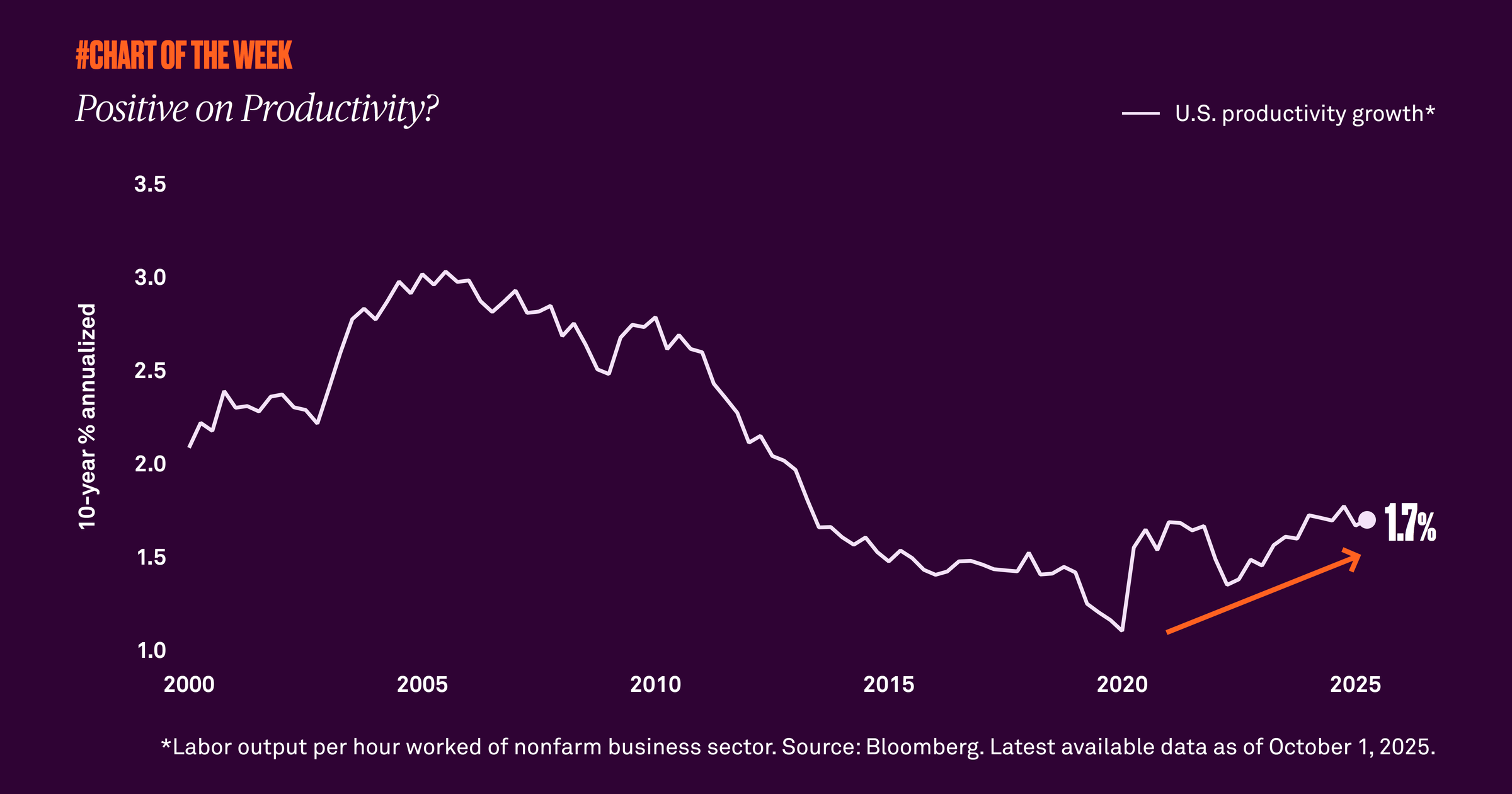

Positive on productivity?

Productivity, or output per hour worked, is a key driver of long-term economic growth. Now, after years of stagnation, productivity is on the rise again, a positive sign for future growth.

The level of productivity in the U.S. economy is something we watch closely because it is a key driver of long-term economic growth: it measures how efficient a country is at producing goods and services with a given level of inputs. Now, after years of stagnation, productivity growth, as measured by output per hour worked, is on the rise again. Productivity has expanded 1.7% on an annualized basis over the last 10 years.

Several factors have been weighing on economic growth of late. One is a reduced labor supply owing to an aging population and declining immigration. Additionally, the job market has been softening as payroll growth has stalled in recent months. In the face of these structural challenges, enhanced productivity may be critical to improving economic growth.

We therefore believe there is reason for optimism. With capital expenditures increasing thanks to provisions in this year’s tax and spending bill, we anticipate a continued acceleration in investment in and adoption of artificial intelligence, which could further improve productivity.

Additionally, higher productivity allows the economy to expand without adding inflationary pressures, which is critical at a time when inflation remains above the Federal Reserve’s 2% target. Given our productivity expectations, our view on the U.S. economy remains constructive.

820045 Exp : 14 October 2026

YOU MIGHT ALSO LIKE

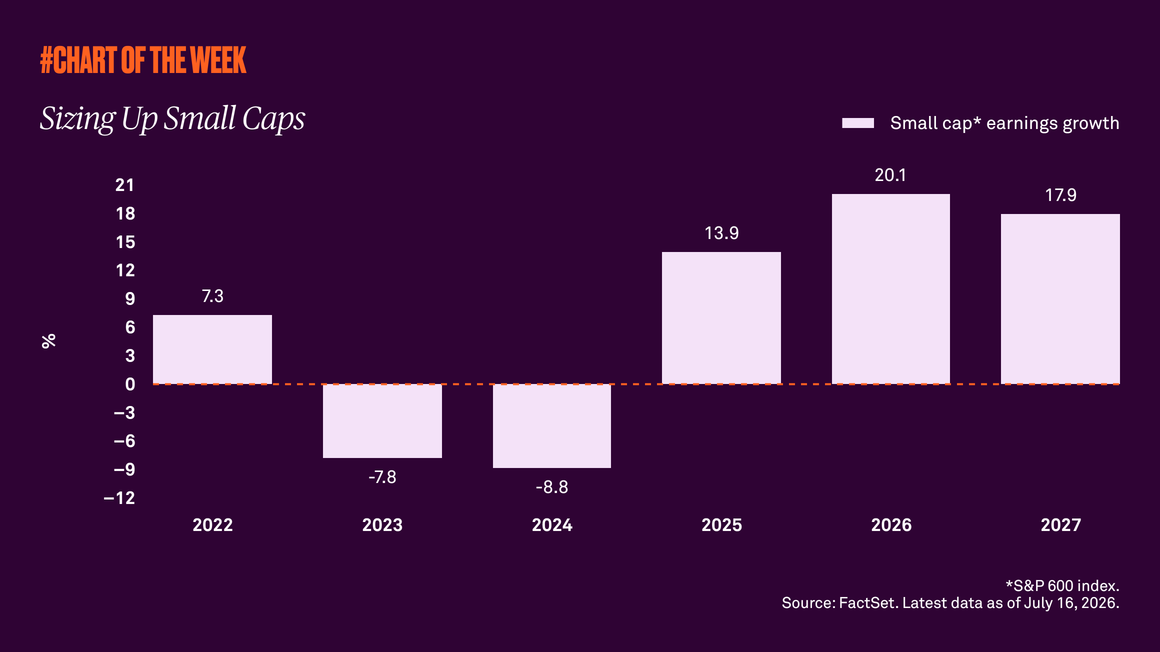

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

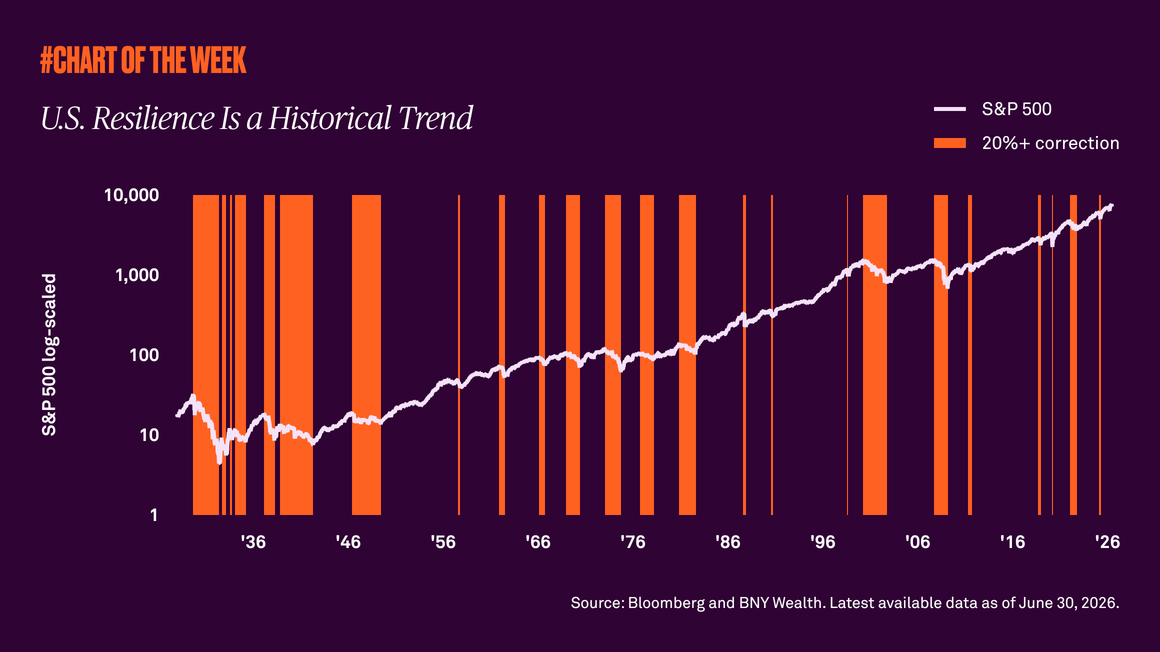

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

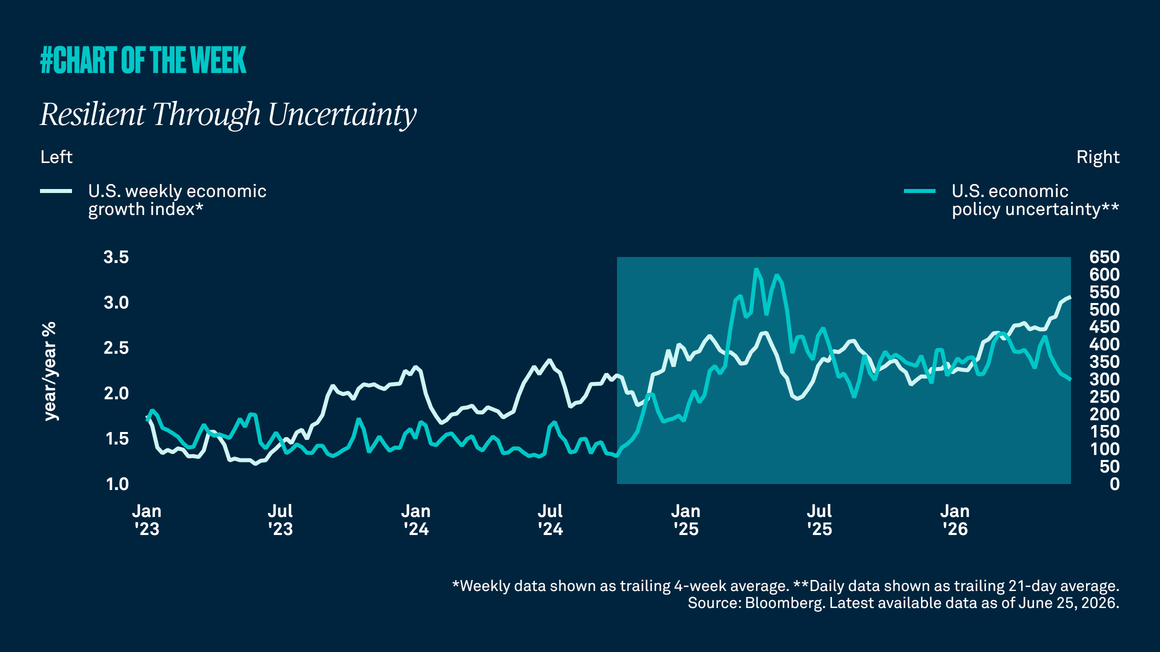

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.