BRL selling leads rebalancing

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 4 minutes

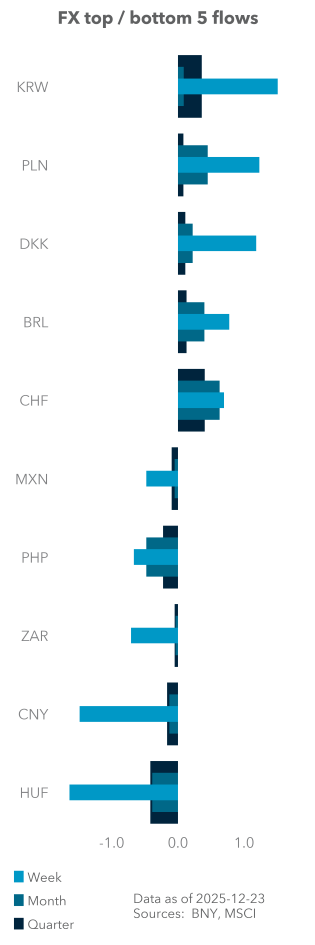

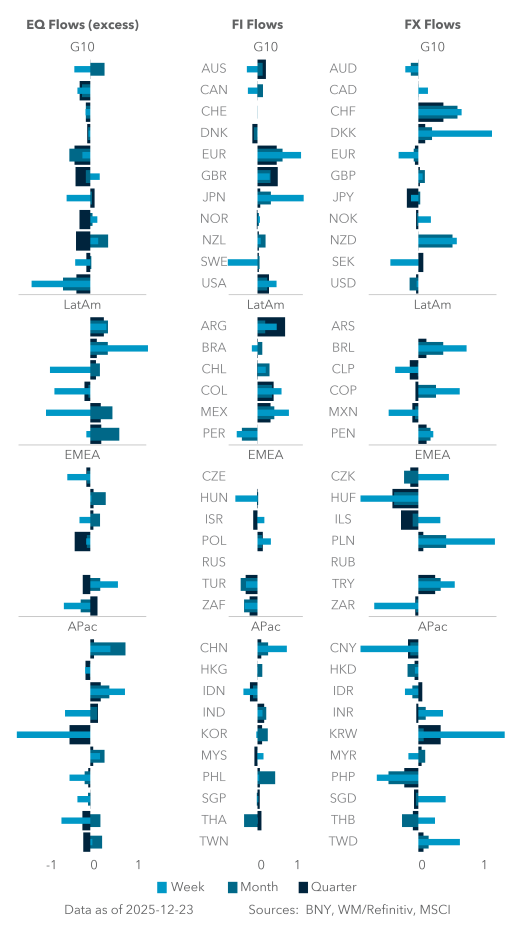

EXHIBIT #1: MONTHLY FX FLOW SCORES (STANDARD SCORES OF 20-DAY SMA IN FLOWS)

Source: BNY iFlow

Our take

We do not expect significant shifts in sentiment or activity between Christmas and New Year’s, so the bulk of the realized flow and asset price movements that generate rebalancing decisions should already have been completed. Based on our flow figures, the month was relatively flat for most currencies on a marginal basis, with no dominant theme despite a general recovery in risk appetite.

Three names stood out: NZD, CHF and BRL. All were strongly bought relative to peers, but there is not much in the way of a unifying theme.

The New Zealand dollar (NZD) may have been one of the currencies that benefited from a shift in inflation and policy expectations toward a more hawkish stance, but the Reserve Bank of New Zealand dismissed such hopes. Other currencies with a stronger case for this narrative were mostly net sold. The Swiss franc’s (CHF) ongoing recovery is consistent with a more favorable policy stance. However, funding currencies also did not benefit as much during the month, so the franc’s gains appear to be an outlier and may reflect ongoing “insurance” accumulation amid elevated valuation concerns in other asset classes. For the Brazilian real (BRL), the real yield story remains compelling even as fiscal dominance concerns linger. Given how well local markets also performed, it is more of a standalone carry play and leaves the currency facing very high rebalancing risk.

Forward look

Based on realized flows up until December 23, NZD, CHF and BRL are clearly at risk of rebalancing, barring a very strong offset from poor monthly returns in underlying markets.

To recap our rebalancing calculations: We use the “markets are made at the margin” principle, and in doing so, instead of outright asset returns against marginal FX flow, we look at the marginal return against marginal FX flow to determine the incremental hedging needs generated by larger-than-expected moves. We construct a set of marginal monthly returns using the 20-day exponential moving average (XMA) against the 65-day simple moving average (SMA). Subsequently, we calculate scores for these marginal returns and flows by dividing the return and flow sets by their rolling 1y standard deviations – the same methodology we use in iFlow. To proxy for hedging needs, we take the difference between the flow scores and chart the “distance” that the FX flows need to cover to hedge the return profiles.

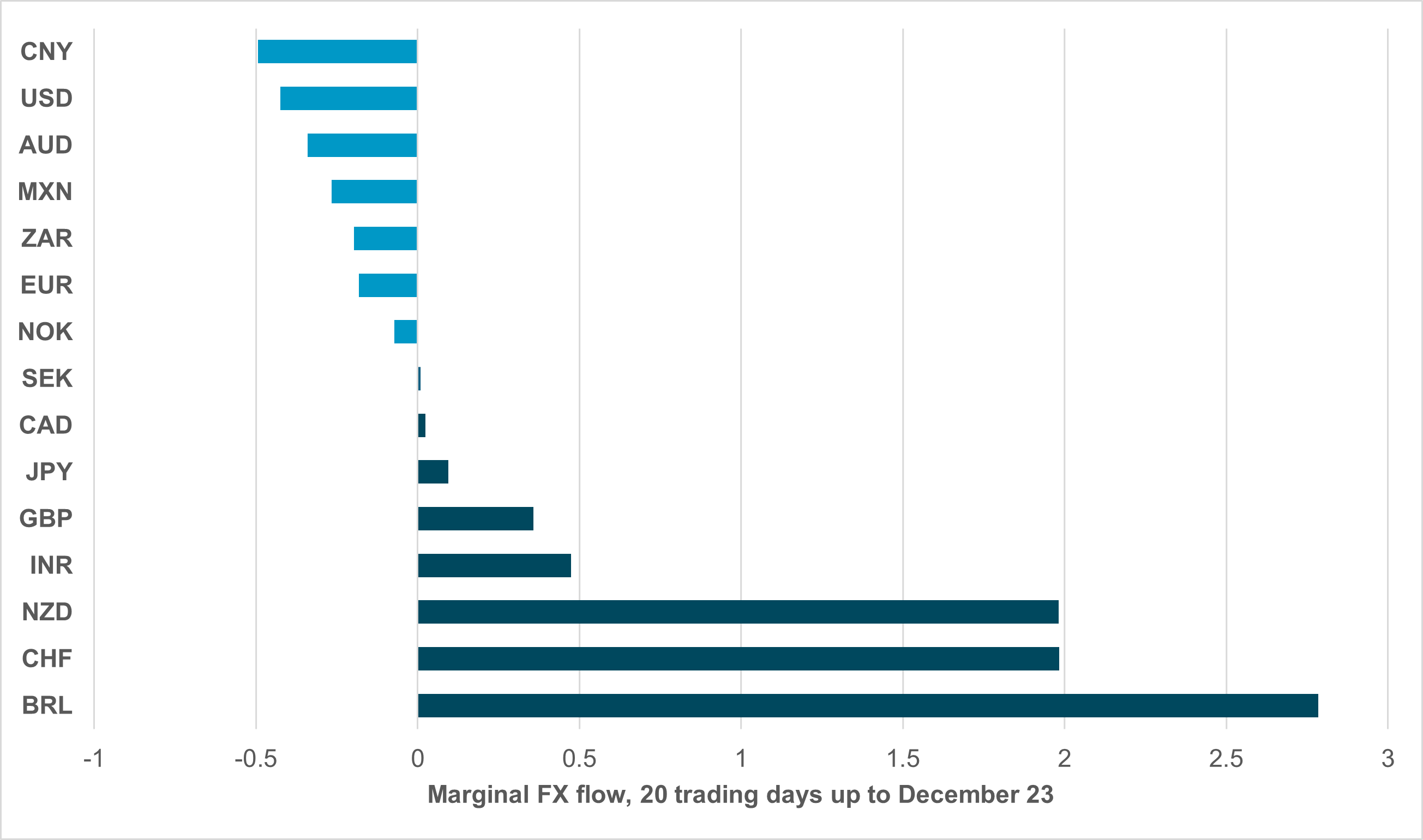

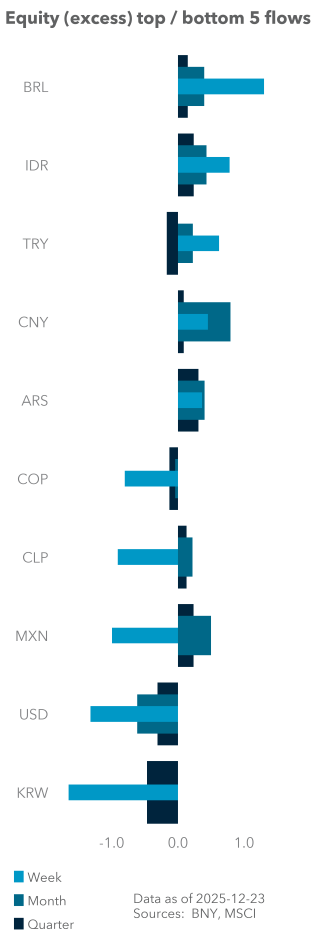

EXHIBIT #2: EQUITY REBALANCING SIGNALS, DECEMBER 2025

Source: BNY iFlow, Bloomberg

Our take

Most of the equity markets we tracked generated positive marginal returns over the month. China, Australia and Norway were the exceptions, and only Australia had a meaningful decline. The Australian dollar (AUD) was also net sold, but even on a combined basis the rebalancing signal was light.

Other currencies that were net sold through the month were offset by good equity performance, which meant that most markets ended the month without a strong rebalancing need for the asset class.

Forward look

Due to their strong FX inflows, the only significant rebalancing signals generated in equity markets were NZD, CHF and BRL. As highlighted earlier, the strong performance of Brazil’s equity market amplified the hedging need, implying significant carry costs if such an approach is adopted. Overall, it is probably preferable to take profits on underlying asset positions toward year end.

Similarly, Switzerland was the best-performing European equity market, as a U.S. trade deal helped recapture certainty for local corporates. In contrast to BRL, there is far less of a carry issue with higher levels of CHF hedging, so this will likely be the preferred approach. Finally, the New Zealand equity market was flat, so FX rebalancing is purely based on realized flows being offset elsewhere.

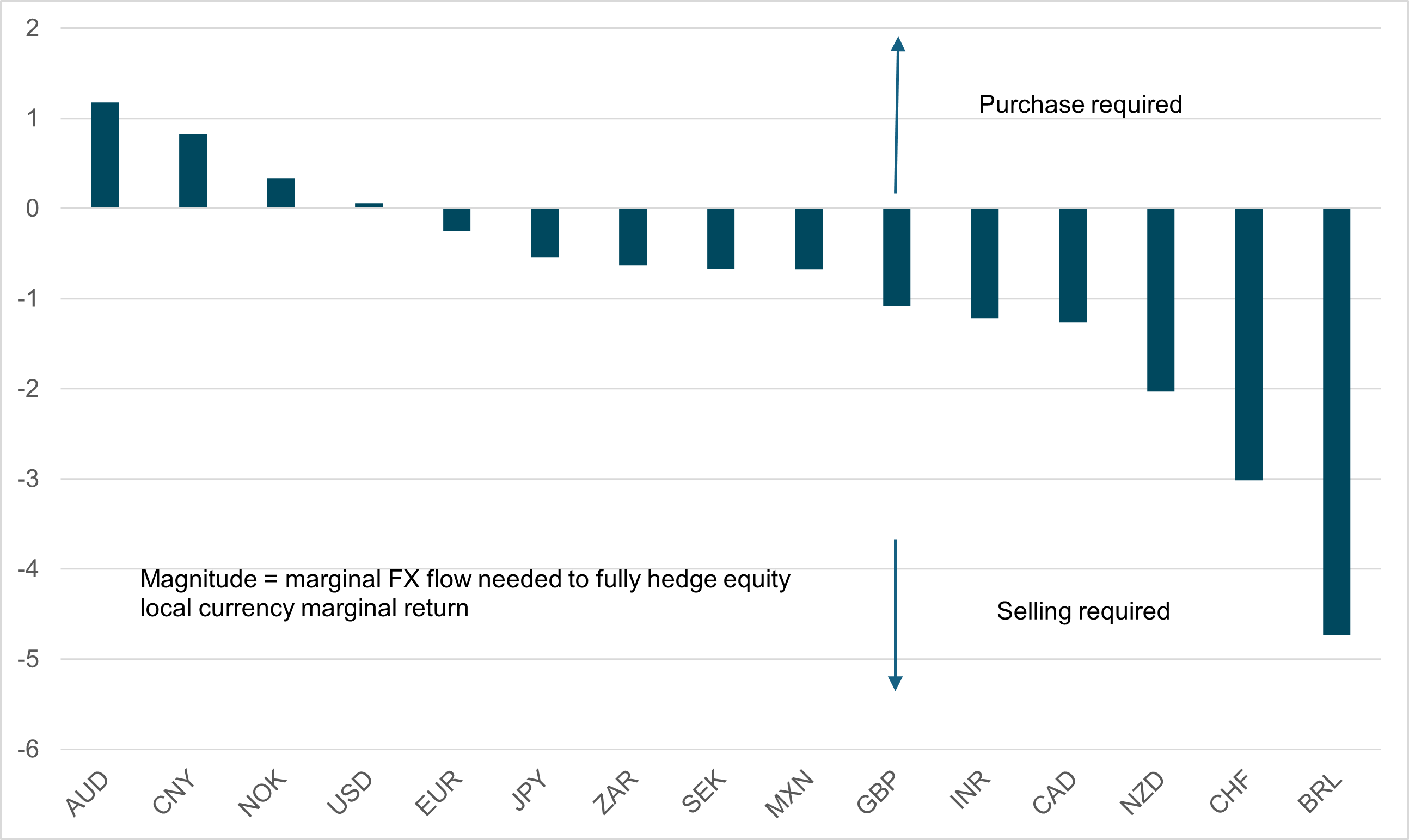

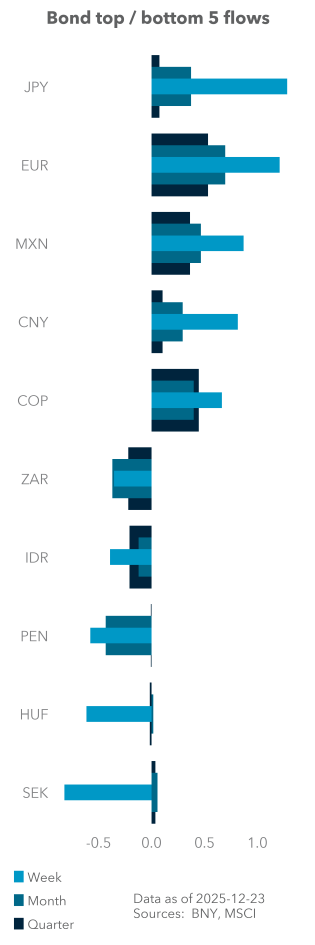

EXHIBIT #3: FIXED INCOME REBALANCING SIGNALS, DECEMBER 2025

Source: BNY iFlow, Bloomberg

Our take

Fixed income performance was more varied through the month. While iFlow Carry was unable to reach positive statistical significance on a marginal basis, South Africa and Brazil were the strongest-performing markets due to positive real rates.

South Africa was again a good example of how a strong and credible inflation mandate could reap dividends for emerging market FX.

Despite being net sold through the month, the rand (ZAR) still generated a net sell rebalancing signal on a combined basis. Of all currencies we track for rebalancing purposes, ZAR has been under the greatest rebalancing pressure throughout the year but has withstood it most effectively due to good alignment between fiscal and monetary policy to avoid fiscal dominance.

Elsewhere, Australia and Japan were the worst performers in fixed income. The former is due to strong expectations of a more hawkish pivot, while the latter is still considered most at risk of fiscal dominance in developed markets, though fears have eased since the budget was put forward.

Forward look

The BRL is once again at risk of rebalancing. Though its fixed income performance was also solid, in absolute terms, duration gains were not as strong as equities over the past 20 trading days, so the combined rebalancing score was somewhat smaller. Nonetheless, it is the only currency in our set with a very strong signal in both assets.

The yen (JPY) and AUD will require some purchases to offset fixed income losses, as currency performance for both was relatively flat. The case to own both remains strong from a valuation point of view, but the latter is preferable in terms of policy execution. Compared to the JPY, AUD holdings are more attractive, and the currency is one of our preferred names for 2026. For the JPY, recent comments by the Japanese government indicate a stronger willingness to push back against currency weakness. However, realizing structural gains would require a far more sustained Bank of Japan tightening cycle and higher real rates, which may continue to run counter to fiscal objectives.