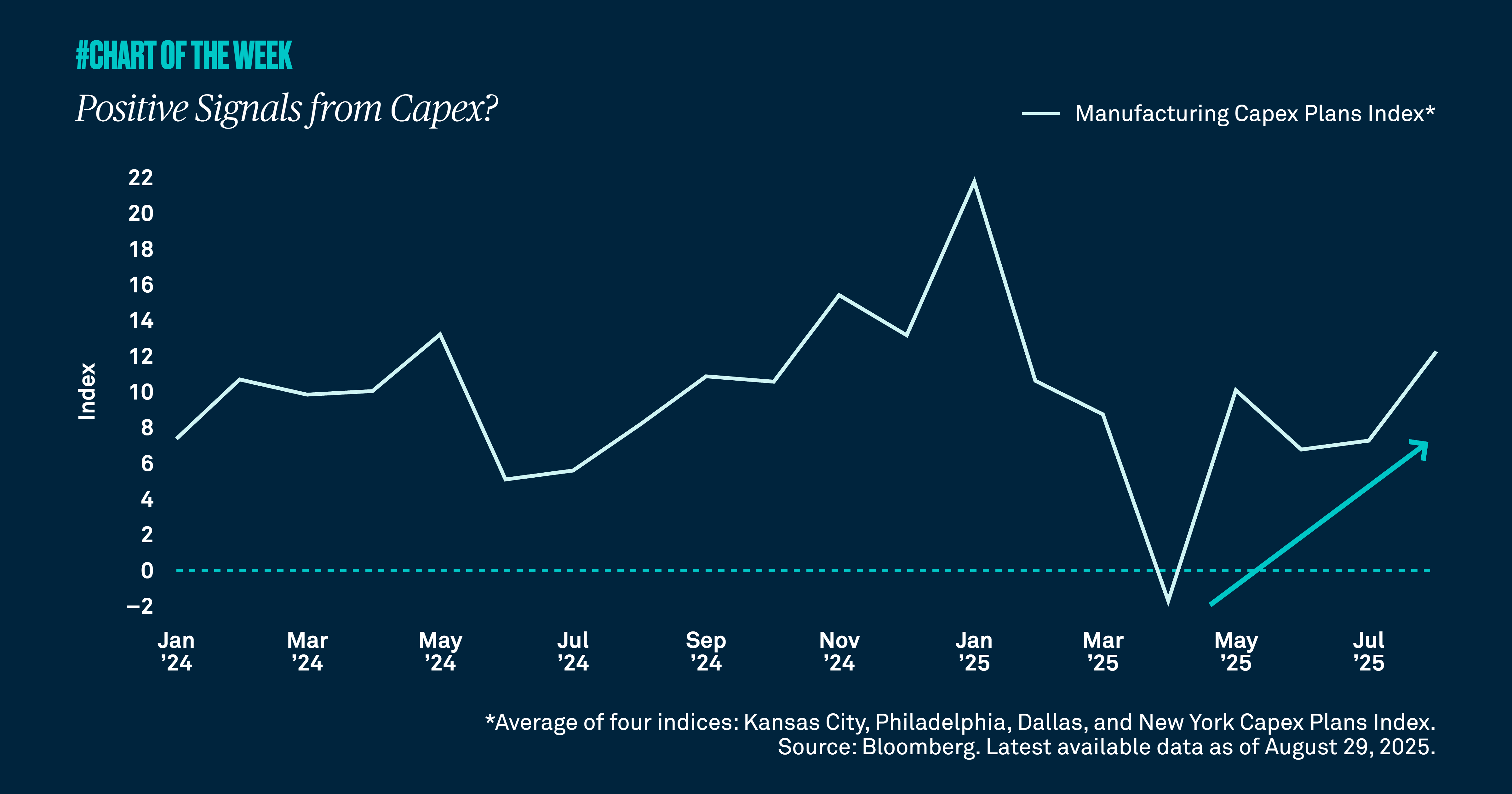

Positive signals from capex?

The One Big Beautiful Bill Act’s provision regarding the full expensing of capital expenditures is already having an impact on companies’ investment plans. We believe this a positive signal for economic growth.

Second quarter earnings season is winding down, with ~92% of S&P 500 companies having reported. Over 80% of those companies beat analysts’ expectations, pleasing many investors and correcting a downward shift in S&P 500 margin estimates that has stabilized since May.

Margins illustrate the quality and durability of corporate earnings by demonstrating how effectively a company controls costs and converts sales into profits. In 2025, net margins are expected to reach 13.3%, up from 12.9% in 2024, as well as increase another 0.7% to 14.0% in 2026. Notably, estimates for technology companies are significantly better than those of the entire S&P 500.

In fact, technology enhancements are the key driver of higher margins for the index. Specifically, the continued development and broadening adoption of artificial intelligence (AI) should bolster companies’ productivity and, in turn, lead to higher margins. Some of the ways that AI increases margins include improving operational efficiency, employing data-driven decision making, enhancing supply chain optimization, and enabling product and service innovations.

The immense progress in AI and its encouraging potential support our constructive view of equities. Improving estimates for both margins and earnings underscore our overweight position in large cap stocks and should push the market higher by year end.

798642 Exp : 01 September 2026

YOU MIGHT ALSO LIKE

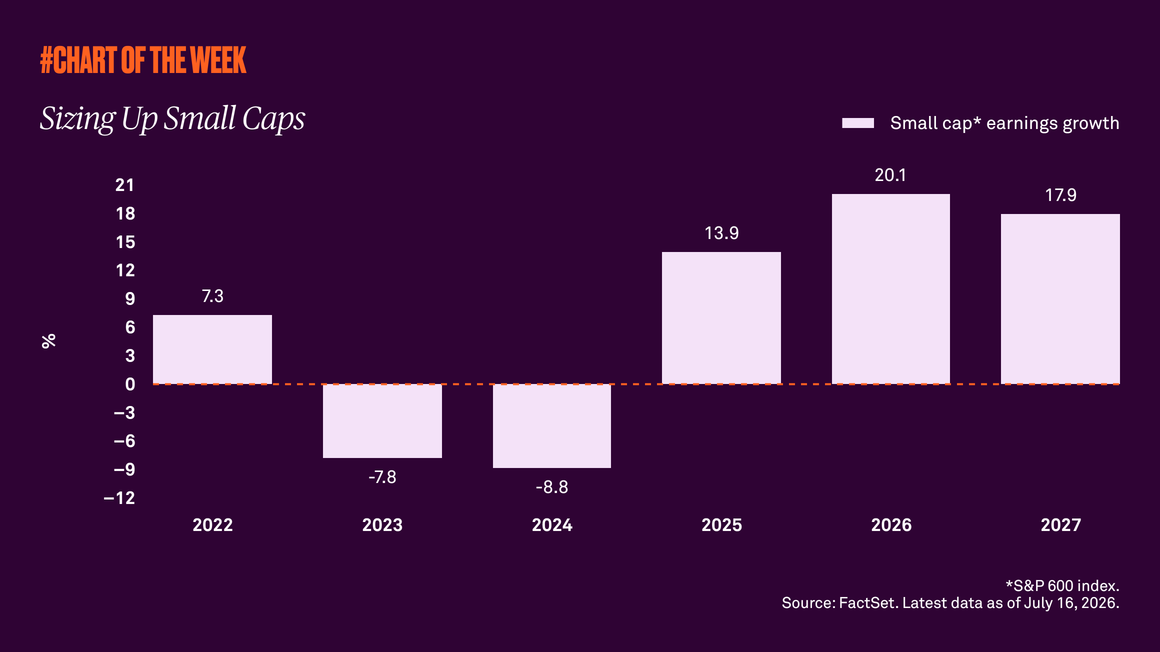

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

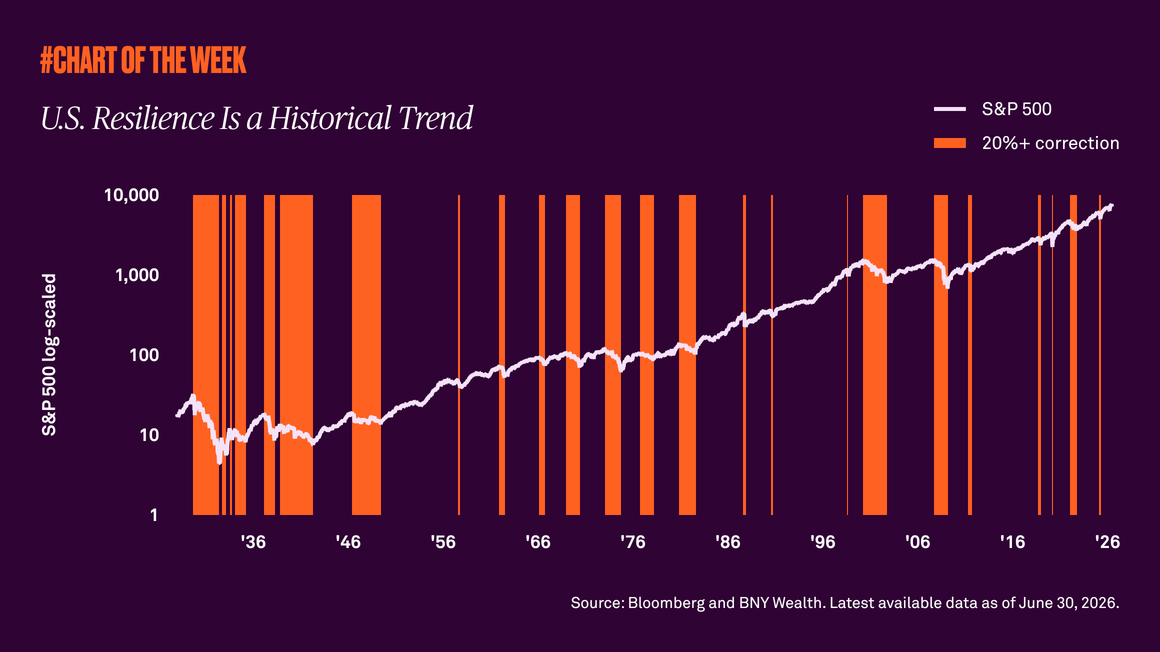

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

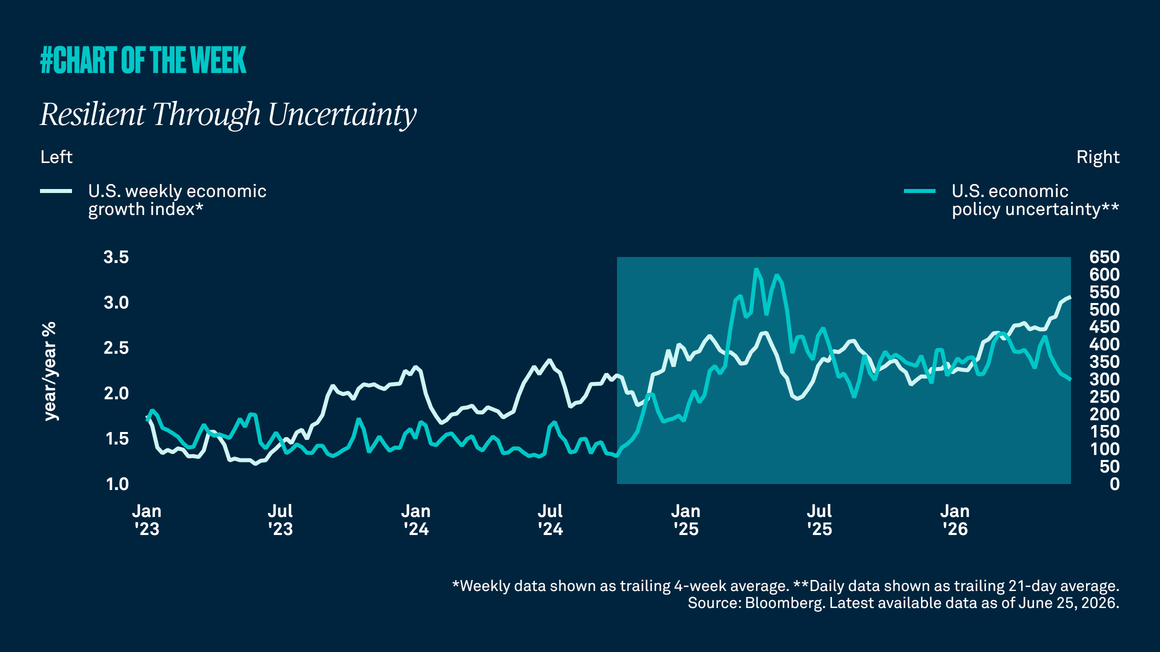

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.