Currency flows should factor in tail risks

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

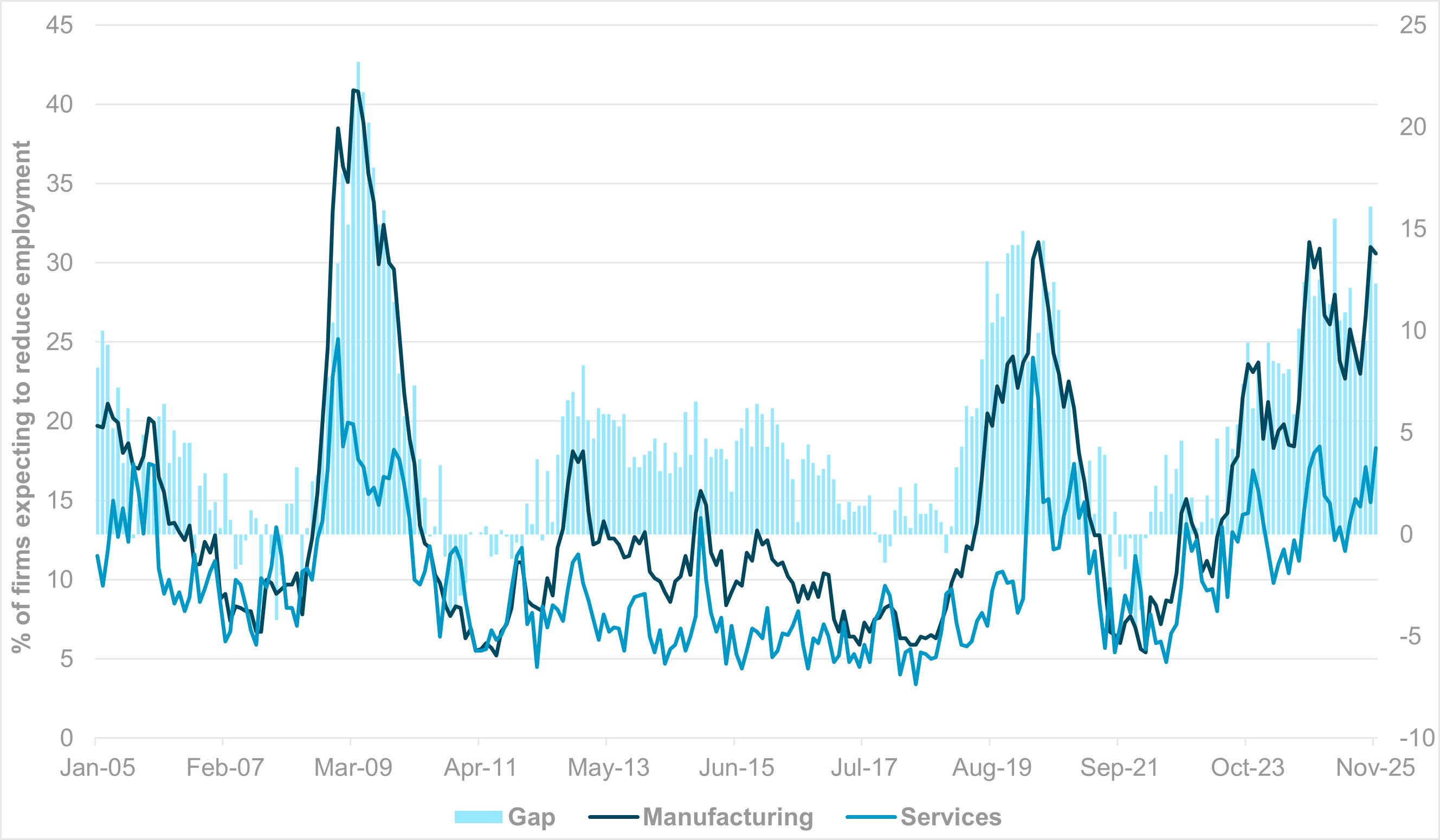

EXHIBIT #1: IFO SURVEY, FIRMS EXPECTING JOB LOSSES BY SECTOR AND GAP

Source: BNY, Macrobond

Our take

Based on the available Q4 macro data, the European Central Bank’s (ECB) December upward forecast revisions will be driven by services-related factors. Yesterday’s labor cost index signaled Q3 wage growth fell to 3.3% y/y, the weakest figure in three years, though still comfortably above current inflation. It will continue to drive real income growth. Construction remains the biggest driver at 4.3% y/y, while industry and services are holding at 3.3% y/y and 3.2% y/y, respectively.

The ECB has long identified construction as a weak productivity sector, while manufacturing has traditionally been the most productive. However, demand for labor in this sector is now falling sharply, as industrial bodies have been highlighting throughout the year. Yesterday's Ifo Business Climate Index for Germany noted that the share of manufacturing firms expecting headcount reductions over the next three months is once again pushing against COVID-period levels. Crucially, the gap in this measure versus services is now at the highest level since the Global Financial Crisis. European leaders are pointing to China as the biggest risk to European manufacturing jobs, with currency valuations a core part of the issue. Yet, the ECB’s ongoing tolerance for currency strength in nominal terms – a far bigger driver this year of the euro’s (EUR) real effective exchange rate (REER) – has barely featured in discourse.

Forward Look

We highlighted recently that the ECB’s repeated raising of anchoring assumptions for the euro’s exchange rate and its impact on inflation has not generated any disquiet within the Governing Council. That is because there has been no impact on services inflation or aggregate wages. That may be correct from an operations perspective, but from a political angle, this stance is no longer tenable. Job losses in manufacturing could mean permanent scarring in the labor force, which means that the high wage growth that the ECB cites becomes less relevant to the real economy. Aggregate demand shifts more toward public spending, which ECB President Christine Lagarde, by her own admission, sees as risking stagflation. We don’t see tensions reaching levels seen elsewhere between monetary authorities and governments. However, the ongoing laissez-faire approach to the exchange rate may no longer be characterized as “benign neglect,” if economic pressures from lack of European manufacturing competitiveness – regardless of the driver – become intolerable.

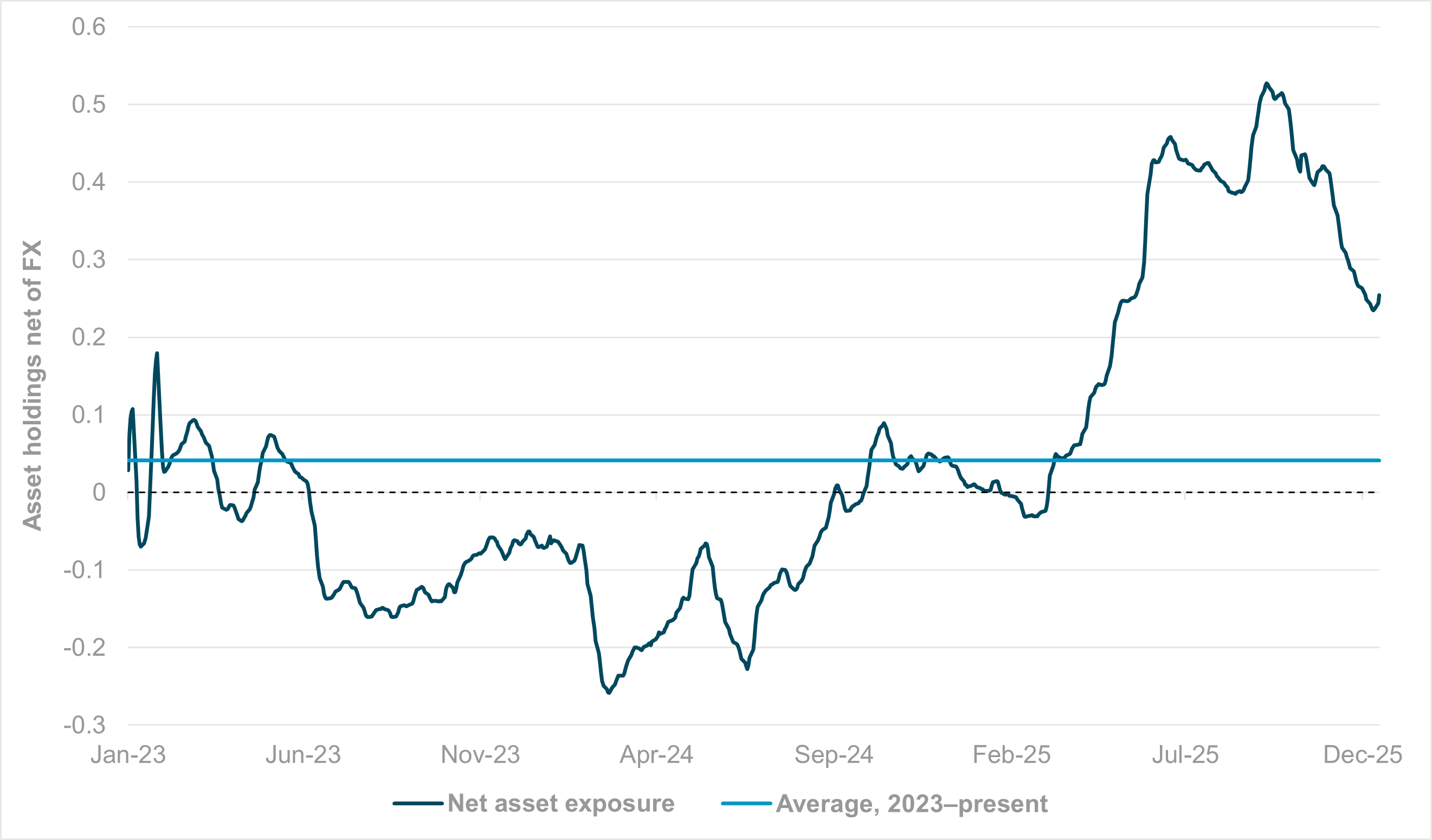

EXHIBIT #2: CROSS-BORDER NET ASSET HOLDINGS IN CHINA, ASSUMING A 25-TO-75 EQUITY-TO-BONDS PORTFOLIO

Source: BNY

Our take

At the beginning of the quarter, we highlighted that net asset exposures to China had reached the highest level in the current cycle. Strong flows into both equity and fixed income markets, boosted further by strength in asset performance, did not generate commensurate levels of yuan (CNY) hedging flows, even though rate differentials continued to favor owning U.S. dollars.

The perception that much of APAC FX would undergo a wave of appreciation to correct imbalances, especially in a more challenging trade environment, has not come to pass. There will be political pressure on Beijing to act next year, but in the near term, we believe FX performance will be carefully managed. The People’s Bank of China (PBoC) will need to closely monitor financial stability, as credit risk in real estate markets has moved to the fore, while equity markets’ performance has become more volatile. The recent round of data across all Chinese sectors disappointed, even against already weak expectations, requiring a more proactive central bank stance. Any planned easing might be brought forward should credit concerns exert additional tightening in financial conditions.

Forward look

Consensus for 2026 points to steady appreciation among surplus economies in Asia. China is under pressure from trade partners to strengthen its REER, but we continue to see the gains taking place through the inflation channel – especially PPI – which is still contracting outright. Doing so fully supports the government’s efforts to curb “involution” and complete the current strategy to boost household demand. The PBoC has also committed to loosen monetary conditions to complement the process, which means that barring a significant risk shock in the U.S., rate differentials will continue to favor retaining relatively high hedge ratios. Even if local assets perform strongly, we expect overall asset exposure, as detailed in Exhibit #2, to gradually revert to the long-term average.

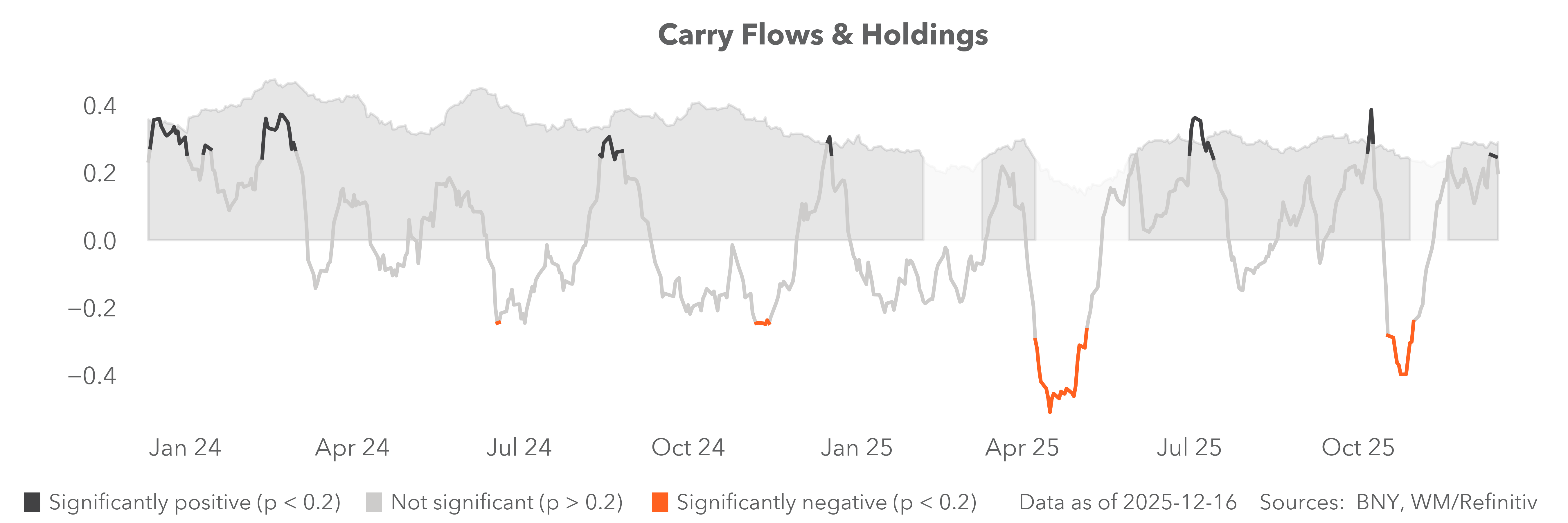

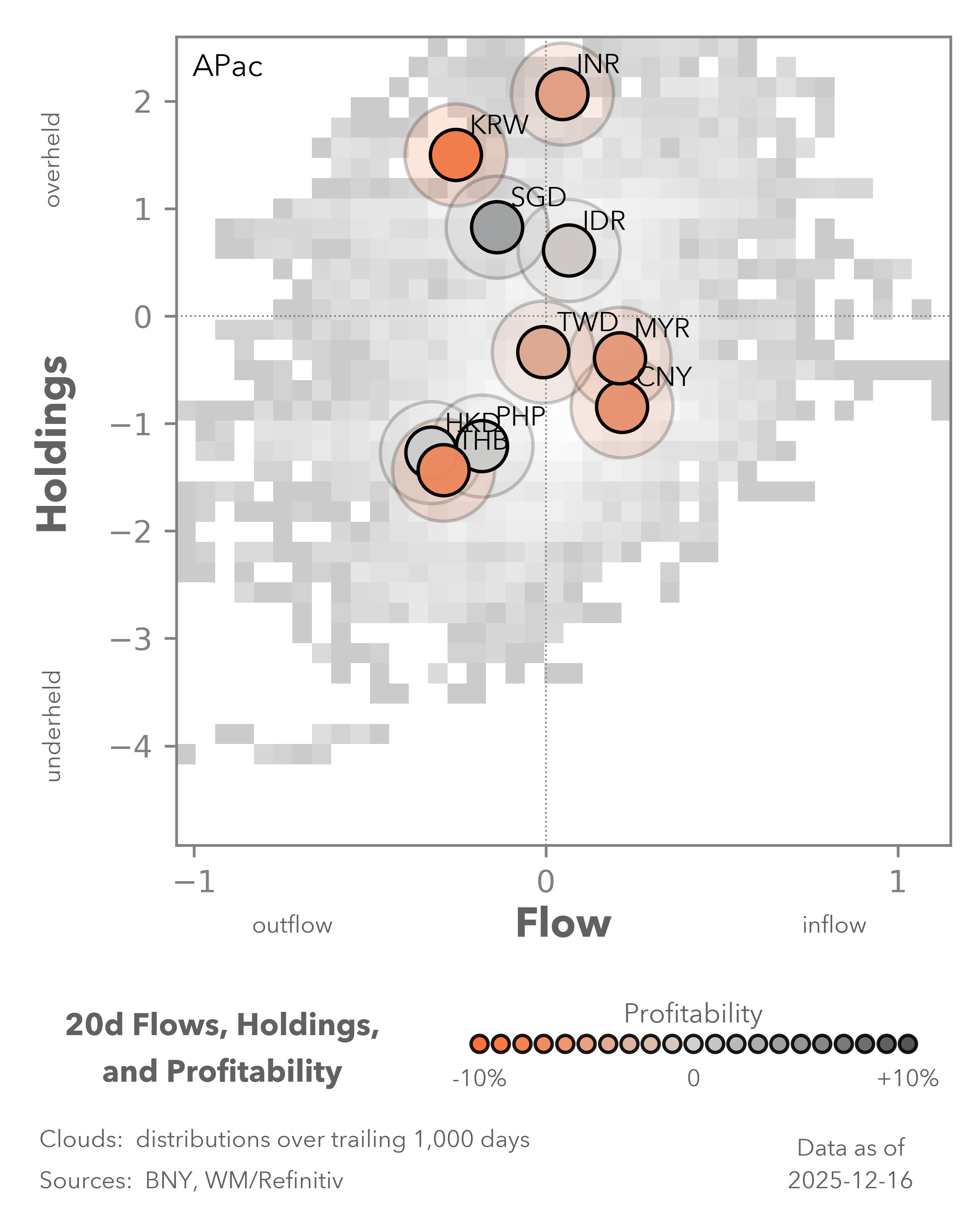

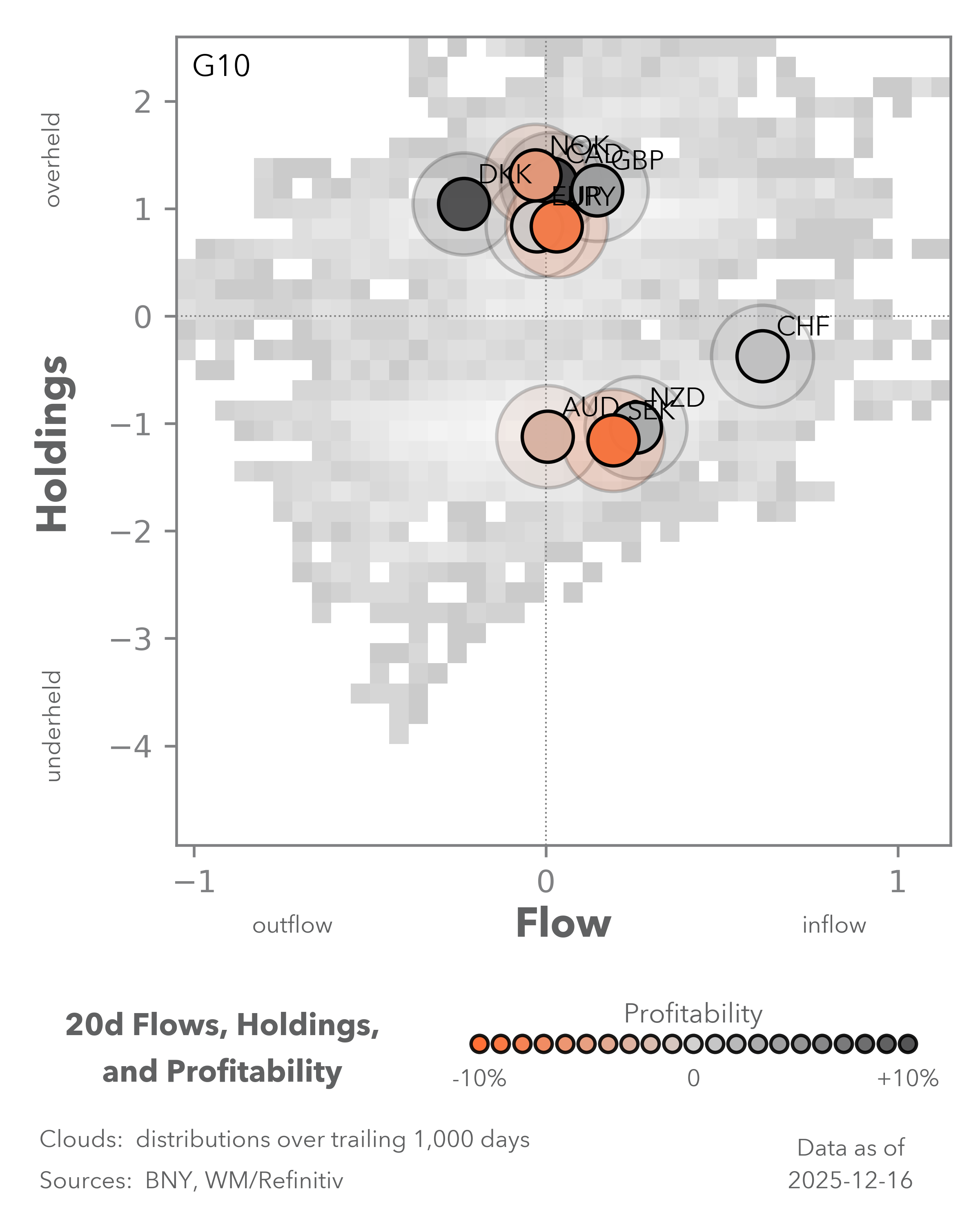

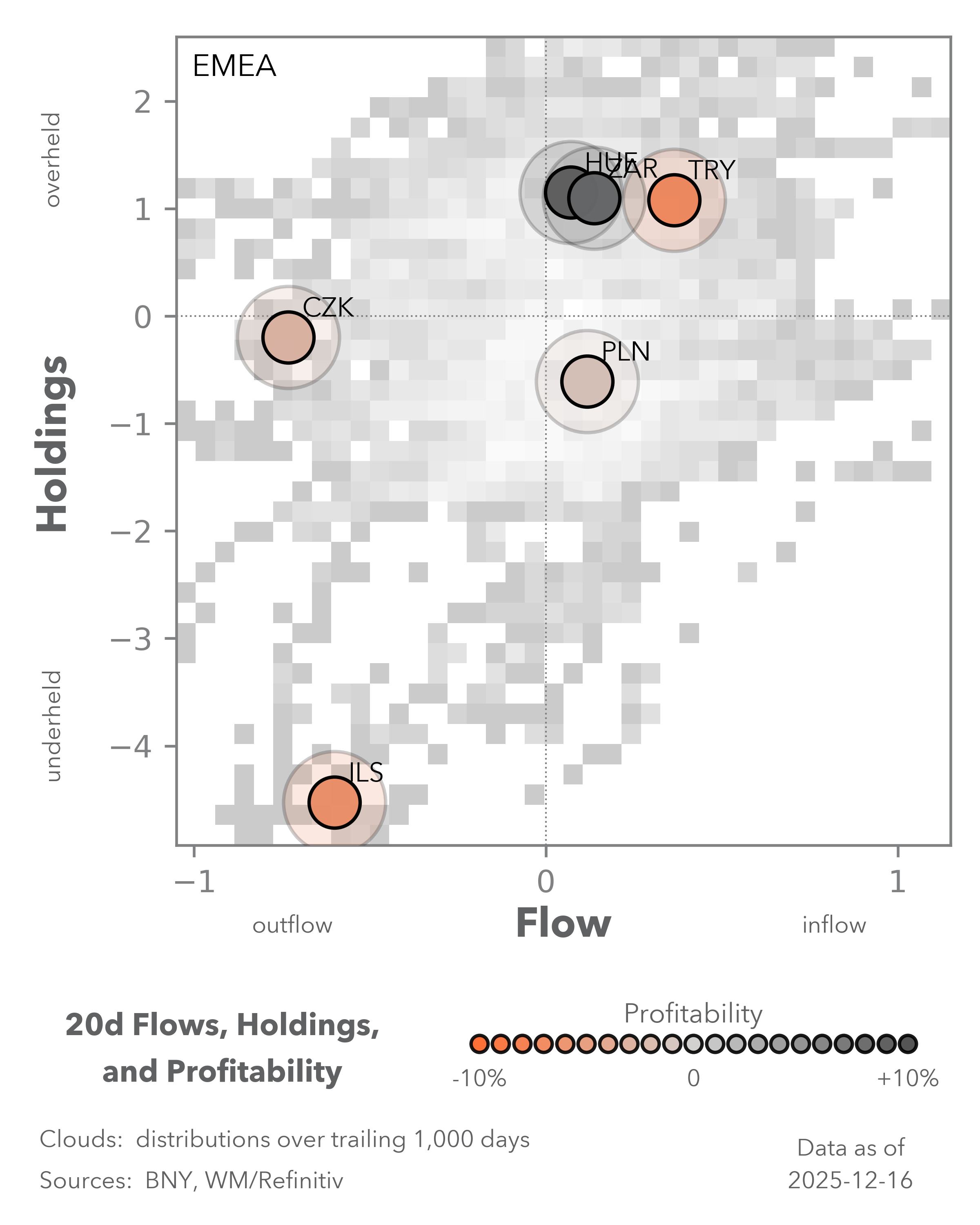

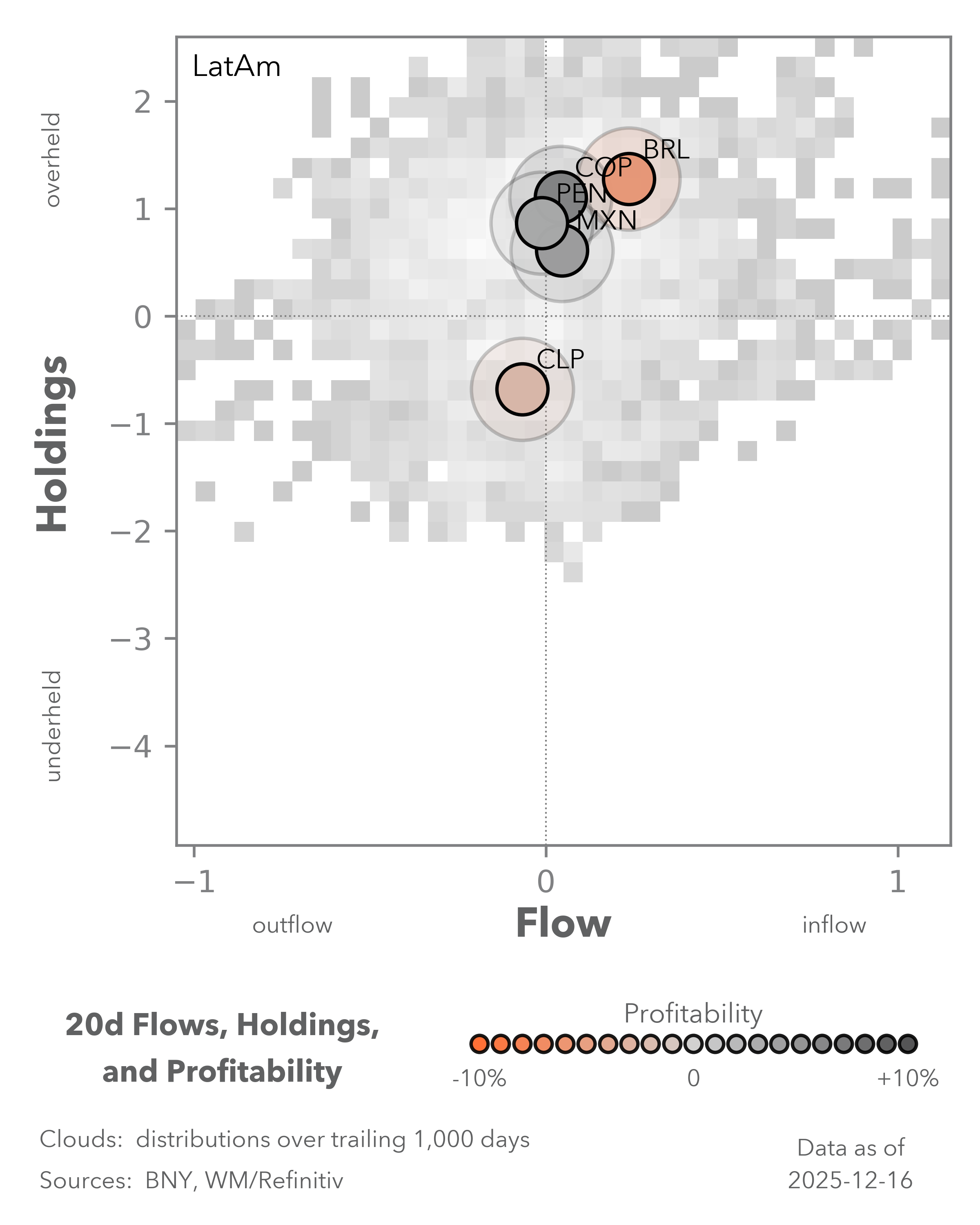

EXHIBIT #3: MONTHLY SMOOTHED FLOW, LATAM AND APAC CURRENCY AGGREGATES

Source: BNY

Our take

If the PBoC remains cautious in the near term, there will be very little relief for financial conditions in other economies across the region. Other economies facing competitiveness concerns from China will likely need to match any moves in the CNY or shifts in PBoC policy. Thailand’s rate cut this week and strong warnings about exchange rate strength are the clearest example of this. At close to 1%, there is even scope to use a basket of APAC currencies as funders for carry trades. Like the CNY, the yen (JPY), won (KRW) and Taiwan dollar (TWD) have a case for long-term valuations-based appreciation, but policy differentials have undermined those efforts.

iFlow is also seeing further selling in the Singapore dollar (SGD), while the Hong Kong dollar (HKD) has retained funding status. This has driven the APAC FX aggregate to its worst flow position in the past five months. Meanwhile just as Latin American (LatAm) currencies are recovering toward their strongest period of inflows over the same period (Exhibit #3).

Forward look

At this rate, iFlow Carry is likely to move back into positive statistical significance, but we doubt there is much appetite to hold large carry positions heading into year end.

Furthermore, we believe markets will need to be selective about funding currencies. Underlying drivers in the region have shifted materially this year, with new sources of volatility including U.S. trade deals and changes in hedging strategies by long-term onshore real money funds. In Taiwan and South Korea, policymakers likely recognize that current surplus levels are unsustainable. Limiting volatility from AI-driven equity stress will also require more active management. Furthermore, if CNY’s REER rises over time, regardless of the nominal or inflation channel, the rest of APAC would be in a much better position to follow.

In LatAm, politics and relations with the U.S. are becoming more dominant flow drivers. Still, as long as central banks can anchor real rates, underlying flow interest is likely to remain strong.