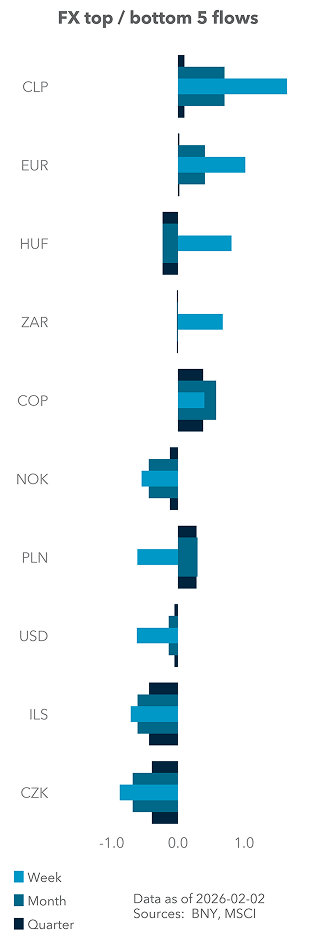

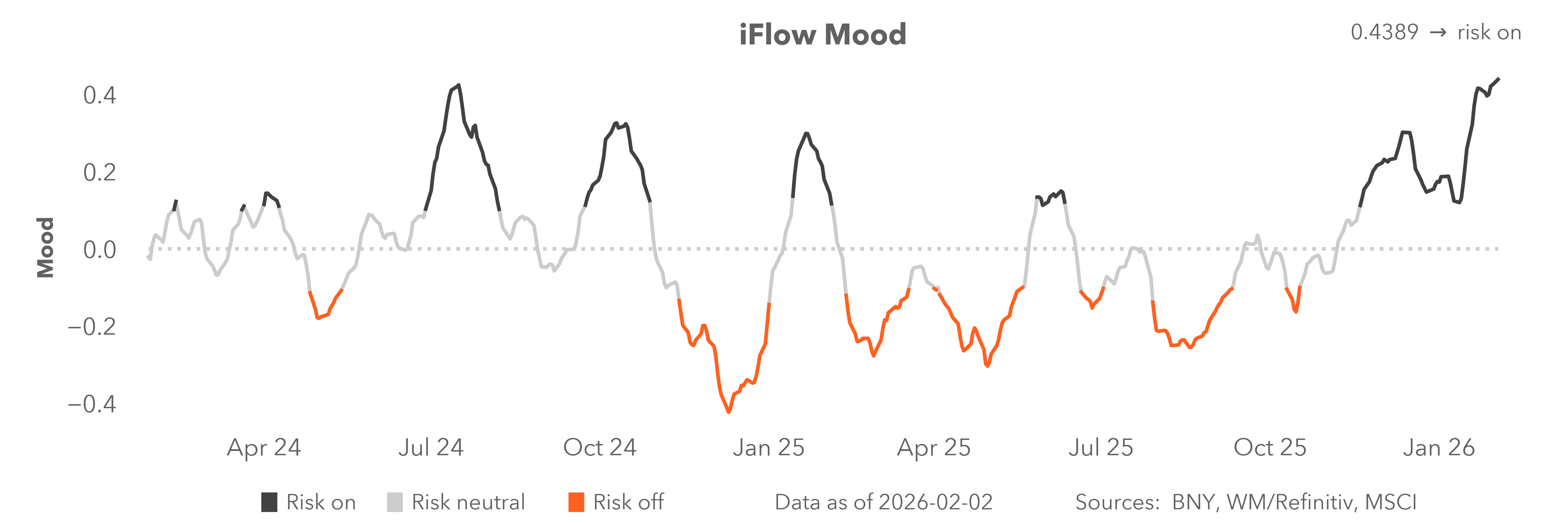

Risk aversion highlights key asset market exposures

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 4 minutes

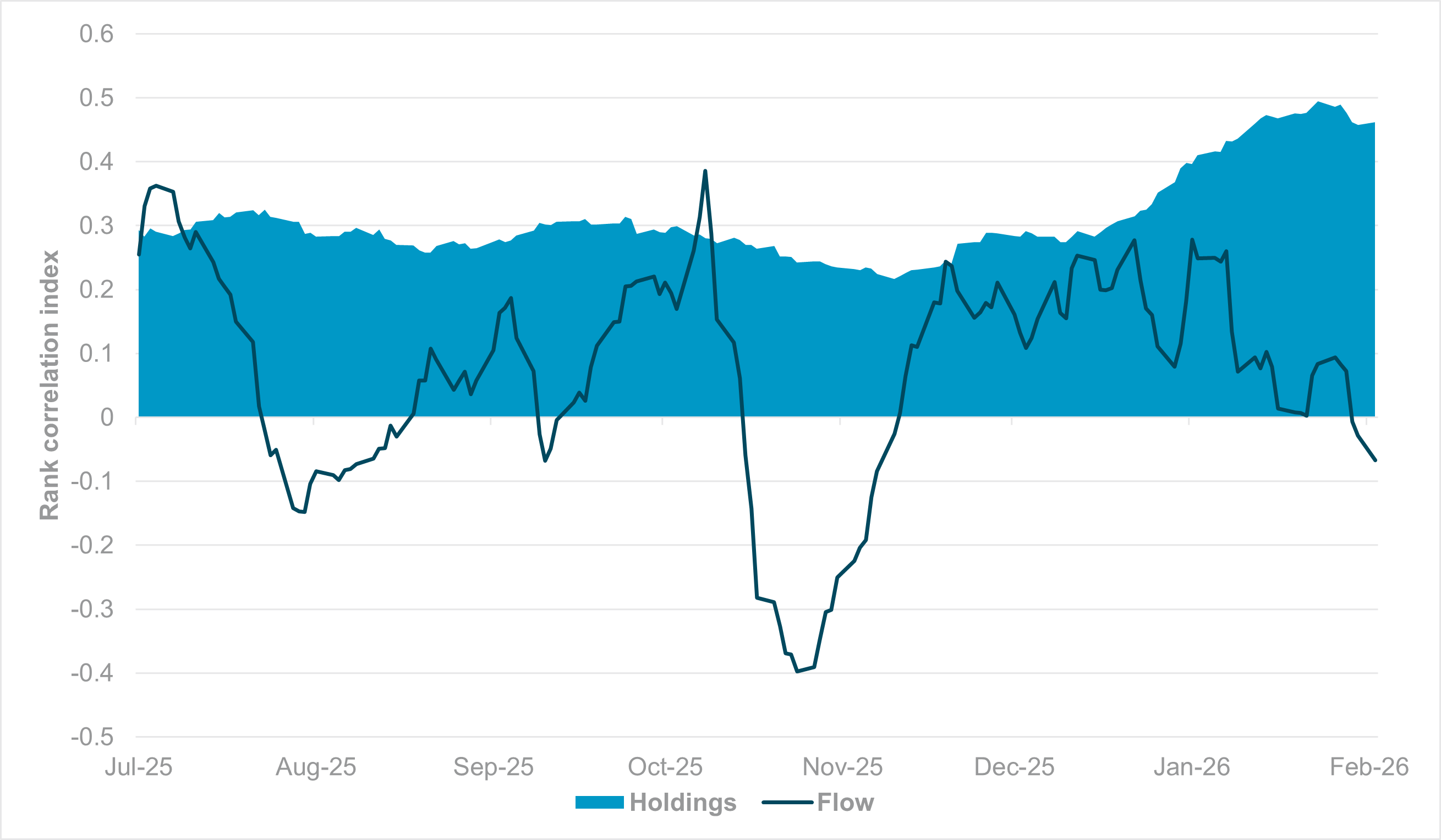

EXHIBIT #1: RANK CORRELATION INDEX OF 5Y OR 10Y CURRENCY YIELDS VS. CURRENT FLOW AND HOLDINGS

Source: BNY, iBloomberg

Our take

Heading into extreme market volatility late last Friday and into this Monday, we highlighted concerns that positioning across asset classes had become increasingly concentrated. The clearest example was in FX markets, where every high-yielding or resource-based emerging market currency in Europe and Latin America (LatAm) was overheld.

Our iFlow Carry (Holdings) index, which tracks the alignment between currency holdings and their underlying 5y or 10y yields, was also at its highest level in around two and a half years. At such extremes, the most likely direction was an unwind.

As of this week, we note that our iFlow Carry (Flow) index has turned negative, implying that high-yielders are now under selling pressure from a relatively overheld starting point. Such a setup renders carry positions particularly vulnerable, as the bar for further outflows is very low.

Forward look

We believe FX carry trades can unwind of their own accord due to excess positioning. With most currencies also profitably overheld, profit-taking ahead of event risk is another important driver.

On a monthly basis, recent sales have been driven by PLN, RON and MXN, but there are still extreme flows on the purchase side as well, led by CLP and HUF. As we expect iFlow Carry (Flow) to move toward negative significance, the best risk-reward lies in fading overbought and positively held currencies, implying that ZAR and COP may also join the mix. Among the beneficiaries, the U.S. dollar should lead. We also see low-yielding APAC currencies performing well, as investors retreat from overseas markets.

We retain caution on European funders, as current valuations in EUR, CHF and SEK are not attractive.

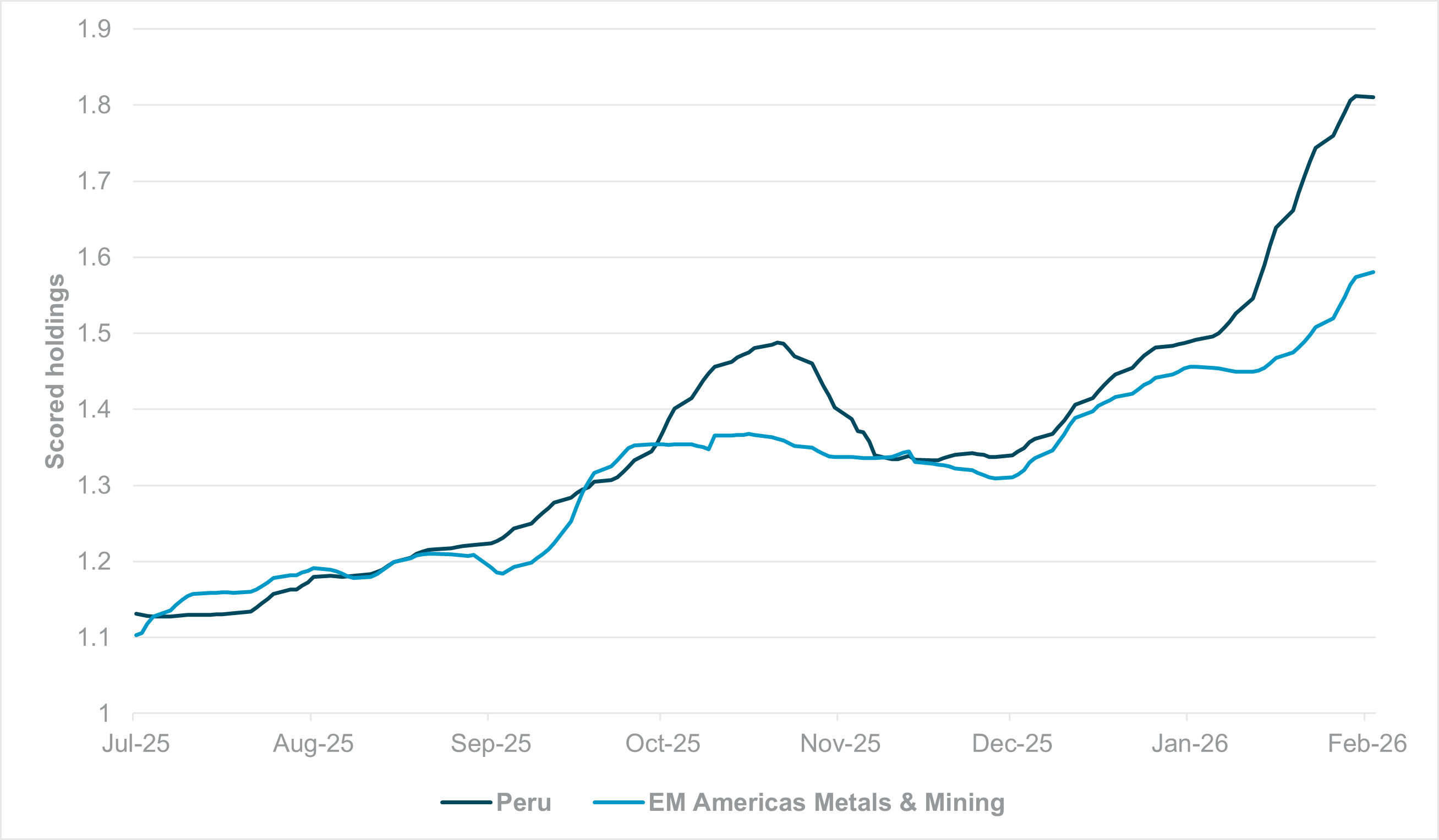

EXHIBIT #2: SCORED HOLDINGS FOR PERU AND EM AMERICAS METALS AND MINING (GICS LEVEL 3)

Source: BNY

Our take

The recent bout of precious metals volatility has threatened to curtail the performance of heavily positioned global assets. As detailed above, the FX carry trade is most exposed. But if prices continue to struggle for precious and industrial metals, the markets with the strongest direct linkages will also continue to struggle. This risk is amplified where underlying economies are considered concentrated and any re-rating takes place on the basis of resources alone.

For example, South Africa’s benchmark registered the biggest decline since the extremes in the early COVID-19 months of 2020 before recovering. However, South Africa has long been considered a positive structural re-rating story, notwithstanding some domestic political uncertainty that surfaced this week. Out of all the markets we track, we still believe LatAm is the most exposed, particularly Peru and the broader emerging markets (EM) Americas Metals and Mining industry group (GICS L3). The near-50% gain in Peruvian equity holdings is extreme by any measure, and the size of the market likely means that the flow sizes involved in driving the change were relatively small and easily reversible.

Forward look

Similarly, the Metals and Mining industry is also running at 60% above the rolling one-year average. These firms have much larger industrial exposure, and maintaining current holdings levels will require metals prices to hold at the same levels. Given that financial conditions are tightening marginally through interest rate and yield curve channels, at the very least we expect a relatively volatile path ahead. FX hedging is clearly already taking place, but other forms of risk mitigation may also be necessary.

In the near term, global industrial metals look particularly exposed, as China and much of Asia enter a seasonal slowdown. Even if this is to be expected, the current extreme levels of positioning mean that such assets will display higher than usual sensitivity to disappointments in growth data.

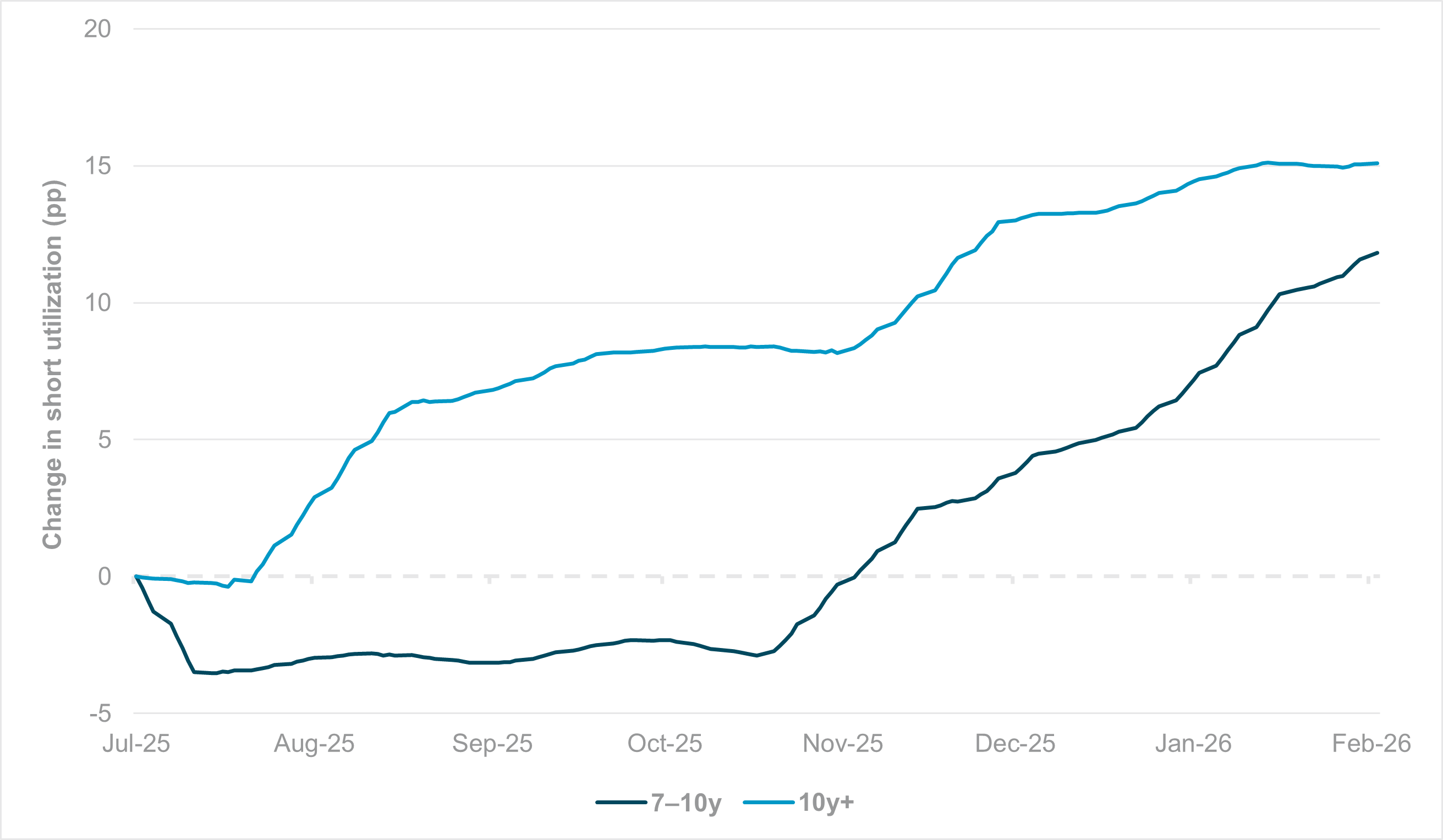

EXHIBIT #3: CHANGE IN NORMALIZATION FOR 7–10Y AND 10Y+ EUROPEAN BONDS

Source: BNY

Our take

The preliminary French inflation figure for January released this week now shows the country is on the verge of flirting with deflation. With the latest –0.4% m/m decline in prices, based on sequential figures from the past six months, French inflation is now running close to –2% y/y. It is no surprise that Banque de France Governor François Villeroy de Galhau was one of the Governing Council members who explicitly called out EUR strength and its impact on monetary policy. Had EURUSD sustained its initial move through 1.20, European Central Bank (ECB) President Christine Lagarde would have faced more pressing questions about FX scenarios. However, we believe the majority of the Governing Council will opt to wait until the March forecasts. Furthermore, the hawkish members of the Governing Council may also point to current behavior in yield curves, as there is little sign of flattening that would indicate concern over inflation trajectories.

Our data support this view: short utilization in the 7–10y and 10y+ parts of European sovereign bond markets has been increasing notably since November, supporting steepening expectations as 30y Bund yields hit 15-year highs.

Meanwhile, labor markets remain tight across the Eurozone, with Spanish unemployment now at the lowest level since the global financial crisis, leading many policymakers to conclude that upside risk to inflation from wage growth is structural.

Forward look

Despite ongoing divergence in rate paths, there has been a general lean away from further easing among developed market central banks over the past cycle. The Reserve Bank of Australia’s hike this week may fuel expectations that more hikes will follow elsewhere. In such an environment, suddenly reintroducing cuts would render the ECB an outlier, especially after it moved away from a dovish bias late last year. We believe that how fiscal policy evolves will have a significant bearing on curves and on structural inflation, especially as wage growth remains strongly driven by spending on public services, with limited signs of productivity gains as an offset. The French budget contains some degree of tightening, while the jury is still out on the net effect of defense-based investment across the EU.

We continue to err on the downside of inflation risk, particularly if national governments take broader concerns over fiscal dominance seriously and this is coupled with the restraining impact of a strong EUR. As a result, an ECB response cannot be ruled out.