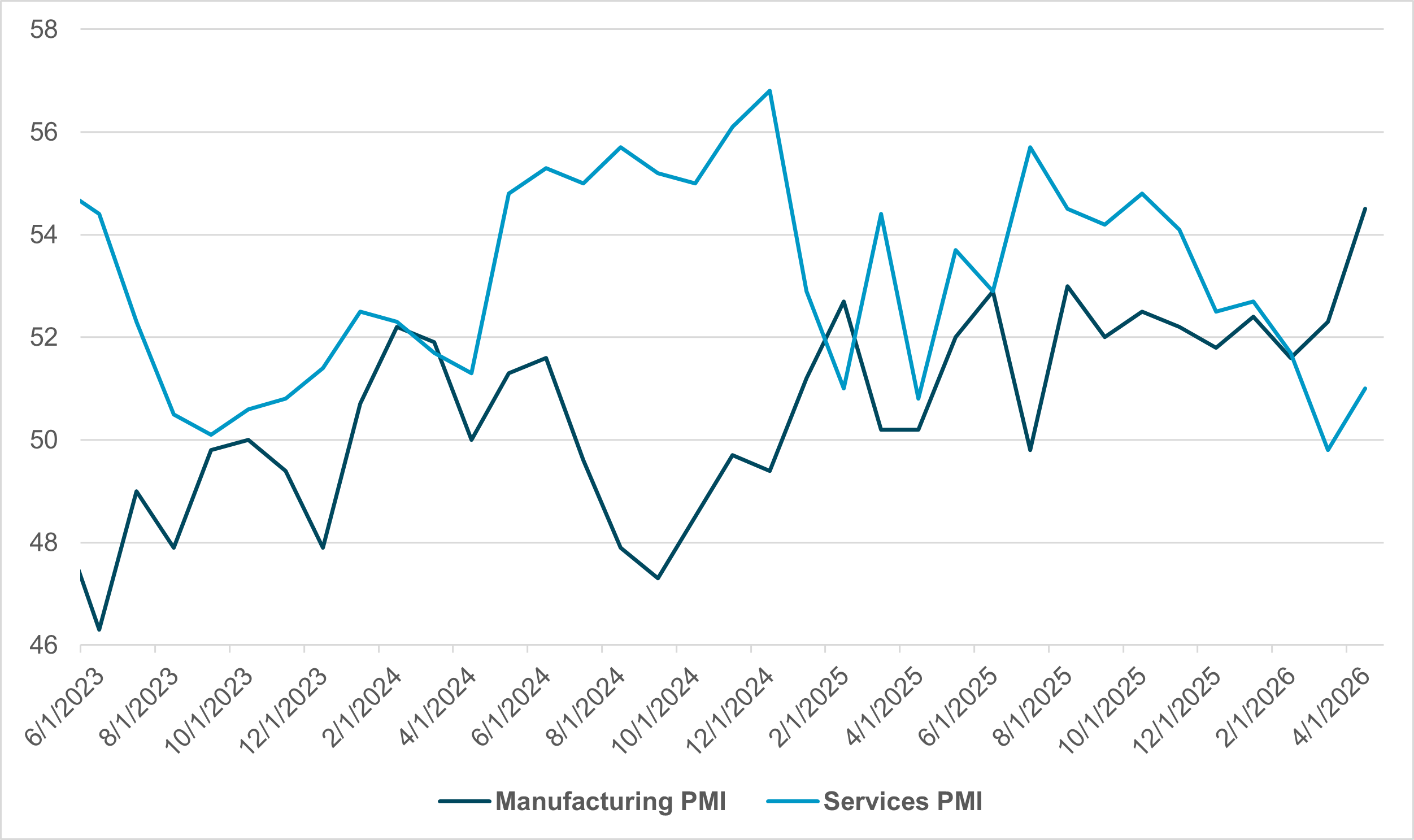

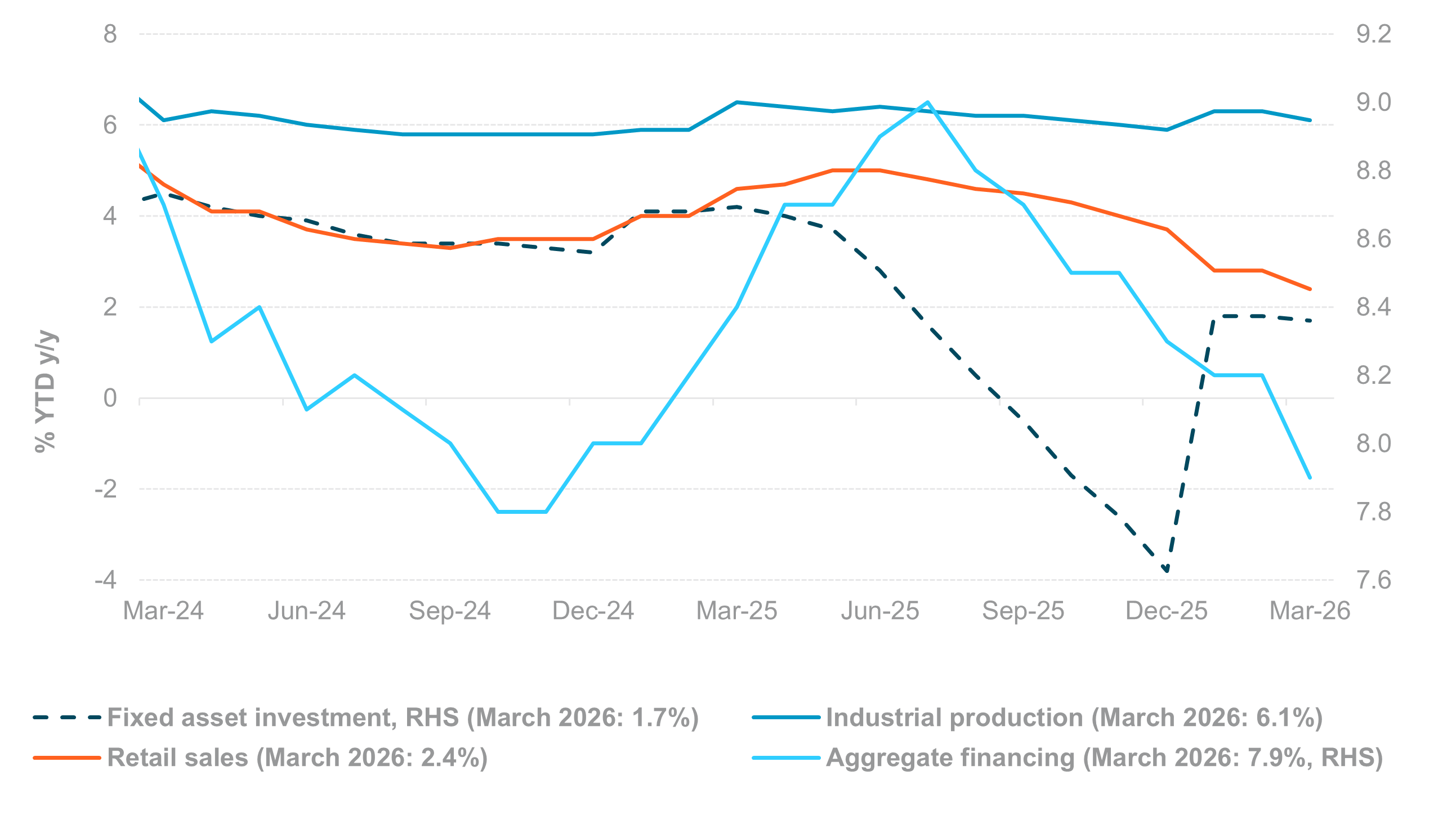

Our take: Eyes this week will be on China’s April activity data – retail sales, industrial production and fixed asset investment – alongside property indicators and the jobless rate, which will offer a full snapshot of domestic demand and potential recovery in real estate. Japan’s Q1 GDP and April CPI are key for BOJ normalization expectations, while South Korea’s early May exports and Taiwan’s export orders provide timely reads on trade and the tech cycle.

Across ASEAN and India, Malaysia’s CPI and trade, Thailand’s Q1 GDP and exports, and Singapore’s final Q1 GDP and April NODX will gauge external demand and electronics momentum. Indonesia’s Q1 balance of payments and India’s PMI will be closely scrutinized to assess the impact from ongoing geopolitical uncertainties.

Australia’s labor market and PMI, alongside New Zealand’s retail sales and PPI, will round out the regional picture. Bank Indonesia is likely to maintain the status quo, with continued focus on FX stability. Overall, the data should signal whether trade and tech are stabilizing Asia’s growth or whether growth is still constrained by weak domestic demand and China’s property sector.

Forward look: The Trump–Xi summit improved global risk sentiment. Expectations for a global trade revival, alongside the ongoing semiconductor and electronics upcycle, are supportive for Asia. Taiwan and South Korea remain pivotal semiconductor suppliers, while ASEAN economies are deeply embedded in the global supply chain.

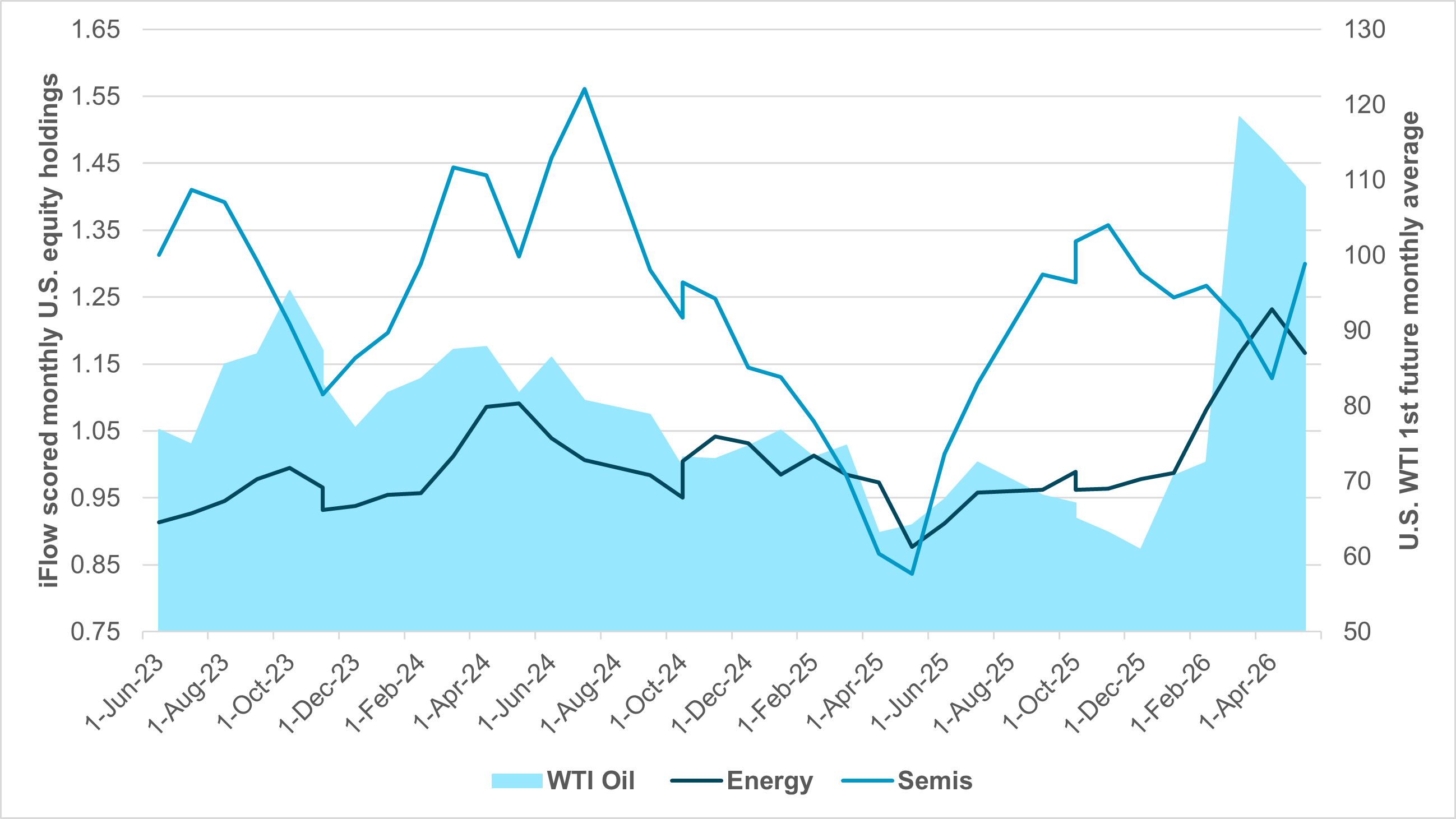

That said, several headwinds continue to weigh on regional assets: elevated oil prices and associated terms-of-trade pressures, a shift in U.S. rate expectations toward further tightening, persistent foreign equity outflows, and weakening fiscal dynamics in parts of the region.

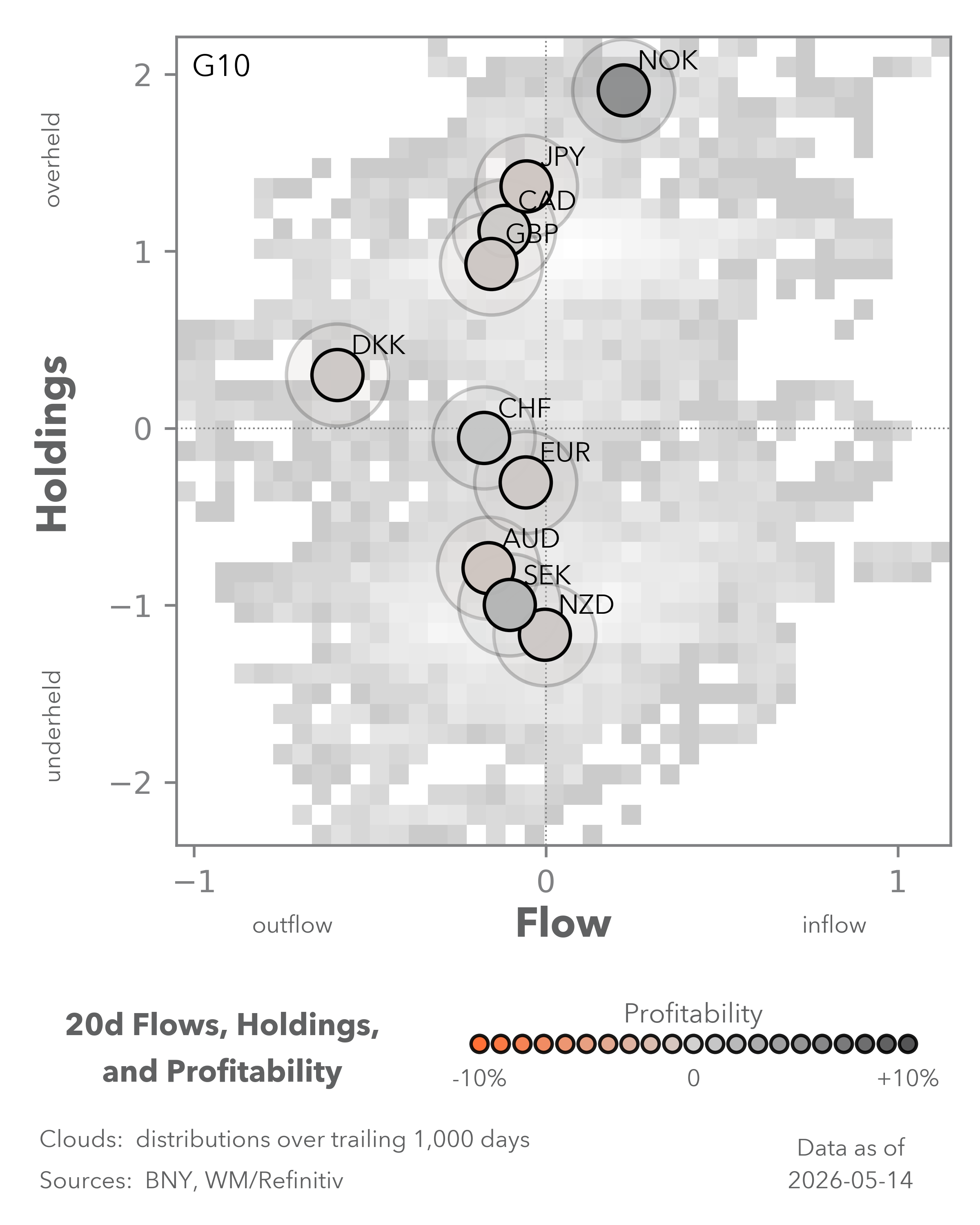

In FX, we highlight a divergence between CNY and INR. We maintain high conviction in a gradual appreciation of the Chinese yuan into H2 2026, supported by sustained capital inflows and improving momentum in the high-tech sector. In contrast, the Indian rupee remains vulnerable to sharper depreciation. Recent macroprudential measures – including higher import duties on gold and silver and proposed tax incentives for foreign bond investment – have had limited market impact, suggesting weakening policy credibility. India’s status as a net commodity importer, combined with limited participation in the semiconductor cycle, further weighs on INR. Across APAC FX, we remain constructive on CNY, KRW, TWD, MYR, and SGD, while maintaining a bearish stance on INR, THB, PHP, and IDR.