Market Movers: Uneasy

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

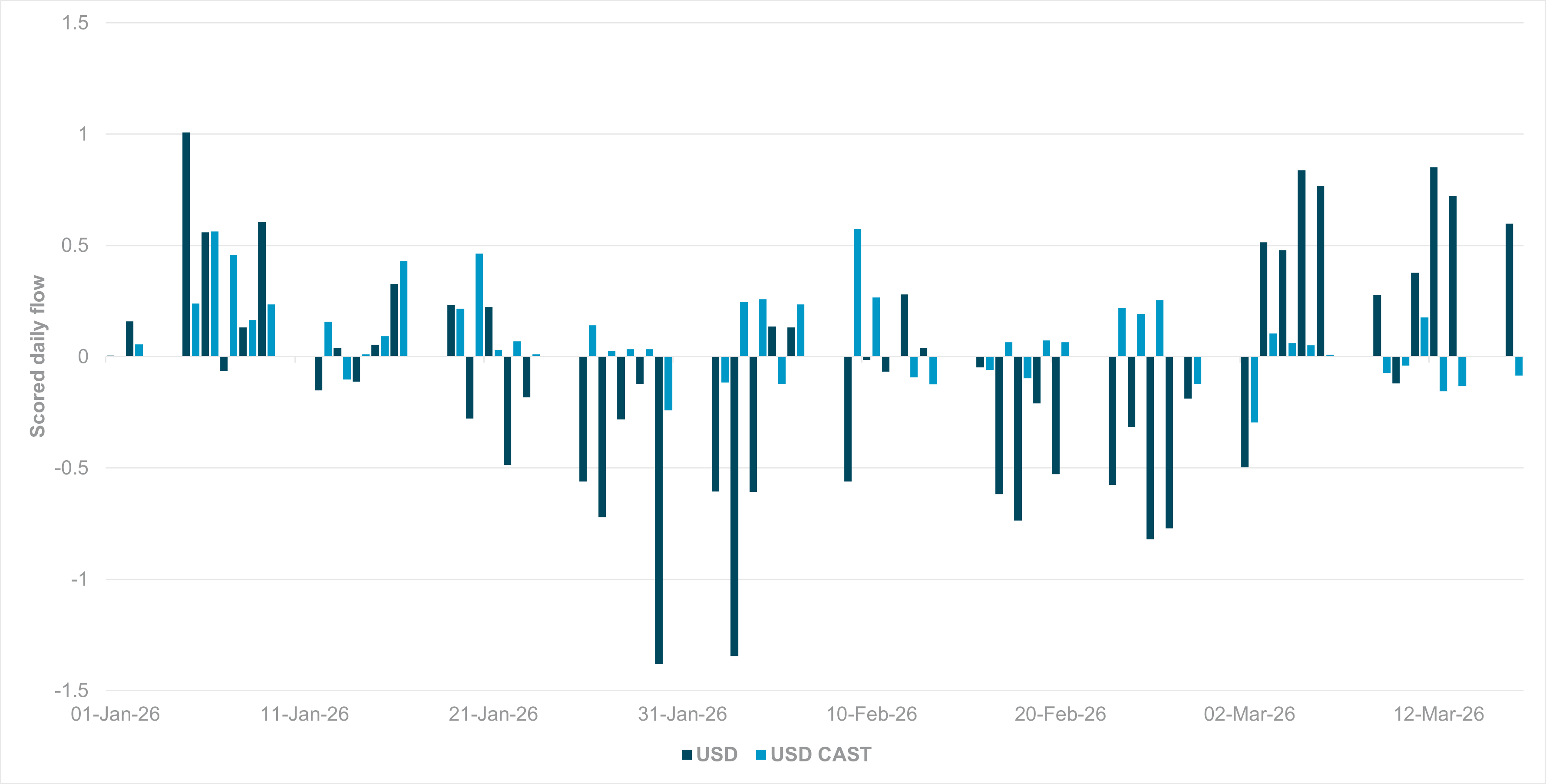

Solid USD and USD cash flow ahead of FOMC meeting

Source: BNY

The dollar is heading into the FOMC decision on solid ground. The conflict in the Middle East has fundamentally changed the dynamics of FX flows, and we note that the February round of net dollar sales (known as the dollar hedging trade) has been fully reversed. The flows from end-January are still weighing on flow averages, but if the conflict progresses to the extent that there are even larger adjustments in Fed expectations away from cuts, further improvement in flow averages is possible. We are mindful of how other central banks are behaving in the current environment as well; if anything, however, the latest developments have underscored the importance of maintaining USD holdings in the event of supply shocks.

Elsewhere, flow in USD cash and short-term instruments (CAST) has largely stayed positive over the past two weeks, although the bulk of the flow was realized during January and February. This should not be considered adverse for USD’s liquidity preference, as the risk environment was different and the dollar can benefit from both sides. Originally, the prospect of U.S. markets continuing to outperform had helped maintain high levels of CAST flows. More recently, USD has been the primary safe haven, as is often the case in geopolitically driven risk-off sentiment. The energy-based nature of risk aversion actually benefits the U.S. due to its net energy-exporting status. This has helped ensure flows are maintained, though the repricing of rate expectations globally may have limited incremental USD CAST flow.

Global equities are higher for a third successive day, with an uneasy calm across markets ahead of key central bank decisions from the Fed and the Bank of Canada. The rise in vessel traffic in the Strait of Hormuz may be modest, but mixed with the alternative pipelines from Iraq and Saudi Arabia, this means oil supply fears are lower. Economic outlooks from data and thinktanks are supporting modest recovery hopes, dependent on the duration of the conflict and its disruption. The surprise for today is that USD is higher even though the commodity supply bid is topping out, along with the correlation to equities. Bonds are also bid, as fears of rate hikes shift toward investors’ wait-and-see stance, leaving an FX volatility factor to watch as we head into the U.S. session.

Oil: The disruption to the Gulf region continues, with Iranian drone and missile attacks on UAE, Saudi Arabia and Kuwait along with U.S. bombing of missile sites along the Strait. Further signals of traffic in the Strait (90 vessels since the war began) support a “new normal” view on oil stuck near $95-100/barrel. Overnight, US API crude inventories rose by 6.556 mb after the previous week’s -1.7 mb – more than the 600,000 expected. Production has fallen 18,000 b/d on the week but is up 103,000 b/d on the year. Gasoline fell by 4.6 mb, but inventories are 5% above average. Distillates fell by 1.4 mb and are 2% below average. The focus is on downstream energy, with products now key for bottlenecks and inflation.

Liquidity: The UAE’s central bank has rolled out a resilience package to support the banking sector and boost liquidity. Lenders can tap 30% of their cash reserves requirement. The one central bank today expected to cut rates is Brazil, where Copom is seen easing by 25bp. The focus will be on financial stress points from liquidity squeezes globally, with the U.S. watching private credit.

Tech: The recovery rally in technology started in Asia, on news that Samsung is thinking about multi-year contracts for memory chips to help stabilize shortage fears. China’s Tencent posted a 13% rise in revenue, led by gaming and advertising, and plans to ramp up its agentic AI products. Nvidia says it is restarting its H200 AI chip production for China after months of mixed signals. The theme of AI driving growth and investment is not slowing and remains underestimated according to Oaktree co-founder Howard Marks, as does the threat to jobs.

Bottom line: The relative calm of markets has been unnerving for many analysts who had expected more volatility. We have moved from the “shock and awe” stage of the current conflict to something else: a new market sentiment state that sees through the war to a new supply narrative for oil and other products, all of which have inflation and growth constraints attached. The downward shift in bond yields and the uptick in shares may be incompatible with stagflation fears, but they do reflect confidence in central bankers getting the policy mix right for the short term. For USD, its safe haven buying link may shift if investors are looking past the war and back to value plays, with hedging the next uneasy step.

Since the war began on February 28, 2026, Iran’s de facto blockade of the Strait of Hormuz has drastically reduced shipping traffic from over 100 vessels/day to just 21 tankers, causing thousands of seafarers to be stranded. Iran appears to be selectively allowing vessels linked to China, Greece, India, Pakistan and Türkiye safe passage under negotiated terms. However, sporadic, seemingly random, attacks on ships continue, targeting vessels from various nationalities and causing widespread disruption. Many ships have diverted to alternative Gulf ports such as Fujairah, Khor Fakkan and Sohar, creating congestion and logistical challenges in the region. Brent -0.648% to 102.75, WTI -2.017% to 94.27, HH natural gas -2.836% to 2.947, Dutch TTF natural gas -0.425% to 51.34.

Japanese Prime Minister Sanae Takaichi has warned that her upcoming meeting with President Trump will be “extremely difficult” following tensions over a withdrawn U.S. request for Japanese warship deployments to the Strait of Hormuz. Takaichi has ruled out naval deployment, citing constitutional constraints, and instead signaled potential logistical support or contributions after a ceasefire. The Washington visit, initially intended to reinforce bilateral ties, has been overtaken by geopolitical friction linked to the Iran war and U.S. pressure on allies. Additional strain stems from U.S. trade actions and tariff investigations, while Japan remains cautious given its Middle East energy dependence and sensitivity to escalating tensions with China. Nikkei +2.866% to 55239.4, USDJPY +0.246% to 158.73, 10y JGB -6.1bp to 2.215%.

Major Japanese firms are set to deliver strong wage hikes in 2026 annual labor talks, extending robust pay growth into a fourth consecutive year amid persistent labor shortages. Early deals include Mitsubishi Motors agreeing to a 5.1% increase, while the Rengo union is seeking a 5.94% increment, slightly below last year’s 6.09% demand (actual: +5.25%). Wage growth remains supported by solid profits and tight labor markets, underpinning the BoJ’s policy normalization narrative. However, rising energy costs from the Middle East conflict and global risks may constrain sustained wage growth and tightening beyond the near term.

Taiwan’s life insurers halved their holdings of forwards in January-February, following regulatory changes allowing them to spread currency fluctuation impacts over bond tenors, reducing immediate balance sheet volatility. This record two-month drop in derivatives, mainly currency-linked, may have contributed to the Taiwan dollar’s 1.5% decline this year amid a stronger U.S. dollar. The Financial Supervisory Commission’s new rules, effective January 1, require insurers to accumulate savings from lower hedging in a special surplus reserve to bolster capital. Key insurers such as Cathay Life cut forwards by 78%, while others trimmed by more than 50%. Hedging demand may return if the U.S. dollar strengthens further. TAIEX +1.513% to 34348.58, USDTWD +0.123% to 31.846, 10y TGB +0.1bp to 1.415%.

Thailand’s Constitutional Court has accepted a petition challenging the validity of February’s parliamentary election over allegations that ballots may be traceable due to the use of barcodes and QR codes. The court voted 6-3 to hear the case, citing potential breaches of constitutional requirements for secret voting and freedom of expression. It has given the authorities 15 days to respond. A ruling that ballot secrecy was compromised could lead to the election being annulled and require a new vote, risking delays to government formation. The decision comes as Prime Minister Anutin Charnvirakul seeks parliamentary endorsement, adding fresh uncertainty to Thailand’s political outlook. SET +0.47% to 1441, USDTHB +0.056% to 32.375, 10y TGN +5.6bp to 2.092%.

U.S. FOMC consensus is for no change at 3.75%, with interest focusing on any shift in the statement or SEP outlook and Chair Jerome Powell’s tone on dual-mandate risks.

U.S. February PPI ex-food, energy is forecast higher at 3.7% y/y vs. 3.6% y/y in January.

U.S. January factory orders expected up 0.1% m/m vs. -0.7% m/m while the ex-transportation measure is expected to be unchanged at 0.4% m/m. Final durable goods orders and durable order ex-transportation are both expected to match initial estimates at 0% m/m and 0.4% m/m, respectively.

U.S. Treasury sells $69bn in 17-week bills.

Mood: Sentiment has deteriorated further, with iFlow Mood slipping deeper into risk-off territory at -0.139. The shift was characterized by continued equity outflows alongside rising demand for core sovereign bonds.

FX: LatAm FX continued to attract steady inflows, contrasting with mixed dynamics elsewhere. PLN, ZAR and COP saw notable buying, while TRY and INR led outflows. Within the G10, USD, NOK and AUD recorded inflows, against selling in EUR, GBP and JPY.

FI: Divergence of flows, with selling in EM APAC versus buying in G10 government bonds. Flows in LatAm and EMEA were mixed. Eurozone and Hungarian government bonds were most bought, against large-scale selling in Turkish, Chinese and Indonesian government bonds.

Equities: Equity selling remained concentrated in China, India and Colombia, with additional outflows in the Eurozone and Sweden. In contrast, LatAm equities continued to see solid inflows, alongside selective buying in Poland and Malaysia. Within EM APAC, selling was broad-based, particularly in the materials and financials sectors, while the energy and utilities sectors attracted inflows. G10 equity flows were relatively muted.

“What is it about silence that makes people uneasy?” – Morrie Schwartz

“Man is not worried by real problems so much as by his imagined anxieties about real problems.” – Epictetus

Euro area inflation registered 1.9% y/y in February, rising from 1.7% in January, while EU inflation increased to 2.1% y/y from 2.0%. The uptick in euro area inflation was primarily driven by services, which contributed 1.54 percentage points, followed by food, alcohol and tobacco at 0.48 percentage points and non-energy industrial goods at 0.17 percentage points, while energy exerted a negative contribution of -0.30 percentage points. Across member states, the lowest inflation rates were recorded in Denmark at 0.5%, Cyprus at 0.9% and Czechia at 1.0%, while the highest were in Romania at 8.3%, Slovakia at 4.0% and Croatia at 3.9%. Inflation decreased in eleven countries, was unchanged in four and increased in twelve. Euro Stoxx 50 +1.02% to 5828, EURUSD -0.009% to 1.1539, BBG AGG Euro Government High Grade EUR -2.6bp to 3.149%.

Switzerland’s economic outlook was revised down slightly in March, with GDP growth for 2026 now forecast at 1.0% (previously 1.1%) and 2027 at 1.7%, reflecting below-average expansion amid heightened geopolitical uncertainty. Inflation for 2026 is now expected at 0.4% (previously 0.2%), driven by rising energy prices linked to the Middle East conflict, while unemployment is projected at 3.0% in 2026 and 2.8% in 2027. GDP rose 0.2% q/q in Q4 following a 0.4% contraction, indicating stabilization. However, subdued global demand, a strong Swiss franc and weaker investment are weighing on growth, while risks remain skewed toward higher inflation and weaker activity due to energy disruptions and potential trade policy changes. SMI -0.2% to 12937, EURCHF +0.155% to 0.90703, 10y Swiss GB -1.7bp to 0.322%.

Switzerland’s March KOF economic outlook projects GDP growth of 1.0% in 2026 and 1.7% in 2027, highlighting the persistent drag from geopolitical tensions and changes in U.S. tariff policy. The U.S.-Israeli war with Iran has driven oil and gas prices higher, disrupted supply chains and increased uncertainty, though the baseline assumes a limited domestic impact. Under a scenario where oil prices remain around 30% higher, growth would slow to 0.7% in 2026 and 1.5% in 2027, leaving GDP 0.6 percentage points lower by end-2027, alongside higher inflation and unemployment. Domestic demand, particularly consumption, is still supportive, while investment and exports remain subdued amid weak global demand, strong franc pressures and elevated trade uncertainty.

Poland’s March consumer confidence indicator fell by 3.1 points m/m to -12.2, reflecting weaker sentiment regarding both current and future economic conditions. The deterioration was driven primarily by a 10.2-point drop in expectations for the future economic situation and a 2.8-point decline in assessments of current conditions, alongside weaker views on household finances and major purchases. The leading consumer confidence indicator also declined, falling 2.5 points m/m to -9.5, with expectations for the future economic outlook and household finances again the main drag. However, sentiment improved slightly for current household finances, savings prospects and unemployment expectations, while the headline indicator remained 3.0 points higher y/y. WIG +0.45% to 124146, EURPLN +0.017% to 4.2613, 10y PGB -8.7bp to 5.461%.

South African CPI came in at 3.0% y/y in February, easing from 3.5% in January, while prices rose 0.4% m/m. The deceleration in annual inflation was driven by both goods and services components, with goods inflation slowing to 1.9% y/y from 2.7% and services easing to 3.8% y/y from 4.2%. The main contributors to the annual rate remained housing and utilities at 4.8% (contributing 1.1 percentage points), food and non-alcoholic beverages at 3.7% (0.7 percentage points) and insurance and financial services at 4.7% (0.5 percentage points). Overall, the data indicate moderating price pressures across both core consumption categories despite continued monthly price increases. JSE TOP 40 -0.29% to 109257, USDZAR -0.093% to 16.6533, 10y SAGB -13.4bp to 8.814%.

Japan’s February 2026 trade statistics show exports rose 4.2% y/y to ¥9.57tn, marking six consecutive months of growth, driven by semiconductor electronic components and mineral fuels. Imports increased by 10.2% y/y to ¥9.51tn, led by semiconductor components and non-ferrous metals, resulting in a trade surplus of ¥57.3bn, a sharp 89.8% decline from last year. Exports to the U.S. fell 8.0% y/y, while imports from the U.S. rose 8.4%. Exports to the EU increased by 14.0% y/y, with imports up 3.1%. Exports to Asia grew 2.8% and imports surged 19.1%, with China showing a 10.9% decline in exports but a 35.4% rise in imports. Nikkei +2.866% to 55239.4, USDJPY +0.246% to 158.73, 10y JGB -6.1bp to 2.215%.

The average condominium price in the Tokyo metropolitan area rose 38.8% y/y to ¥110.25mn in February 2026, up from ¥79.43mn in February 2025 (14.2% y/y in January 2026). Prices in Tokyo Central rose by 37.4% y/y, Kanagawa by 41.1% and Chiba by 118.0%. Tokyo suburbs rose 33.6%, while Saitama declined by 40.7%. Unit supply totaled 1,762 in the metropolitan area, with Tokyo Central supplying 517 units. The data reflects strong price growth across most regions, particularly in Chiba and Kanagawa, despite mixed supply trends.

New Zealand’s Q4 2025 balance of payments showed a seasonally adjusted current account deficit of NZ$4.6bn, NZ$857mn wider than the previous quarter. The annual current account deficit narrowed to NZ$16.3bn (3.7% of GDP) from NZ$20.0bn (4.7% of GDP) in 2024. The goods deficit widened to NZ$866mn due to higher imports of petroleum and machinery, while services recorded a NZ$122mn surplus, led by travel exports. The primary income deficit widened by NZ$664mn, driven by lower income from New Zealand investments abroad and higher foreign investment income. The financial account had a NZ$3.8bn net inflow. New Zealand’s net international liability position narrowed to NZ$197.2bn (44.3% of GDP). NZX 50 +1.012% to 13315.6, NZDUSD +0.48% to 0.5866, 10y NZGB -7.9bp to 4.595%.

New Zealand’s Westpac-McDermott Miller Consumer Confidence index fell by 1.8 points to 94.7 in Q1 2026, remaining below the neutral 100-point level. While more households reported improved financial positions over the past year (-23.8 vs. Q4 2025: -24.4), growing global concerns, particularly the outbreak of the Middle East conflict during the survey period, have increased economic outlook worries (1.9 vs. Q4 2025: 5.6). The initial decrease in confidence is modest, but ongoing conflict and rising fuel prices may further pressure household finances and reduce confidence in the coming months.

South Korea’s February 2026 seasonally adjusted unemployment rate dropped to 2.9% from 3.0%. The economically active population reached 29.406 million, up 1.0% y/y (+287,000). The labor force participation rate rose to 64.0%, increasing by 0.3 percentage points y/y. Employed people totaled 28.413 million, up 0.8% y/y (+234,000), with the employment-to-population ratio at 61.8%, up 0.1 percentage points y/y. The unemployment count increased by 5.7% y/y (+54,000) to 993,000, pushing the unemployment rate to 3.4%, up 0.2 percentage points y/y. The economically inactive population declined by 0.2% y/y (-39,000) to 16.536 million. KOSPI +5.045% to 5925.03, USDKRW +0.253% to 1484.5, 10y KTB +2bp to 3.7%.