Good news on inflation?

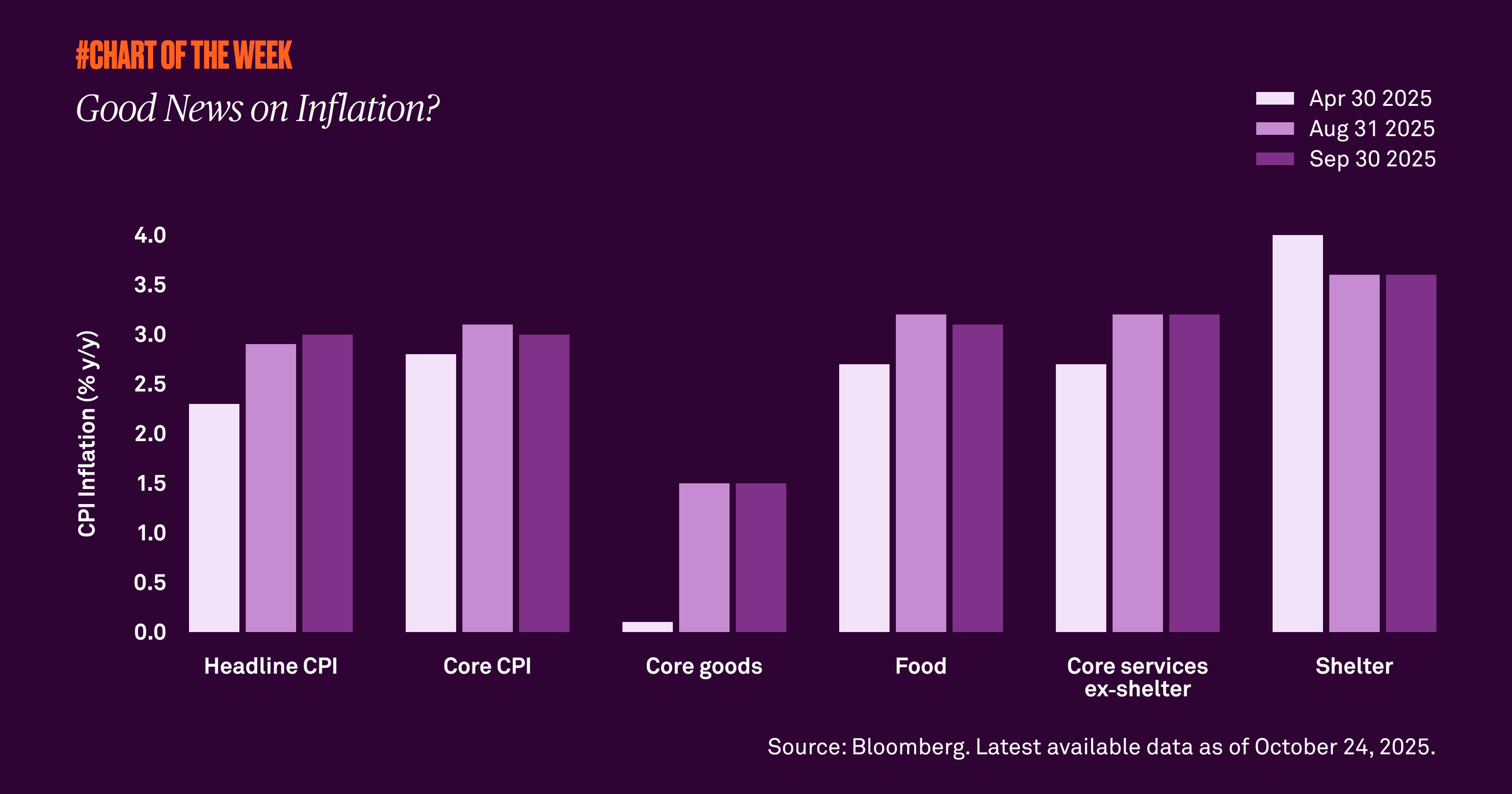

Last week’s Consumer Price Index report, a widely used indicator of inflation in the U.S. economy, showed growth of 3% in September, which was above 2.9% in August but less than expected. Despite the modest increase, various categories have shown signs of stabilization. What does this mean for inflation going forward?

Last week’s Consumer Price Index (CPI) report, a widely used indicator of inflation in the U.S. economy, showed modest growth from 2.9% on an annual basis in August to 3% in September. Yet, the number came in below analysts’ expectations, helping to allay fears of rising inflation. Consequently, the market ended the week higher.

Though the inflation reading was slightly higher than in August, a look at underlying components is encouraging. Core goods, food and core services ex-shelter have risen since April, but appear to have peaked with readings either unchanged or lower in September. Importantly, shelter, which accounts for 35% of CPI, continues to slow, helping to stabilize inflation.

There is the question of what the impact of tariffs will be on inflation once all potential deals are in effect, but we maintain that the result will be a one-time rise in prices rather than a sustained increase. Our view is that inflation will remain within a range of 2.6% to 3.3% through year end.

829871 Exp : 28 October 2026

YOU MIGHT ALSO LIKE

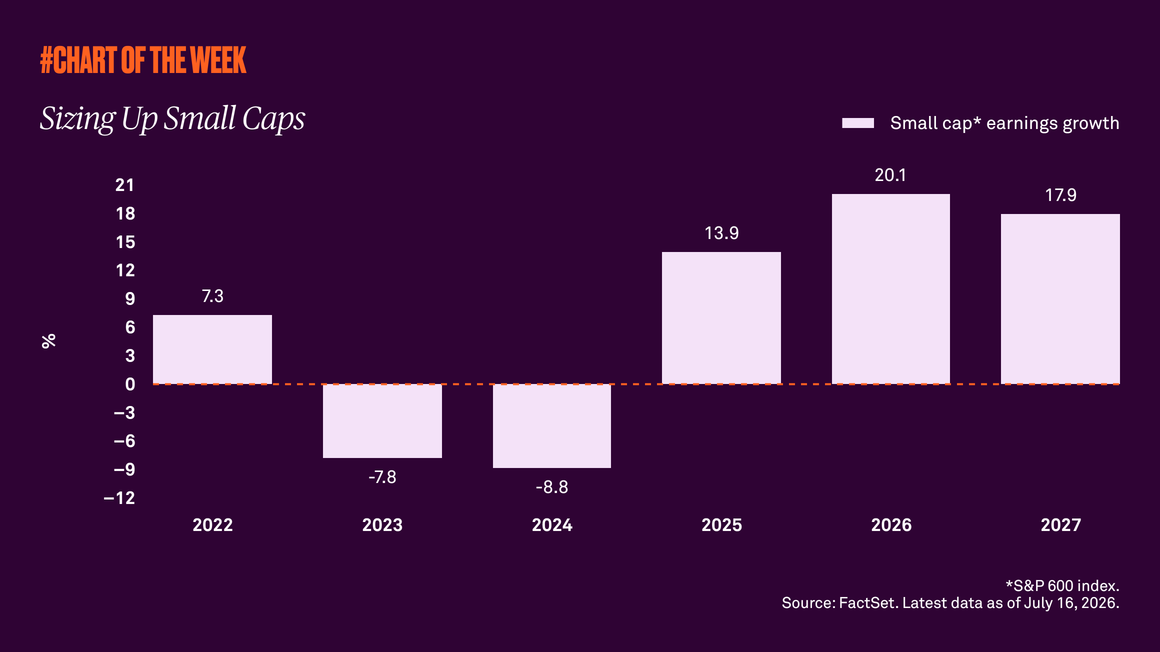

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

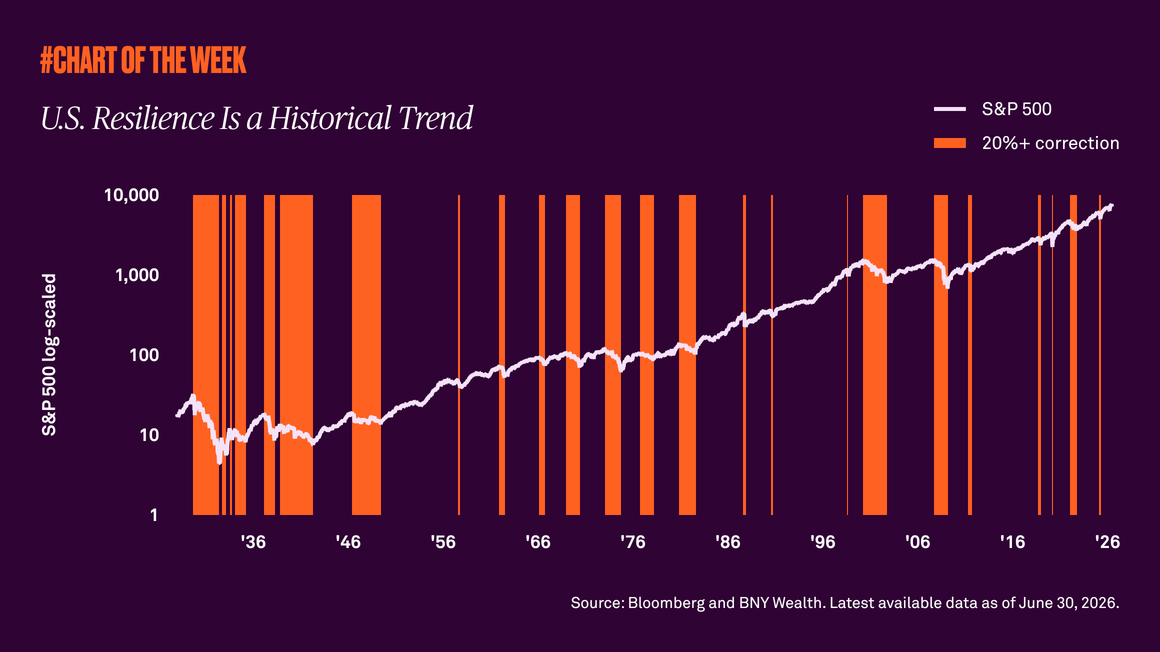

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

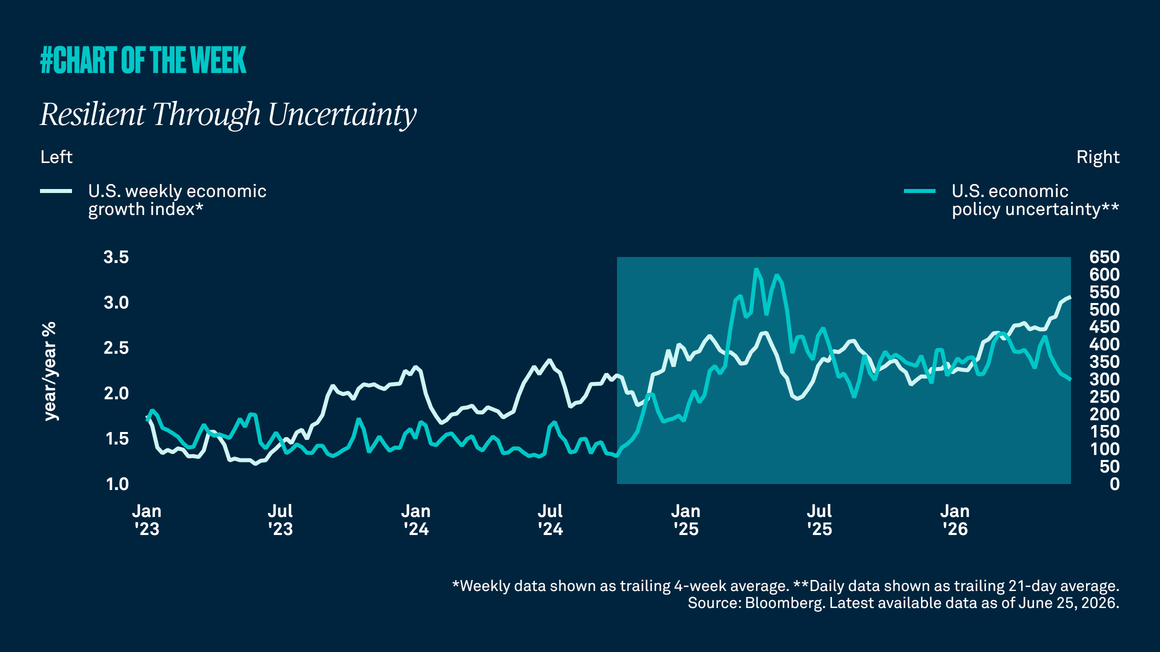

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.