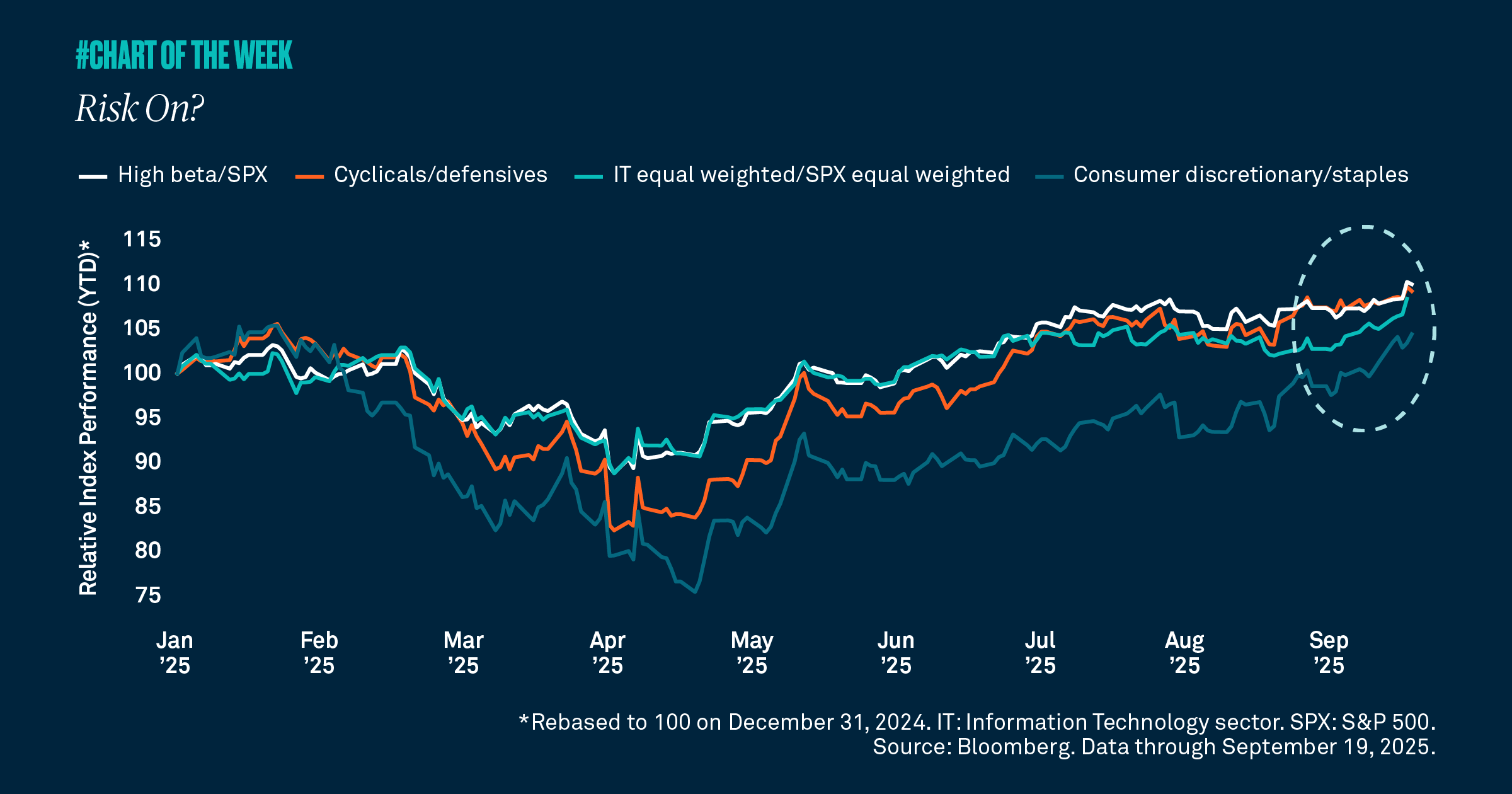

Risk on?

The S&P 500 is trading at record highs, which some investors didn’t see coming after the tariff-fueled drop in April. What may come as a bigger surprise, however, is the rally is broadening beyond big technology companies. Let’s examine different measures that prove this point.

Ever since early April, when policy uncertainty took the market down around 20%, equity indices have been gaining, hitting all-time highs with notable frequency. The S&P 500 is now up over 13% year to date, which some investors didn’t see coming. What may come as a true surprise, however, is that the rally is broadening beyond big technology companies.

Cyclicals are outperforming defensive sectors, indicating that investors are becoming more positive on the outlook. Additionally, high beta stocks — or those that tend to experience larger price swings — are at a year-to-date high compared to the overall market, as measured by the S&P 500. When high beta stocks outperform, it typically signals the market is becoming more bullish. Consumer discretionary is leading staples, suggesting the consumer can remain resilient despite slowing job growth. Lastly, the equal-weighted technology sector is outperforming the average stock. This means technology stocks other than the Magnificent Seven are performing well too, implying a more diversified constellation of companies is gaining.

Together, these signals demonstrate that the market is more positive on the forward outlook. Slowing job growth remains a risk, and we will watch closely in case it spills over into consumer spending. Nonetheless, we believe equities can continue to move higher as the Federal Reserve eases into an improving earnings environment.In our view, despite slowing jobs growth, the economy is showing signs that the outlook heading into 2026 is improving. Earnings are strong and growing stronger, and companies only stand to benefit from easing monetary policy. Though gross domestic product may fall short of 2024 performance, we anticipate it will come in positive this year between 1.5%-2%. While we believe improving small business optimism is positive for growth, we will continue to monitor the attitudes of small business owners, watching to learn whether recent momentum can persist.

808020 Exp : 22 September 2026

YOU MIGHT ALSO LIKE

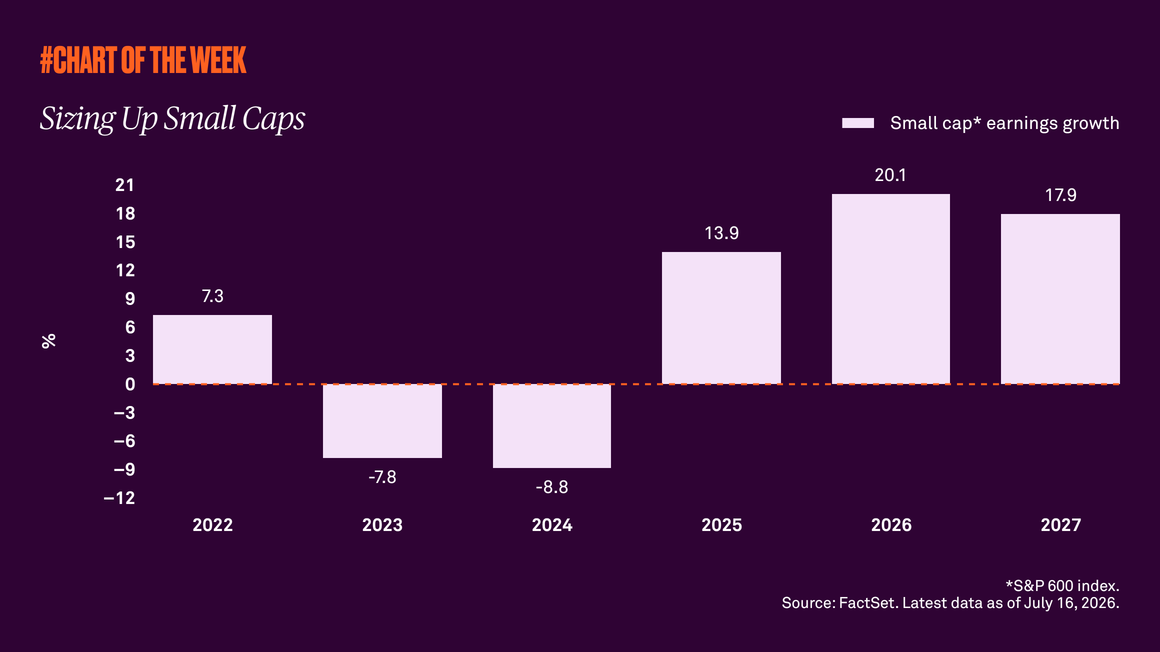

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

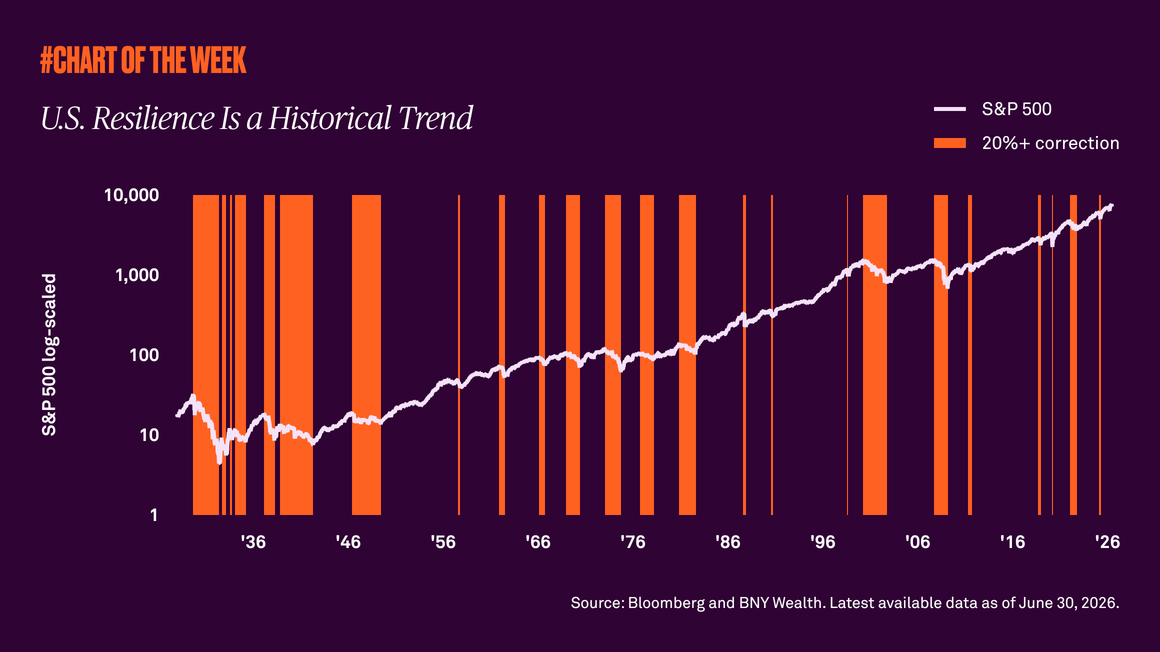

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

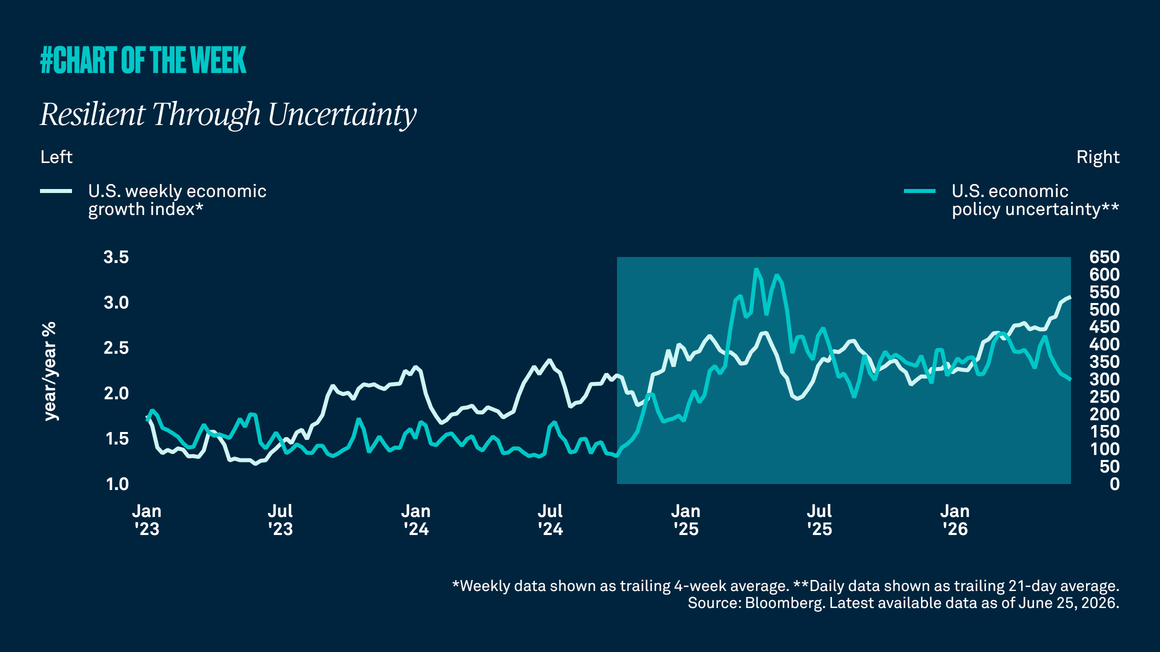

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.