Not only is this positive for the manufacturing sector and those companies tied to it, but it is also an indication that a recession may be unlikely in the near term.

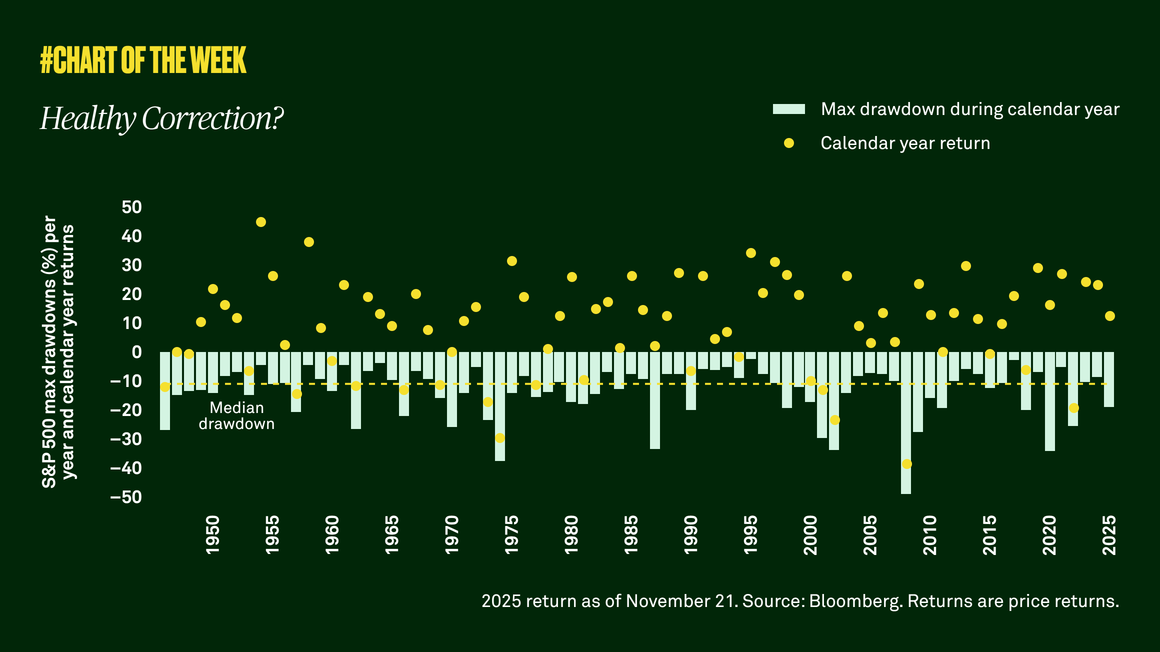

Healthy correction?

After climbing 17% year to date through late October, the S&P 500 declined 5% through November 20. We believe the market was due for a healthy correction. While further downside is possible, it would not concern us.

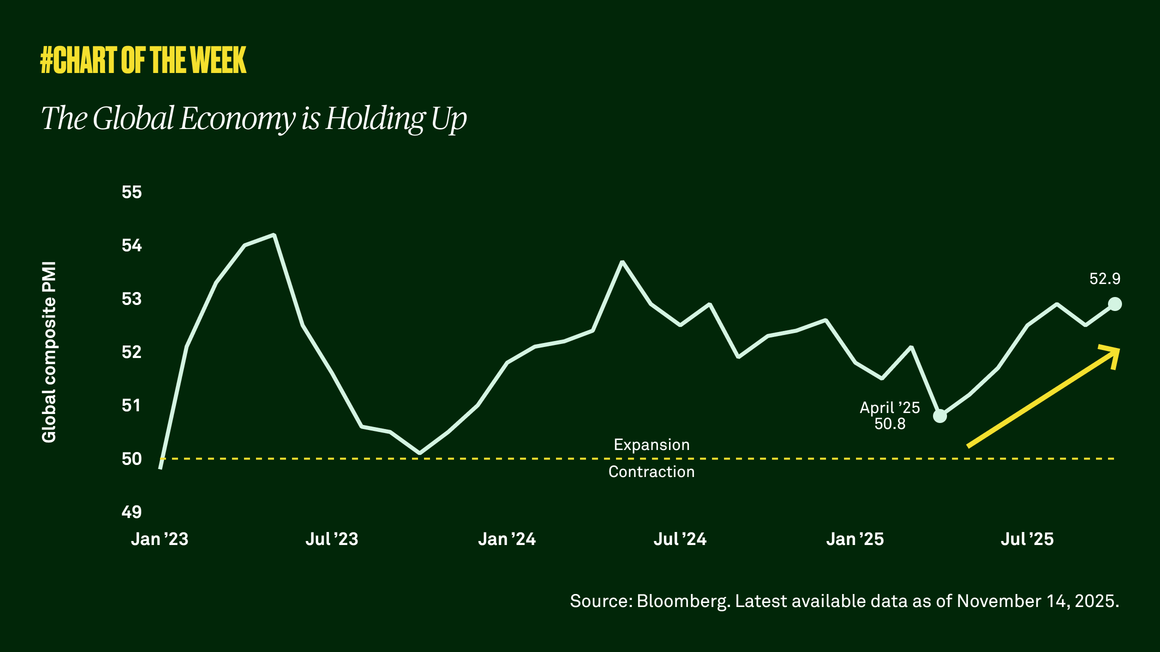

The global economy is holding up

This past year was rife with risks to the global economy: policy changes, tariff uncertainty and more. Yet, the global economy held up as manufacturing and services activity strengthened across the world. We see an opportunity for U.S. investors to diversify geographically.

Retail sales remain resilient

Considering the slowing job market, we dove into retail sales data to search for signs of the direction of household spending. We analyzed existing-store sales and found that, despite the softening labor market and concerns about growth, aggregate consumer spending remains resilient.

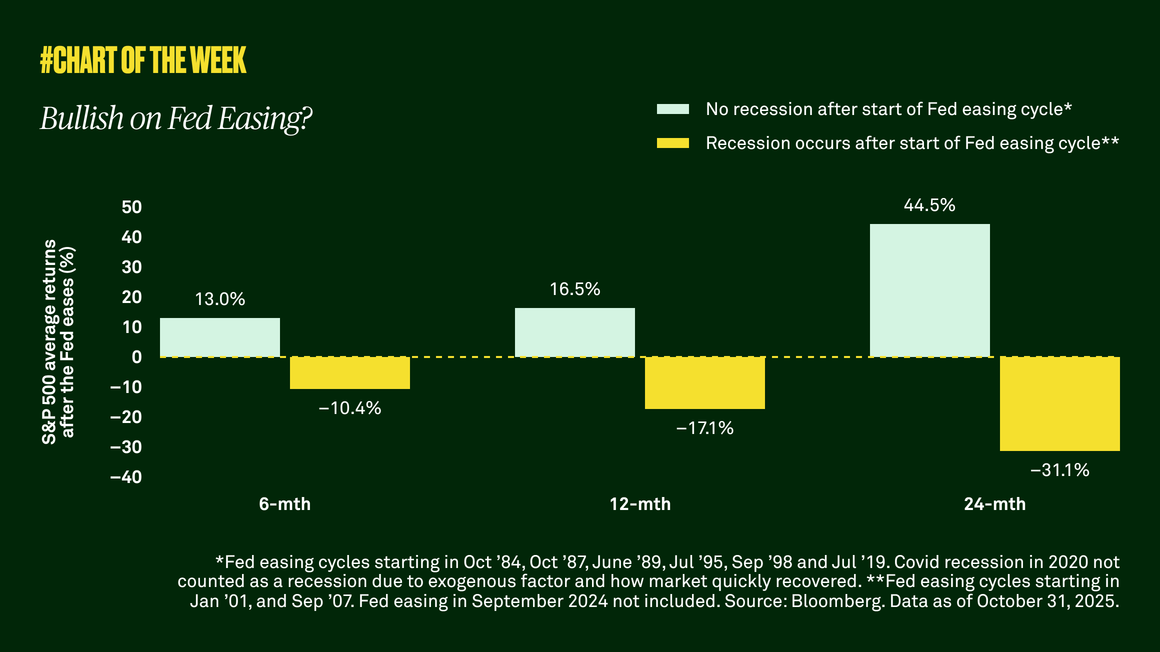

Bullish on Fed easing?

As expected, the Federal Open Market Committee delivered another 25-basis point rate cut. Investors are now focused on the pace of cuts from here. However, the more important driver of future equity returns is whether the Fed is easing into an economy that is growing or not.

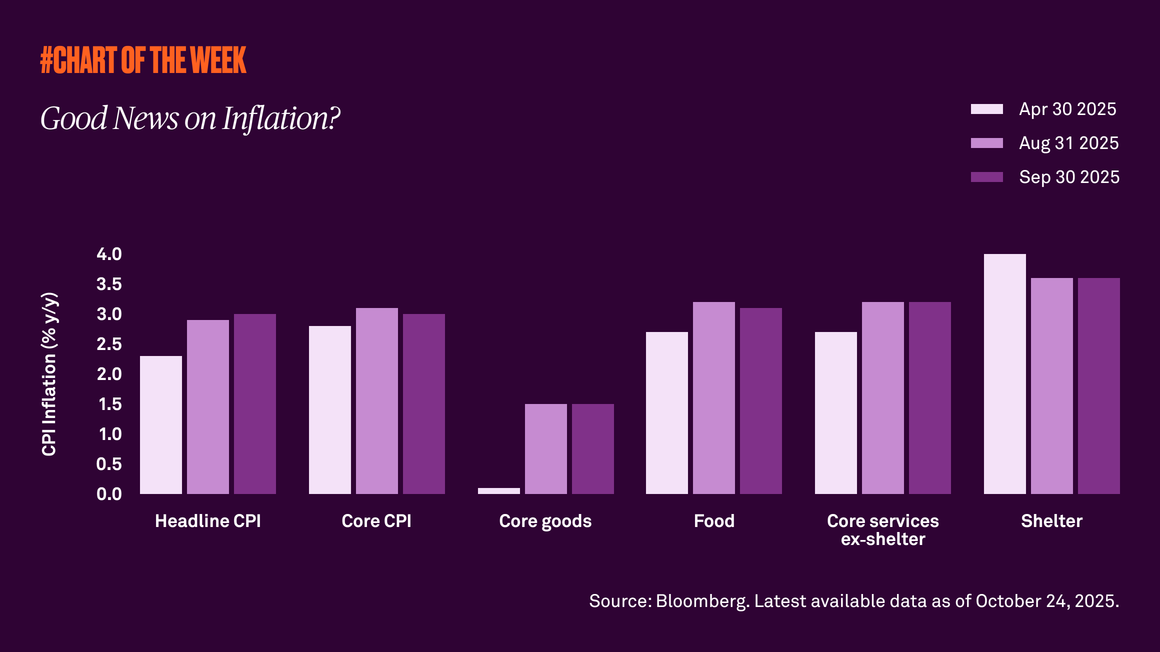

Good news on inflation?

Last week’s Consumer Price Index report, a widely used indicator of inflation in the U.S. economy, showed growth of 3% in September, which was above 2.9% in August but less than expected. Despite the modest increase, various categories have shown signs of stabilization. What does this mean for inflation going forward?

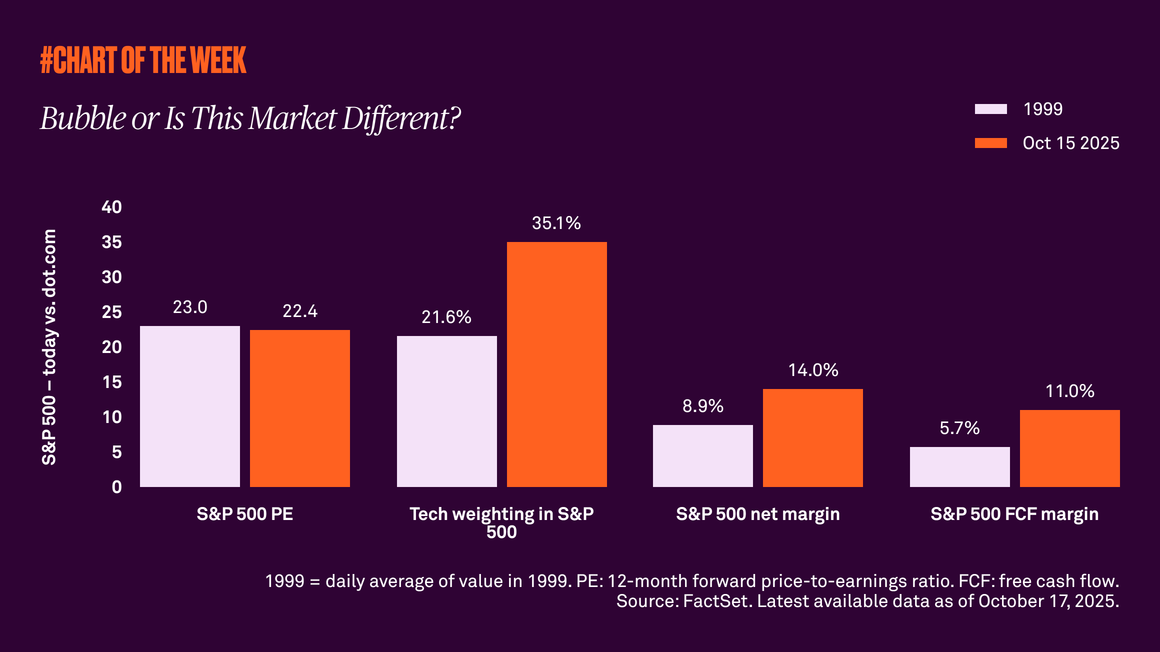

Bubble or is this market different?

The S&P 500 is up 14% year to date after gaining more than 20% annually over the past couple of years. Valuations are certainly elevated, but we believe the market is in a new world where higher multiples are normal rather than stretched.

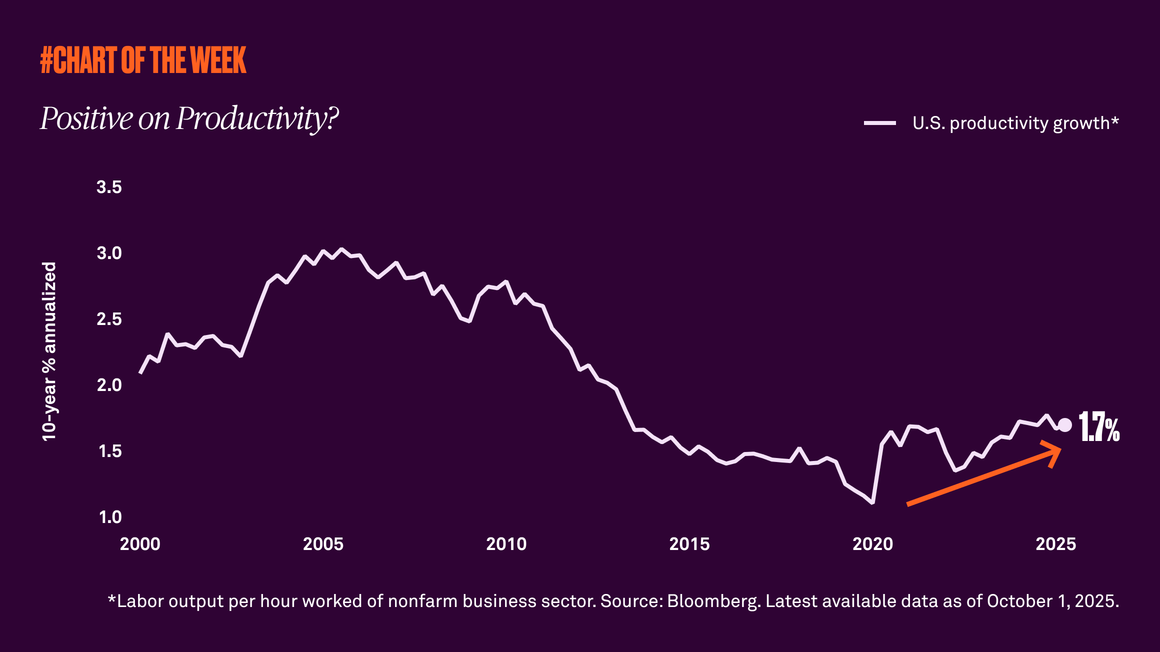

Positive on productivity?

Productivity, or output per hour worked, is a key driver of long-term economic growth. Now, after years of stagnation, productivity is on the rise again, a positive sign for future growth.

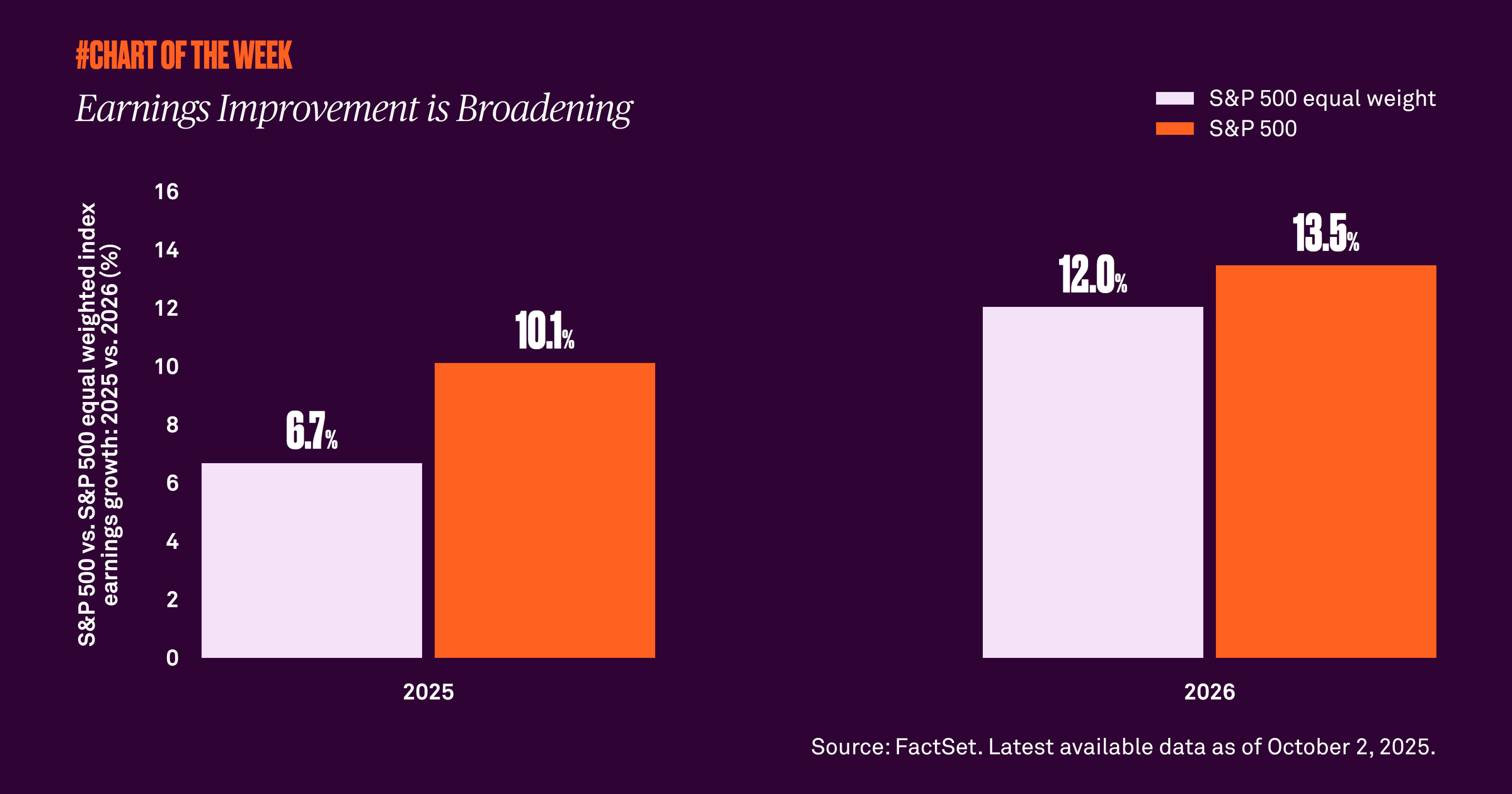

Earnings improvement is broadening

Earnings growth is on investors’ minds, especially as it broadens beyond the big tech stocks that have shown the most improvement in the past. We believe this is a positive sign for continued equity gains.

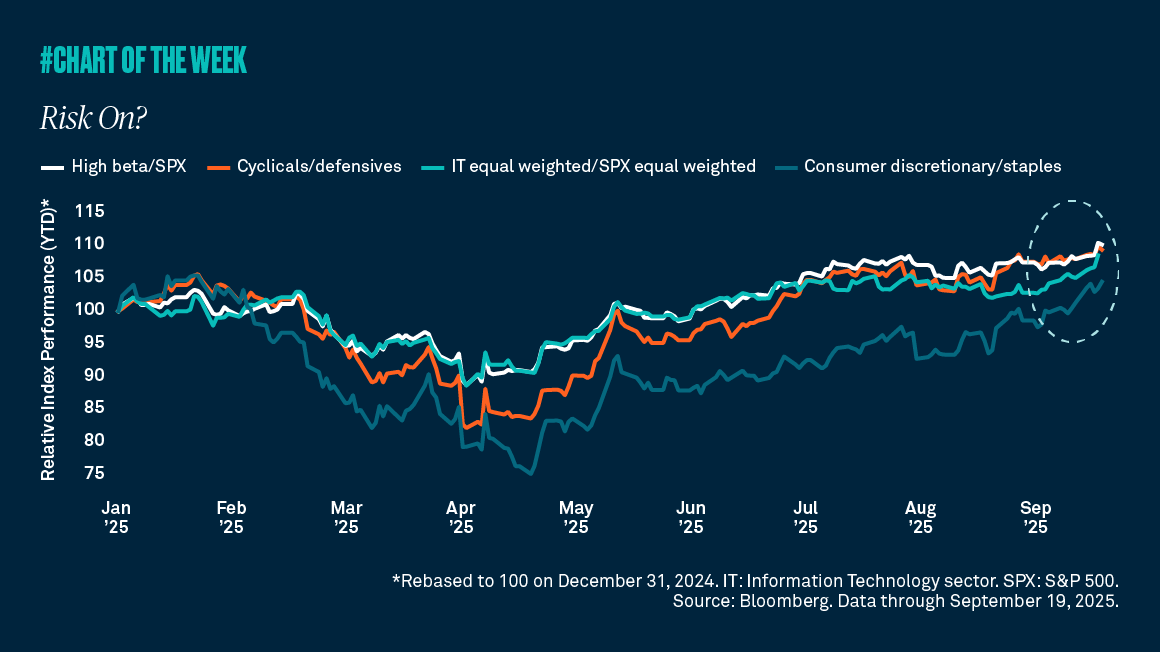

Risk on?

The S&P 500 is trading at record highs, which some investors didn’t see coming after the tariff-fueled drop in April. What may come as a bigger surprise, however, is the rally is broadening beyond big technology companies. Let’s examine different measures that prove this point.

Optimism grows among small businesses

Small businesses are becoming more optimistic, a positive indication at a time when economists are debating whether growth will slow. We view this confidence as a positive signal for future growth.

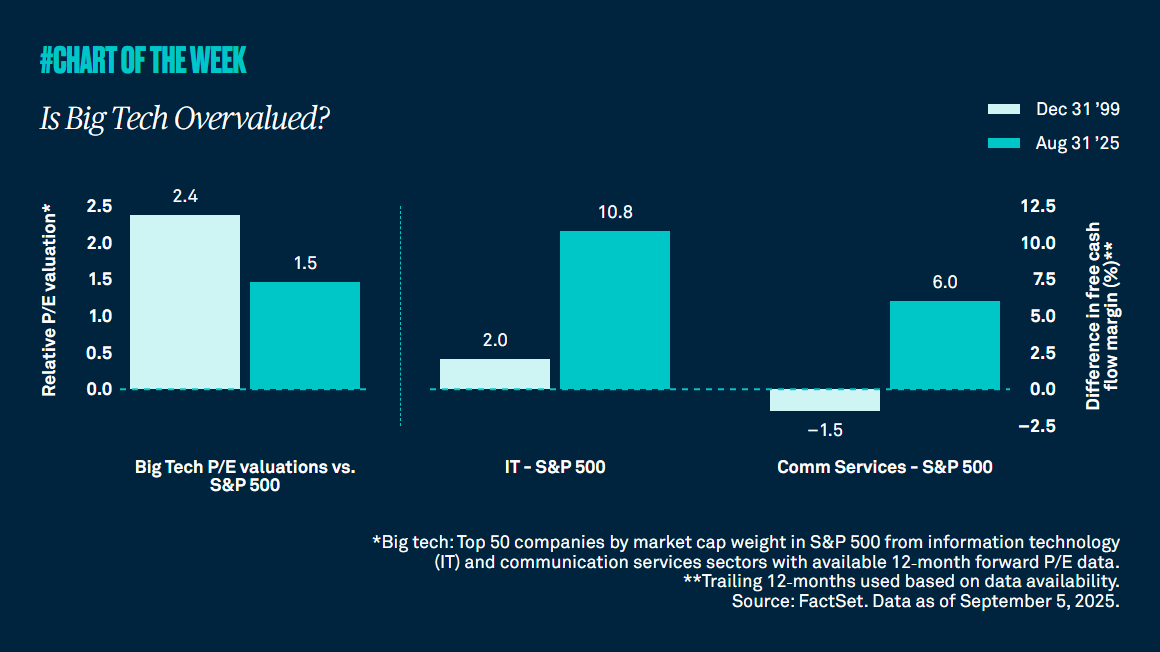

Is Big Tech Overvalued?

It’s true that the S&P 500 currently exhibits high valuations, with the technology sector alone comprising over 40% of its market capitalization and driving concerns about valuations. Are those high multiples justified?

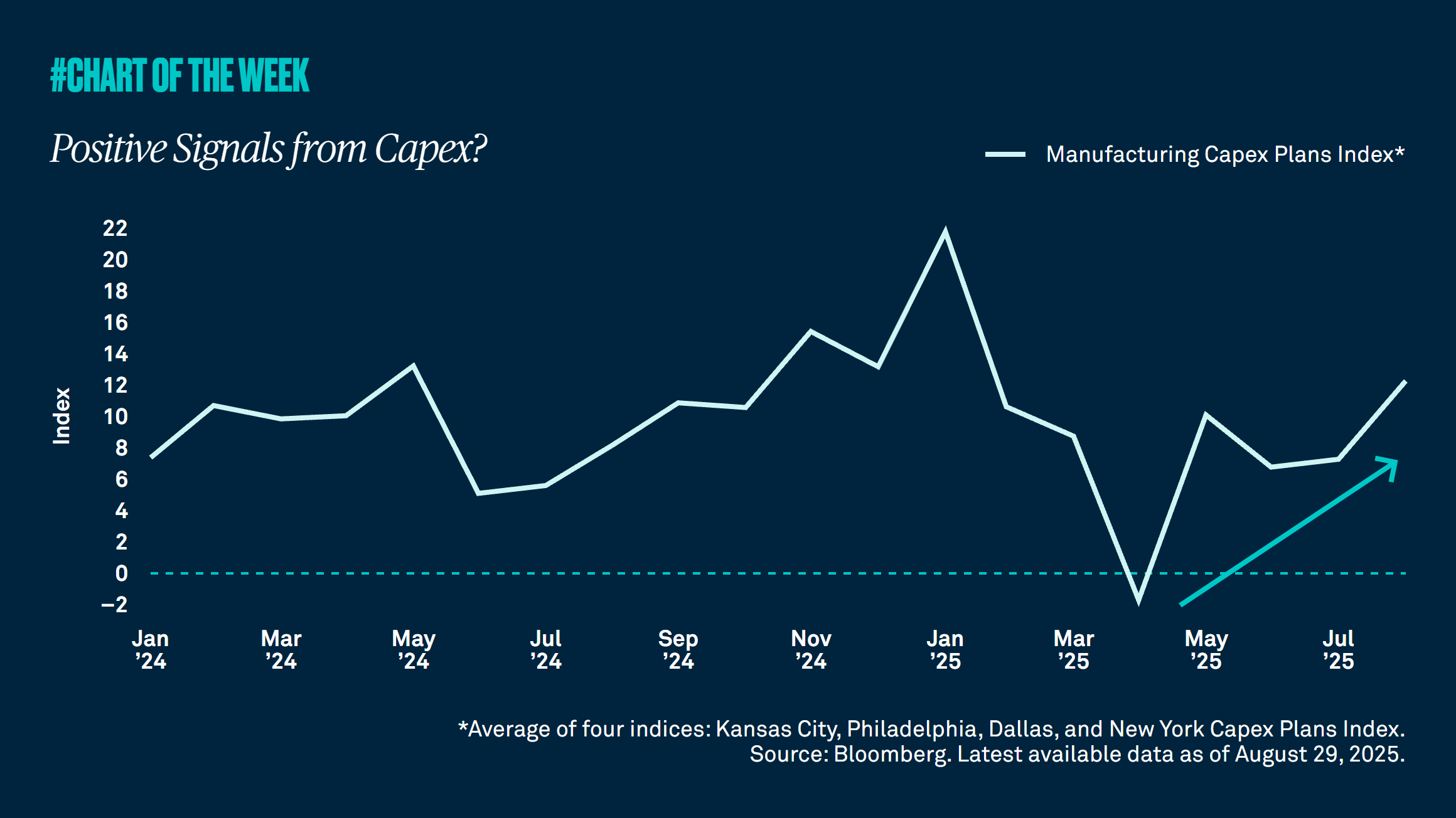

Positive signals from capex?

The One Big Beautiful Bill Act’s provision regarding the full expensing of capital expenditures is already having an impact on companies’ investment plans. We believe this a positive signal for economic growth.

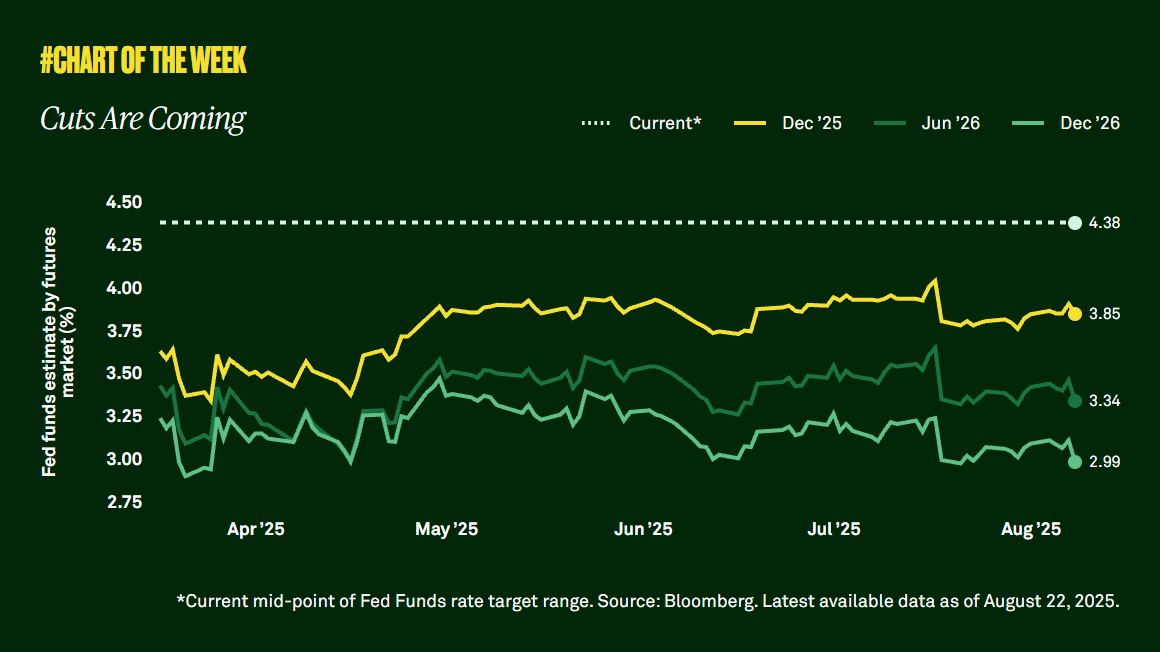

Cuts Are Coming

Last Friday, Federal Reserve Chair Jerome Powell described a shift in the balance of employment and inflation risks, and the market rallied on the news. For us, nothing has changed. We have been closely monitoring the labor market and indicators of inflation, and we continue to expect two rate cuts this year.

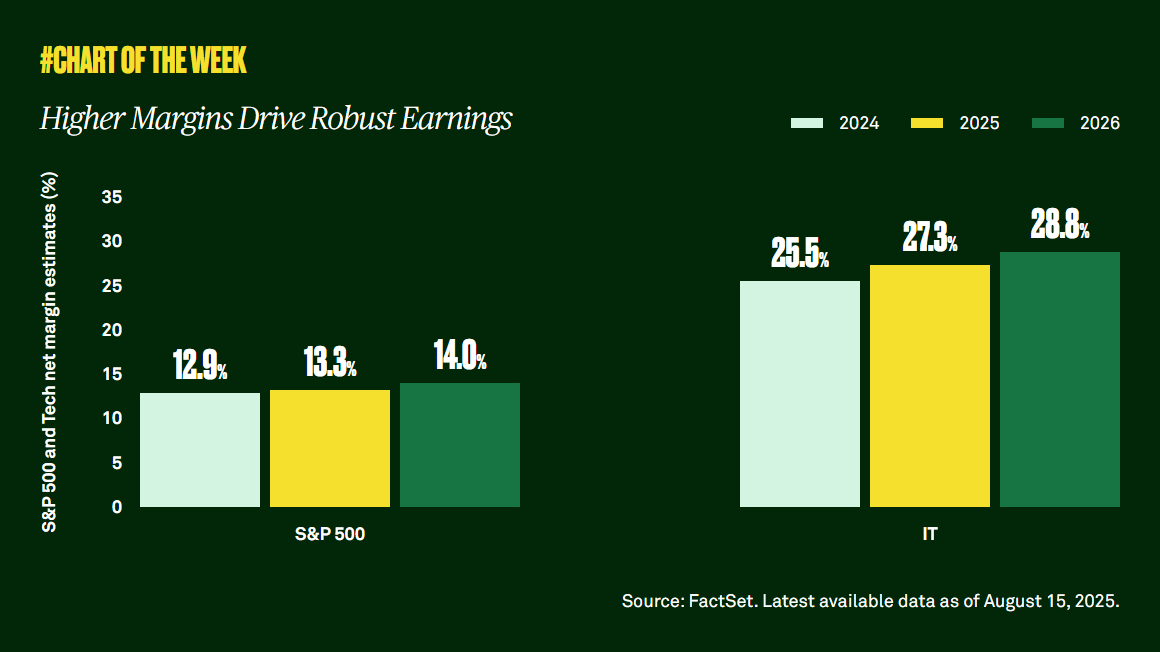

Higher Margins Drive Robust Earnings

Second quarter earnings season is winding down. Nearly all companies have reported, and the majority beat expectations as margin estimates continue to rise.

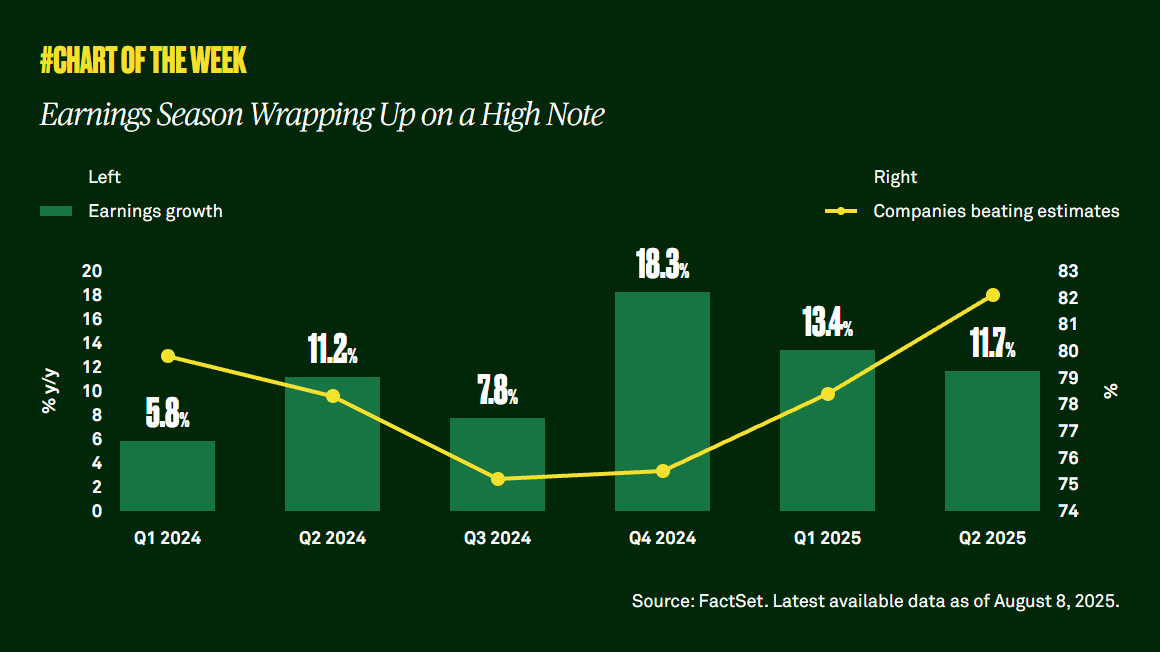

Earnings season wrapping up on a high note

Second quarter earnings season is winding down, but earnings are up, and better than expected. Despite some potentially concerning signals from the real economy, including muted job gains, and possible seasonal volatility, we remain constructive on equities. A positive second quarter earnings season strengthens our conviction.

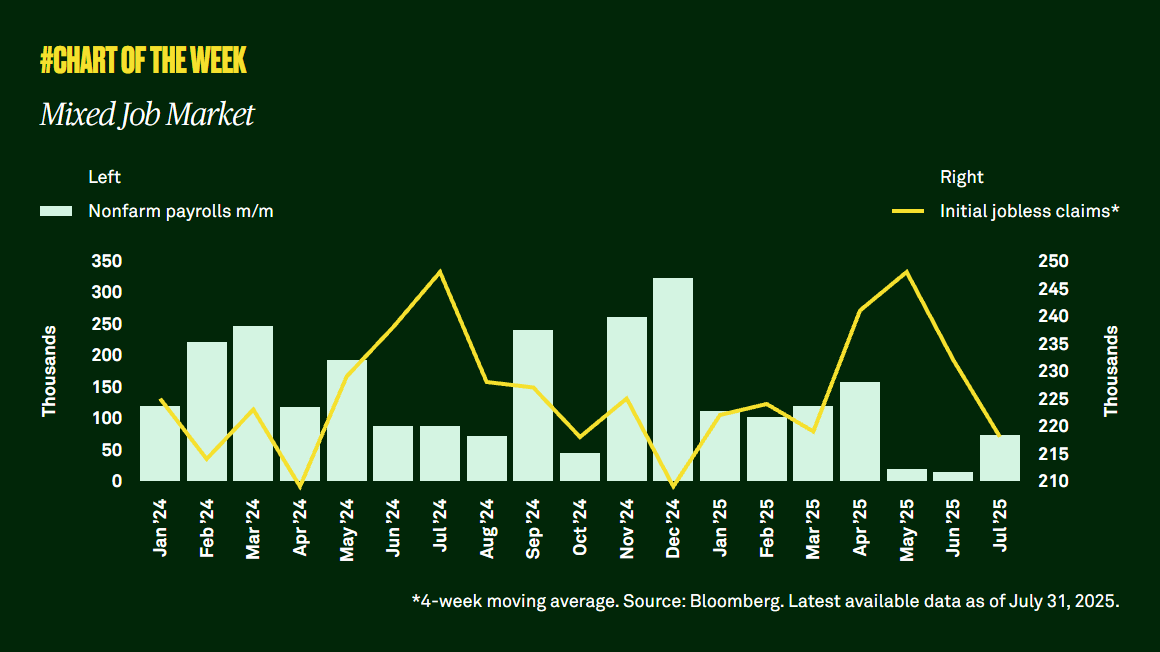

Mixed Job Market

Last week the market received mixed messages about the condition of the labor market. Nonfarm payrolls came in lower than expected, and the previous two months of data were revised sharply lower. Yet initial jobless claims were also lower, and the unemployment rate remains in range. We believe the U.S. economy can still deliver modest growth this year.

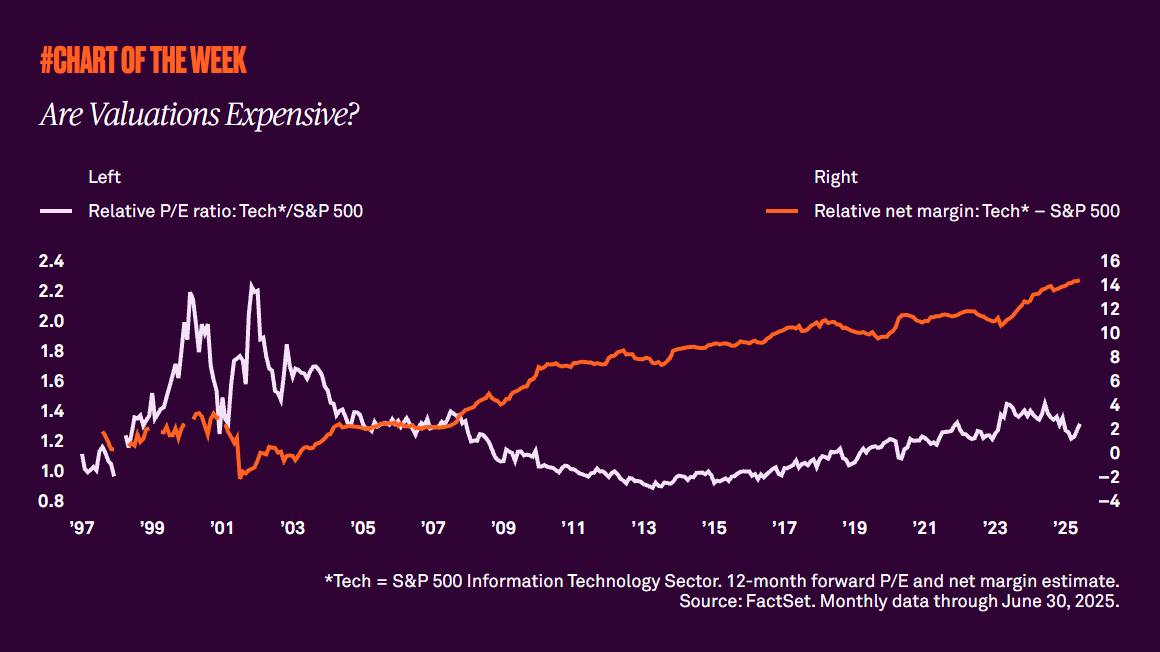

Are valuations expensive?

This year has been characterized by policy uncertainty and fears about the potential impact of tariffs on inflation. While many expected the consumer would crack amid weaker sentiment, it hasn’t happened yet. Retail sales remain resilient, supported by a job market that remains good enough to support spending.

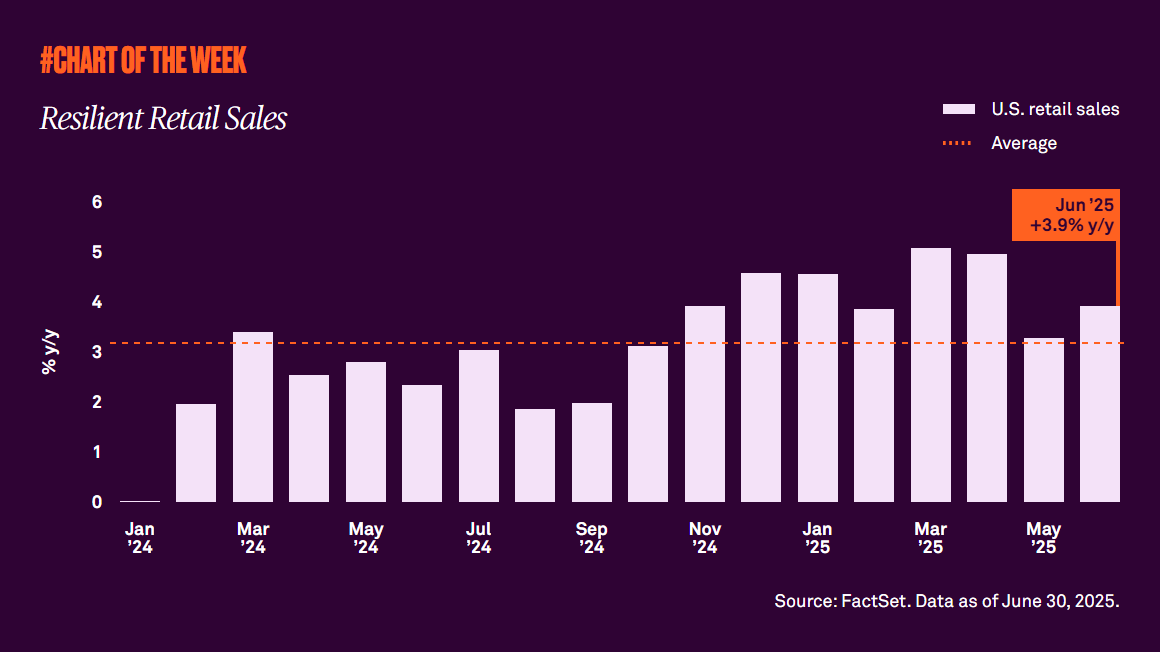

Resilient retail sales

This year has been characterized by policy uncertainty and fears about the potential impact of tariffs on inflation. While many expected the consumer would crack amid weaker sentiment, it hasn’t happened yet. Retail sales remain resilient, supported by a job market that remains good enough to support spending.

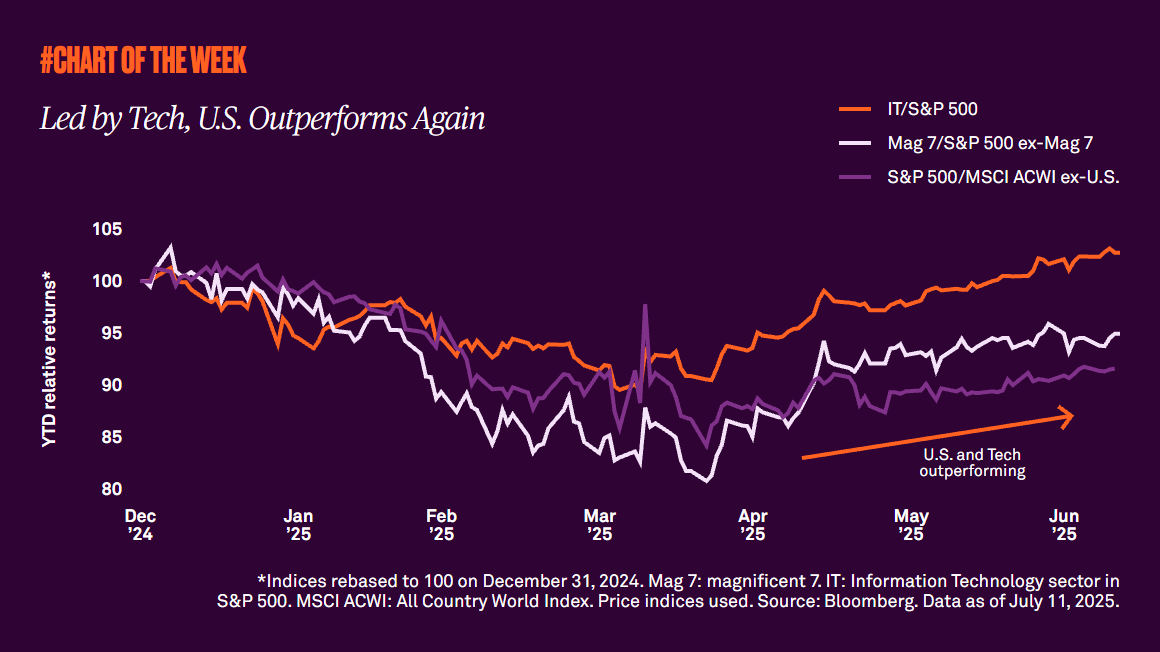

Led by Tech, U.S. Outperforming Since mid-April

After years of outperformance, the U.S. underperformed other regions during the first quarter. While the debate over whether U.S. exceptionalism can persist continues, the U.S. has resumed its leadership since mid-April - led by the technology sector.

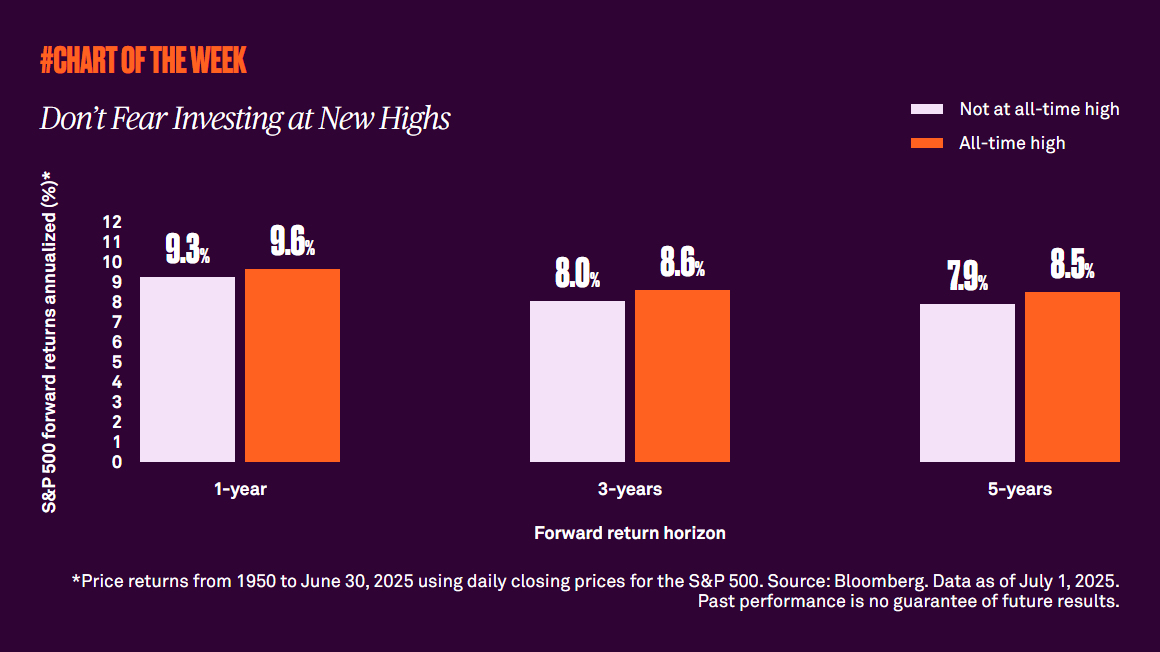

Don’t Fear Investing at New Highs

The S&P 500 recently hit another all-time high. Is it therefore time to exercise more caution? Not in our view. We see the potential for further upside, and history is on our side.

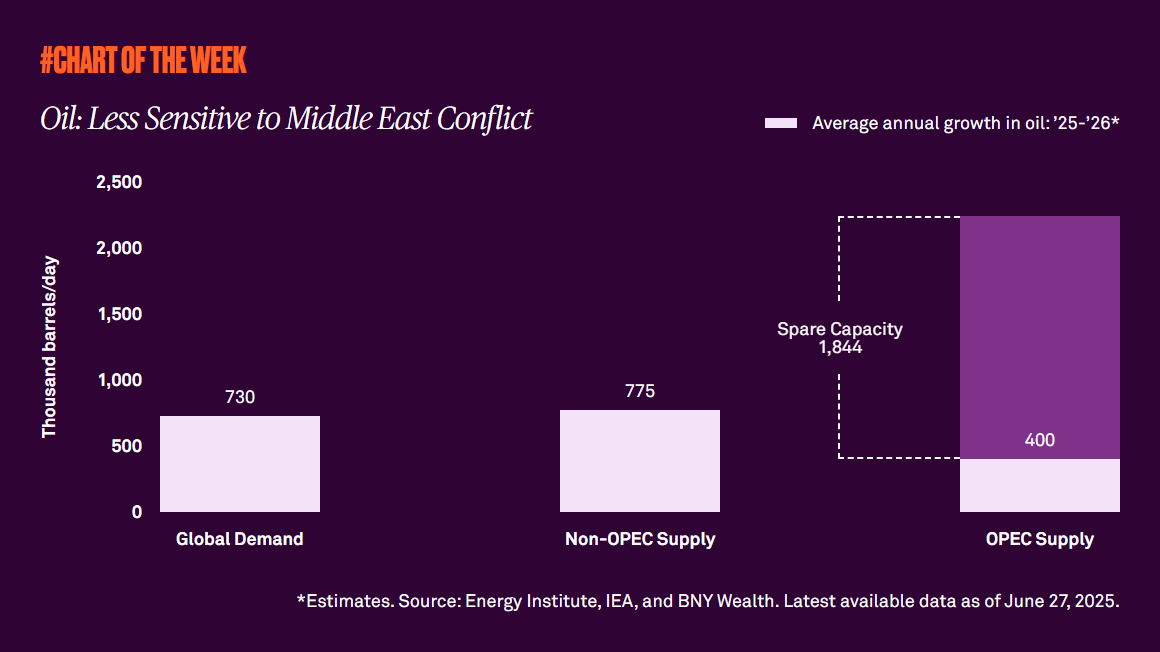

Oil: less sensitive to middle east conflict

The recent Middle East conflict sparked concerns surrounding Iran’s oil supply and the impact it could have on oil prices and the current disinflation trend. However, the price of oil is now at the level it was before the first strike on Iran. Due to the shale revolution, the oil market is ruled by new dynamics.

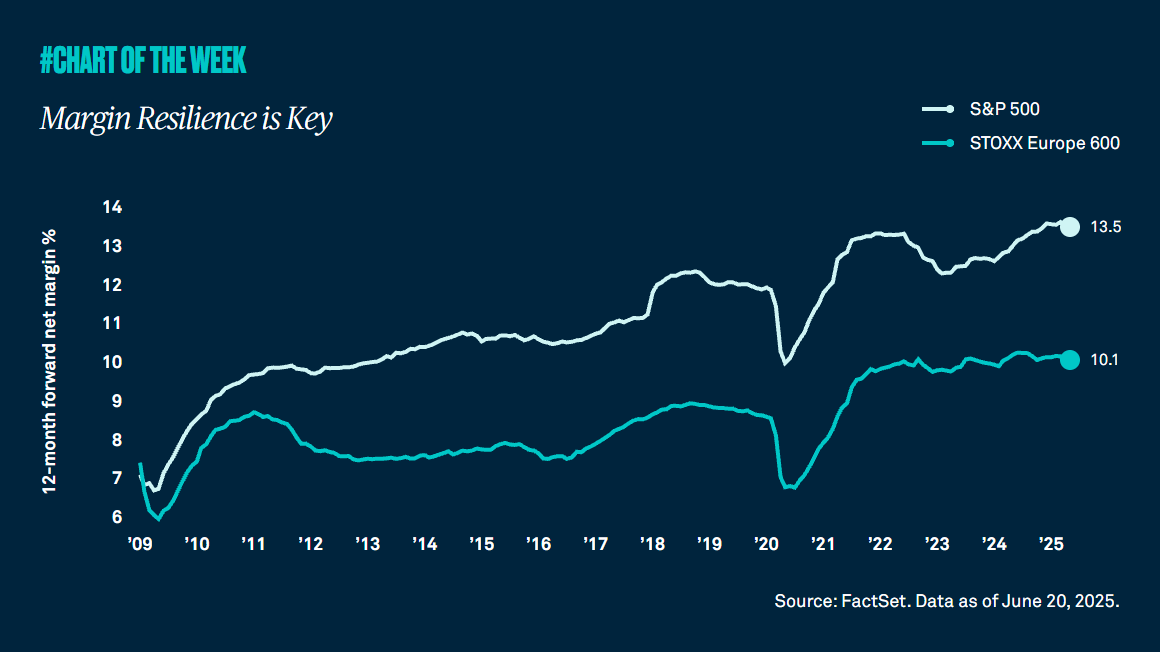

Margin Resilience Is Key

This year U.S. equities have underperformed the rest of the world due largely to policy uncertainty. However, an important driver of U.S. equity outperformance over the longer term has been stronger earnings and profit margins relative to peers, and our view is these factors will continue to drive long-term U.S. exceptionalism.

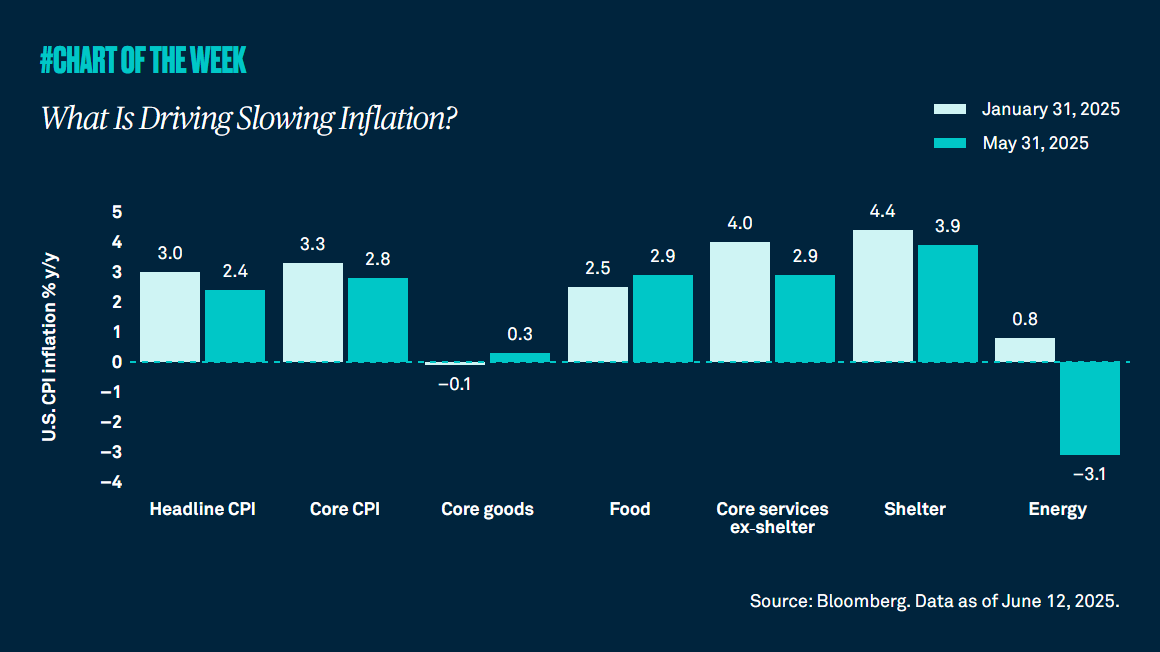

What Is Driving Slowing Inflation?

Inflation came in cooler than expected in May. In fact, it’s down from January’s growth rate of 3.0% year over year to 2.4%. While stickier services components such as shelter have driven this decline, could the recent uptick in oil prices and higher tariffs pose headwinds?

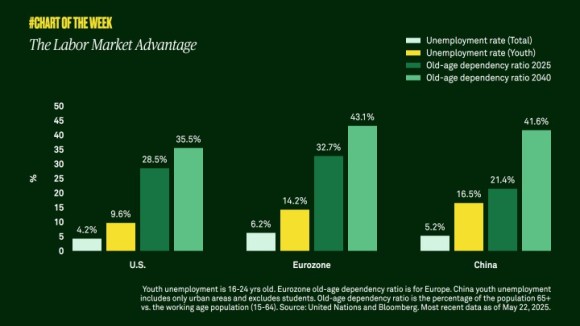

The labor market advantage

The labor market is an important consideration when evaluating the economic growth prospects of a country. In the U.S., unemployment and demographics metrics look favorable compared to other major economies.

A “Good Enough” Job Market

By no measure are we seeing a booming job market, but we are also not seeing a deteriorating one. In fact, current labor metrics lead us to conclude that the job market remains “good enough” to support our economic growth expectations for the year.

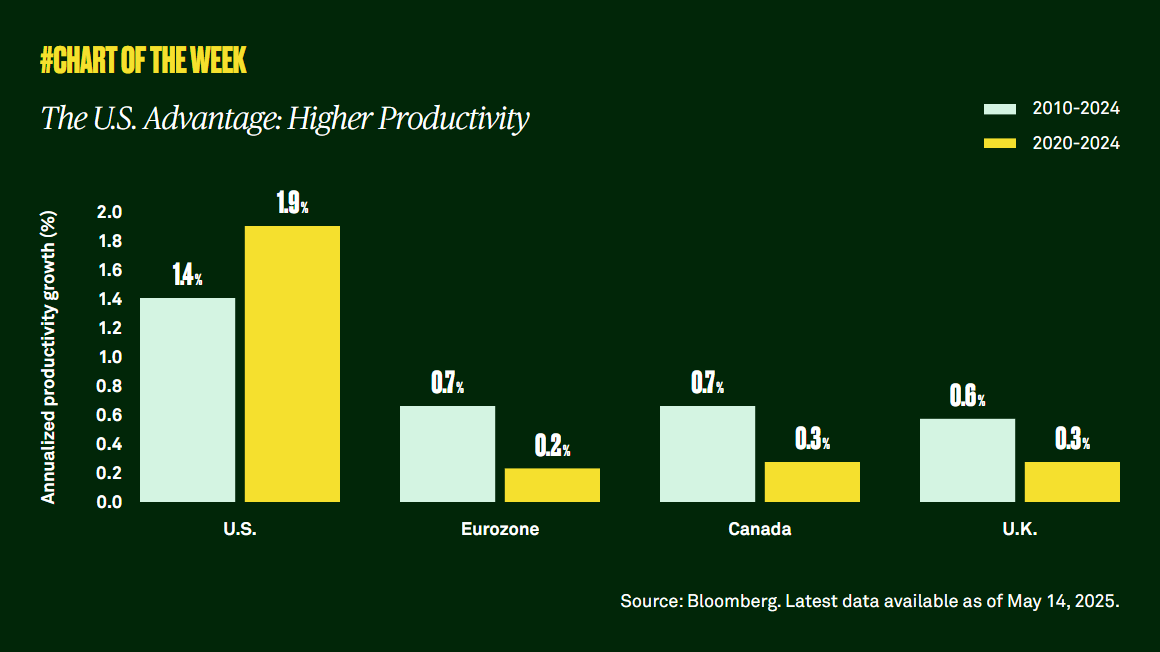

The U.S. Advantage: Higher Productivity

Lately, non-U.S. equities are outperforming the U.S. Is U.S. exceptionalism dead? Productivity growth tells a more positive story.

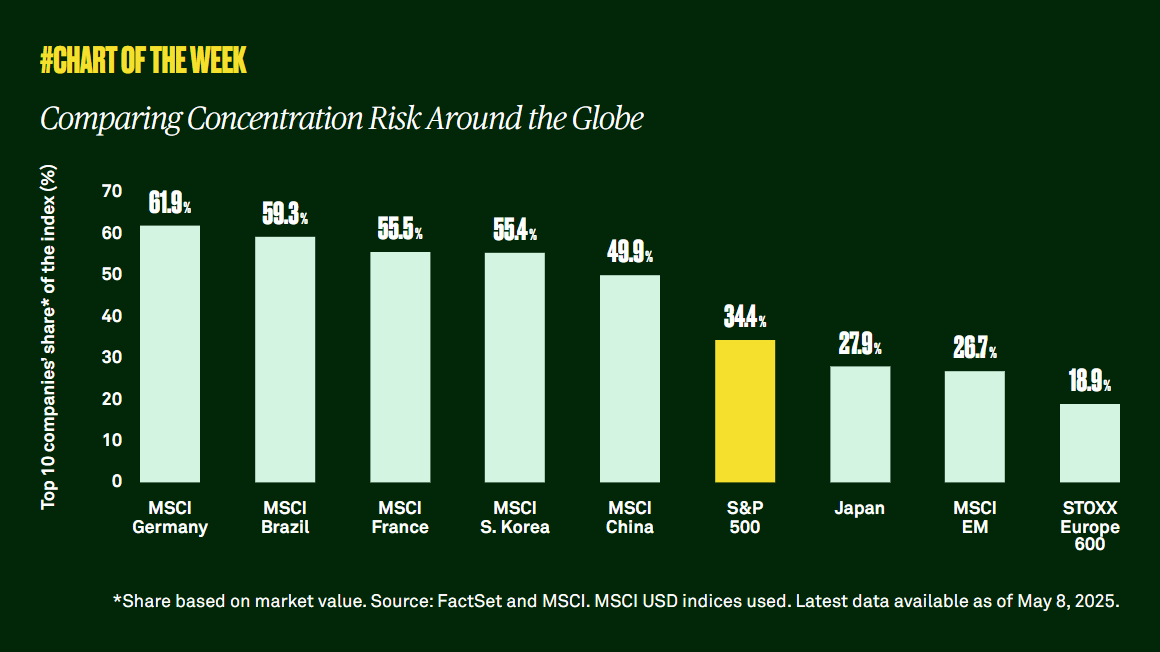

Comparing concentration risk around the globe

While some fear the S&P 500 is too concentrated in its top 10 stocks, our analysis tells us something different.

U.S. exceptionalism expected to prevail

International equity markets are outperforming the U.S. year to date. Is this a durable trend? According to relative earnings growth, the U.S. still has an advantage.