Warsh nominated to be Fed chair

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 4 minutes

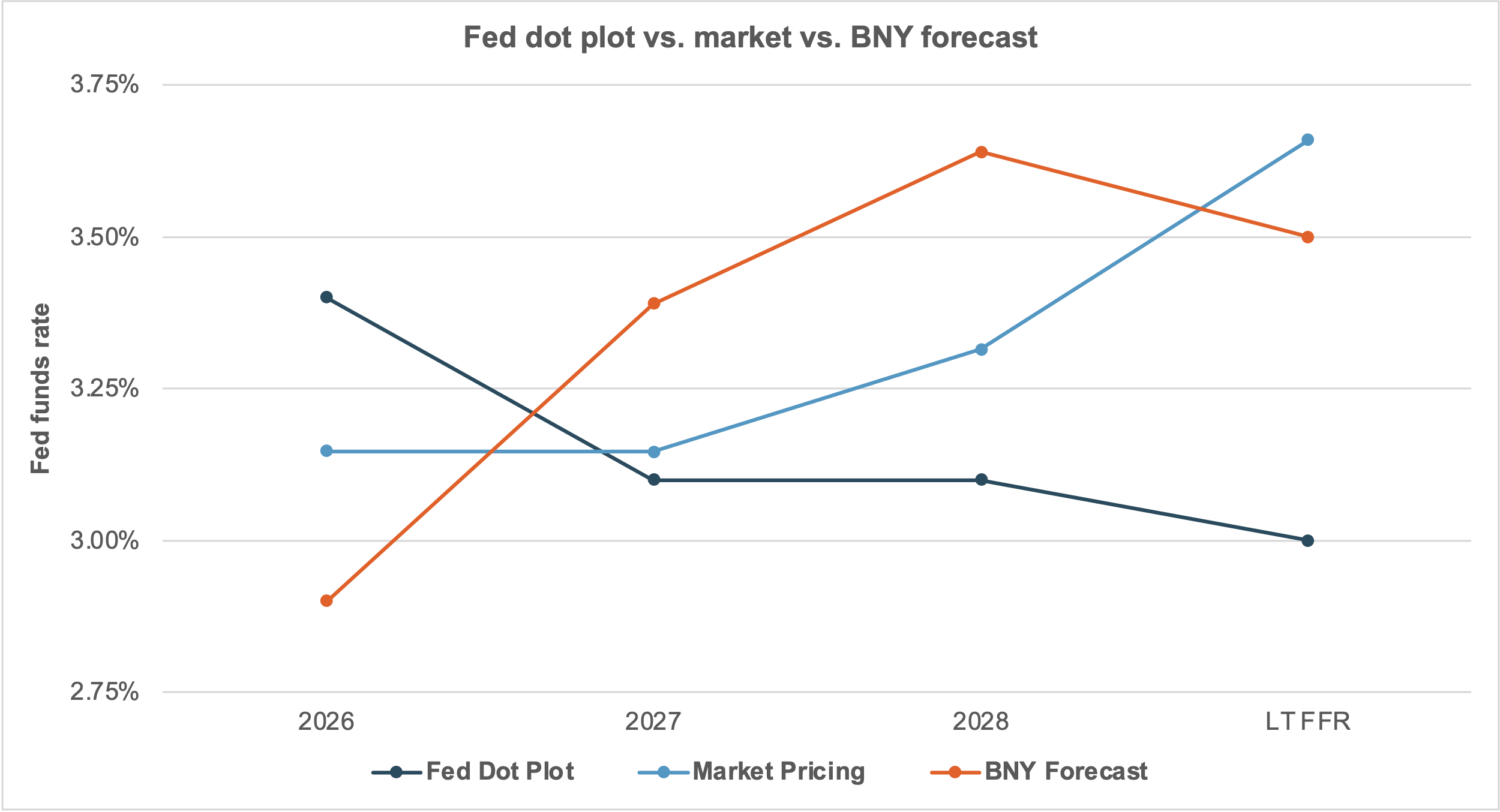

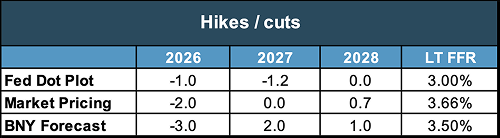

EXHIBIT #1: ALMOST NO CHANGE IN RATE EXPECTATIONS

Source: BNY Markets, Bloomberg

After months of speculation, shifting odds and much discussion, Kevin Warsh, one of the original frontrunners for the job, was nominated by President Trump to be the next Fed chief. Once confirmed, a process that may or may not be smooth sailing, Warsh will assume the Board of Governors seat currently held by Stephen Miran, himself a Trump appointee whose term formally expired on January 31 but will continue until Warsh is confirmed.

Confirmation at this juncture doesn’t look like it will be a simple matter of the Senate giving the pick a rubber stamp. Senator Tom Tillis, outgoing Republican from North Carolina and a member of the Banking Committee, has vowed that until the Department of Justice’s investigation of the Fed headquarters refurbishment is concluded, he will not vote to advance any Fed nominees, including Warsh, whom he nevertheless described as “a qualified nominee” with the “deep understanding of monetary policy.” Although he declared himself “pleased” by Warsh’s nomination, Senator Tillis reiterated his intent to hold off on any nomination vote. This will leave Warsh short of the votes needed to pass

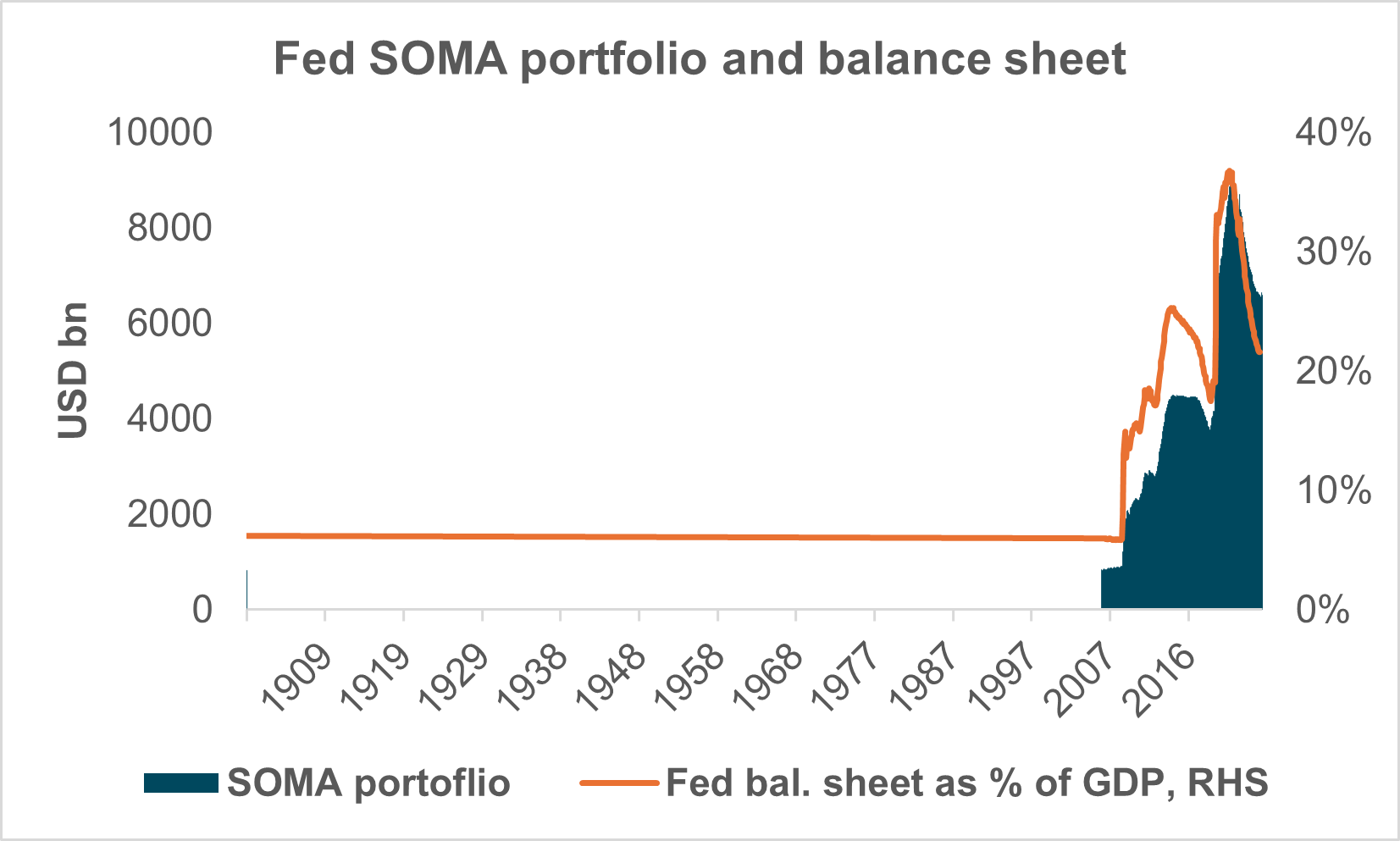

EXHIBIT #2: BALANCE SHEET DYNAMICS SINCE THE GFC

Source: BNY Markets, Federal Reserve Board of Governors, Bloomberg

Aside from the confirmation politics, investors have been trying to gauge what a Warsh Fed would look like. He has a long paper trail, having served as a Fed governor from 2006 through 2011, a period that included the GFC and the Fed’s first foray into quantitative easing. Much has been discussed about whether he is a hawk or a dove. During his first stint on the FOMC, he advocated raising rates on the eve of the 2008 crisis and again in 2009, even with the unemployment rate near 10%. In 2011, he ultimately resigned in protest over the second round of post-GFC quantitative easing, known as QE2.

This might make him seem like an odd choice for an administration advocating rate cuts, but he appears to have changed his stripes in recent years, essentially arguing that higher U.S. productivity, through deregulation and AI-led growth, would allow rates to be much lower than they are now without stoking inflation. The market hasn’t yet moved in either direction, perhaps because his confirmation is still uncertain. The implied path for the federal funds rate this year is, as of this writing, almost identical to where it was before last week’s FOMC meeting. Indeed, rates markets seem to be moving at the moment more on broader market swings and volatility than on the eventual Fed transition. Of course, a single voter, even the chair, cannot make rate policy alone – they must bring the Committee with them.

Warsh has made himself clear on another aspect of monetary policy: the balance sheet. Calling it “bloated,” he has advocated reducing its size. This would certainly represent a shift in current Fed policy. QT ended last October, and in December, balance sheet expansion resumed through reserve management purchases (see here), aimed at stabilizing funding markets. This is not QE in the sense that it is aimed at ensuring sufficient market liquidity now that reserves have reached an ample level. Reducing the size of the Fed’s System Open Market Account (SOMA) portfolio from its current 22% of GDP, or some $6.6tn, would again need to be endorsed by a majority of the Open Market Committee, similar to a change in rates. Here again, Warsh must shepherd the members to his side.

Warsh has also advocated for a “new accord” between the Treasury and the Fed. As he described it in a CNBC interview last summer: “If we have a new accord, then the Fed chair and the Treasury secretary can describe to markets plainly and with deliberation, ‘This is our objective for the size of the Fed’s balance sheet.’” What this means exactly is unclear, but it could shape debt dynamics and monetary policy for years to come under a Warsh Fed.

The recent FOMC concluded without many fireworks, as expected. The statement veered slightly hawkish. Economic growth was characterized as “expanding at a solid pace,” rather than the “moderate” pace referenced in the previous meeting. The statement described the labor market as “showing signs of stabilization.” The post-meeting press conference was almost straight down the middle. Also, as we expected, many questions dealt with Fed independence, the DOJ investigation, and the Lisa Cook hearing before the Supreme Court the week before the meeting. Unsurprisingly, Chair Powell declined to address most of the issues.

Regarding rates, the market has barely reacted, pricing in only a few bp of additional easing by December but essentially seeing two cuts this year. We still maintain our call for three cuts, based on our view that the labor market is in danger of transitioning from essentially zero jobs growth to something worse; this was the reasoning for a cut that Governor Christopher Waller offered in his dissent. This week would have offered a pivotal test of our view with several labor market data releases on the schedule, including the January NFP. However, due to the shutdown, which we hope is short-lived, the Labor Department has indicated that these data will be delayed until after the shutdown ends.

We aren’t as convinced as Waller on inflation, about which he is less concerned, arguing that ex-tariff inflation is just around 2%. We aren’t sure that tariff pass-through is completely over, and we remain concerned about the level of services inflation ex-housing. Nevertheless, we think that the Fed would lean more toward easing rates if the labor market deteriorates, even if overall core PCE is above 2%.