ETF Corner: Market Intelligence hub

Explore ETF market intelligence from BNY, including industry trends, ETF innovation, lifecycle insights, and data-backed perspectives.

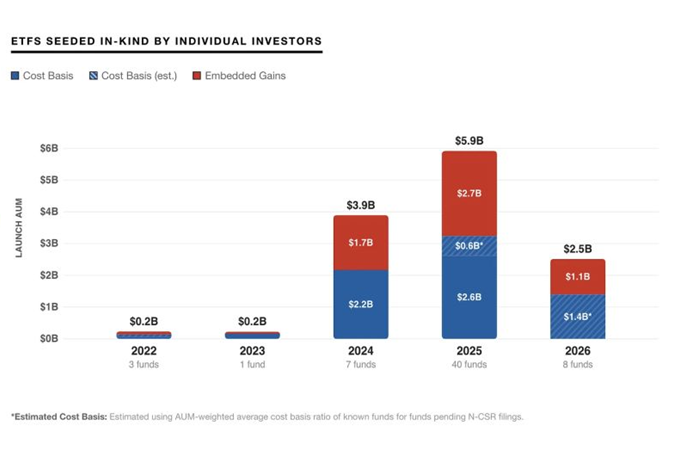

As ETFs continue to evolve from simple investment vehicles into strategic portfolio tools, Section 351 conversions are drawing broader attention across the market. As of May 2026, 77 U.S. ETFs launched with approximately $16.6 billion in seed assets from individual investors, underscoring how quickly this part of the market is evolving.

59

ETFS

$12.8B

Launch AUM

$7.1B

Cost basis

*$6.9B known + $2.3B est. (18 funds pending N-CSR)

Last updated March 23, 2026

Disclaimer: Graph created and data compiled by 351.tax using publicly available information from SEC EDGAR filings, Bloomberg Terminal data, issuer press releases, and fund sponsor websites. Cost basis and embedded gain estimates are derived from disclosures contained in N-CSR filings and related regulatory disclosures.

Source: The Street - Wall Street Found an ETF Tax Loophole Worth $8.7 Billion; 351.tax; ETF Prime Podcast: 351 Exchanges, Thematic Investing, and Leveraged ETFs

Section 351 conversions are gaining traction because they sit at the intersection of several forces shaping the ETF market today. Investors are looking for more tax-aware ways to manage concentrated positions, while issuers and service providers are supporting more sophisticated approaches to ETF seeding, portfolio transition and product development.

For asset owners, the opportunity is not just transactional. It reflects a broader strategic question: how can existing holdings be used more efficiently in support of future portfolio goals? In that context, 351 conversions are becoming part of a wider conversation about portfolio construction, product access and how legacy positions can be transitioned into more scalable investment vehicles.

Much of the interest in 351 conversions stems from their potential tax treatment. If the relevant conditions are satisfied, investors may be able to contribute appreciated securities into a newly launched ETF and receive ETF shares on a carryover basis, with gain generally deferred until a later taxable disposition.

In addition, for investors with concentrated positions, a 351 conversion may also create a path to greater diversification. Once assets are held through the ETF wrapper, investors may also benefit from the features that continue to support ETF growth more broadly, including flexibility, transparency and liquidity.

For asset owners, that makes 351 conversions relevant not simply as a tax-efficient transition tool, but as a potential way to improve how exposures are packaged, accessed and managed over time.

That matters because qualification depends on specific requirements, and both structure and intent matter. Key considerations include:

For asset owners, the implication is clear: as interest in the structure grows, so too does the importance of governance, documentation and disciplined design.

BNY’s Execution Services team has supported approximately $4 billion in Section 351 conversion activity over the past two years, helping ETF issuers navigate the creation and redemption process for newly launched ETFs. Working across single and multiple custodial relationships, the team coordinates the receipt of ETF basket components, facilitates efficient ETF creations and supports timely share delivery to the appropriate custodians.

Even where the strategic case is compelling, 351 conversions are not simple to execute. They can require close coordination across execution, custody, operations, tax and ETF servicing functions, often involving multiple parties and multiple custodial relationships.

That operational complexity is one reason the market is placing greater emphasis on end-to-end support. As 351 conversions become more visible, firms are increasingly evaluating not only whether a transaction is feasible in theory, but whether it can be delivered smoothly in practice.

Numerous Pershing RIA clients have also inquired about the mechanics of a Section 351 conversion and the ability to support the process across the ecosystem, including as sub-advisor for the newly formed ETF.

For clients, that means the quality of the operating model matters. The ability to coordinate basket receipt, facilitate ETF creations and manage timely share delivery across custody arrangements can directly affect how effectively a conversion is implemented. Just as important is the ability to navigate nuance, because each client set-up, portfolio profile and servicing ecosystem may look different.

Providers that can combine execution capability, operational coordination and ETF ecosystem knowledge can help clients move from concept to implementation with greater confidence - especially when the structure requires precision rather than standardization.

The next phase of the opportunity is unlikely to be defined by demand alone. It will be defined by preparedness across a broader set of questions. Does the portfolio qualify? Does the intended ETF strategy align with the assets being contributed? Is there a governance framework around rationale, documentation and oversight? And is there an operating model in place that can support the transaction from launch through ongoing servicing?

The firms best positioned to benefit from the 351 conversion opportunity will be those that can connect tax awareness, product strategy and operational readiness in a coherent way.

That is why the conversation around 351 conversions is becoming more strategic. The opportunity is real - but so is the need for thoughtful execution.

For more insights about ETF, visit BNY’s ETF Corner, one destination for ETF market intelligence and expertise.

READY TO TALK ABOUT

WHAT'S NEXT?