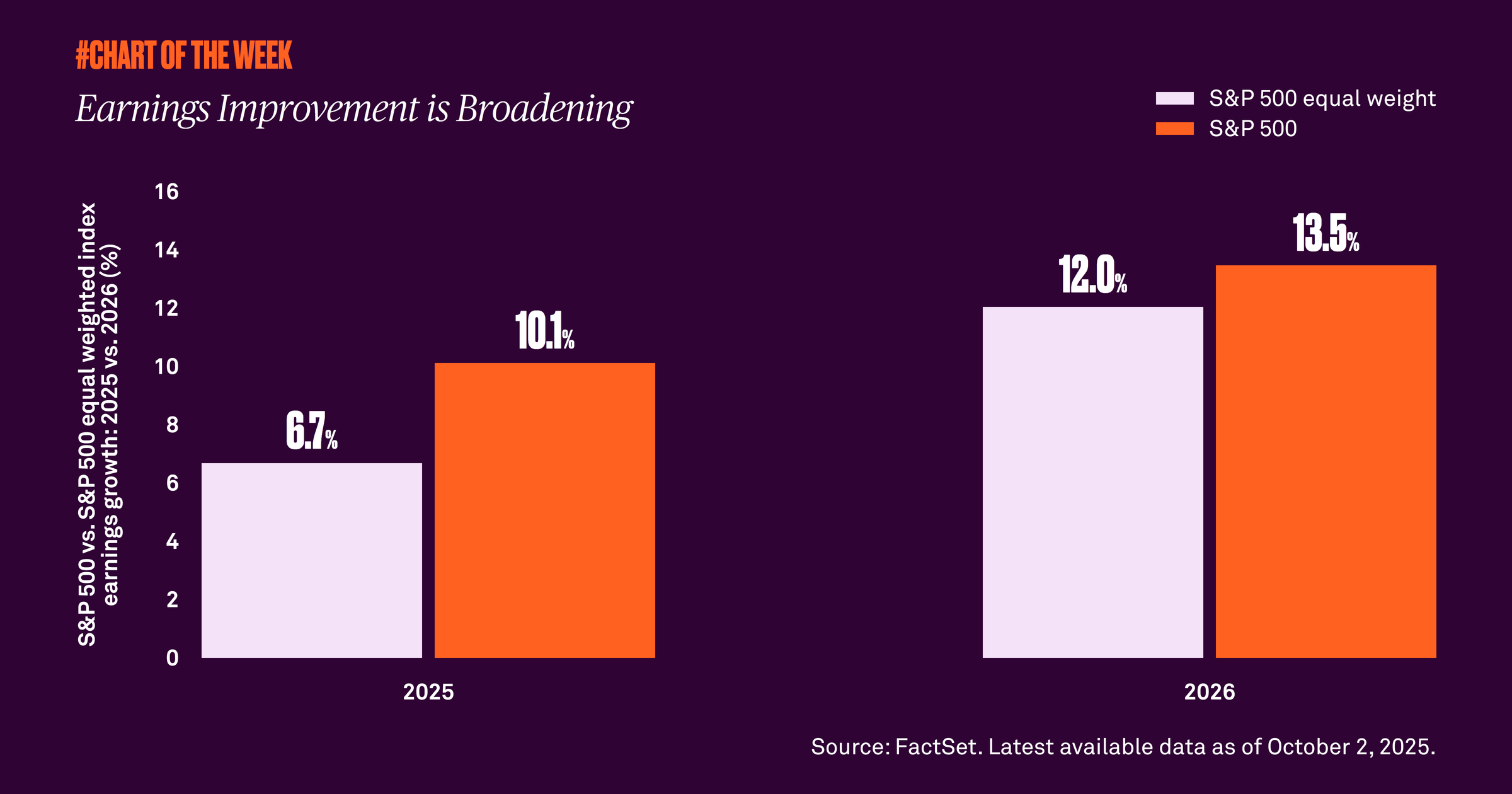

Earnings improvement is broadening

Earnings growth is on investors’ minds, especially as it broadens beyond the big tech stocks that have shown the most improvement in the past. We believe this is a positive sign for continued equity gains.

Equity market performance this year has been driven by better-than-expected earnings. With big tech dominating much of this growth, some investors have become concerned about concentration risk among technology stocks. However, current forecasts suggest earnings are improving beyond big tech into other sectors.

As of today, the market capitalization-weighted S&P 500’s earnings are forecasted to grow 10.1% in 2025 compared to 6.7% for the index’s equal-weighted counterpart, representing a gap of 3.4%. However, despite concerns about slowing jobs growth and the impact on the economy, that gap is expected to narrow in 2026 with S&P 500 earnings forecasted to grow 13.5% compared to 12% for the equal-weighted index — only a 1.5% difference.

Broadening earnings revisions should continue to support U.S. equities. Additionally, we are entering a seasonally favorable period, as the fourth quarter has historically been the best performing quarter of the year. These factors, combined with the Federal Reserve’s easing of monetary policy and improving margins, should be positive for stocks through year end.

815085 Exp : 07 October 2026

YOU MIGHT ALSO LIKE

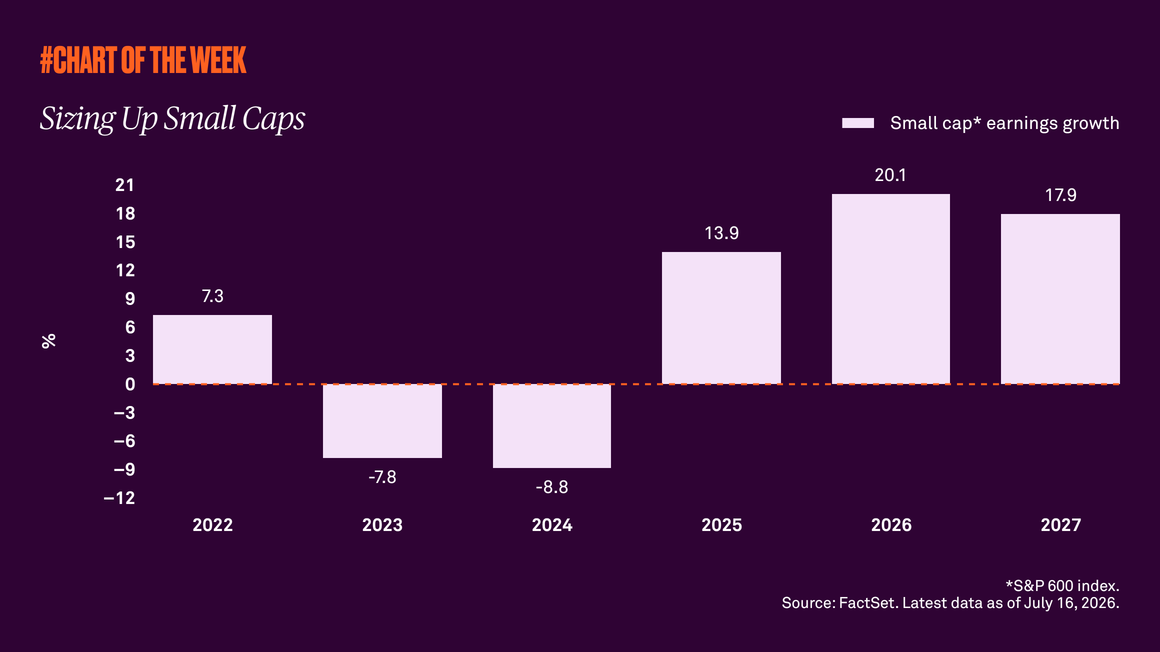

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

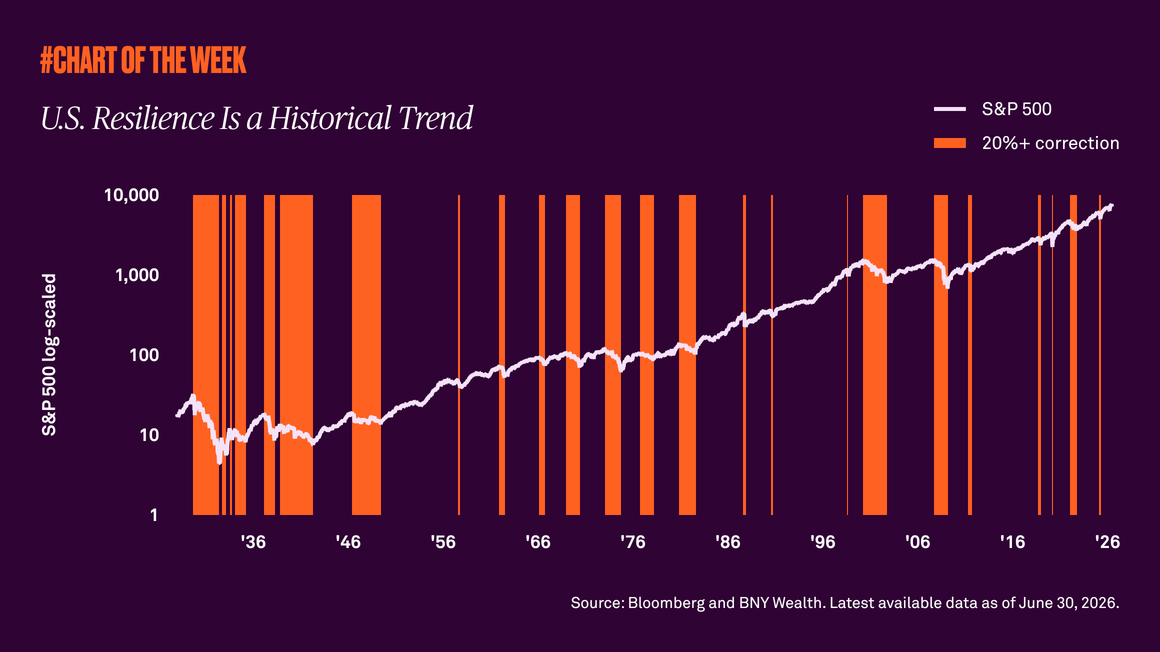

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

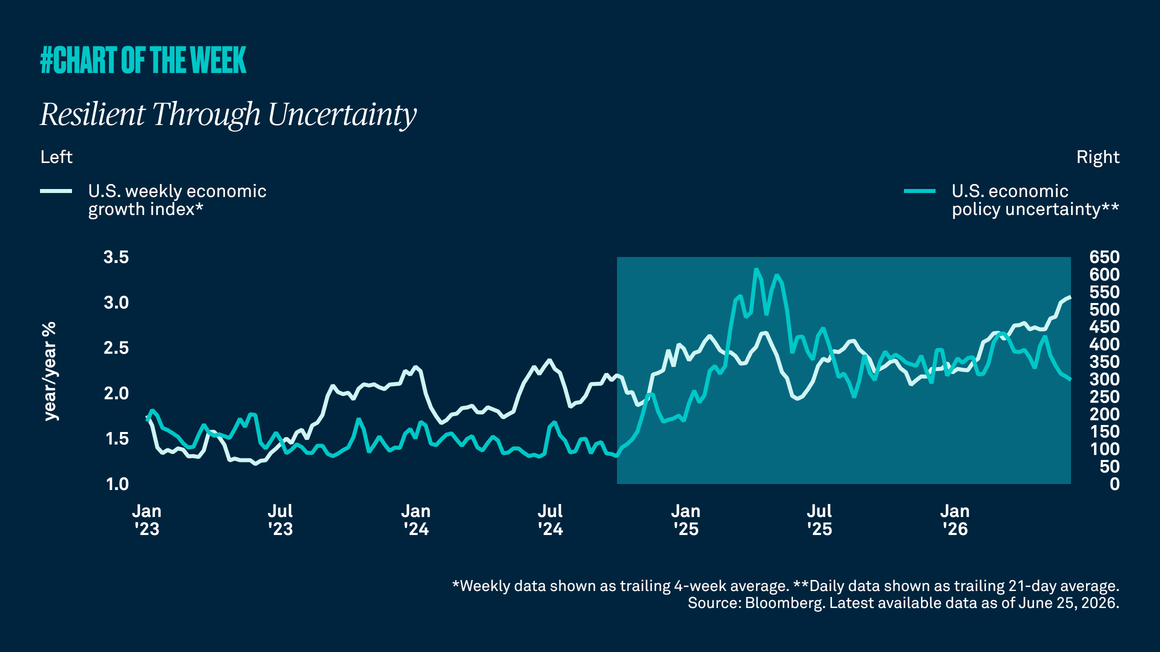

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.