U.S. asset demand shows no sign of abating

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 4 minutes

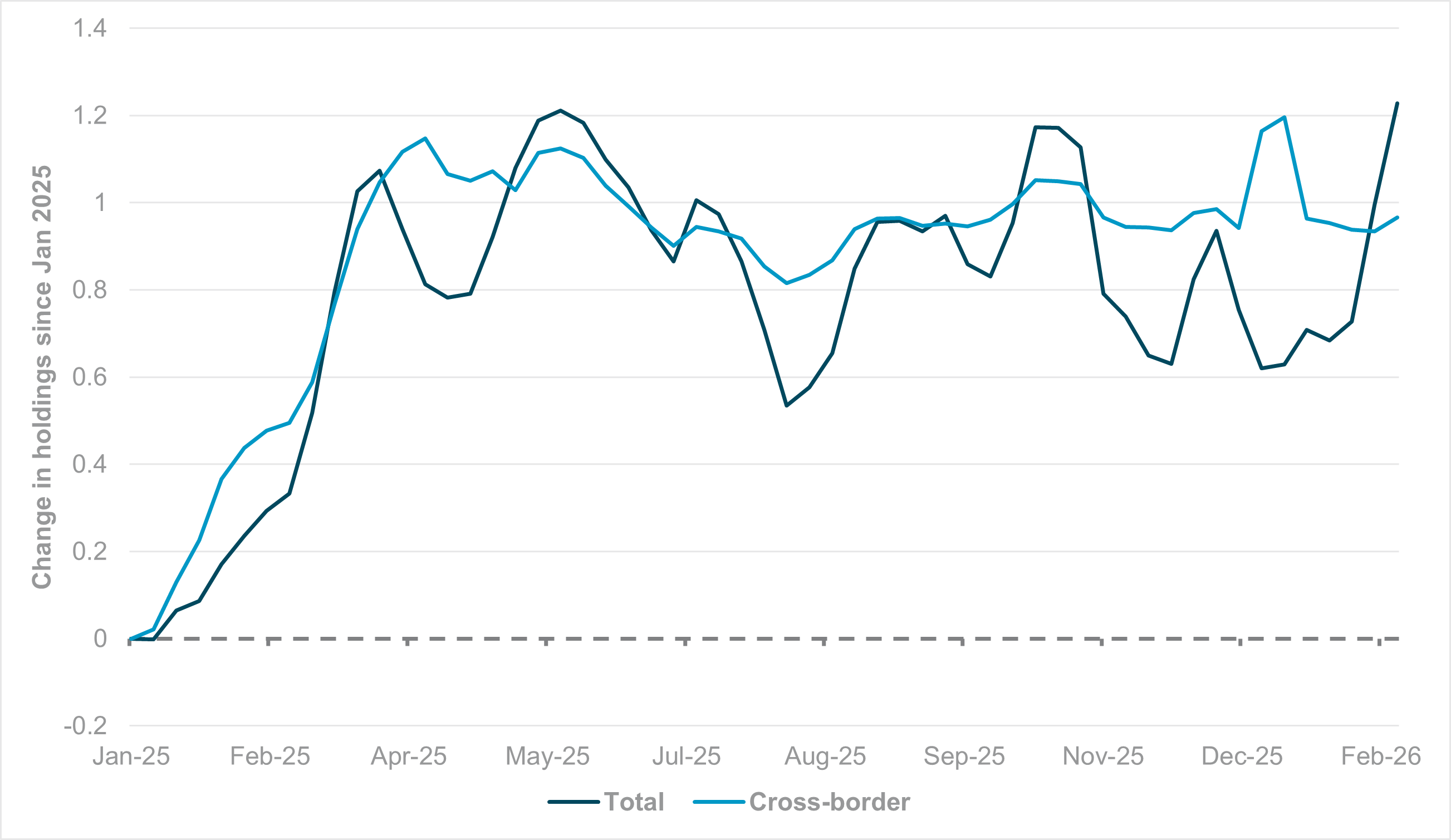

EXHIBIT #1: CHANGE IN EUR HOLDINGS AMONG CROSS-BORDER AND AGGREGATE INVESTORS

Source: BNY

Our take

The European Central Bank (ECB) February decision has helped prevent further euro strength, and we expect the Governing Council to be relatively comfortable with its current language. The bar for a direct policy response to euro strength remains high, and it would take far greater downside surprises in German, Spanish and Dutch inflation to materially drag the price outlook away from current projections. Nonetheless, we also believe the ECB needs to acknowledge that currency preferences have shifted fundamentally, especially among Eurozone-based investors.

Historically, our flow data support the view that the marginal driver of exchange rates rests largely with cross-border investors. Onshore investor holdings are generally passive in nature and mandate driven. These onshore asset allocators typically forward-buy their home currency, usually against the dollar, but hedge sizes depend on net asset value performance. For example, our data showed that even during extreme volatility in April last year, the initial reaction was a decline in domestic EUR purchases because their U.S. positions had declined significantly in value. Hedges were taken off accordingly. Meanwhile, cross-borders investors into the Eurozone have greater discretion to scale EUR exposures up or down.

The most significant move in EURUSD last year was driven by increased EUR holdings from cross-border and EUR-based asset allocators in H1. Our figures indicate that it was largely cross-border investors that materially reduced a heavy underweight EUR position. Over the past few months however, except for some seasonal adjustments around year-end, our data show that there has been very little relative change in cross-border EUR holdings. In contrast, there has been a jump in the total EUR holdings figure, indicating that the current marginal driver of EUR performance is coming from Eurozone or EUR-denominated asset allocators and beyond what asset gains would justify.

Forward look

The shift in behavior suggests that Eurozone investors have increased hedging on overseas portfolios, largely focused on U.S. assets. In previous cycles, especially during the phases of “U.S. exceptionalism,” investors were happy to run minimal hedge ratios, particularly as U.S. yields were high and the ECB was seen as more dovish. Over the past quarter, the script has flipped, as the ECB pivoted in December toward monitoring inflation while the Fed was seen as more dovish, alongside exogenous factors. Consequently, the ECB will likely rely on the Fed to limit further pricing of rate cuts but may also need its own adjustments to manage the shift in local preferences, including acknowledging the role of non-monetary factors in weaker dollar preference.

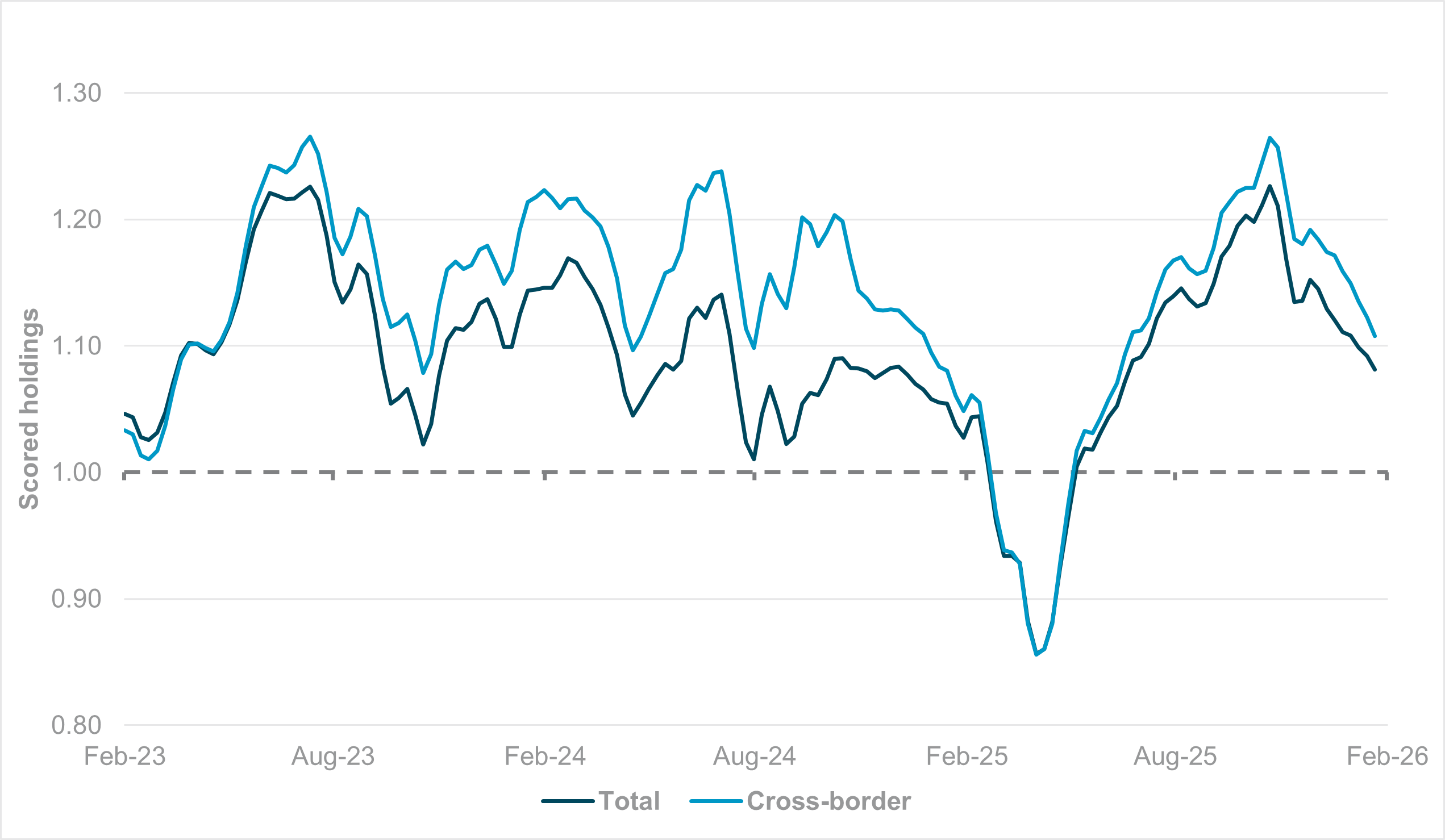

EXHIBIT #2: SCORED HOLDINGS IN U.S. IT SECTOR (GICS L1) STOCKS, TOTAL AND CROSS-BORDER

Source: BNY

Our take

Despite the volatility seen in recent weeks, U.S. equity markets have broadly managed to steady performance, and the Tech sector continues to lead allocations. Fears that AI-related capital expenditure could weigh on valuations persist, but financial conditions remain loose enough to support investment plans, despite questions over long-term returns. Our data show that global allocations in the broader IT sector (GICS Level 1) remain well below 2025 highs but sit about 10% above the rolling 12-month average, which is already a high base.

Crucially, international investors remain heavily invested in the theme. After the gyrations of “Liberation Day” in Q2 2025, our data show that cross-border investors took full advantage of the adjustment in dollar valuation to add to U.S. equity exposure. Although allocations are not as strong as during the “U.S. exceptionalism” period from 2023 to 2024, the cross-border “premium” remains intact. For all the talk of diversifying away from the U.S., global investor conviction appears stronger than that of domestic peers.

Forward look

One of the reasons behind the initial convergence between U.S. and global equity holdings in U.S. tech was the notion that new themes were emerging externally. While China is advancing its own technological capabilities, investment channels remain relatively limited. The European defense theme has also strengthened home bias in Europe. However, despite some turbulence in trans-Atlantic relations, there is very little scope for decoupling, and U.S. investments will remain a crucial part of European strategic asset allocation. It may simply come down to the fact that the dollar’s weakness is helping compensate for whatever risk premia is deemed necessary, and that increased allocations into emerging markets need not come at the expense of U.S. investments. As long as earnings continue to deliver, “U.S. exceptionalism” in tech-related investments is unlikely to fade.

In the near term, global industrial metals look particularly exposed, as China and much of Asia enter a seasonal slowdown. Even if this is to be expected, the current extreme levels of positioning mean that such assets will display higher than usual sensitivity to disappointments in growth data.

EXHIBIT #3: SCORED HOLDINGS, U.S. IG AND HY CREDIT

Source: BNY

Our take

Corporate credit is dominating asset allocation this month, as U.S. tech companies launch global bond offerings to fund capital expenditure. For some issuers, coverage ratios remain very high across currencies and maturities, helping dispel concerns that markets cannot fund investment plans. Corporate credit’s relatively under-positioned status may be another driver of interest, particularly in investment-grade assets.

Our data indicate that this asset class underperformed for much of the past three years. While nominal and real rates from government issuers were relatively high, there was simply no incentive to move into corporate credit. “Liberation Day” tariffs affected sentiment further amid fears of margin risk for import-exposed names. However, as Fed easing moved up the agenda and the central banks of most large developed markets maintained a very cautious outlook, the case for spread capture has picked up, especially as financial conditions have not tightened as feared. Even episodes of fiscal dominance have cast corporate issuers in a more positive light.

Forward look

It will take time for strong demand in primary market issuance to generate a flow and holdings impact within iFlow, but we can see that at least for U.S. corporate credit, the holdings picture is stable and at its strongest in three years. Furthermore, at around 10% above the rolling 12-month average, holdings are not even stretched. For tech issuers with strong free cash flow, we see an additional holdings discount among investment-grade names, suggesting scope for further additions. Unless there is a material pivot toward tighter financial conditions, led by the Fed in response to inflation, we will not be surprised if corporate credit continues to perform well in the primary and secondary markets.