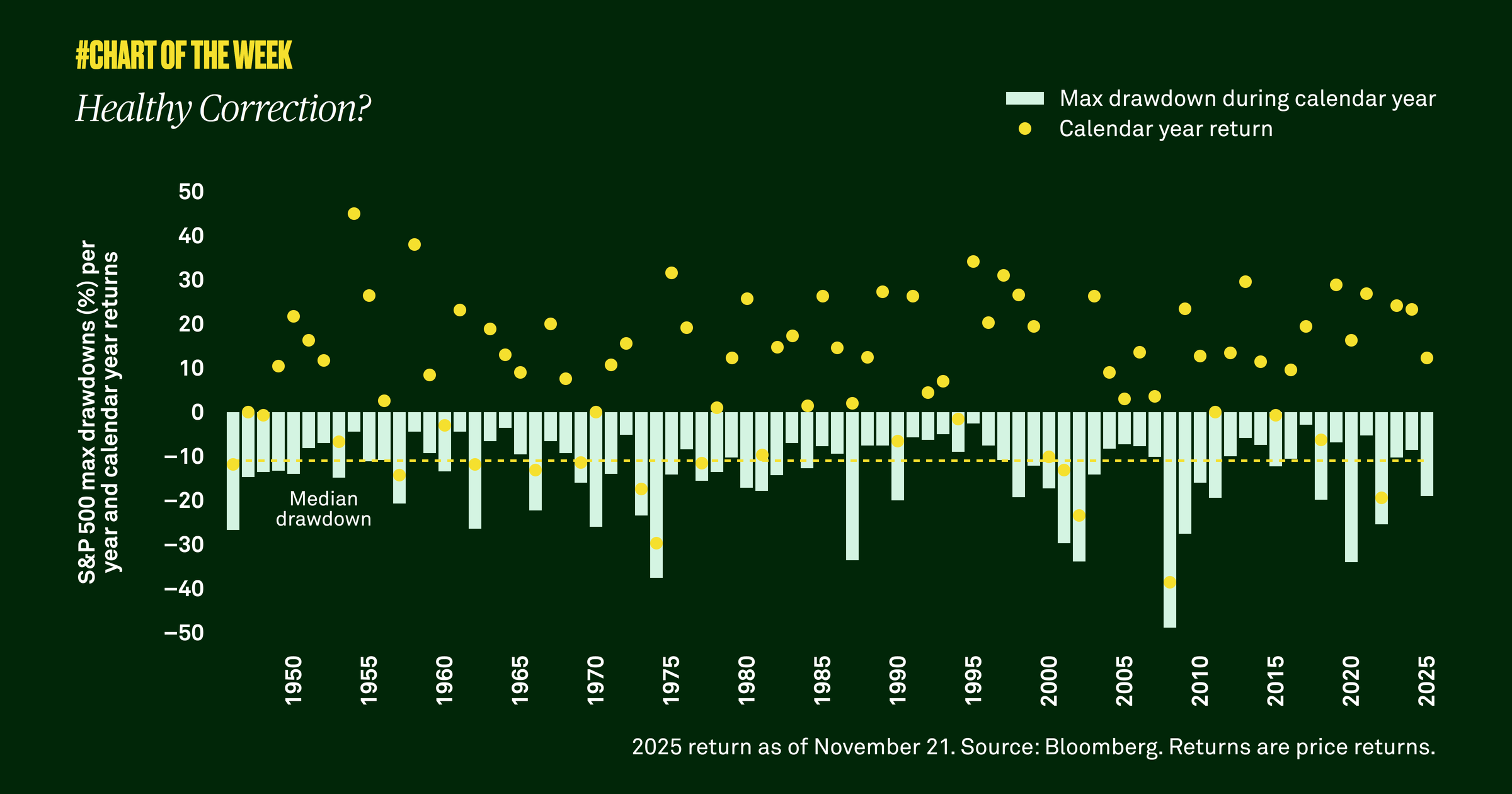

Healthy correction?

After climbing 17% year to date through late October, the S&P 500 declined 5% through November 20. We believe the market was due for a healthy correction. While further downside is possible, it would not concern us.

After reaching a new all-time high on October 28, the S&P 500 declined 5% through November 20, leading to concerns of a renewed correction. We believe the market was due for a healthy correction and while further volatility may persist, additional downside would not concern us.

History shows that markets don’t move in a straight line, and drawdowns are normal. Since 1946, the S&P 500 has experienced a median annual correction of 11%.

Additionally, we do not believe we’re heading for a bear market or imminent recession, and we see the latest decline as more technically driven rather than a change in fundamentals or a more negative outlook. In 2026, we expect economic growth near 2% and earnings growth to continue to broaden beyond the tech sector, which should support equity performance. Therefore, staying invested and weathering the downside is critical for capturing potential upside.

845652 Exp : 25 November 2026

YOU MIGHT ALSO LIKE

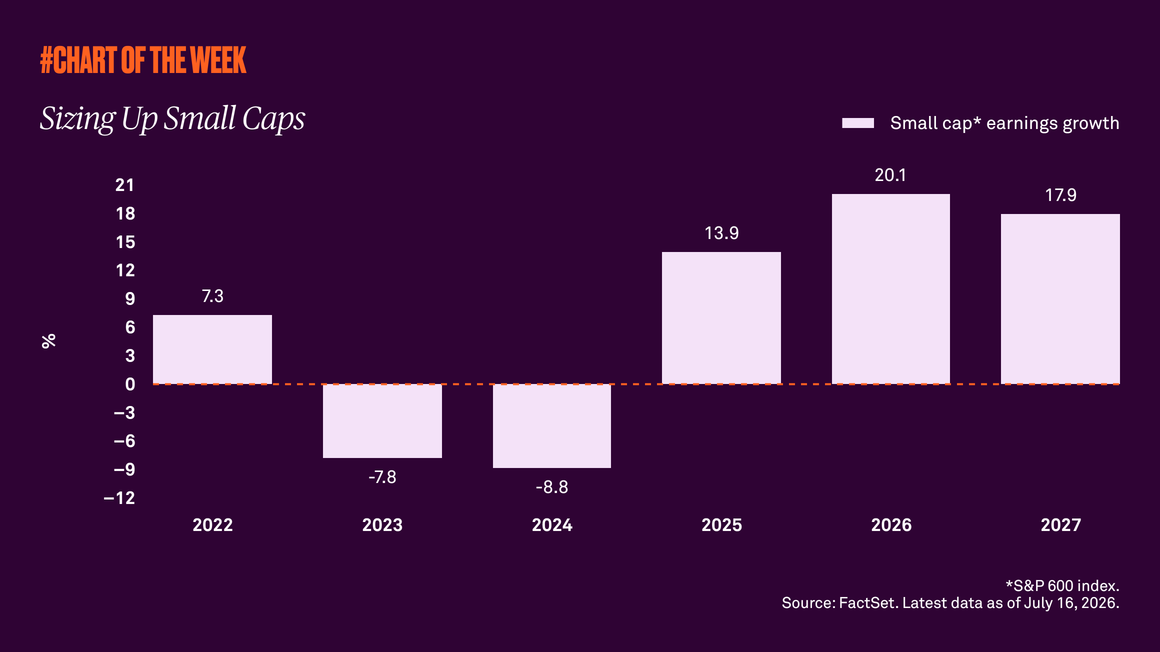

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

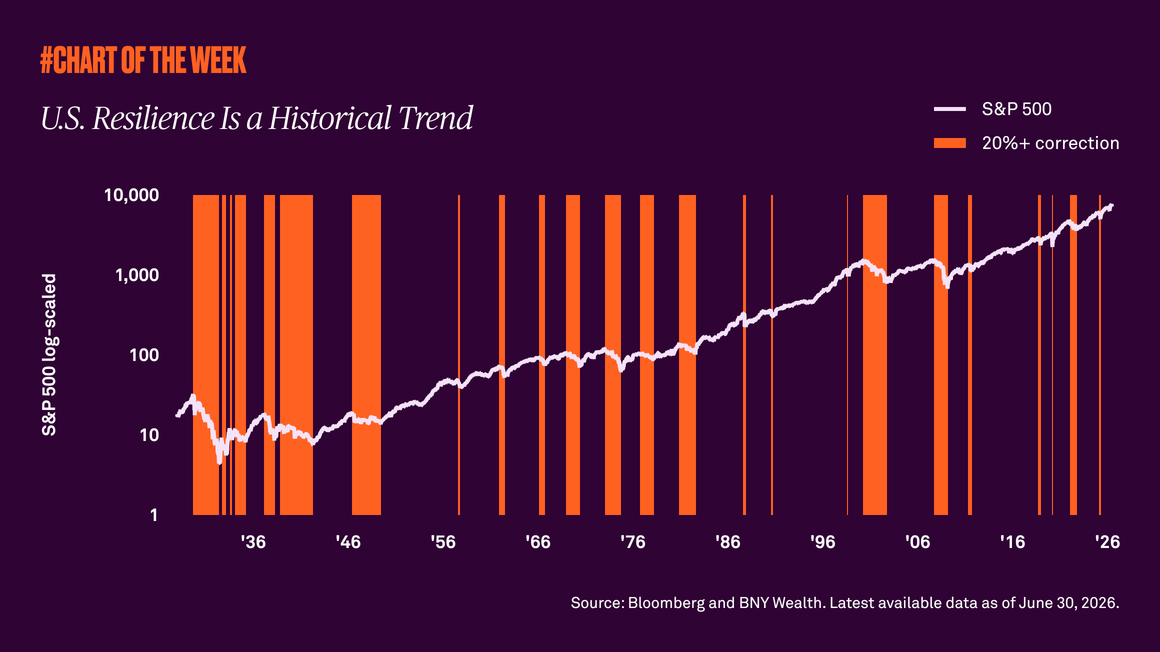

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

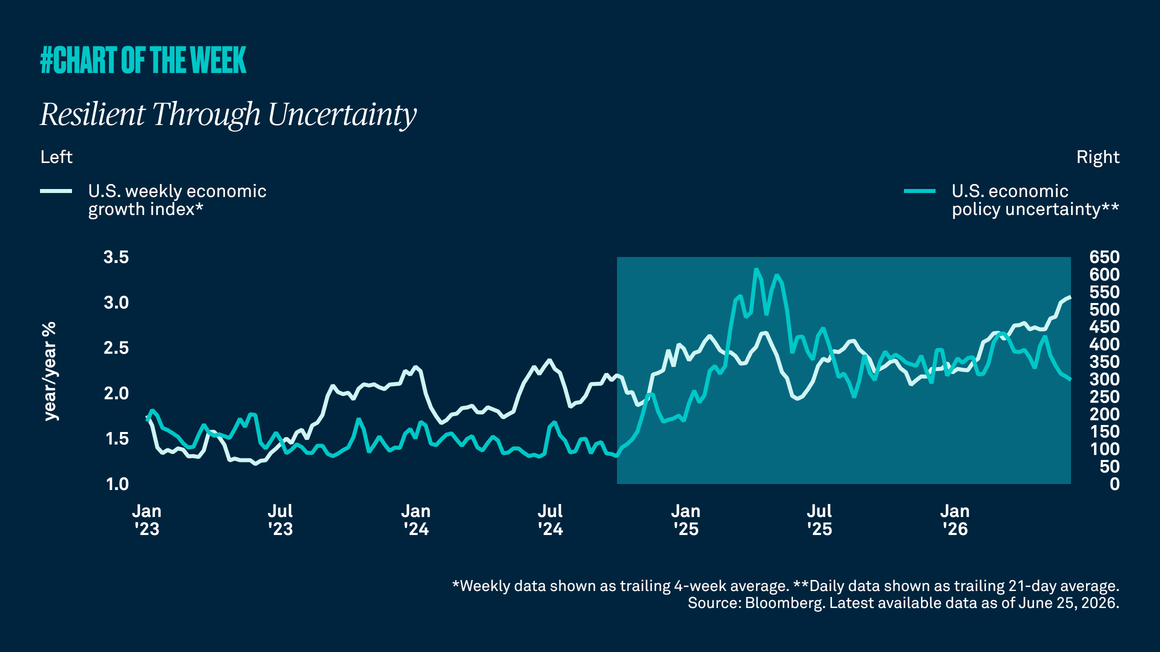

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.