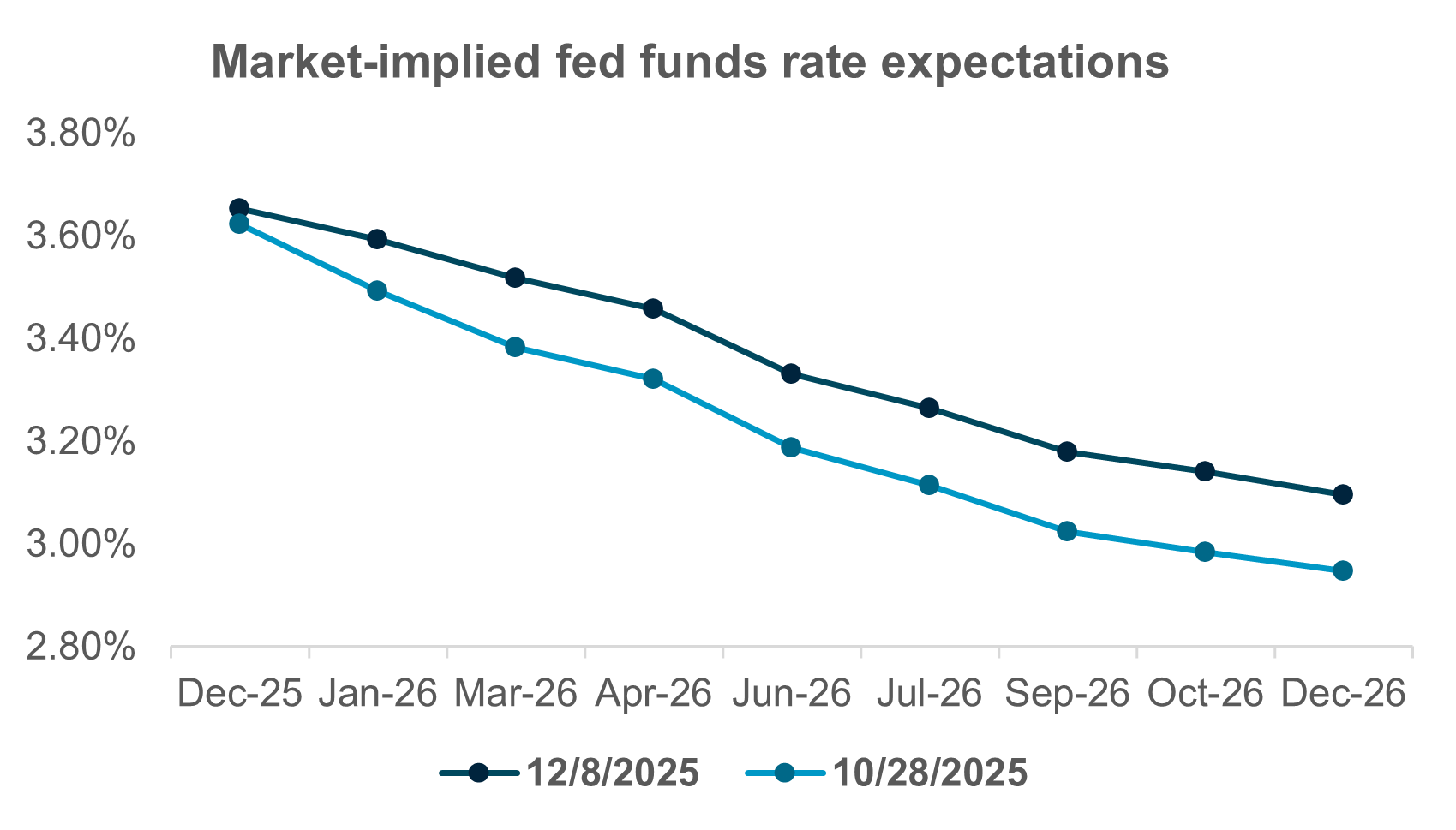

To us, the rate decision is relatively straightforward, even if the commentary around it could take on multiple, nuanced implications. Just as interesting – and crucial – will be whether the Fed announces term repo operations or a new policy of open market operations going into the end of the year and beyond.

Quantitative tightening (QT) formally ended just a week ago, on December 1, in response to tightening liquidity conditions in funding markets. Reserves began to fall this past summer, the result of heavy T-bill issuance after the signing of the Republican budget plan in early July. Between July 1 and November 30, Treasury sold $939bn in bills. Through the end of October, total issuance since July 1 amounted to just over $800bn, and money market mutual funds picked up over $600bn of that – a remarkable asset allocation shift for MMFs. We are still awaiting final money fund data for November, but we expect it to reveal that a similar proportion of short-term Treasury paper was purchased by the market.

This has led to a drain of reserves, something we have been commenting on over the past several weeks (see here and here), ultimately leading to the FOMC announcing the termination of QT at its October meeting, as we expected. At that meeting, the New York Fed’s money markets desk argued that “further reductions in the size of the portfolio may prove short-lived because they would bring forward the time when the Desk would need to restart purchases of securities to maintain ample reserves.” In other words, as we approach critical funding dates (like month-, quarter-, and year-end), the Fed may need to step in and provide liquidity support and find itself regrowing the balance sheet.

Admittedly, we have wavered on this question. Last week, we wrote that we were unconvinced that such an announcement would be forthcoming, given the lack of public commentary from relevant Fedspeakers. However, we have changed our view based in part on those comments in the minutes, as well as based on where we see funding markets at year end. We expect term repo operations to be offered over the year-end turn, and possibly the creation of a TOMO-like facility to support money markets as reserves stay under pressure.

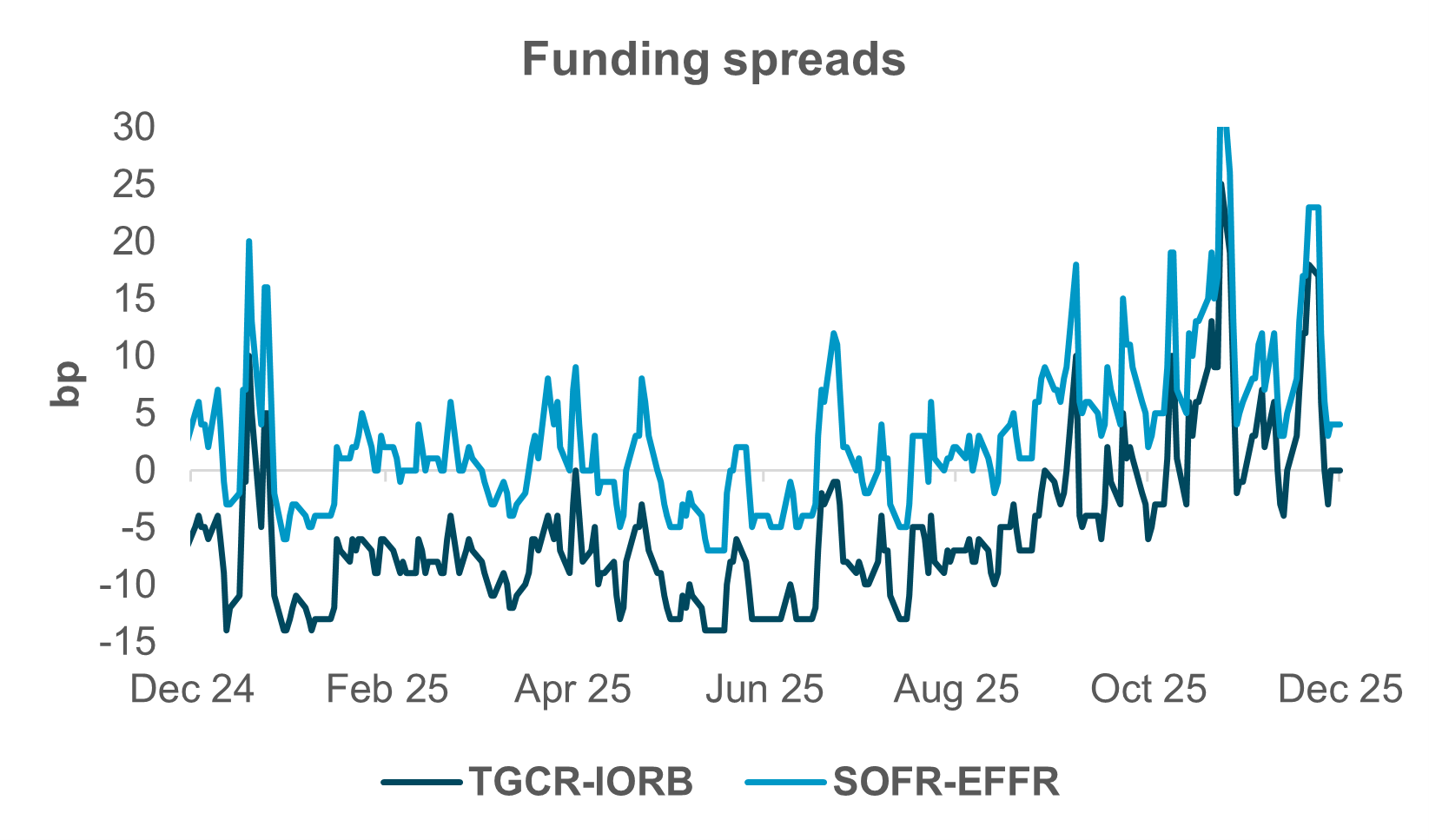

The need to maintain ample reserves (rather to let them slip into a scarce state, in which rate control would be severely compromised) is important. An ample reserve regime is defined as one in which changes in reserves (say, lower) lead to upward movements across the constellation of front-end interest rates. As Exhibit #2 shows, funding spreads have been on the rise since the end of August, corresponding to the concurrent decline in reserves. The chart also shows a pronounced rise in funding rates at the end of 2024, a period that most observers would describe as featuring abundant reserves. If reserves are now merely ample, then funding pressures at the end of this year could be even more acute than last year. Hence the need for vigilance and preparedness going forward.