Volatility Doesn’t Scare Investors

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

We end January with a bang. The volatility in FX, commodities and stocks stands out. Reversals in gold, silver and crypto were notable but didn’t change the fact of substantial price gains across risk assets as we start 2026. Financial conditions are easier globally even with central bankers delivering “on hold” decisions in the U.S., Canada, Brazil and Sweden. The month’s most notable shift, which continued this week, was in flows to emerging markets (EM), with gains in their stocks and FX holdings now outpacing those in developed markets, according to iFlow data. Pullbacks in metals curtailed some of the FX moves in AUD and ZAR markets and moderated recent U.S. dollar weakness. The focus last week started with FX intervention risks in JPY and KRW but ended with Trump’s nomination of Kevin Warsh as the next Federal Reserve chair. Trade and geopolitical concerns are ever present, with the USD becoming a macro focus for volatility across markets.

Five focus items dominate this week:

1) Geopolitics. Markets are watching oil and natural gas, with Ukraine–Russia and U.S.–Iran talks ongoing. Thailand’s election, where the opposition leads in polls, and Japan’s upcoming election will also be closely watched in FX.

2) Supply. U.S. investment grade issuance topped $205bn in January, with February expectations at $185bn. Add in the Treasury’s quarterly borrowing plans this week, and coupon bond supply will test fixed income appetite.

3) Central banks. The rate decisions from the RBA, ECB, BoE, RBI and others will test how central banks align with market optimism about global growth, inflation and risk.

4) Q4 earnings. More results from big tech. Amazon and Alphabet will set the tone for AI investment. With over 20% of S&P500 reporting, investors will be watching for signs of adoption and margin strength.

How hot is the U.S. economy?

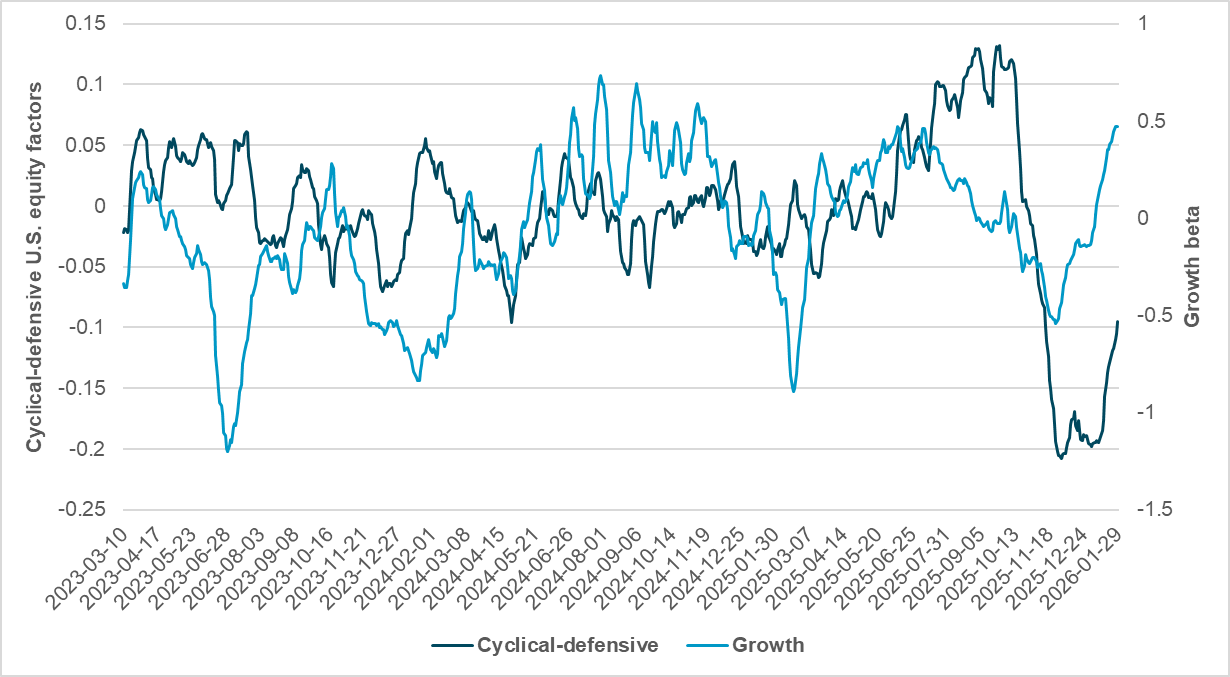

EXHIBIT #1: IFLOW U.S. EQUITY GROWTH BETA VS. CYCLICAL-DEFENSIVE

Source: BNY, Bloomberg

Our take: The economic surprise index for the U.S. in January is positive. Regional Fed surveys point to labor and growth optimism, and our U.S. equity factors point to flows supporting this outlook. The last two months of flows show investors have been aggressively repricing U.S. economic growth factors. According to our data, there is room for more optimism, but it looks like it will require something new to regain momentum.

Forward look: This week’s U.S. data will matter, with ISM and jobs clearly key, along with further Q4 earnings and forward-looking Q1 guidance. Also notable is the sharp drop in consumer confidence from the Conference Board last week, alongside significant layoff plans from big companies. The Friday jobs report looks critical to expanding the current uptrend in risk and equities for the U.S.

The role of financial conditions in supporting growth is one key feedback loop and measure of success for current policy mixes. The Trump administration noted the S&P 500 breaking above 7,000 as a sign of success, so investors will again be watching equities as a driver of potential policy shifts. Given the one-day, over 20% unwind in silver, the ongoing rotation from big tech to small caps, and persistent rates with the 10y above 4.20%, markets are challenging the resilience of January’s rally as we begin a new month under renewed uncertainty.

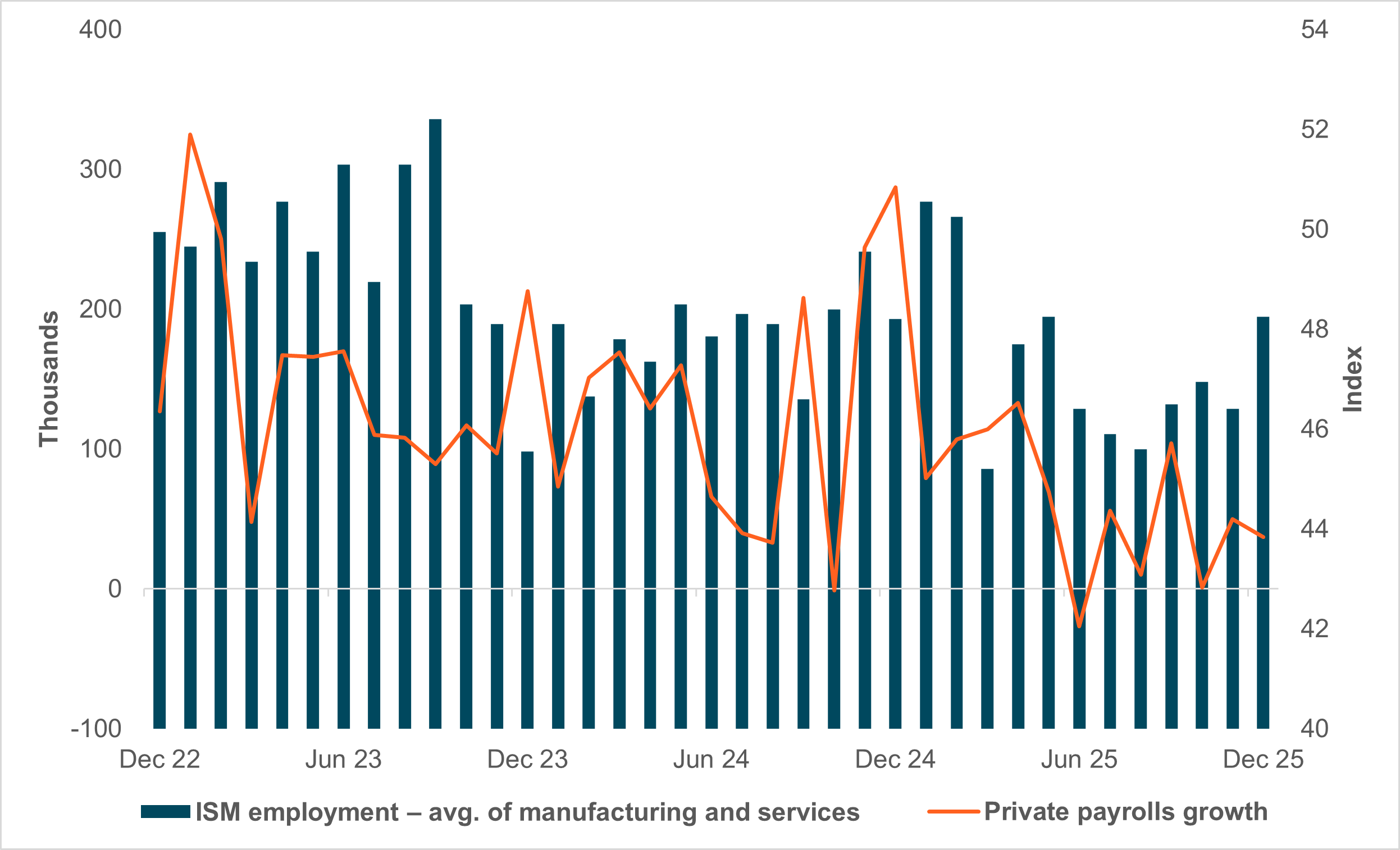

U.S. jobs remain key to rates and the dollar

EXHIBIT #2: U.S. PRIVATE EMPLOYMENT GROWTH

Source: BNY, Bloomberg

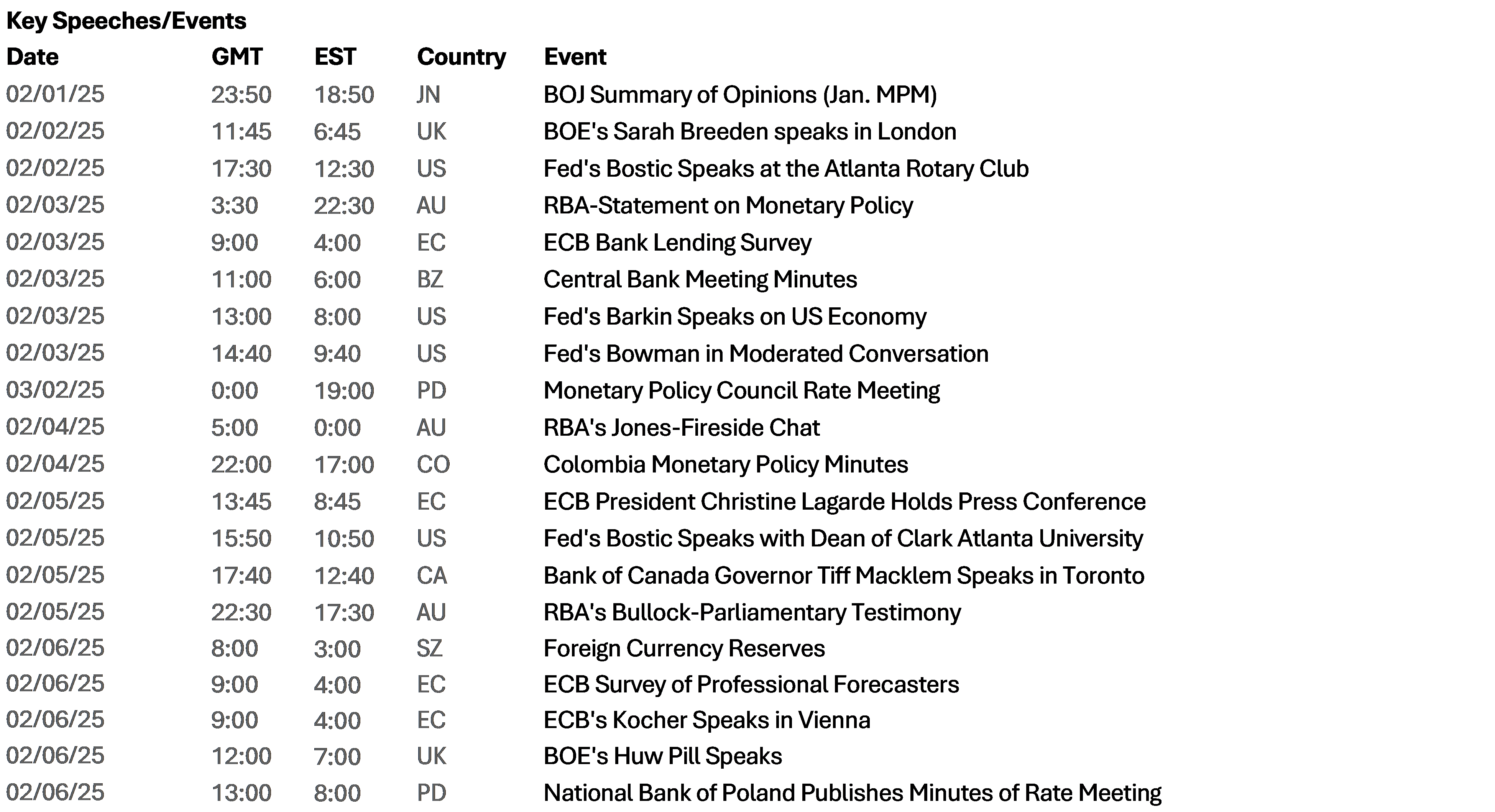

Our take: It’s going to be another action-packed week, assuming a long government shutdown is avoided. The data calendar is heavy – especially on the labor front. Furthermore, the Fed’s blackout period has ended, and we’re likely to get plenty of reactions to the naming of Fed chair nominee Kevin Warsh. Corporate earnings season will be in high gear, as well.

Forward look: On the data front, the first week of the month is jobs week. We start out with the December JOLTS data on Tuesday. Recent prints have shown a significant decline in job openings, adding to our concern over the labor market. On Wednesday, we’ll receive the ADP report and on Friday, of course, nonfarm payrolls. Expectations for NFP are for 65k jobs, after December’s 50k print. Given the Fed’s recent rate hold and the central bank’s relatively sanguine outlook for both inflation and the jobs market, we’re primed to see if the employment data this week challenge the benign view.

ISM surveys will be out as well, with the manufacturing poll released Monday and the non-manufacturing report on Wednesday. Michigan Consumer Sentiment is also released Friday. Recent survey data has painted a more optimistic picture than we’ve seen previously.

Canada is not spared this week either. Jobs data are also released this Friday, while Bank of Canada Governor Tiff Macklem will speak in Toronto on Thursday. His remarks follow last Wednesday’s Governing Council meeting, which resulted in no rate change but conveyed a cautious and uncertain outlook.

We expect a number of Fed speakers this week to reflect on last week’s policy hold and comment on the chair nomination. Bond markets could also respond to the Treasury’s quarterly refunding announcement. Bill supply is expected to stay above 20% of all debt issued, and we’re looking for any indications of changes in coupon supply as well.

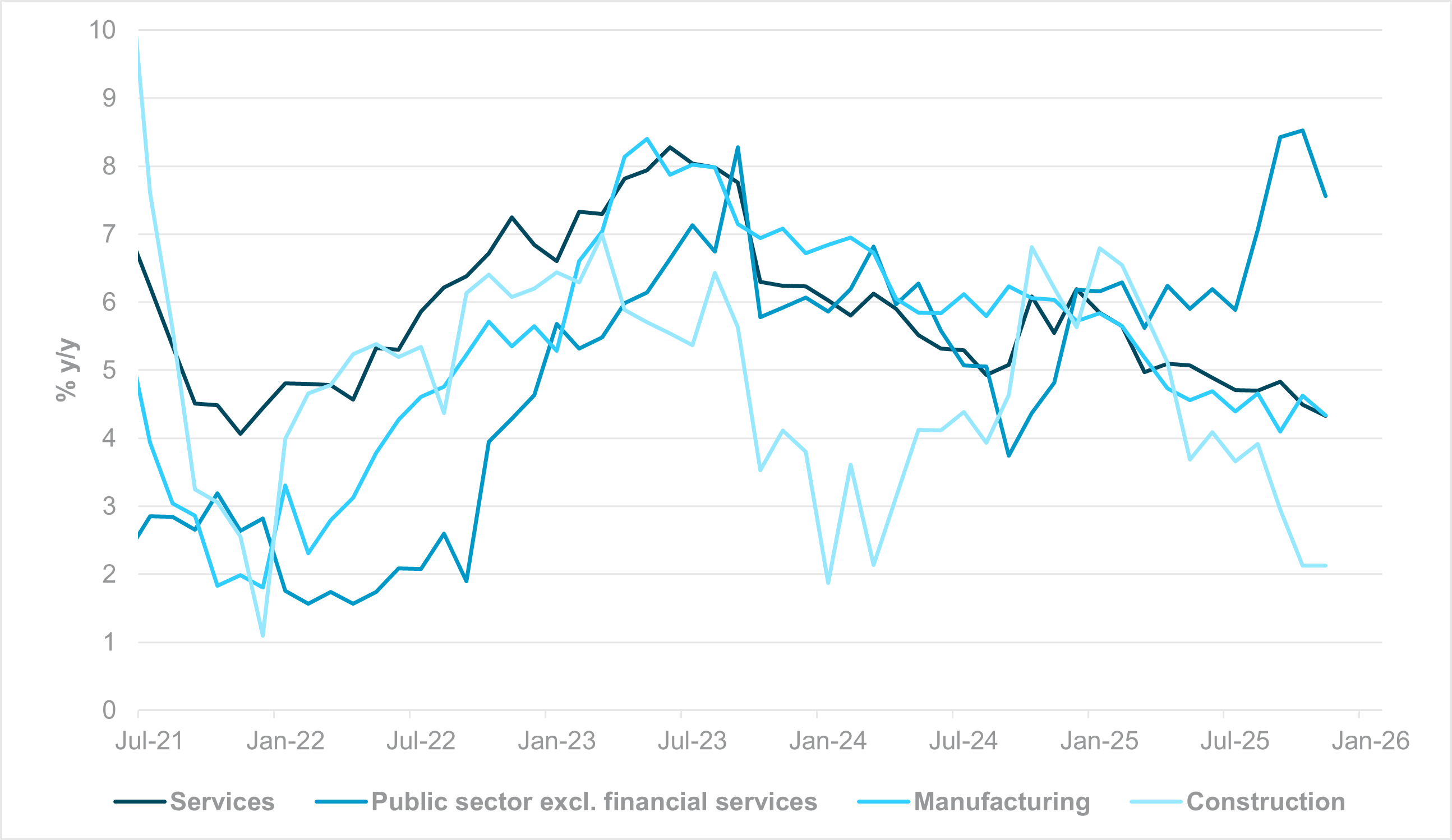

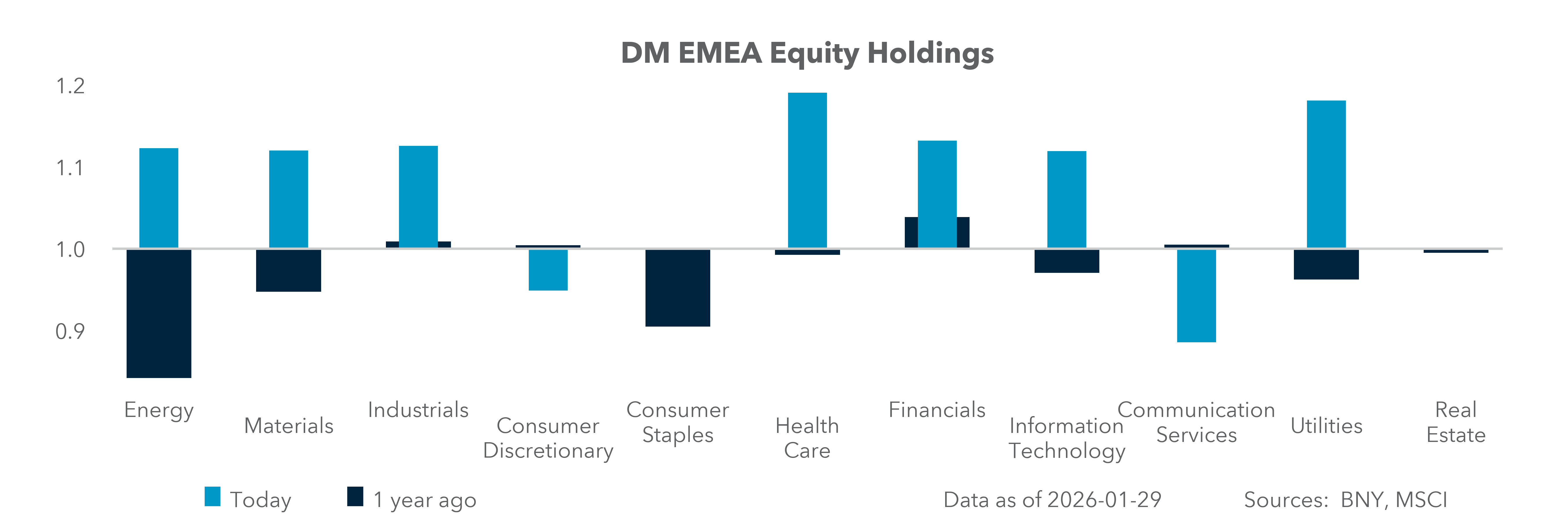

EMEA: GBP and EUR may struggle to justify safety status as key decisions loom

EXHIBIT #3: WAGE GROWTH DECOMPOSITION – U.K.

Source: BNY, Macrobond

Our take: Last week marked a notable shift in European central bankers’ attitude toward currency appreciation. As the U.S. dollar fell through key technical levels, policymakers’ rhetoric moved away from a singular focus on inflation vigilance and toward concerns that sustained exchange rate strength could begin to exert downward pressure on inflation.

The market will closely scrutinize the European Central Bank’s (ECB) upcoming decision for signs of alignment with the message recently delivered by the Riksbank. Sweden’s central bank recently moved away from advocating a gradual appreciation of the Swedish krona and instead highlighted the downside inflation risks associated with currency strength. Should similar concerns be formalized in the ECB’s communications, this would amount to a tacit acknowledgment that the pivot toward heightened inflation vigilance late last year may have been misplaced. For the time being, inflation readings remain broadly in line with expectations, and preliminary January data do not indicate any material downside risks.

Domestic demand continues to show resilience, despite mixed signals from recent PMI surveys. However, developments in January also underscored the potential for trade tensions to re-emerge at short notice, threatening stability within Europe’s export framework. In this context, competitiveness pressures linked to China, alongside an overvalued exchange rate, would further complicate the outlook. One mitigating factor may be that policymakers across Asia increasingly recognize the risks associated with excessive currency undervaluation, with a degree of alignment among regional central banks around the need for currency strength. Whether such dynamics can be sustained along the euro’s trajectory, however, remains uncertain.

For the Bank of England (BoE), the situation differs somewhat. Sterling has moved above 1.40 against the U.S. dollar for the first time in years, yet the U.K. has historically exhibited limited sensitivity to inflation dynamics from the exchange rate. The relationship has tended to be asymmetric. Currency strength has typically generated little pass-through disinflation while supporting domestic demand. By contrast, policymakers have historically been more willing to tolerate a weaker exchange rate to support exports or manage growth expectations during periods of cyclical deterioration. In a stagflationary environment, the exchange rate itself is therefore likely to play only a limited role in the transmission of monetary policy.

As a result, we expect the Monetary Policy Committee to remain focused on developments in domestic wage growth and broader labor market conditions. The signals from the latest data remain mixed at present. Based on the most recent wage growth decomposition (Exhibit #3), public sector workers continue to record the strongest pay increases, with annualized wage growth in the high single digits as of late last year. By contrast, wage growth in sectors such as construction has begun to flatten. Wage growth across the broader services sector – an important input into U.K. inflation expectations – remains well above 4%, with only very modest signs of deceleration so far. Against this backdrop, there is insufficient evidence for the more hawkish BoE members to materially revise their stance. Governor Andrew Bailey, who continues to act as the key swing voter, is also likely to maintain a cautious approach, consistent with his recent communications.

Forward look: The remaining central bank decisions in Central and Eastern Europe, particularly in Poland and Czechia, will be a key test of the resilience of carry trades in EMEA. In Poland, another rate cut is possible, although we retain serious misgivings about the direction of policy in an environment characterized by a strong fiscal impulse. Recent market developments have highlighted that highly correlated moves across asset classes can be damaging for high-yielding economies, whether returns are assessed in nominal or real terms. While Poland benefits from relatively subdued inflation dynamics, wage growth pressures cannot be overlooked and appear increasingly structural in nature.

More broadly across the region, currencies are sufficiently strong to deliver a meaningful disinflationary impulse and to act as a restraint on broader economic conditions. The broader challenge is that such positioning is becoming increasingly difficult to sustain. Carry trades are widely held but are no longer seeing any additions, largely due to FX valuation constraints. This asymmetry suggests that episodes of correlated selloffs, such as those observed recently, are less likely to be repeated. However, it also raises the risk that central banks, including Poland’s, could be easing policy into an environment of weakening currency performance.

This consideration may partly explain why South Africa refrained from cutting rates last week and reflects the broader stance adopted by higher-yielding central banks across the Asia-Pacific (APAC) region. While incoming data will continue to guide policy decisions, the current macroeconomic environment remains exceptionally volatile. For emerging markets in particular, maintaining a degree of buffer through positive real rate differentials continues to be an important policy consideration.

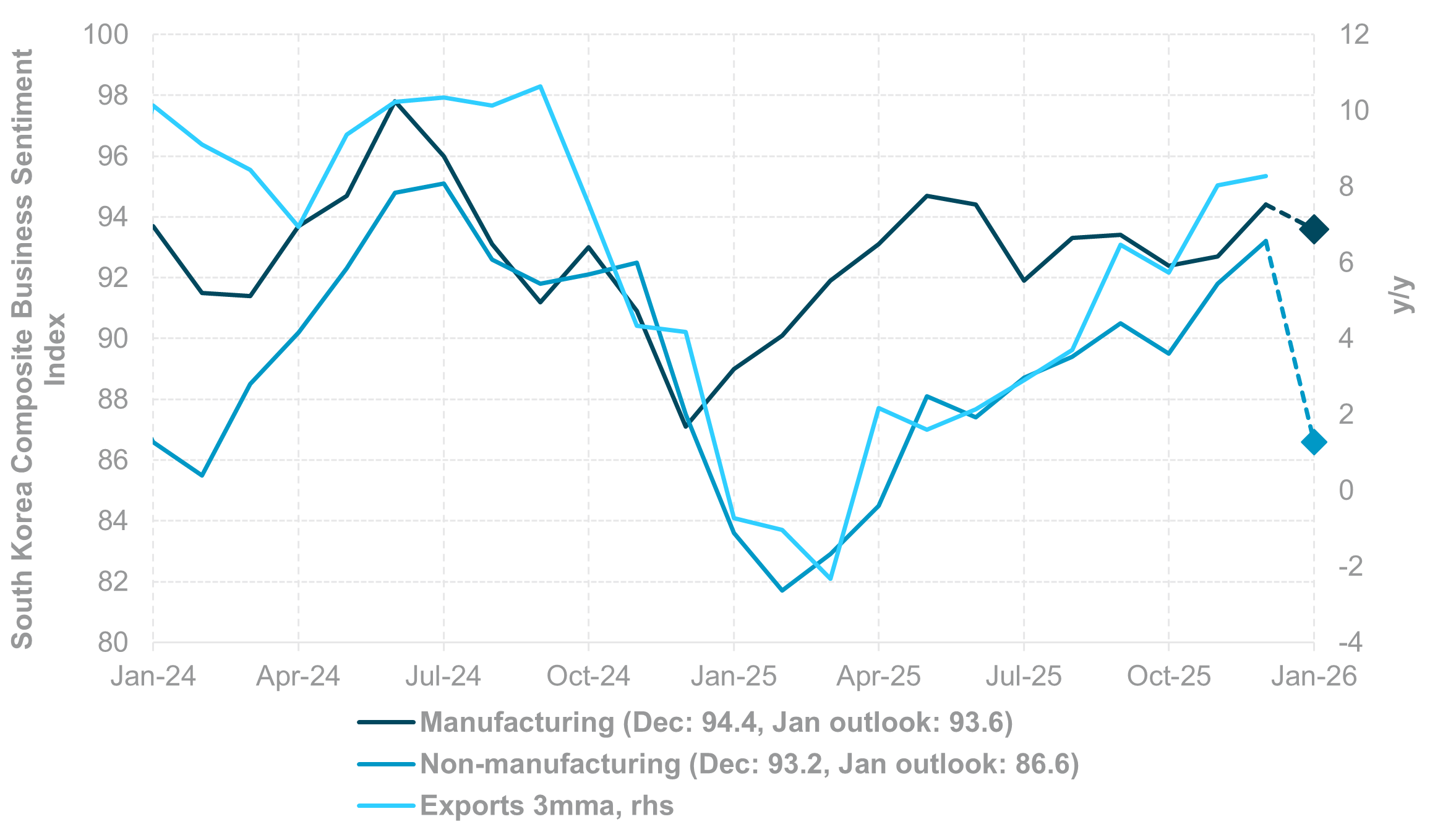

APAC: Growth and inflation to test RBA and RBI policy meetings

EXHIBIT #4: APAC PMI MANUFACTURING SENTIMENT RECOVERY MOMENTUM

Source: BNY

Our take: Key APAC data releases include the regional PMI, inflation and January foreign reserves. Additional noteworthy reports are South Korea’s balance of payments; Indonesia’s export figures and Singapore’s retail sales for December; New Zealand’s Q4 unemployment rate; and Japan’s household spending and leading economic indicators, also for December.

The latest PMI results for January will offer valuable insights into whether the recent positive trends can be maintained, particularly after a synchronized expansion, with all regional PMI above 50. This was fueled by strong recoveries in South Korea (50.1), Taiwan (50.9), and the Philippines (50.2). The ASEAN region also saw a high PMI at 52.7.

Inflation rates for January will be examined closely due to ongoing upward pressure, highlighted by Indonesia’s headline inflation reaching 2.92%. In contrast, Thailand continues to experience deflation, with December marking nine straight months of negative y/y inflation at –0.28%. Inflation risks are skewed to the upside, partly reflecting a more than 10% rise in crude oil prices in January. That said, absolute inflation levels remain low across most of the region and are unlikely to be enough to shift the prevailing dovish-to-neutral monetary policy stance.

South Korea’s December balance of payments will be important in gauging the scale of outbound domestic equity flows, which have weighed on the South Korean won. Domestic investors purchased $18bn and $12.5bn of foreign equities in October and November 2025. Meanwhile, New Zealand’s Q4 labor market data will be closely scrutinized as a key input into the Reserve Bank of New Zealand’s February policy decision.

The Reserve Bank of Australia and the Reserve Bank India will meet this week. The RBI faces a tough meeting, weighing the need to boost growth against pressure from depreciating domestic assets prices. February will be active, with central bank meetings in New Zealand (February 18), Indonesia and the Philippines (February 19), Thailand (February 25), and South Korea (February 26).

Forward look: While we are confident in the AI-led growth recovery and continued capital inflows, geopolitical and trade tensions, along with stretched market technicals, pose downside risks to APAC assets in the near term. Note that market liquidity may be thinning out into Lunar New Year in the second half of February. Many APAC equity indices are in technically overbought territory, while the USD appears technically oversold against Asian currencies. Factoring domestic macro fundamentals, capital flows and market technicals, we maintain that THB and SGD are expensive. KRW, TWD, CNH, MYR and IDR offer value, while INR remains under depreciation pressure.

Elsewhere, Thailand and Japan will hold general elections on Sunday. At the time of writing, polls in Thailand suggest that support for the opposition People’s Party rose to 34.2%, while Prime Minister Anutin Charnvirakul’s Bhumjaithai Party trailed with 22.6%. No party is expected to win a majority, making coalition bargaining inevitable. In Japan, Prime Minister Sanae Takaichi, in a new alliance with the Japan Innovation Party, is expected to secure election majority.

Beyond that, market focus will shift to China’s 14th National People’s Congress (NPC) and the Chinese People’s Political Consultative Conference (CPPCC) scheduled for March 4 and 5, where official macroeconomic target for 2026 will be released.

Looking ahead, markets are entering a phase where policy signals, labor data and geopolitical developments will interact more forcefully with positioning and liquidity. The durability of the risk rally hinges on whether U.S. employment and ISM data validate expectations of resilient growth without reigniting inflation concerns.

Central bank meetings across the U.S., Europe and APAC will test the market’s confidence that policy can remain on hold while financial conditions stay accommodative. At the same time, heavy sovereign and corporate supply will challenge fixed income appetite and shape rate volatility.

For currencies, the U.S. dollar is reasserting itself as a macro barometer, sensitive to both growth surprises and political risk. Emerging markets remain a relatively bright spot, but crowded carry and valuation constraints argue for selectivity.

Overall, investors should expect higher cross-asset volatility, favor dynamic risk management, and remain focused on data-driven confirmation as markets transition from optimism toward validation.

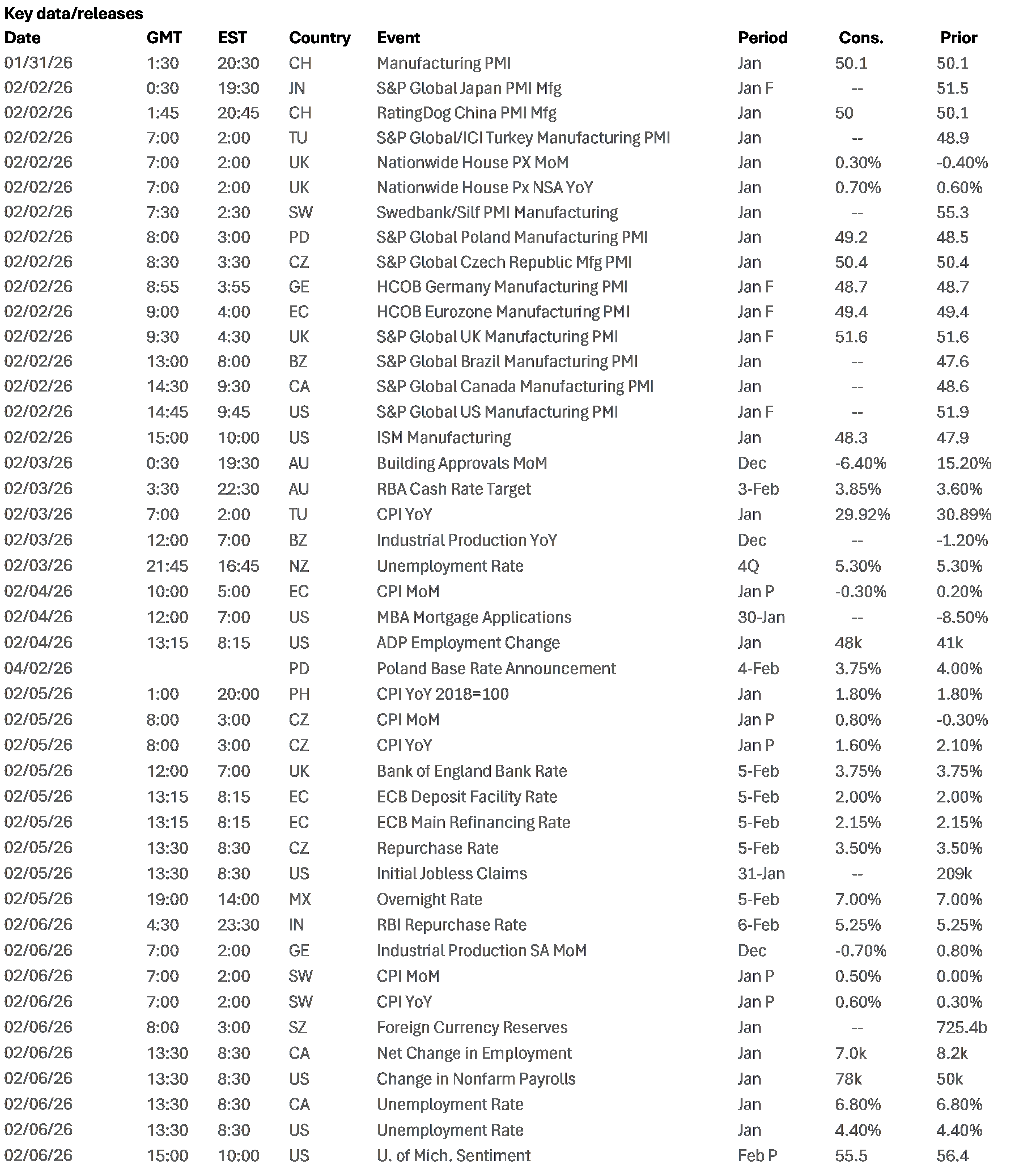

Central bank decisions

Australia, Reserve Bank of Australia (RBA) (Tuesday, February 3): The RBA is expected to resume its tightening cycle with a 25bp hike to 3.85%. The pivot has been in the works for some time, as inflation risk has moved back up the agenda. Strong December CPI figures and robust employment growth have effectively confirmed the RBA’s evolving assessment. However, we are cautious in interpreting the move as the start of an aggressive cycle. Markets are currently pricing in only two hikes for 2026. AUD’s broad strength has also tightened financial conditions, which the RBA is likely to emphasize as APAC FX adjusts valuations.

Poland, Narodowy Bank Polski (NBP) (Wednesday, February 4): The NBP is expected to resume easing, cutting the policy rate to 3.75% despite concerns over financial conditions and a strong fiscal impulse. However, we acknowledge that there is room for cuts with inflation falling to 2.4% for December and not registering any sequential growth. However, annualized wage growth continues to surge, hitting 8.6% y/y in December despite softer employment growth. Balancing wage pressures against soft labor market demand remains a challenge for policymakers globally. The NBP appears focused on growth risks, especially given the current exchange rate levels.

U.K., Bank of England (BoE) (Thursday, February 5): The BoE will likely keep rates on hold at 3.75% as inflation figures continue to frustrate efforts to ease rates. We still see potential scope for the MPC to cut further, but presently the wage and headline inflation figures remain too high for comfort. Governor Bailey remains the swing voter and has given no indication that inflation tracking the lower end of expectations. A clear path toward 3.0% y/y in CPI is probably required for the next cut.

Eurozone, European Central Bank (ECB) (Thursday, February 5): We do not think any ECB meetings are “live” in the first half of the year, and the latest January figures suggest inflation risk remains to the upside. However, the recent comments from Martin Kocher and Francois Villeroy suggest that the EUR’s value is moving high up the policy agenda. A move well above 1.20 will materially challenge the ECB’s projections and lead to a larger than expected drag to the headline CPI figure for the year, but it will probably take 1.25 or higher to trigger an immediate policy response. An early indication of downside price risks would arise if the Governing Council used the phrase “a good place” with respect to policy more sparingly, or not at all.

Czechia, Czech National Bank (CNB) (Thursday, February 5): The CNB remains an outlier in EMEA, with no immediate fiscal impulse complicating its policy outlook. Rates are likely to remain on hold at 3.5%, even as sequential inflation shows clear signs of contraction. Output is also starting to struggle due to global uncertainty, but the CZK is treated as a funding currency in the region and is the only currency that is not overheld in EMEA and Latin America. However, if disinflationary trends are emerging in the Eurozone, then the CNB will also need to look into an offset.

Mexico, Banxico (Thursday, February 5): The overnight rate is expected to remain at 7.0%, which should provide a large enough buffer to help Banxico manage inflation risks. For much of Latin America, the commodity rally has been a critical factor in boosting terms of trade, and Mexico itself will benefit as a large silver producer. However, CPI is running near 4%, offering little room for comfort, while domestic demand remains robust, with continued strength in retail sales and output. Until certainty is established in trade with the U.S., we expect Banxico to stick to caution as well.

India, Reserve Bank of India (RBI) (Friday, February 6): With downside risks to growth still prominent, we expect the RBI to cut the rate by 25bp to 5.0%. However, such actions carry the risk of increasing capital outflows and intensifying depreciation pressures across foreign exchange, equity, and bond markets. The upcoming meeting will be pivotal, but our outlook favors another 25bp cut to 5.00%. We will closely monitor the RBI’s forward guidance to determine if it signals openness to further cuts.

Source: BNY

Source: BNY