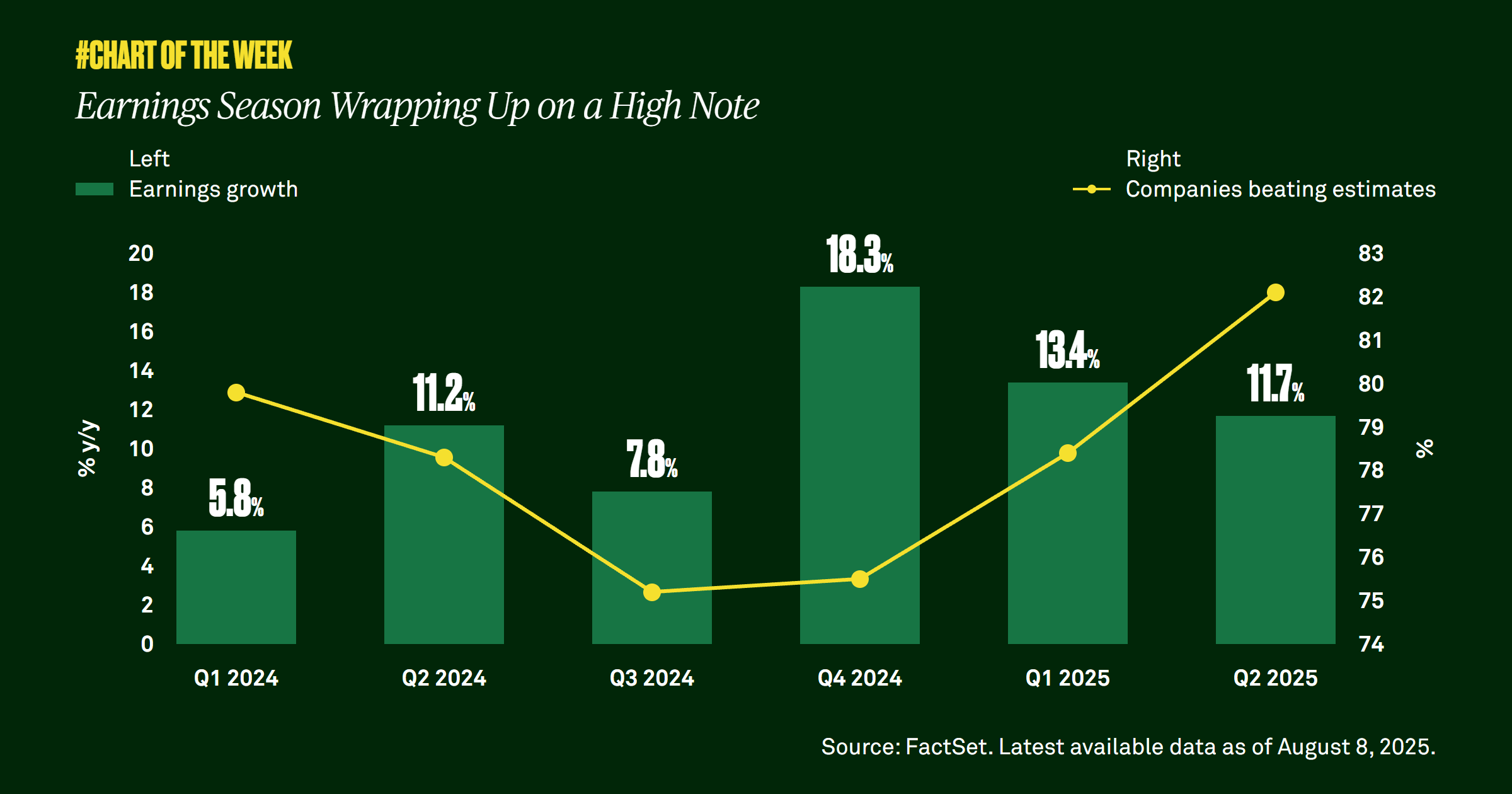

Earnings season wrapping up on a high note

Second quarter earnings season is winding down, but earnings are up, and better than expected. Despite some potentially concerning signals from the real economy, including muted job gains, and possible seasonal volatility, we remain constructive on equities. A positive second quarter earnings season strengthens our conviction.

Second quarter earnings season is winding down, and results have delighted many investors. More than 90% of S&P 500 companies have already reported and 82% beat estimates, the highest rate in four years. Once all data comes in, earnings are expected to have grown 11.7% compared to 4.9% projected at the end of June.

Additionally, estimates for the full year have also improved; consensus estimates call for 10.2% annual earnings growth, up from 8.7% in June. Despite signs of potential weakness in the real economy and job market, earnings have been better than anticipated.

Historically, August and September have been seasonally challenging months, suggesting we could see an increase in volatility in the near term, but the ongoing strength of earnings instills us with confidence in equity performance over the long term. We also remain positive on the artificial intelligence (AI) growth story, which bolstered the results of Magnificent Seven companies this past quarter. The innovation’s benefits are not only affecting technology companies; AI is driving margin expansion and productivity enhancements across many other sectors too, further supporting our constructive stance on the future outlook of the U.S. equity market.

787959 Exp : 11 August 2026

YOU MIGHT ALSO LIKE

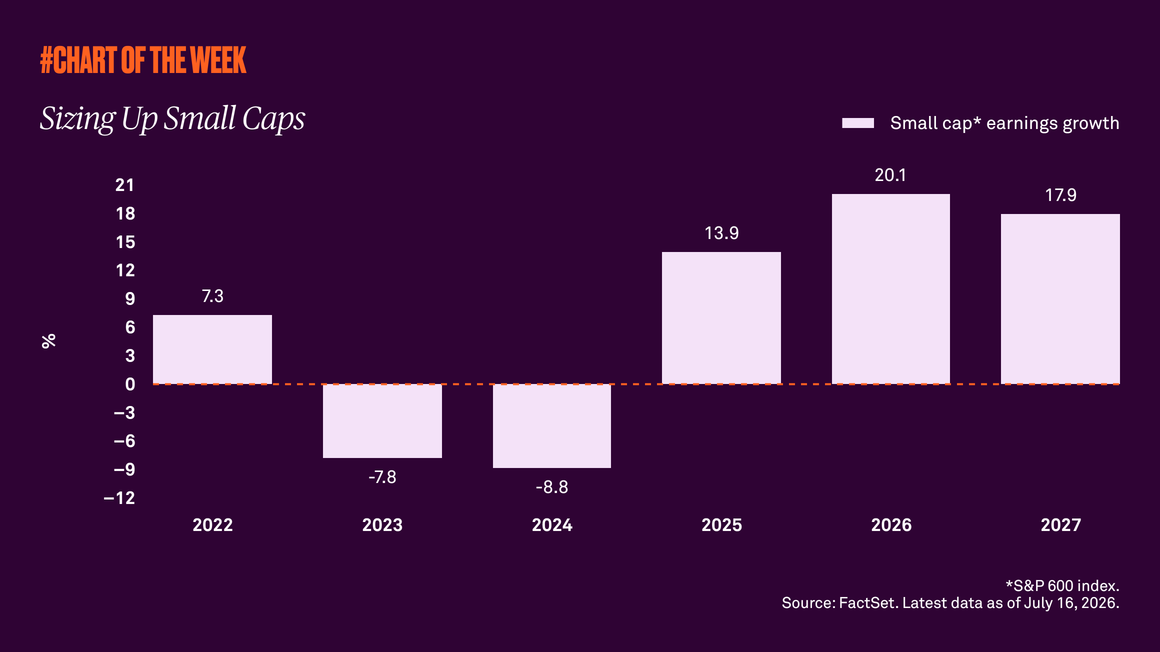

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

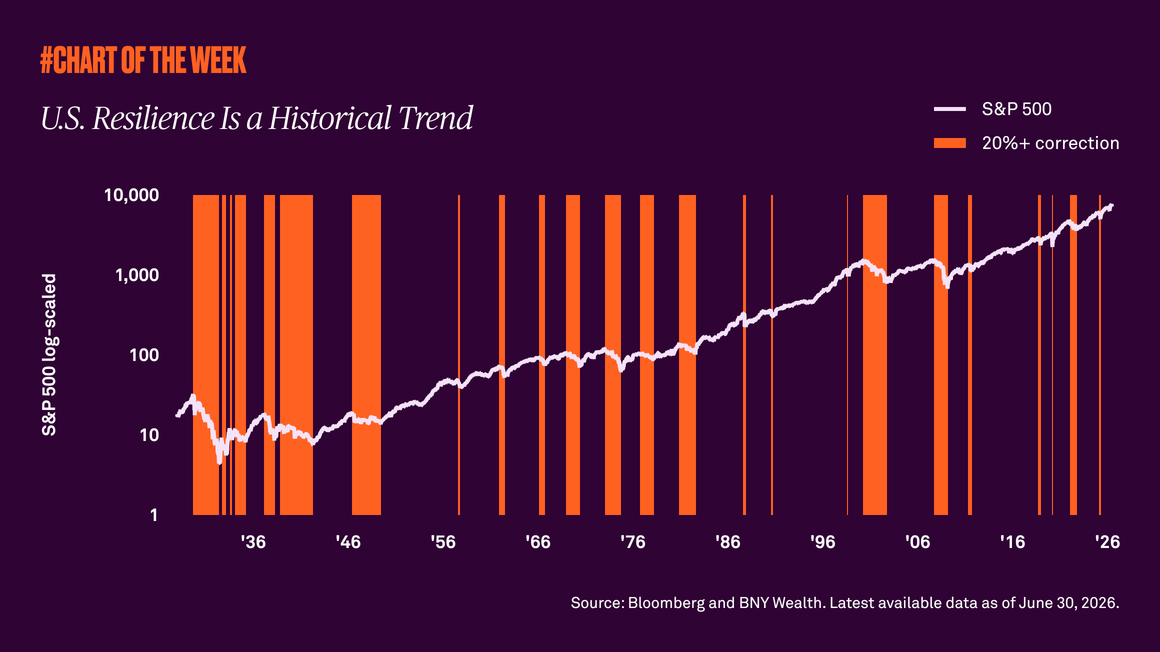

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

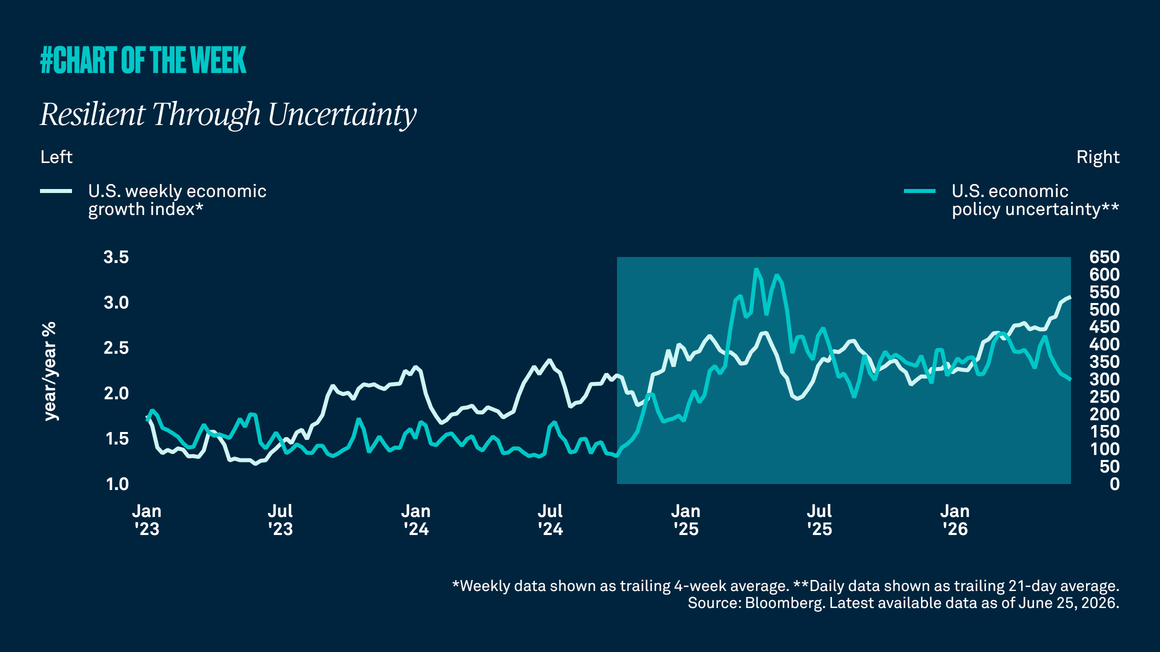

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.