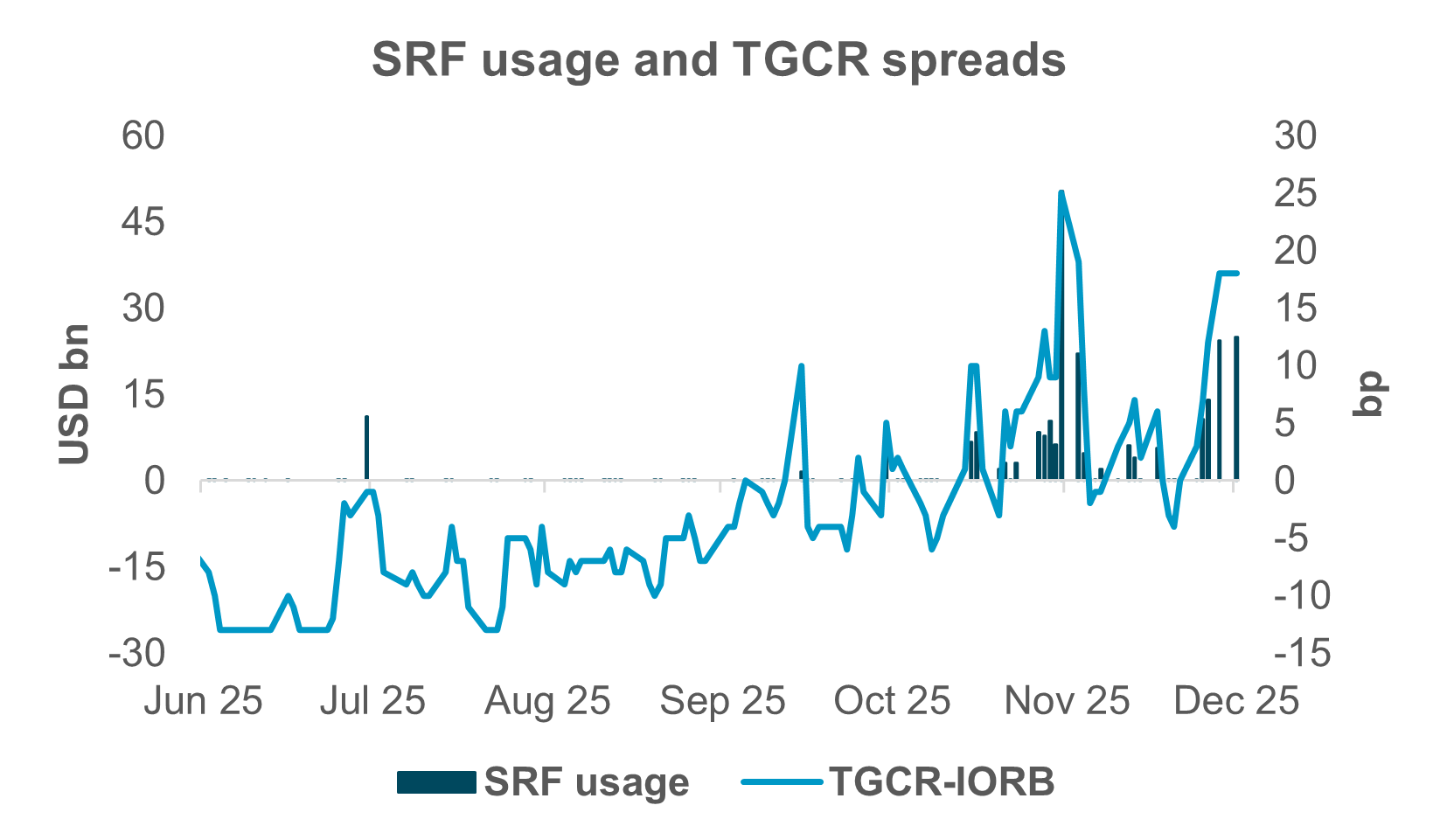

The Fed’s standing repo facility (SRF) was tapped for $26bn over the course of the day on December 1, making it the largest daily uptake since $50bn in usage on October 31. Also on December 1, the triparty general collateral repo rate (TGCR) rose to 18bp over the interest paid on reserves at the Fed (IORB). Both developments speak to tightening in funding markets heading into year end. The current situation is hardly a surprise, as we have commented on recently (see here and here).

However, on November 28, the effective federal funds rate moved up a basis point, from 4.88% to 4.89% with TGCR-IORB spreads at 18bp. This illustrates the Fed’s discomfort with such upward pressure on repo spreads. Tight liquidity conditions in the funding markets can ultimately lead to upward pressure on the Fed’s operating target, threatening rate control.

While funding pressure has materialized around specific dates (month- and quarter-ends, settlement days, tax dates), there is the risk it will happen more frequently, including on otherwise uneventful days. This is why the Fed has indicated it will eventually need to resume increasing its balance sheet. As other balance sheet liabilities increase (namely, currency in circulation), reserves will fall, exacerbating tight liquidity conditions in the funding markets. Reserves are currently reckoned to be no longer abundant, but merely ample. Reserve management operations will eventually feature in the Fed’s toolkit, although pinpointing when they might commence is difficult.

Exhibit #1 shows the daily usage of the SRF over the past half year and illustrates how its usage increases when funding is stressed. It’s worth noting that the Fed would probably prefer to see the SRF used more frequently and in larger sizes than it currently is, reducing the eventual need for open market operations. Moving to the latter presents a potential communications problem for the Fed, which would have to make it clear that such operations are not a return of quantitative easing, but are indeed reserve management policies. The SRF’s attractiveness suffers due to both internal and executive stigma, as well as a lack of central clearing.

We wrote about the Fed’s upcoming monetary policy decision last week and will write a formal preview of the FOMC next week. However, it’s worth asking here whether the Fed would announce reserve management operations at next week’s gathering. We think it’s unlikely to occur so soon. For one thing, there have so far been only vague references to such market operations in the Fed’s public communications. We would have expected more specific guidance if they were to commence soon. Furthermore, with funding market strains still mostly limited to specific dates, it could be a bit premature to set up such operations. Nevertheless, we expect them to begin early in 2026, as funding markets gradually tighten further.