FOMC minutes discuss RMPs and the SRF

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 5 minutes

EXHIBIT #1: REPO SPIKES AT YEAR END; SRF TAPPED

Source: BNY Markets, Bloomberg, Federal Reserve Bank of New York

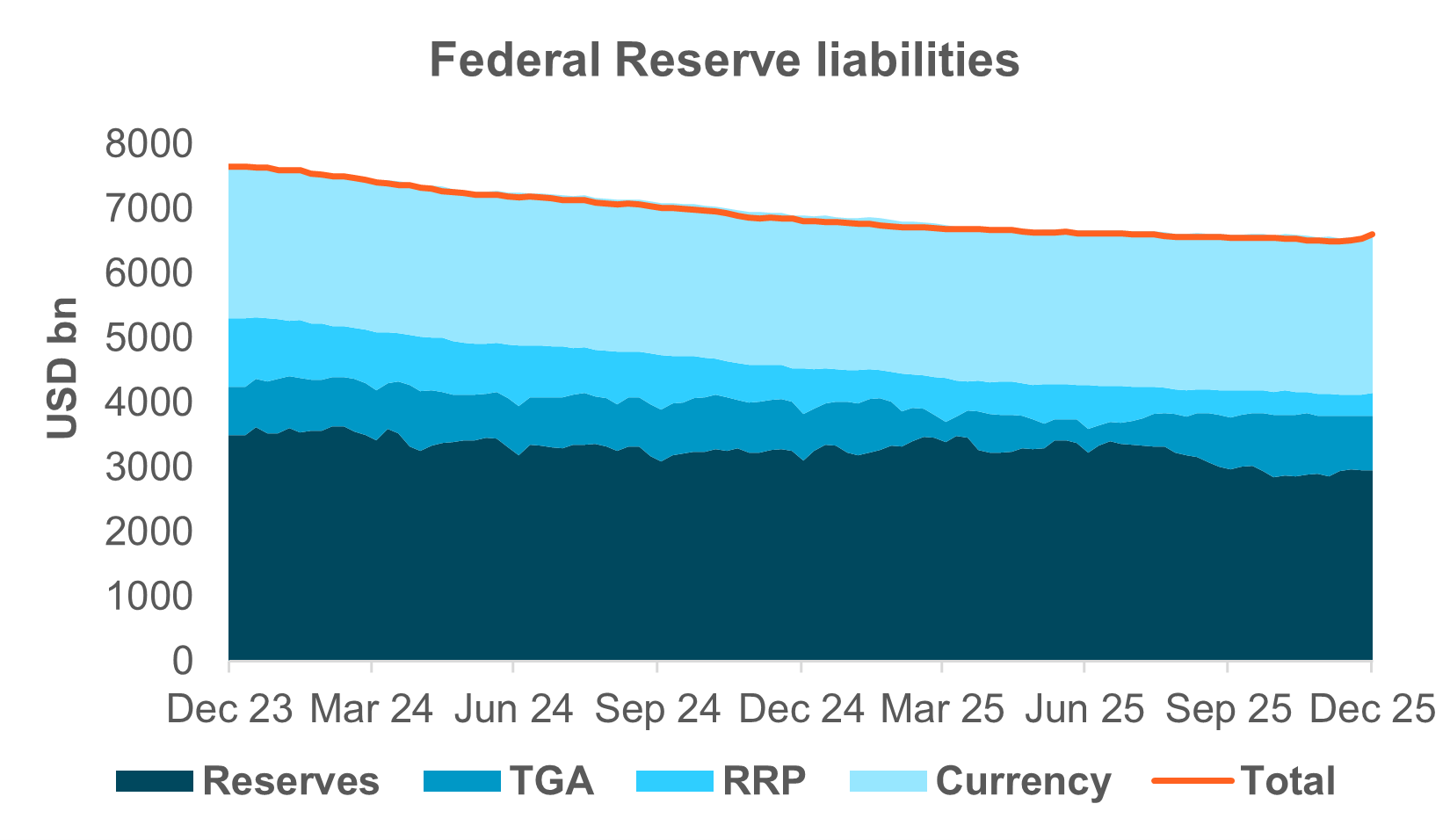

EXHIBIT #2: LARGER TGA BALANCES LEAD TO LOWER RESERVES AND MARKET LIQUIDITY

Source: BNY Markets, Federal Reserve Board of Governors

Not unexpectedly, funding markets showed signs of strain around year-end 2025. Repo spreads rose significantly, and the Federal Reserve’s standing repo facility (SRF) saw notable use at the end of December. Of course, month-end periods tend to see spiking demand for funding in the market, and the pattern of rising spreads during those times has held since the end of last summer. This can be seen in Exhibit #1, which shows money market spreads over relevant administered rates, as well as daily take-up of the SRF.

Since mid-December, SRF operations haven’t been the only mechanism employed by the Fed to keep these markets functioning relatively smoothly. Commensurate with its announcement at the December 10 FOMC, the central bank began purchasing T-bills to keep reserve balances steady. All in all, the Fed purchased around $38bn in bills last month, roughly equivalent to the $40bn indicated at the meeting. Note that in his press conference on the day of the meeting (see transcript here), Fed Chair Jerome Powell indicated that such reserve management purchases (RMPs) “may remain elevated for a few months to alleviate expected near-term pressures in money markets.” Most likely the Fed will keep up a similar monthly pace at least through April, when the tax date leads to an increase in demand for liquidity.

It's important to note that even though these RMPs increase the size of the Fed’s balance sheet, these purchases are not intended as monetary policy easing akin to QE. Instead, they are what their name proclaims them to be – reserve management operations aimed at keeping the plumbing of the money markets intact and the federal funds rate in its established range.

The December FOMC minutes devote a lot of space to balance sheet issues, summarizing the Committee’s discussions on the topic. Much of this section deals with themes we’ve explored recently in Short Thoughts (see here, here and here for examples). These include: the judgment that reserves are now ample (rather than abundant); the Fed staff’s recommendation (subsequently adopted by the Committee) to begin RMPs to keep reserves ample; the intention to buy mostly T-bills to better align the Fed’s balance sheet with the public UST market; and the need for flexibility in sizing RMPs in response to swings in reserve demand and demand for nonreserve liabilities.

“Nonreserve liabilities” refer to the Treasury General Account (TGA). After the debt ceiling was dealt with in early July 2025, the TGA swelled from below $300bn to a peak of $1tn in late October and has recently settled within an $800bn to $900bn range – roughly the level promised by the Treasury in its last few quarterly funding announcements. Higher TGA balances mean more bill issuance and falling reserves, hence less money market liquidity. Exhibit #2 shows how the TGA has increased over time and the effect that this growth has had on bank reserves, currently below $3tn, a level that they exceeded for most of 2025.

Also interesting in the minutes was the FOMC’s view on the SRF itself. Fed staff indicated that the SRF has played a role in keeping the effective federal funds rate (EFFR) within its target range, although it was also noted that “while usage of these operations had increased recently, there had been days when a large volume of repo trades occurred well above the operations’ minimum bid rate, suggesting reluctance by some potential participants to engage in standing repo operations.”

In other words, on days that saw elevated money market rates, borrowing from the Fed’s SRF would have been more economical than relying on the market. However, this rarely occurred. The minutes suggest that a combination of “misperceptions about the intended purpose of standing repo operations” and “specific operational features” of the facility itself is contributing to the underuse of the facility. We interpret the former concern to imply potential counterparties feel there is a stigma to using the SRF, much like the discount window. To deal with the latter, the Fed cites market participants suggesting a move to centrally clear SRF transactions, as well as eliminating the $500bn aggregate limit on the facility.

Furthermore, it appears there are two schools of thought about the SRF’s role in interest rate control in an ample reserve regime. The minutes cite the preference of “some participants” to use the facility more actively for EFFR control, while “several participants” (i.e., more than just “some”) prefer RMPs. Reasons for these preferences weren’t cited. But we recall a speech by Vice Chair for Supervision Michelle Bowman, in which she advocated for a balance sheet that keeps reserves closer to scarce than ample, arguing that it would reduce the Fed’s “footprint” in the markets. In addition, running reserves closer to scarce than ample would allow for more active balance sheet management, responding only during periods of market stress. This would represent a return to pre-GFC conditions, when such active management was common.

Also interesting in the minutes was the FOMC’s view on the SRF itself. Fed staff indicated that the SRF has played a role in keeping the effective federal funds rate (EFFR) within its target range, although it was also noted that “while usage of these operations had increased recently, there had been days when a large volume of repo trades occurred well above the operations’ minimum bid rate, suggesting reluctance by some potential participants to engage in standing repo operations.”

In other words, on days that saw elevated money market rates, borrowing from the Fed’s SRF would have been more economical than relying on the market. However, this rarely occurred. The minutes suggest that a combination of “misperceptions about the intended purpose of standing repo operations” and “specific operational features” of the facility itself is contributing to the underuse of the facility. We interpret the former concern to imply potential counterparties feel there is a stigma to using the SRF, much like the discount window. To deal with the latter, the Fed cites market participants suggesting a move to centrally clear SRF transactions, as well as eliminating the $500bn aggregate limit on the facility.

Furthermore, it appears there are two schools of thought about the SRF’s role in interest rate control in an ample reserve regime. The minutes cite the preference of “some participants” to use the facility more actively for EFFR control, while “several participants” (i.e., more than just “some”) prefer RMPs. Reasons for these preferences weren’t cited. But we recall a speech by Vice Chair for Supervision Michelle Bowman, in which she advocated for a balance sheet that keeps reserves closer to scarce than ample, arguing that it would reduce the Fed’s “footprint” in the markets. In addition, running reserves closer to scarce than ample would allow for more active balance sheet management, responding only during periods of market stress. This would represent a return to pre-global financial crisis conditions, when such active management was common.

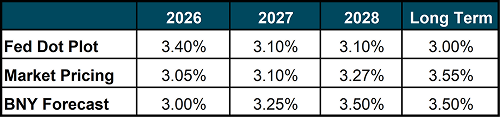

Market-implied rate expectations for the new year suggest an effective federal funds rate of 3.04%, or about 2.5 rate cuts. We find it interesting that the forward curves are not more dovish. A string of weaker economic data, however, could force those expectations lower. We maintain roughly the same outlook for 2026 as the market, although we are ready to downshift that view in response to data. Odds of a January cut remain below 20%, while only the June meeting reflects a greater than 50% chance of a cut.