In the Gulf Cooperation Council (GCC) and other majority-Muslim regions, Shariah-compliant financial instruments have evolved from a niche offering to a core capital markets solution. Islamic financial products, including Sukuk (asset-backed financial certificates) and the underlying financial transactions, like Murabaha (syndicated cost-plus sale facilities), have become increasingly popular, evolving in line with cross-border needs and regulatory developments. This has led to several key trends:

-

Driven by their clear structure, fixed returns and compliance with Shariah principles, Islamic financial instruments have become a popular mechanism for addressing funding requirements on capital markets.

-

The increased use of Shariah-compliant instruments has led to a need for operational infrastructure to support cross-border execution, central securities depositary (CSD) integration and post-trade integrity.

-

Agents*, which enable scalable, repeatable and audit-ready Islamic finance have become – when orchestrated effectively – a crucial element.

Islamic finance – a system of financial transactions conducted in accordance with Shariah principles – has gone from a regional segment to a global asset class. Islamic financial products now account for $5.4 trillion in assets and are set to grow to $9.75 trillion by 2029.1

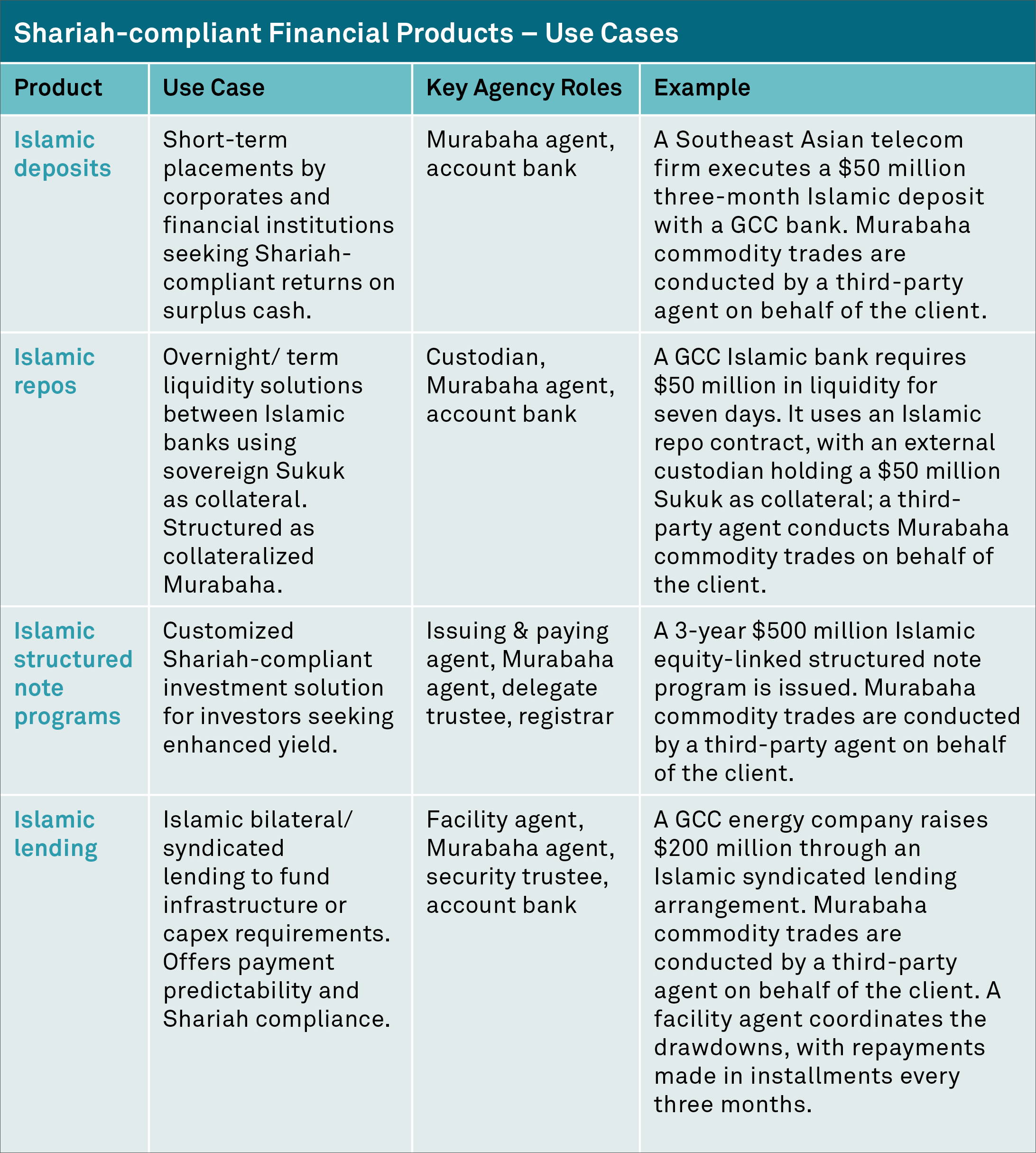

A Murabaha financing transaction – in which the seller and buyer agree on the price of an asset in advance – has emerged as a key element of Shariah-compliant finance. This type of financing is an ideal solution for issuers and investors seeking Shariah-compliant, asset-based financing alternatives.

The structural and strategic factors driving the use of Murabaha financing

Murabaha’s cost-plus sale structure offers distinct advantages for those looking to comply with Islamic finance principles. It has a structural versatility that provides treasurers and deal arrangers with price predictability while also limiting risks. This is especially valuable given interest-rate volatility. The resulting transparency also supports effective liquidity and capital management for stakeholders and Shariah Supervisory Boards.

From a regulatory perspective, Murabaha transactions benefit from clearer accounting treatment under International Financial Reporting Standards (IFRS) and Basel frameworks, which can help reduce capital uncertainty for financial institutions and help maintain robust liquidity ratios – critical factors for banks and sovereign issuers. Additionally, subject to the tax rules of the relevant jurisdiction, Murabaha profit margins may benefit from more straightforward withholding tax treatment than profit sharing models, which can support more efficient cross-border implementation.

Operationally, Murabaha’s modular and repeatable structure supports scalable financing programs, whether for deposit-taking, syndicated or bilateral lending, repos or Sukuk issuance. This replicability is vital as market participants increasingly seek to raise funds in international markets while adhering to complex multi-jurisdictional regulatory requirements.

Regulatory momentum and market evolution

Regulators across the GCC and other majority-Muslim regions are actively refining frameworks to support the growth of Islamic financial instruments. Examples of regional efforts to deepen liquidity and expand the investor base include the United Arab Emirates’ introduction of the T-Sukuk, a Shariah-compliant financial instrument denominated in the dirham, the country’s currency, and Saudi Arabia’s enhanced investor access through cooperation with Euroclear.

In addition, the International Islamic Financial Market (IIFM) continues to standardize the documentation required for collateralized Murabaha, and other instruments like Wakala placements and Islamic repos, with the aim of reducing cross-border friction and decreasing the lead time on deal execution.

The role of agency infrastructure: Enabling seamless execution

As Murabaha-based structures gain traction, robust agency support is becoming increasingly important to ensure efficient and reliable transaction execution. Trusted intermediaries who can coordinate across time zones, help ensure documentation integrity and facilitate timely cash flows for complex capital market transactions are crucial for successful issuance and post-trade transaction management.

Agents play a crucial role in carrying out compliant transactions, as they can be responsible for a number of critical tasks. There may be many different types of agents, including:

-

Murabaha agent: Helps ensure Shariah-compliant execution of asset purchase and deferred-sale transactions, while maintaining audit trails and operational clarity.

-

Issuing, paying and settlement agent: Manages International Securities Identification Number (ISIN) allocation, oversees deal closing and interfaces with central securities depositaries, including Euroclear, Clearstream, CMU and DTCC. Ensures lifecycle events take place seamlessly.

-

Facility agent and account bank: In their respective capacities, administer their portions of the syndicated loan mechanics, including managing drawdowns, notices and lender communications, and ensuring asset segregation and anti-money laundering (AML) compliance for the accounts they maintain.

-

Delegate trustee and registrar: Represents investor interests, enforces deal covenants and maintains accurate investor records.

-

Custodian/collateral (security) agent: Safeguards Shariah-compliant assets, monitors collateral eligibility and manages substitution rights and collateral release protocols.

This comprehensive agency ecosystem can help transform complex Islamic finance transactions into scalable, repeatable and audit-ready market flows, potentially reducing operational risk and enhancing investor confidence.

Looking ahead: Strategic growth and client opportunities

As Islamic finance continues to evolve across the Middle East, the opportunities for innovative financial solutions are expanding in tandem with the region’s broader economic transformation. The current range of regional financial offerings – including Murabaha financing, structured note programs, securitizations, project finance and private credit – is broad enough to support the ambitious growth targets of Saudi Arabia’s Vision 2030, the country’s blueprint for transformation, emphasizing real-asset investment, private-sector participation and innovation in the tourism, logistics and renewable energy sectors.

From a market structure perspective, emerging trends such as fintech integration for faster execution and tokenized Murabaha structures to facilitate cross-border liquidity are also likely to gain traction, presenting new opportunities for market participants to capitalize on this evolving area of Shariah-compliant financial instruments.

As issuers look to participate in the region’s dynamic growth and embrace new financial instruments, having an experienced partner is critical. Agents like BNY have the operational infrastructure and market insight necessary to help clients with both domestic and cross-border transactions. By providing tailored support, robust infrastructure and in-depth understanding of regional trends, we help issuers navigate complexity, build investor confidence and unlock new avenues for strategic growth.

1https://www.greenwich.com/corporate-banking/unlocking-growth-islamic-finance-sees-global-expansion

*Agents include paying agents, Murabaha agents, calculation agents, custodians, etc.