AI, IPOs and the Next Market Test

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 6 minutes

The 2026 risk debate reflects a broader economic philosophy, with “you win, I lose” global equity flows connected to AI-bubble risks and the U.S. dollar. The consensus view of a the U.S. soft-landing favors a win-win environment, where strong corporate earnings create a positive-sum outcome, allowing various sectors to thrive together and helping the rest of the world, too.

Proponents of this view see opportunities beyond tech giants, arguing that collaboration and a long-term focus can benefit everyone. But fears of an AI crash and renewed U.S.–China trade conflict highlight downside risks, where a “conflict or trade” choice could disrupt global markets. Political zero-sum debates also loom, with U.S. partisanship and key elections for Brazil and beyond reshaping how investors view long-term growth. Renegotiation of the U.S.–Mexico–Canada Agreement (USMCA) may prove pivotal in settling trade and investment direction.

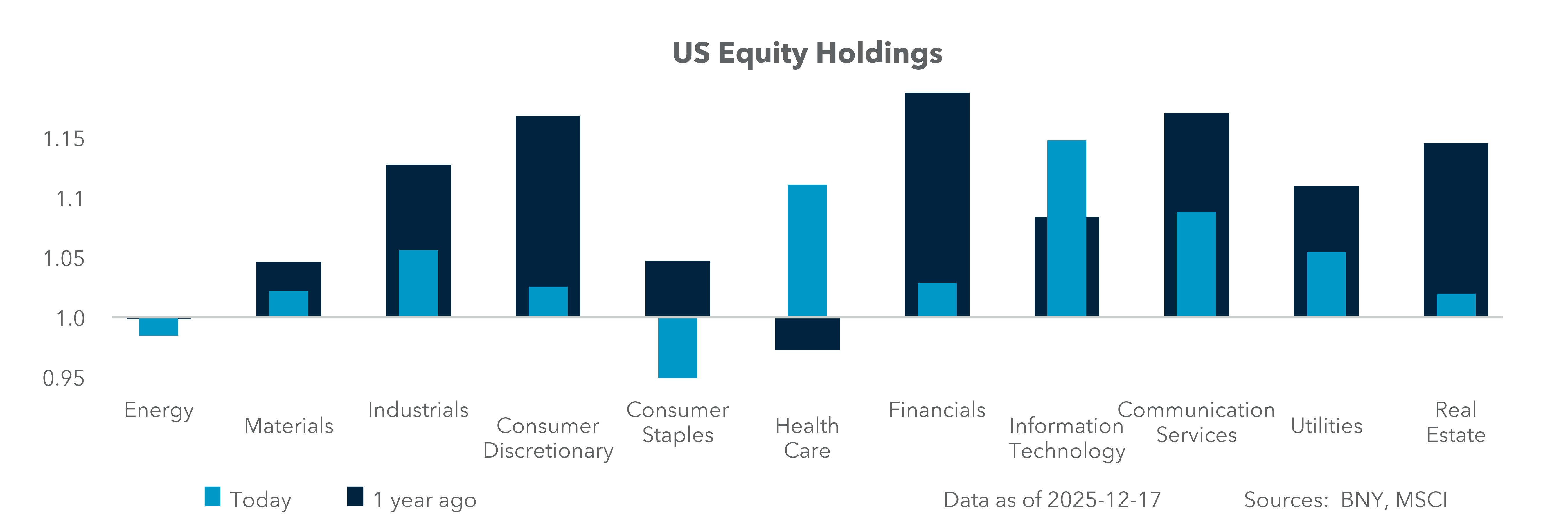

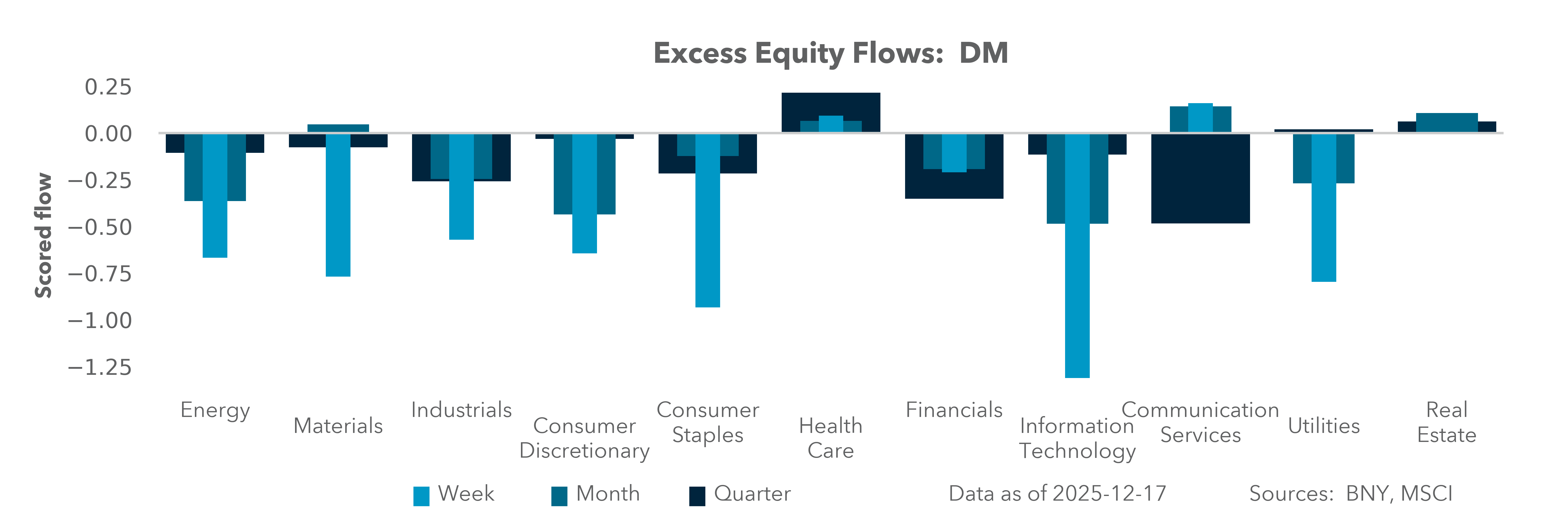

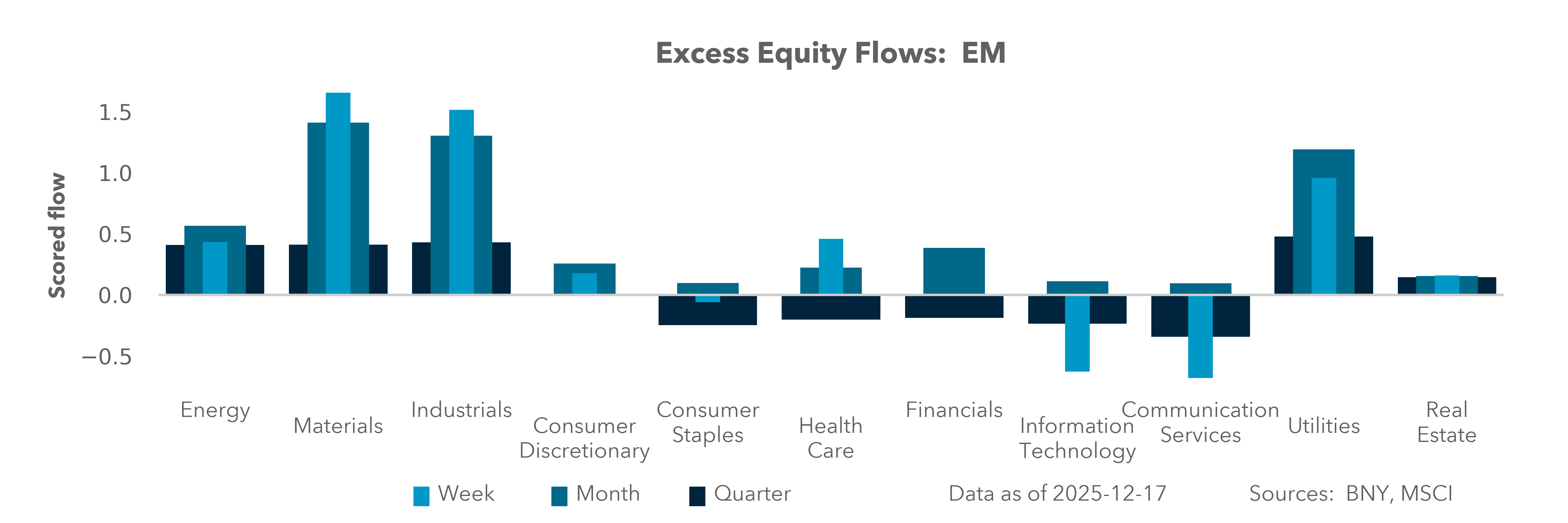

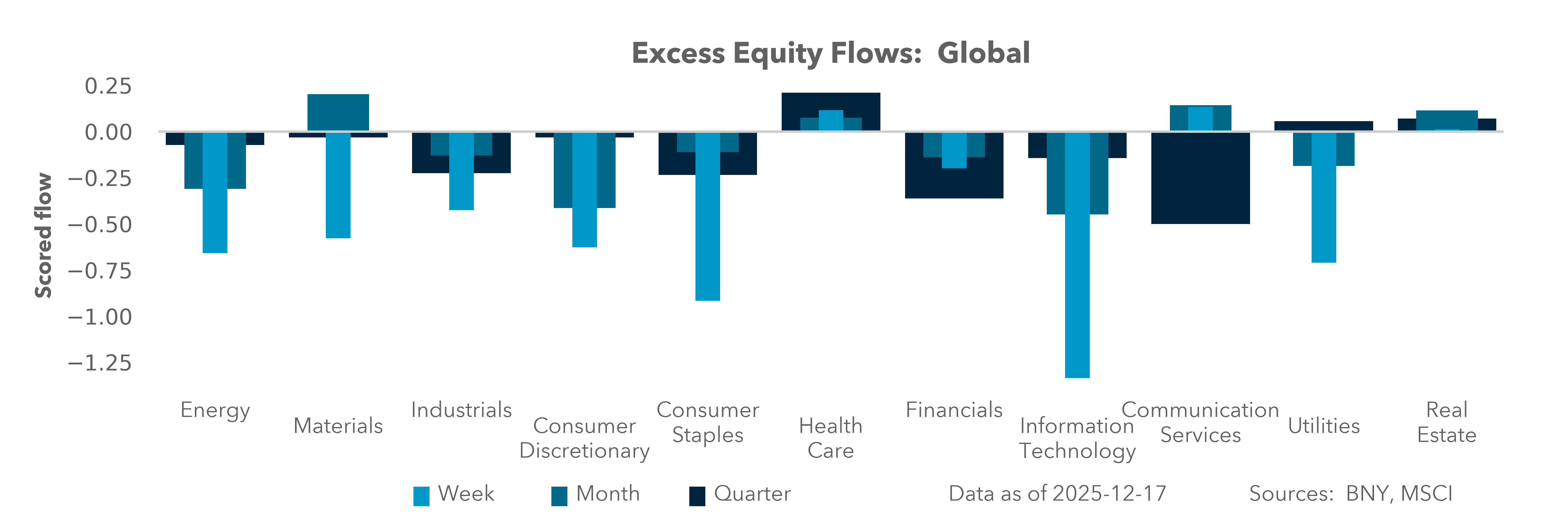

The bearish case for equities starts with stretched technology valuations and turns to which alternatives can manage the rotation. iFlow shows 65% of equity exposure in the U.S. markets and under 1% in China. Markets want a win-win scenario that includes Financials, Industrials and Consumer Staples, but each requires its own economic and policy setups. The outcome will rest on FOMC rates, U.S. midterm elections and global policy tweaks.

Digging into the AI risks continues to be the main exercise for equities into 2026.

AI and the temporal problem. Time remains a uniquely human concept, which is why many argue AI remains far from artificial general intelligence (AGI) – the kind that can think and adapt like a human. In theory, a system with vast knowledge should be able to interpret time through a historical lens, identify patterns and apply them to current conditions. But modern markets reward deep specialization over generalist knowledge, creating silos where micro-level narratives can unexpectedly drive macro outcomes. As a result, AI must evolve in how it compares disparate information sets. At the same time, there is a risk that marketing-fueled investment may be oversupplying data centers and chip capacity, echoing the excesses of the late-1990s dot-com bubble.

Data centers and energy. The biggest IPO in 2026 will be SpaceX, with valuation estimates ranging from $1tn to $1.5tn. The company is challenging the communications industry, from AT&T and Verizon to Charter Communications and Comcast. The biggest surprise of the IPO is its longer-term goal to put data centers into space. Solar power and space cooling could offset the cost of putting centers into orbit. There is also a security benefit, as Earth-related disasters are ongoing and costly.

LLM battles and winner-take-all thinking. OpenAI is set to launch the second-largest IPO of 2026, estimated at $1tn. The risk of another China DeepSeek moment seems high heading into this event. In the same vein, the battle between OpenAI, Google, Anthropic and others is wide open, with winner-take-all concerns rising as large-language models (LLMs) link to consumer and corporate demand. The interlinked ecosystem matters: Microsoft owns 27% of OpenAI, which is also one of Nvidia’s largest customers. Oracle and CoreWeave’s AI data center buildouts add to circularity concerns, as OpenAI has committed $1.4tn to future expansion, financed through blended investment and commercial agreements.

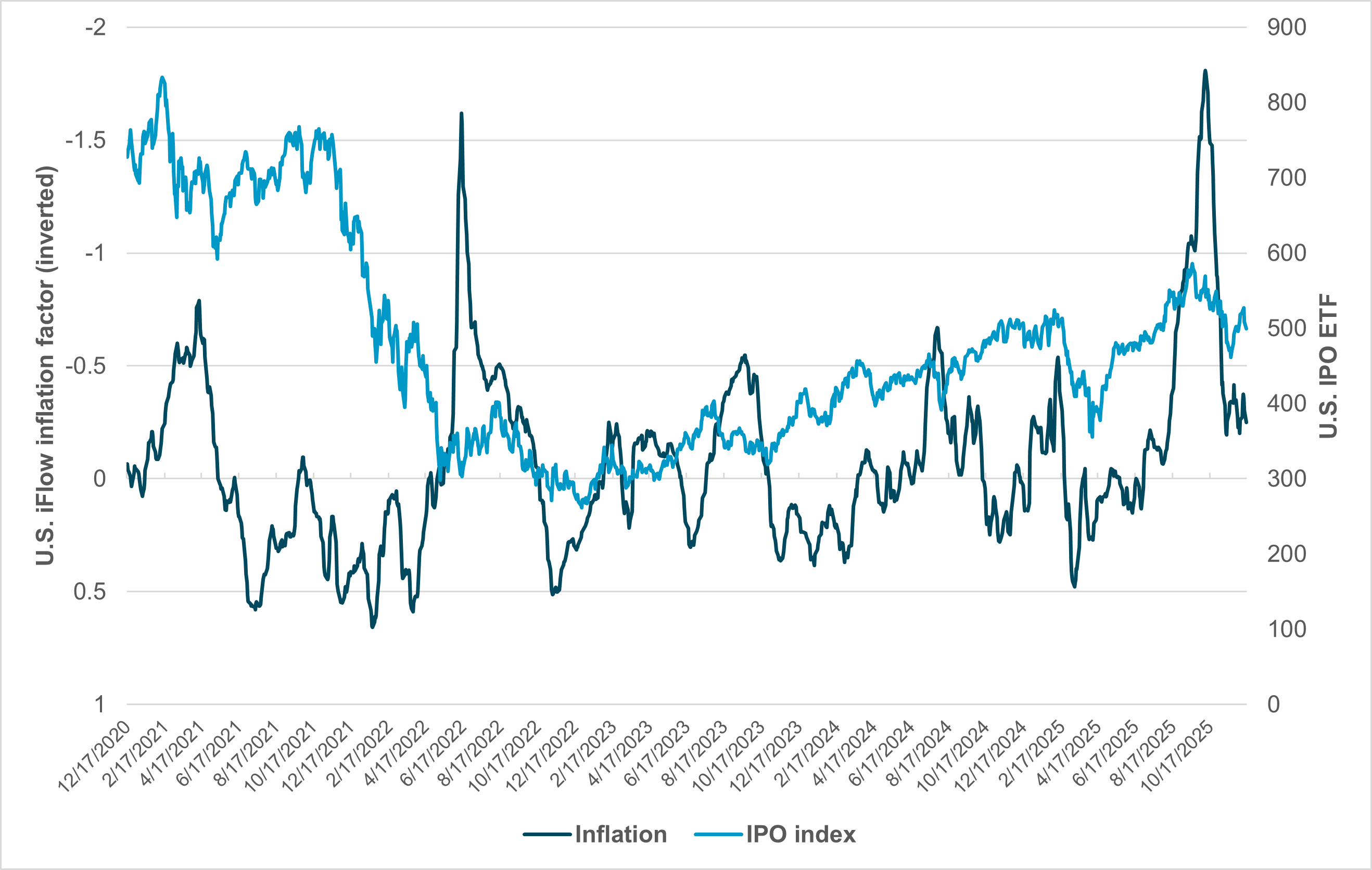

EXHIBIT #1: : U.S. IFLOW INFLATION FACTOR VS. IPO ETF

Source: BNY, Bloomberg

Our take

iFlow tracks U.S. equity flows linked to the inflation beta of S&P 500 stocks. This inflation factor dropped sharply in 2025 but rebounded after the Q4 Fed cut. Inflation fears are inversely related to IPO expectations and payout.

The IPO ETF tracks the performance of newly listed U.S. companies, and it tends to perform best when inflation fears are low. Business success rests on earnings and margins, where inflation causes trouble unless costs can be passed on to the end consumer. The current IPO environment is constructive, supported by a positive trend and distance from the 2020 period of low rates and confusing demand.

Forward look

Energy costs will be critical to midterm outcomes and could set the pace for corporate earnings. Energy still has a disproportionate role in costs across most sectors. Concerns that data centers are driving electricity costs to consumer-pain levels have already materialized.

The link between inflation, politics and corporate margins will be increasingly important in how markets trade in 2026.

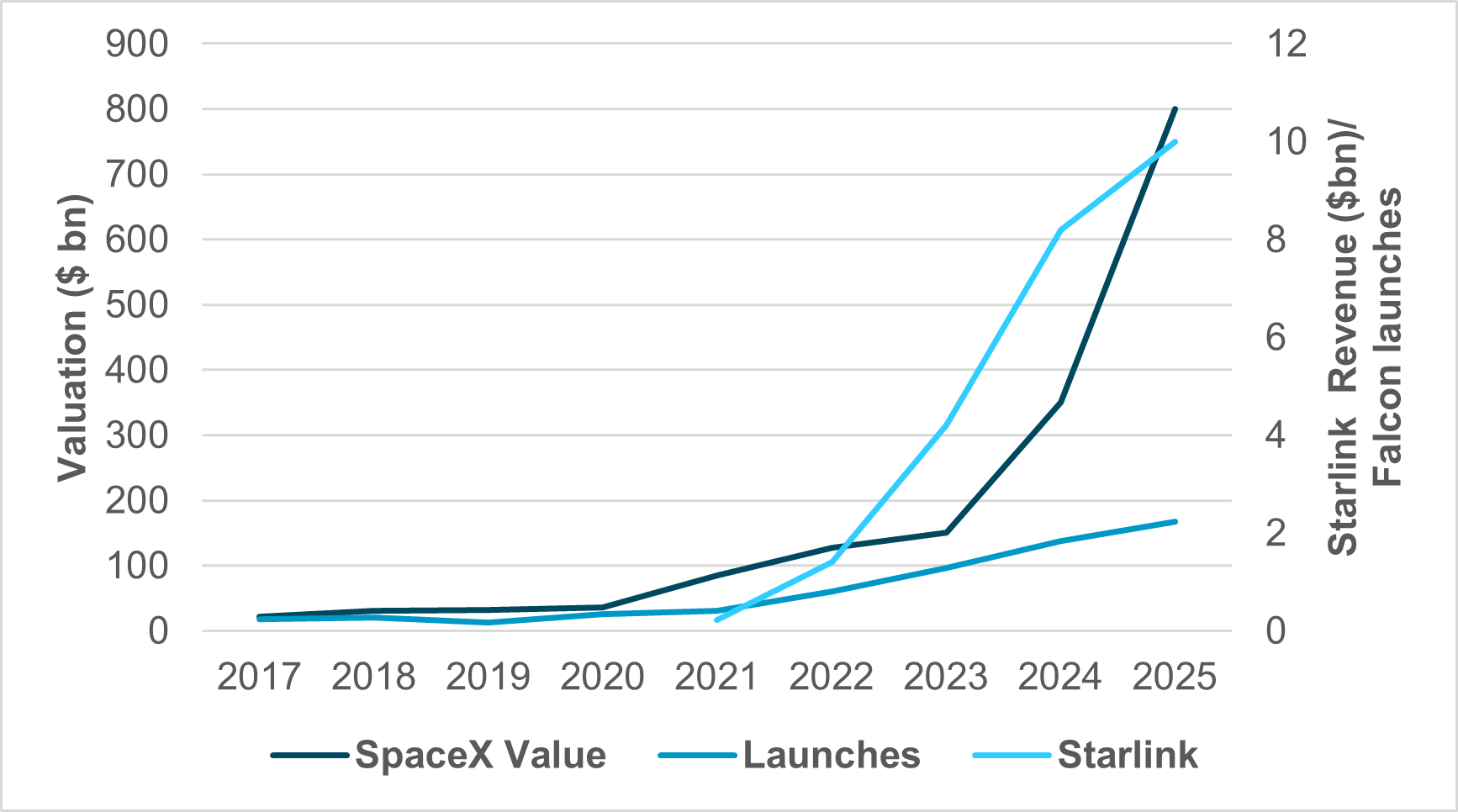

EXHIBIT #2: SPACEX VALUATION VS. REVENUE DRIVERS

Source: BNY, Bloomberg

Our take

SpaceX’s last valuation of $800bn came from private market share sales, double its $400bn value in July 2025. The company confirms it is planning an IPO in 2026, with some analysts calling for a $1.5tn valuation.

Currently, SpaceX generates about $15bn in revenue, with $10bn from Starlink customers, whose numbers have grown from 2.3mn in 2023 to 8mn in 2025. The rest of its revenue comes from Falcon launches, which grew from 25 in 2020 to an estimated 170 in 2025. SpaceX also holds multi-year government contracts, including moon base development through Human Landing Systems. Lunar missions are a high-stakes part of SpaceX’s future, with mineral extraction and data center projects linked to the effort.

Forward look

SpaceX faces two key risks – debt and the need to grow faster in core businesses as it expands into data centers and lunar infrastructure.

SpaceX’s current debt includes a $17bn deal to acquire EchoStar Spectrum, with $2bn in debt payments through November 2027, $8.5bn in cash and the remainder in stock. Leveraged loans were tapped over time, but since 2024, the company has been self-funded. Free cash flow is projected to top $5bn in 2026. This implies a P/E ratio of 53, one that could shift dramatically if other units start generating revenue.

This is the key to a higher valuation. The two largest U.S. communications companies saw 35–40% declines in market cap, down from $125bn, with P/E ratios around 17 in 2025, reflecting challenges in the consumer cable and connectivity sector. The SpaceX threat is not part of that equation yet, but it will be in 2026.

Equinix and Digital Realty – two mature data center providers – have a combined market capitalization of roughly $140bn and P/E ratios of 17. While the risk that SpaceX will eat into their businesses is low today, it may increase over time. For investors, modeling future demand and growth will depend on how the broader AI investment cycle plays out.

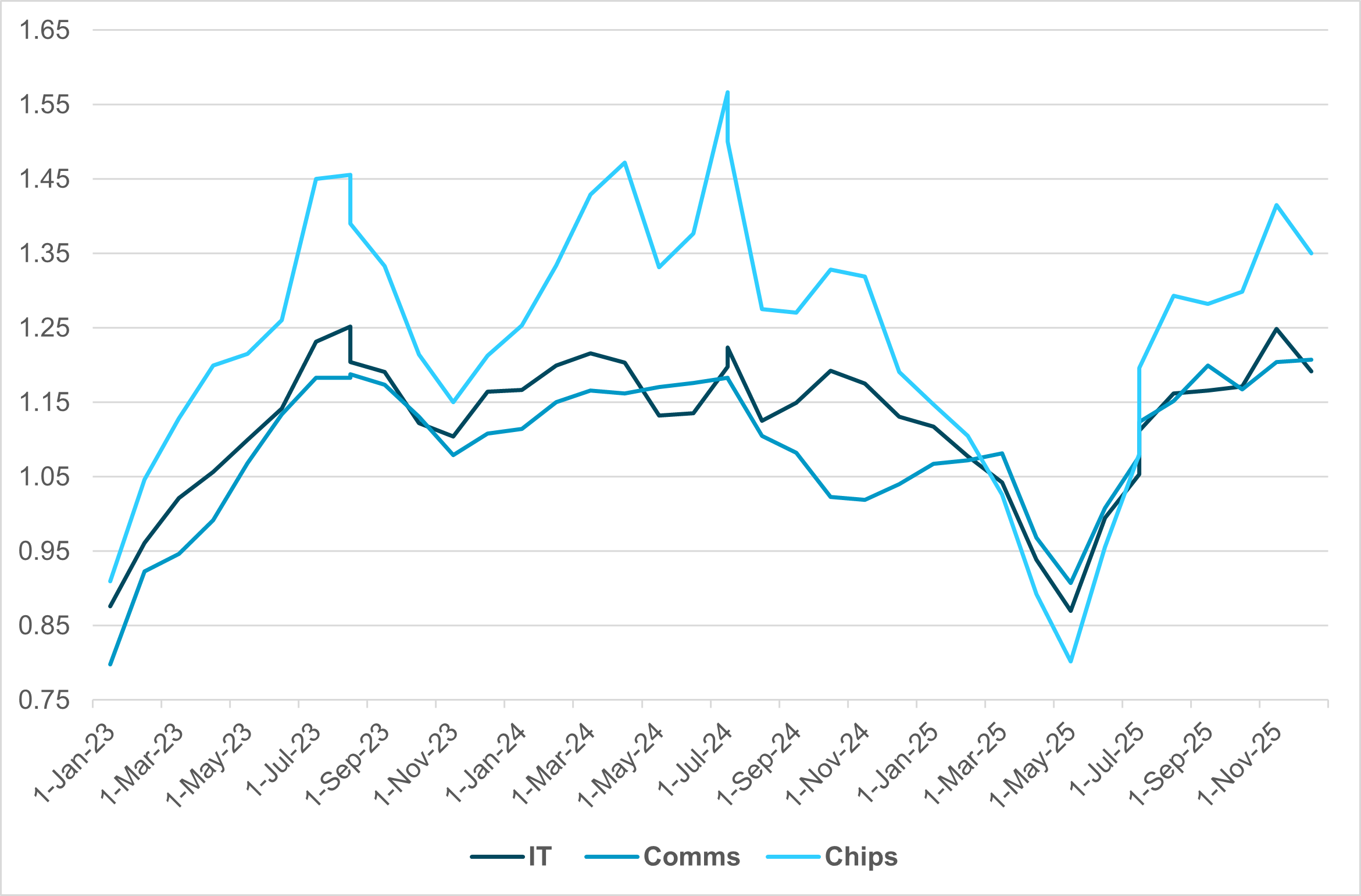

EXHIBIT #3: IFLOW CROSS-BORDER HOLDINGS – U.S. IT, COMMUNICATIONS AND SEMICONDUCTORS

Source: BNY

Our take

Foreign investors hold the key to extending the AI investment boom. IT equity holdings are 6% above their 3y average, while Semiconductor and Communications holdings are 10% above average. A return to the longer-term 10y average could imply a 15–20% drop in market capitalization.

Investors hold a winner-take-all view on AI, with U.S. and China in competition. Upcoming LLMs and IPOs are clearly in play.

According to Bloomberg, OpenAI’s latest infrastructure roadmap could drive nearly half of the projected $2.6tn in combined capex by Microsoft, Meta, Google and Amazon AWS from 2025 to 2030 – more than triple their aggregate spending from 2023 to 2025. New supply agreements with Nvidia, AMD and Broadcom, built on the $500bn Stargate program, lift OpenAI’s total planned compute investment to more than $1tn through the end of the decade, making it the largest driver of AI accelerator demand.

Forward look

The anticipated 2026 OpenAI IPO will be closely watched, especially as a contrast to SpaceX. The current burn rate for OpenAI is estimated to be around $4bn a month. This reflects deep infrastructure investments, from data centers and chips to R&D. Revenue has grown exponentially, from $200mn in 2022 to $13bn today.

Currently, 70% of revenue comes from subscriptions to its Agents, while cloud computing plans remain under development. Hardware partnerships with Apple and others, along with Sora’s text-to-video platform, also contribute to its bottom line. The projection for OpenAI to break even comes in 2030, with peak burn in 2028 of $78bn. The implication for markets seems clear: leverage and belief in the AI model narrative will shape how 2026 unfolds.

Looking ahead, markets face an unusually binary outlook shaped by the tension between collaborative economic expansion and zero-sum competitive pressures. The viability of a win-win environment will hinge on whether policymakers can engineer rate cuts that stabilize inflation without reigniting it, while geopolitical actors avoid escalating trade conflicts that could fracture global supply chains.

Meanwhile, the outsized influence of AI-related capital expenditure – driven by SpaceX’s infrastructure ambitions and OpenAI’s unprecedented compute buildout – will test both energy systems and investor conviction. High-stakes IPOs could either validate decades-long innovation narratives or expose structural overreach reminiscent of prior tech cycles.

Ultimately, 2026 will be defined by how effectively markets reconcile technological optimism with political and macroeconomic constraints. If policy clarity improves and AI investment proves durable rather than speculative, the year may evolve into a broadly positive-sum outcome. If not, volatility could dominate as global capital reassesses risk.