OUTLOOK

6 FOR 2026

Essential Questions for Investors

OUTLOOK

6 FOR 2026

Essential Questions for Investors

6 For 2026

Investors are navigating markets that feel familiar yet fundamentally different. Growth is uneven but still has room to run. AI is transforming productivity, yet its impact on profits is still being tested. Meanwhile, rates across the globe are moving in different directions.

In uncertain times, asking good questions matters as much as good answers. We tackle six questions that may shape 2026.

BNY Investments

DISCOVER HOW WE CAN HELP INVESTORS

We believe markets are positioned for growth in a supportive, but increasingly multi-dimensional, environment.

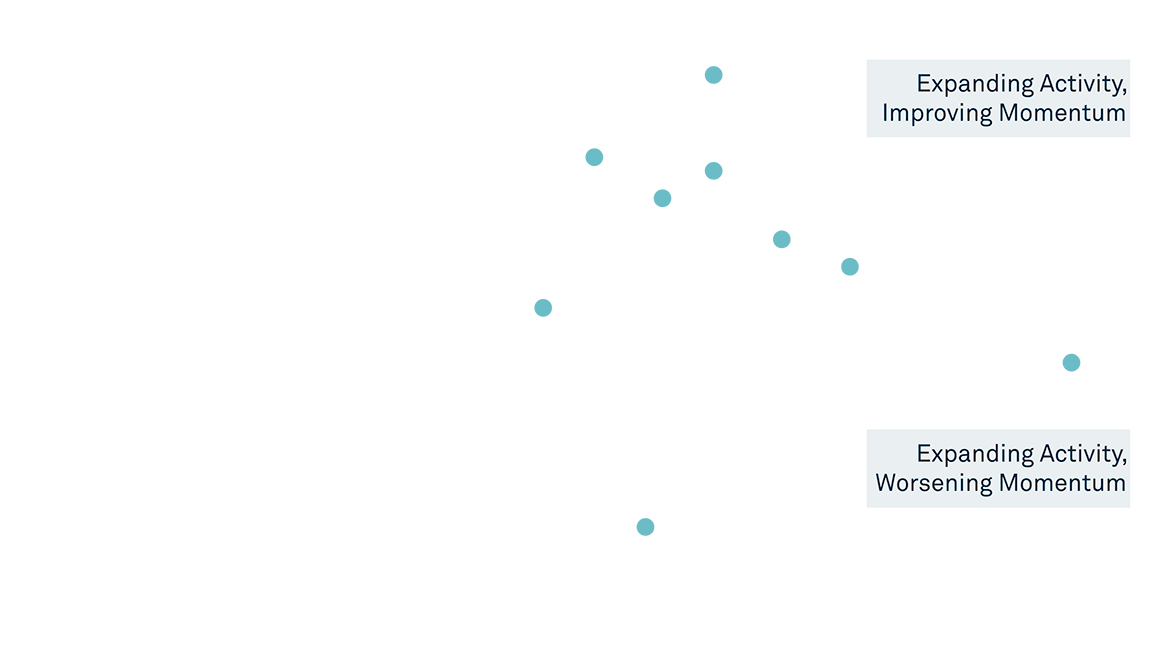

We see forces balancing toward growth re-acceleration, with support from fiscal and monetary policies. U.S. growth is expected to lead in 2026, as the Federal Reserve (Fed) eases and fiscal actions gain traction. Europe should expand modestly, driven by Germany’s fiscal stimulus and improving real incomes. China’s recovery could remain uneven amid property-sector strain and deflation pressures.

Overall, the economy looks primed for a steady advance against a firmer economic backdrop, which also continues to shift. We remain optimistic and will closely watch the evolving signals.

Sources: BNY Investments, Macrobond, as of October 28, 2025. The Purchasing Managers’ Index (PMI) is a monthly economic indicator that measures the health of the manufacturing and services sectors, based on surveys of purchasing managers. A score above 50 indicates economic expansion, while a score below 50 signifies contraction, and 50 represents no change.

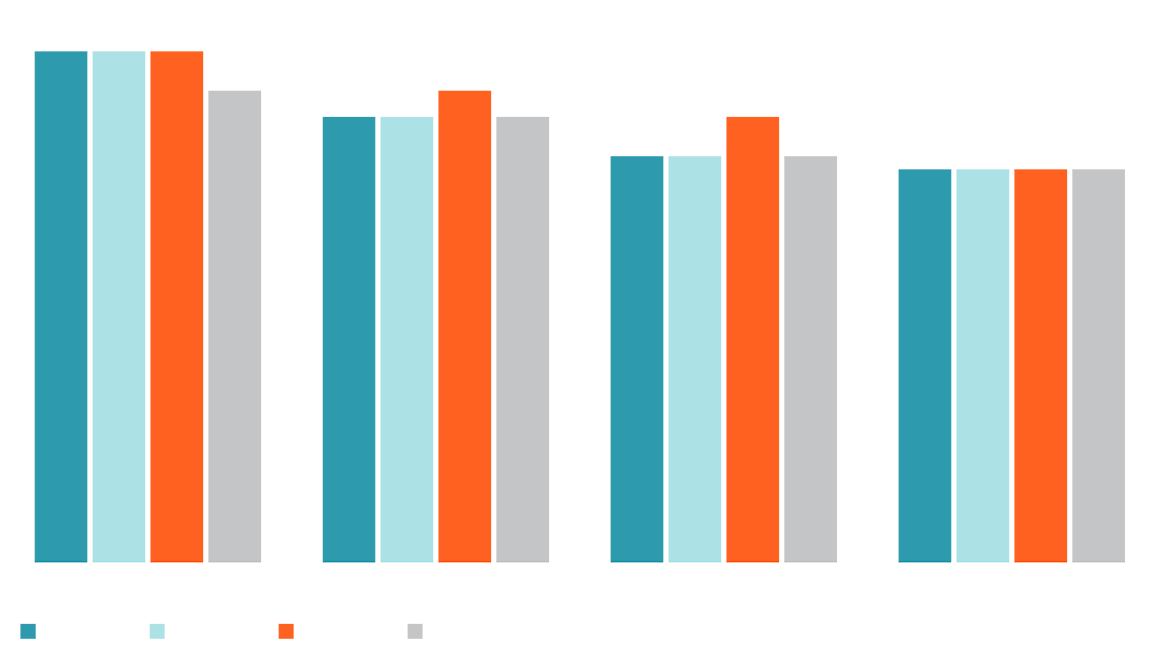

With U.S. inflation projected to be just modestly above target, the Fed will likely emphasize supporting employment and growth, though upcoming board changes could affect the size and speed of rate cuts. The Fed will likely keep cutting rates next year until the economy and financial markets stop it, bringing the lower bound of the range to 2.5% by 2027.

The European Central Bank may ease slightly, while the Bank of England and Bank of Japan are likely to firm policy rates, with the latter negotiating a complicated government transition that leaves it open to domestic political pressure.

Sources: Federal Reserve, Summary of Economic Projections, at https://www.federalreserve.gov/monetarypolicy.htm various quarters. Calculations by BNY Investments, October 24, 2025.

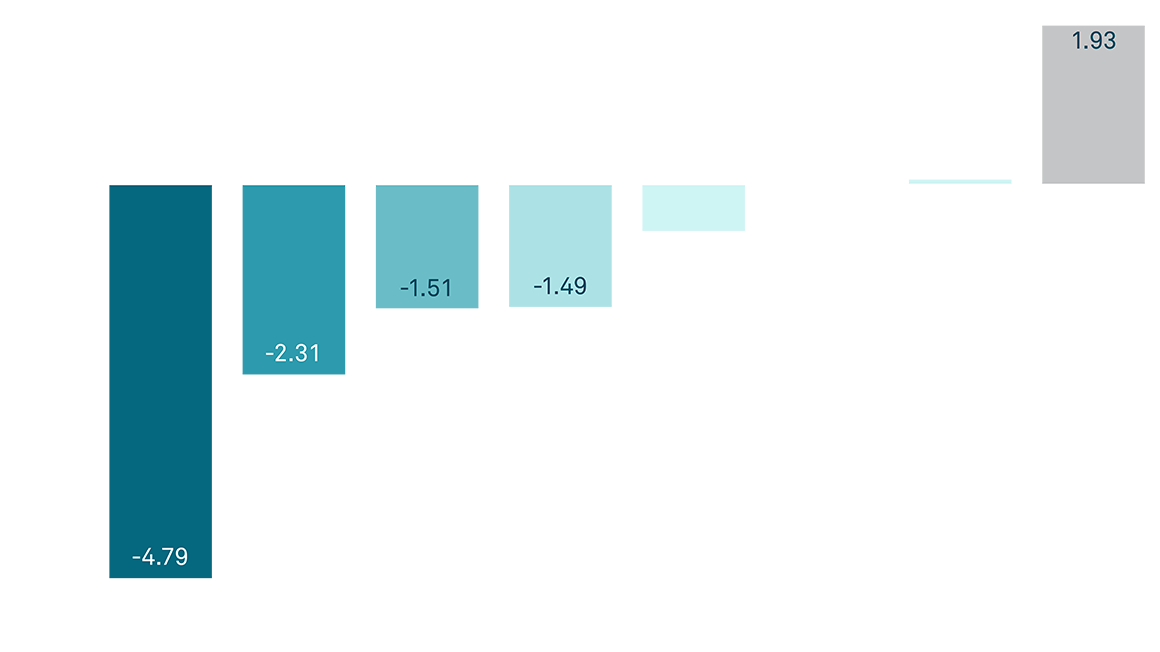

After years of synchronized easing, monetary paths now vary. This dispersion is creating new opportunities in fixed income but also demands a more selective approach. In the U.S., the Fed’s renewed rate cuts and fiscal expansion could support front-end Treasuries and high-quality credit, though long-end risks remain.

The European Central Bank faces uneven growth and fiscal strain, especially in France where widening deficits and political gridlock over deficits make a resolution difficult. The Bank of England is navigating stubborn inflation and wage growth. Most countries in Latin America and Asia are in the process of cutting rates while retaining policy flexibility in case growth momentum slows.

Opportunities are becoming more idiosyncratic and investors who stay nimble and selective across regions, duration and credit quality may be well positioned to capture them.

Sources: BNY Investments, Macrobond. Data as of October 28, 2025.

As the world continues to shift toward a multi-polar balance of power, we think multiple reserve currencies will be used for trade finance, payments and store of value. As fiscal vulnerabilities across developed economies weigh on major currencies, the U.S. dollar’s safe haven status is on softer footing. We think investors will increasingly hedge their U.S.-dollar exposure. Demand for U.S. assets will also matter. Overseas investors are generally underweight the U.S., and given our view for U.S.-led growth in 2026, it is likely they may increase their exposure to U.S. assets while actively managing the currency exposure.

Sources: BNY, as of October 10, 2025.

We see today’s valuations as part of a higher-multiple environment supported by stronger profitability and a larger index weight to tech. Economic and earnings growth remain resilient, with global earnings revisions trending higher and profitability broadening beyond big tech. Rising productivity and ongoing AI adoption should further reinforce record-level margins and long-term earnings growth. In our view, higher valuations reflect stronger fundamentals.

Sources: BNY Investment Institute, Bloomberg.

AI lowers the cost of accessing and transforming information, reducing the scarcity that underpins information-based competitive advantages. As a result, sectors whose advantages stem from physical assets, regulatory barriers or network effects may find their advantages preserved, and AI-related productivity gains in these sectors could more likely accrue to shareholders.

At the same time, AI’s impact extends beyond productivity to demand — as prices fall, more consumers can access previously out-of-reach goods and services. This dynamic may unlock new markets and drive broader profitability. AI’s winners will be firms that convert technological efficiency into enduring demand and durable market power.

Sources: Oxford Economics and BNY Investments. Data as of August 31, 2025.

Key Takeaways

Markets are positioned for broader growth, creating opportunities across countries, sectors and currencies.

A sharp pivot to meet power-hungry AI workloads supports infrastructure, energy and metals.

Profitability and productivity should drive a higher-multiple environment and broader earnings growth.

Divergent central bank policies open sources of yield and return in global fixed income.

Easing central banks, China’s growth stimulus, and U.S. dollar weakness make EM assets attractive.

BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally. This material and any products and services mentioned may be issued or provided in various countries by duly authorized and regulated subsidiaries, affiliates, and joint ventures of BNY. This material does not constitute a recommendation by BNY of any kind. The information herein is not intended to provide tax, legal, investment, accounting, financial or other professional advice on any matter, and should not be used or relied upon as such. The views expressed within this material are those of the contributors and not necessarily those of BNY. BNY has not independently verified the information contained in this material and makes no representation as to the accuracy, completeness, timeliness, merchantability or fitness for a specific purpose of the information provided in this material. BNY assumes no direct or consequential liability for any errors in or reliance upon this material.

This material may not be reproduced or disseminated in any form without the express prior written permission of BNY. BNY will not be responsible for updating any information contained within this material and opinions and information contained herein are subject to change without notice. Trademarks, service marks, logos and other intellectual property marks belong to their respective owners.

© 2025 The Bank of New York Mellon. All rights reserved. Member FDIC.