Rate Cut and RMPs Feature at December FOMC

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 5 minutes

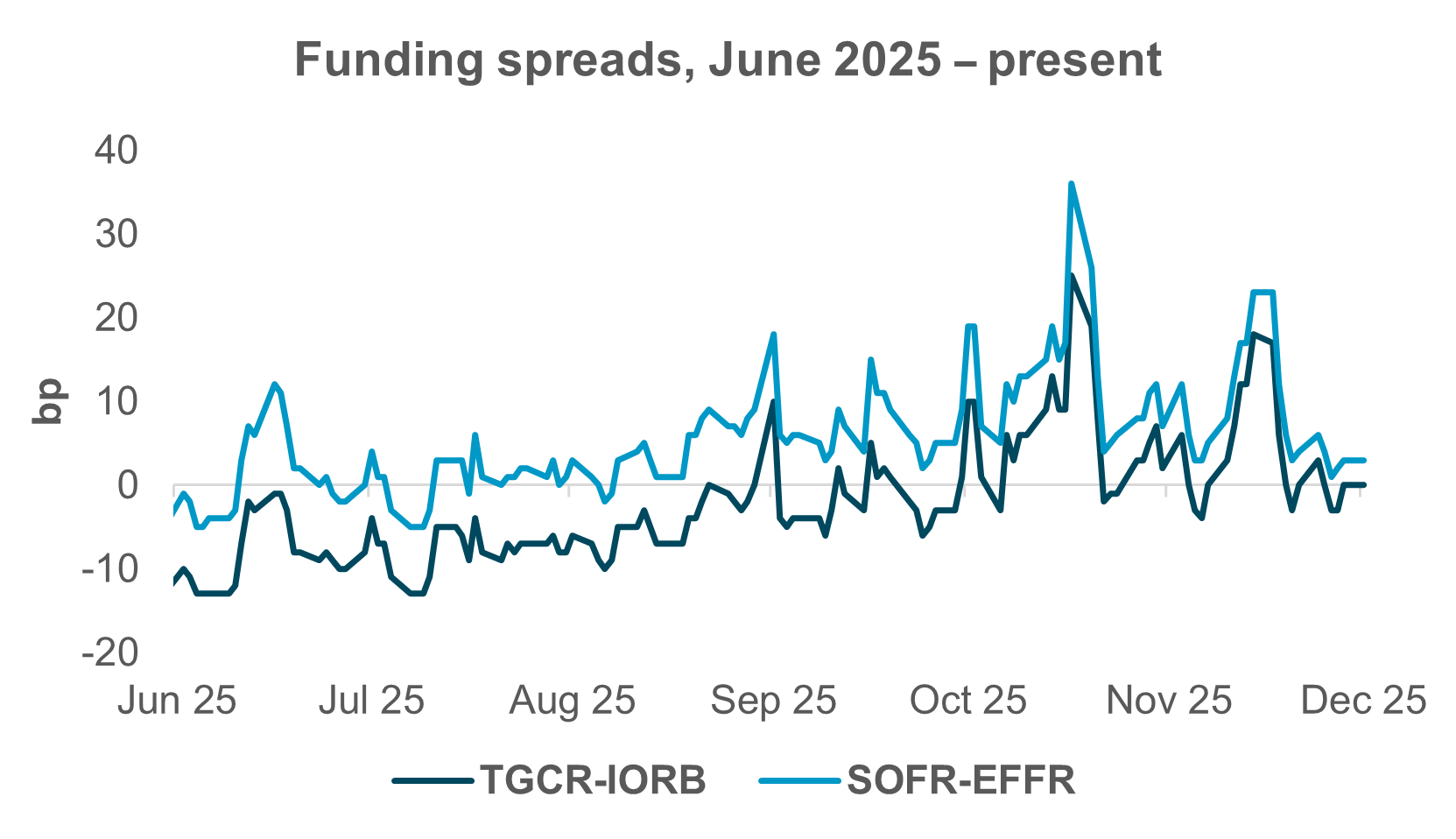

EXHIBIT #1: HAS THE ANNOUNCEMENT OF RMPS SETTLED FUNDING MARKETS?

Source: BNY Markets, Bloomberg

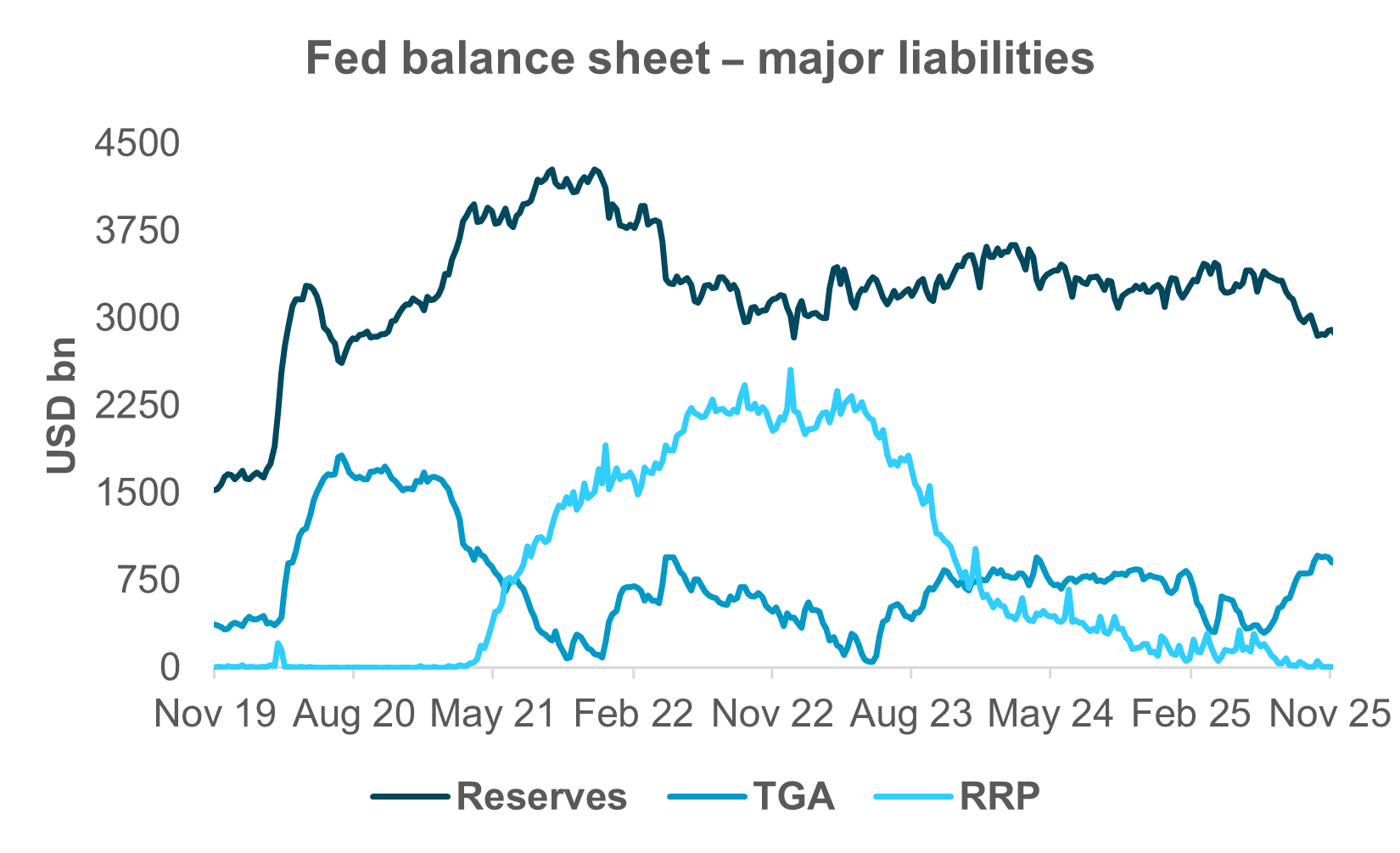

EXHIBIT #2: TGA GROWTH DRAINED RESERVES IN H2 2025

Source: BNY Markets, Federal Reserve Board of Governors

As expected, the FOMC delivered a 25bp rate cut last week, although the December Summary of Economic Projections (SEP) indicated a more hawkish trajectory for 2026 and even featured some “silent dissents” in the 2025 dots. Dissents in opposite directions were registered: Governor Stephen Miran was in favor of a larger 50bp reduction, while Chicago Fed President Austan Goolsbee and Kansas City President Jeffrey Schmid voted for no rate cuts. The policy move wasn’t unexpected, nor were the dissents.

We’ll offer our analysis of monetary policy in the following section. Here, we’ll discuss the Fed’s other big move announced last week, namely the beginning of reserve management purchases (RMPs) aimed at keeping reserves ample and therefore tamping down on money market rate volatility. This action was also generally expected. The FOMC pledged $40bn in bill purchases this month and similar monthly RMPs through April 2026. In his press conference after the meeting, Chair Jerome Powell emphasized that these purchases are being enacted for the “sole purpose of maintaining an ample supply of reserves over time.” This is not monetary policy activity, and although the Fed’s balance sheet will increase due to the RMPs, this is not quantitative easing.

If the Fed were to purchase $40bn per month through April next year, we’d see a total of $200bn in T-bill buying as part of the RMP program. If the central bank were to reduce that by half thereafter, we’d see an additional $160bn in purchases through the end of next year. This excludes the new T-bill purchases announced at the Fed’s October meeting, as MBS redemptions are being redirected toward front-end purchases to better align the Fed’s portfolio with the duration and mix of USTs outstanding in the public market. Altogether, we could see the Fed buying around $500bn in T-bills between now and the end of next year.

Since the beginning of July, the Treasury has issued nearly $1.6tn in T-bills. Over that same period, the Treasury General Account (TGA) has increased by $500bn, while money market mutual funds (MMFs) have purchased an additional $850bn between the end of June and the end of November. This leaves roughly $250bn absorbed elsewhere. While the TGA has increased by around half a trillion dollars since mid-year, reserves have fallen by $300bn, transitioning from abundant to merely ample. Over half of the H2 bill issuance was used to rebuild the TGA after the debt ceiling was lifted with the passage of the Republican spending plan. See Exhibit #1.

To maintain ample reserves in a regime where the federal funds rate is managed by the upper (IORB) and lower (RRP) administered rates, the Fed has decided to pursue these RMPs, lest reserves transition from ample to scarce – a state in which open market operations would be required to maintain rate control. As Exhibit #2 shows, the decline in reserves to ample corresponds to the TGA rebuild.

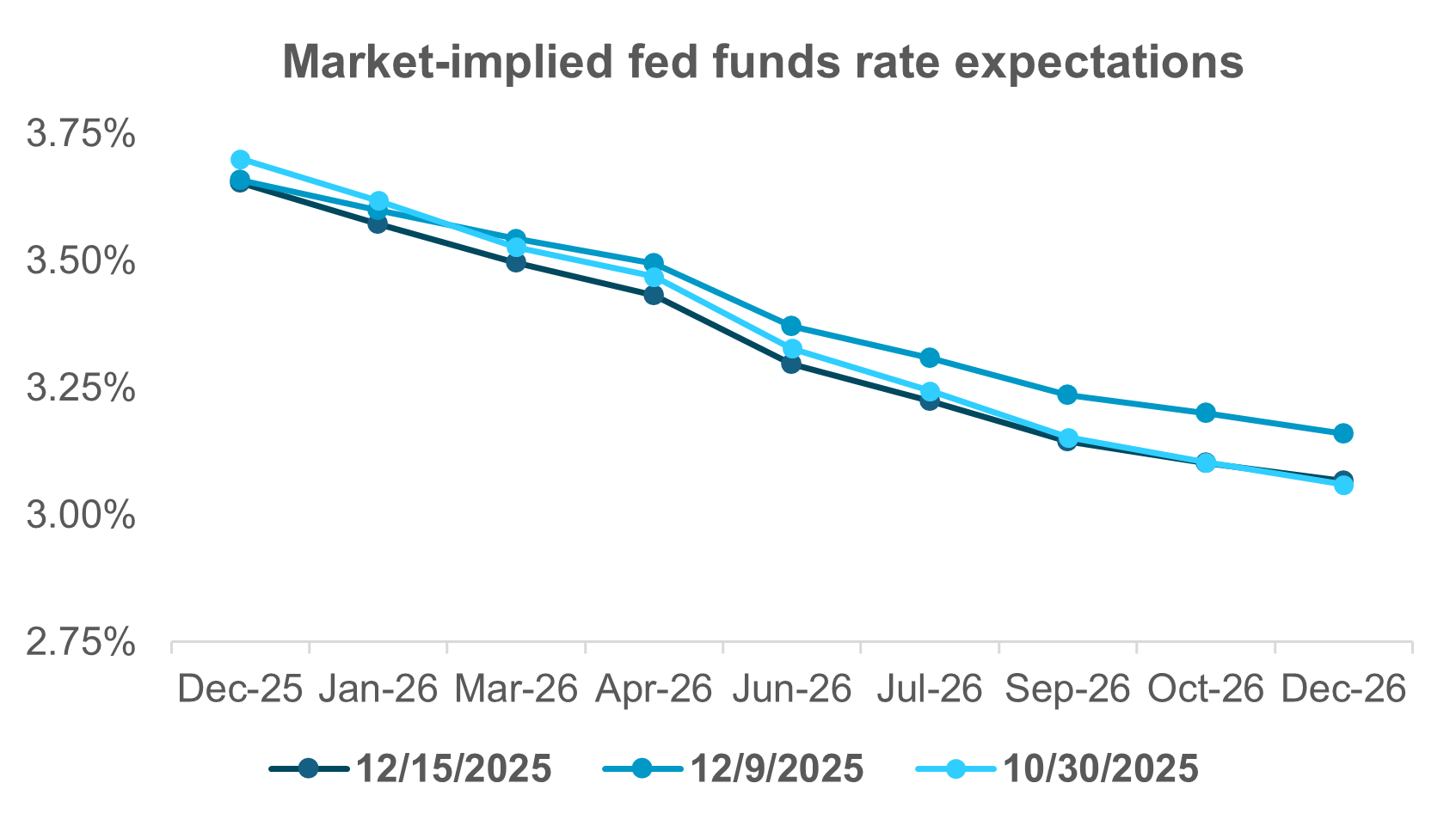

EXHIBIT #3: POLICY EXPECTATIONS BACK TO OCTOBER FOMC LEVELS

Source: BNY Markets, Bloomberg

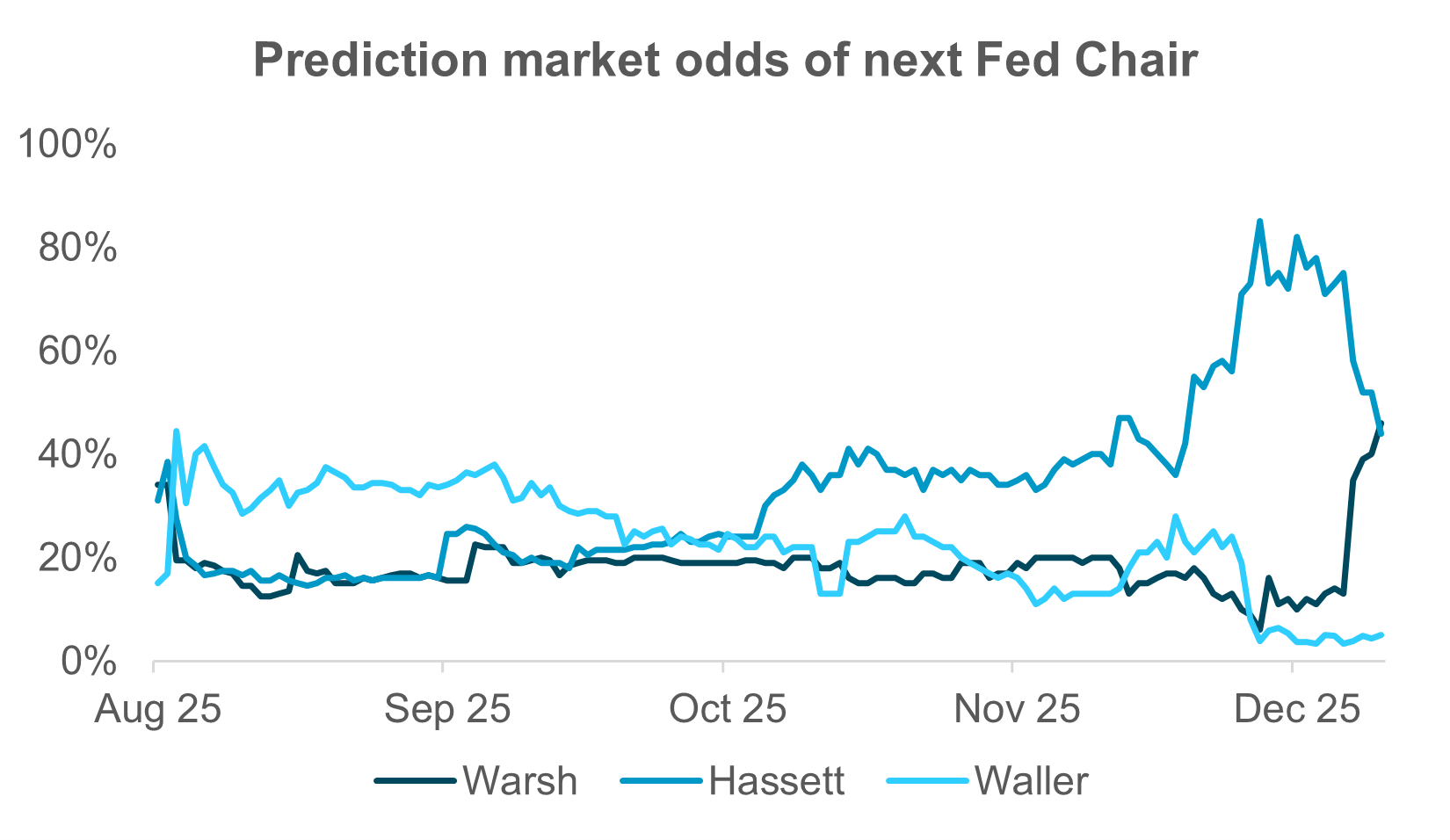

EXHIBIT #4: NEW CO-FRONTRUNNER FOR FED CHAIR?

Source: BNY Markets, Polymarket, Bloomberg

As noted above, the expected rate cut drew the expected open dissents from Messrs. Miran, Goolsbee and Schmid. However, in the dots associated with the SEP, six members (including both FOMC voters and participants) posted dots above the 3.50%–3.75% target range for the federal funds rate decided at the meeting. This gives the impression of a “hawkish cut” and leaves expectations for next year somewhat in stasis. The forward curve for 2026, shown in Exhibit #3, hasn’t really moved much since the October FOMC a few months ago, indicating that the market still expected a few more rate cuts for the year.

We have always said that given the peculiarities of the current moment, disagreement within the Fed is not something that strikes us as terribly worrisome. The economy is clearly at an inflection point, but there are not enough data (yet) to indicate its current state. Furthermore, both goals of the Fed’s dual mandate are potentially under threat. We think that more data, when they finally become available, will go a long way to settling the dispute. There are also Board personnel changes coming in 2026 that will be key in determining the path of policy.

Tuesday’s labor market report will finally give us an official read on the state of the job market and – relatedly – tell us more about where monetary policy is expected to go in early 2026. Currently, the market-implied odds of a January 29 rate cut are just 22%. This could shift higher if our concerns about a weakening labor market are confirmed with the October and November NFP data. We believe that the economy is slowing, and unofficial, privately produced labor data suggest that indeed the jobs picture is deteriorating, likely driving further rate cut expectations. In addition, on Thursday this week, the November CPI will come out, clarifying the inflation picture.

Of course, the FOMC changes composition at the start of the year, as regional Reserve Bank presidents switch places. Hawkish voters Schmid (Kansas City) and Alberto Musalem (St. Louis), as well as Chicago’s Goolsbee (who, we remind readers, favored no cut) and Boston’s Susan Collins rotate off. Cleveland President Beth Hammack and Dallas President Lorie Logan – both hawks – gain voting status, as do Neel Kashkari from Minneapolis and Anna Paulson from Philadelphia. This mix is slightly more hawkish at the moment, but again, that’s in the absence of comprehensive labor market data.

In addition, of course, once Governor Miran’s term ends, the Trump administration will be able to appoint a new governor to replace him, and that person would presumably be elevated to the Chair’s role when Chair Powell’s tenure ends in May. Powell could, in theory, remain on the Committee as a Governor until early 2028, even though he would no longer be Chair. This would be largely unprecedented, making it more likely that Powell resigns from the FOMC when his term as Chair ends, in which case the administration would be able to appoint a new Governor to replace him – someone in line with its preferences, likely a dove.

Regarding the soon-to-named Chair, there has been a new development. Until the end of last week, prediction markets have been coalescing around current National Economic Council Director Kevin Hassett as the likely Chair-designee, but that has changed in recent days. Former Fed Governor Kevin Warsh has seen his odds increase from just over 10% to close to 40%, while Hassett’s odds went from around 75% to just around 50% (Exhibit #4). In the market’s view, the race has tightened.

The choice to succeed Powell will likely be announced soon, although there is no official timetable. Either candidate would likely lean dovish. However, we view the new Chair’s ability to influence and potentially reshape all manner of the Federal Reserve System’s operations and structure as at least as important as their influence on monetary policy.

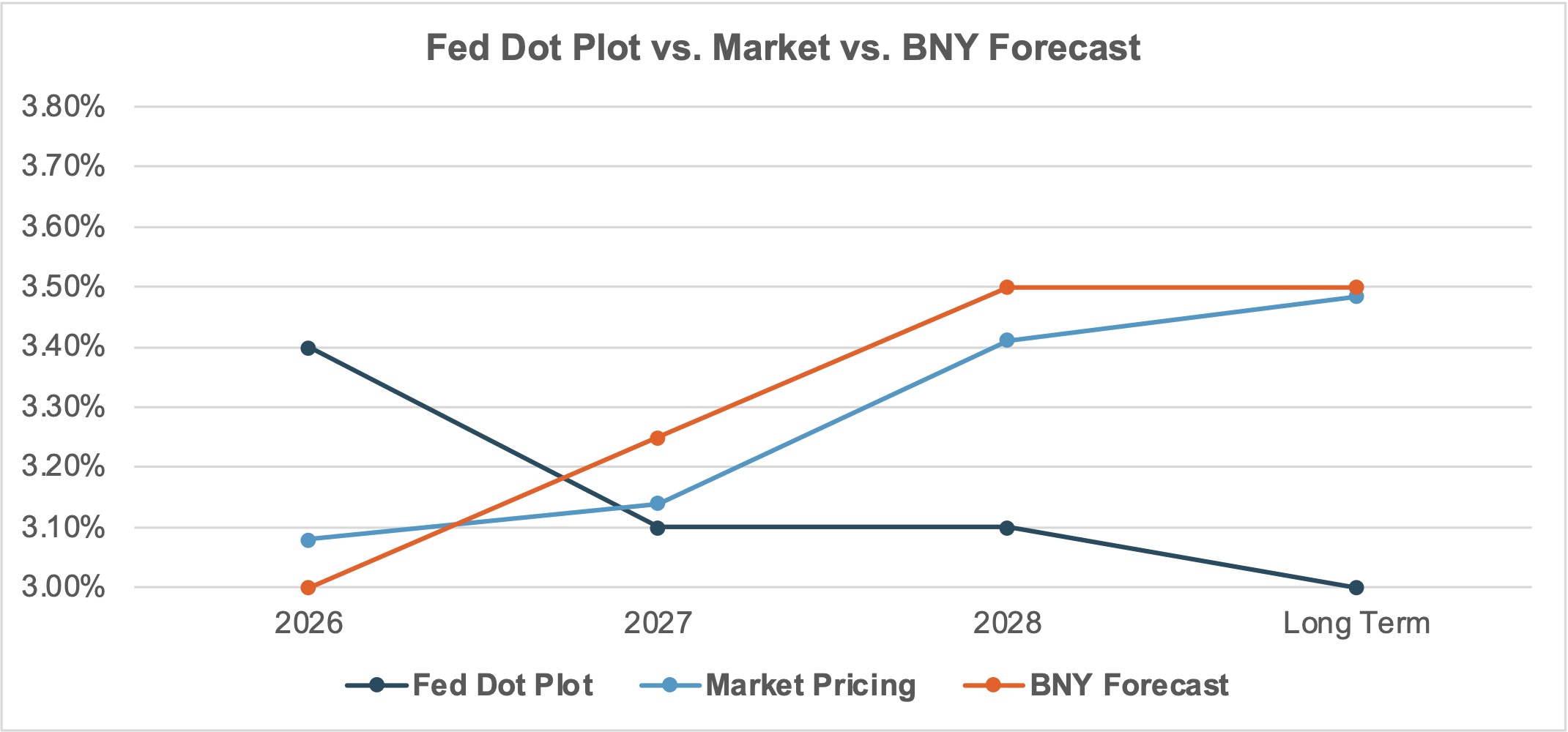

As mentioned above, the new dots from the December SEP remain unchanged from October, with the 2026 federal funds rate median seen at 3.4%, and 2027 and 2028 both at 3.1%. Market expectations have also remained mostly unmoved and see a more hawkish path for rates over the next three years, as do we. The more interesting takeaway from the December SEP was that 6 members did not advocate for an additional rate cut in 2025, essentially providing “silent” dissents to the policy move last week.