Securities Finance

Agency lending, principal lending, and additional funding and prime services.

Insights

Alternative Asset Strategies for Private Wealth Managers

Time to Read: 6 minutes

Alternative assets, or “alts,” such as real estate, private equity, private credit, hedge funds and infrastructure have historically constituted less than 3% of private wealth portfolios,1 but industry experts predict alternative assets under management (AUM) for private wealth investors to grow three-fold from $4 trillion to $12 trillion over the next decade.2

Wealth managers are increasingly drawn to alternatives due to their ability to deliver diversification and lower correlation versus listed equities or bonds, helping portfolios absorb shocks and smooth returns across cycles. Alternative assets were historically built for institutional operating models, and their product structures and distribution methods reflected that framework. As access to alts broadens into the wealth channel, alternative asset managers are reworking those models — introducing interval and evergreen structures, enhancing transparency and tax‑efficient wrappers and aligning distribution and reporting to meet private‑wealth needs and preferences.

With growth of the global high-net-worth individual (HNWI) population at estimated at 2.6% in 2024,3 it may constitute the single biggest source of demand for alts from the private wealth sector, which tracks to why over 84% of wealth managers surveyed by BNY Pershing last year expected their alts allocations to increase into 2026.

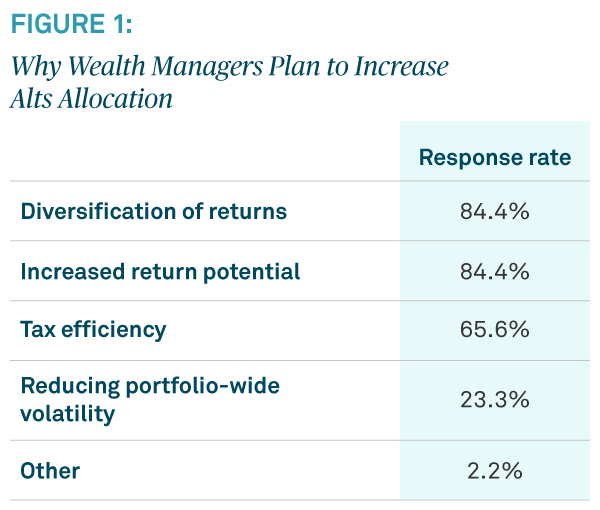

Wealth managers are increasingly drawn to them because of their capacity to deliver enhanced and longer-term returns, lower volatility, tax efficiency and meet the need for portfolio diversification. Among the wealth managers surveyed by BNY Pershing, a high proportion said they use alts for longer-term returns (89%) and to generate current income (69%). BNY Pershing’s survey also found that diversification of returns and increased return potential are among the greatest drivers for future alts investment — 84% of respondents selected these two factors as reasons they plan to increase allocation to alts over the next year.

Source: BNY Pershing survey: “Wealth Trends in Alternatives: Optimizing Opportunities,” Feb. 10, 2025

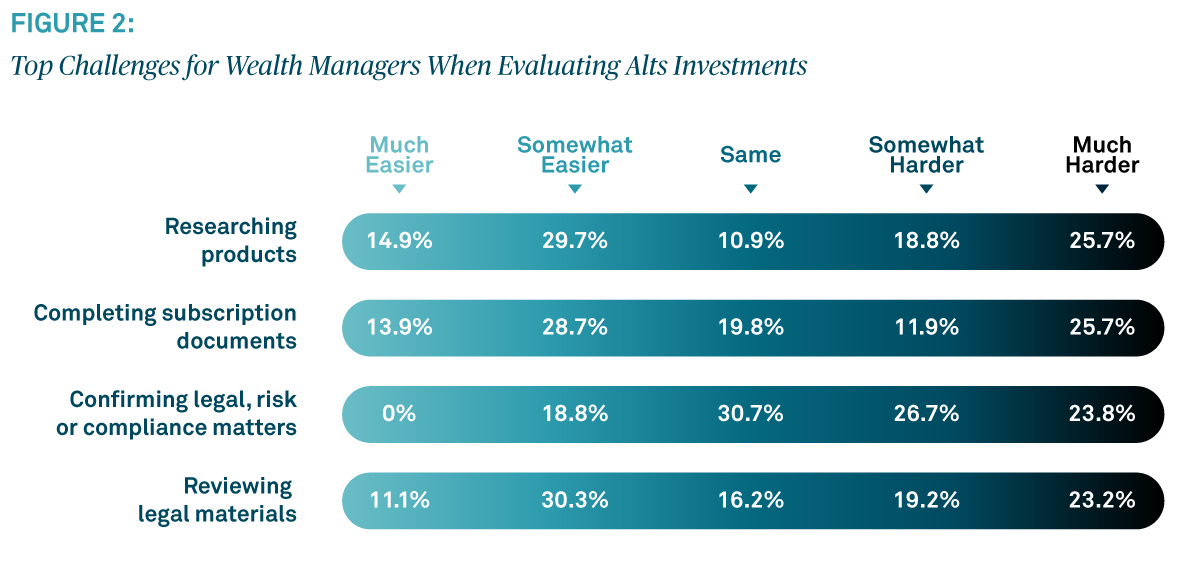

For private wealth clients, simple, transparent alts investment strategies are strongly preferred for two reasons. First, wealth managers and RIAs, many of whom are new to the alts space, are obliged to understand, inside-out, the investment benefits of their strategy so that it can be communicated with clarity to their clients. Wealth managers may have limited bandwidth for the detailed, time-intensive work of research and manager selection. Almost half (44%) of the BNY Pershing survey respondents agreed it is harder to research alts products than traditional investments. Indeed, advisors with significant demands on their time want straightforward, actionable strategies. When investment approaches are communicated clearly, wealth managers have more potential to inspire clients to act.

Additionally, tax efficiency and liquidity are attractive to private wealth clients — compared to institutional investors — as they operate on shorter time horizons and are not tax-exempt. BNY Pershing’s survey found that more than half of wealth managers cited tax efficiency and liquidity as key concerns when selecting alts investments.

Source: BNY Pershing survey: “Wealth Trends in Alternatives: Optimizing Opportunities,” Feb. 10, 2025

A high demand strategy appealing to private wealth managers is long-short equity strategies that seek to provide tax efficient returns in individual separately managed accounts (SMAs).

Key differentiators of long-short equity strategies:

Delivering this strategy to private wealth clients efficiently requires institutional-grade infrastructure. Running dozens or hundreds of personalized accounts is operationally more complex than administering a combined fund. Wealth managers need integrated trading, compliance and reporting systems to manage client-specific mandates effectively.

Evergreen funds are another type of alt strategy that can also meet private wealth clients’ preferences for simplicity, liquidity, tax efficiency and transparency.

Evergreen funds, open-ended private market vehicles designed to hold assets indefinitely rather than for a fixed life like traditional closed-end funds, allow investors to subscribe and redeem on a periodic schedule, subject to some limits. Despite their limited tax efficiency, evergreen funds have become exceedingly popular and are today the most widely adopted alts product by wealth managers (47%) thanks to their inherent simplicity.4

Closed-end interval and tender funds are not far behind in popularity. While smaller than evergreen funds, 14% of wealth managers surveyed said they leverage these funds to access alts, further demonstrating the importance of tailoring products for the unique expectations of the private wealth segment.

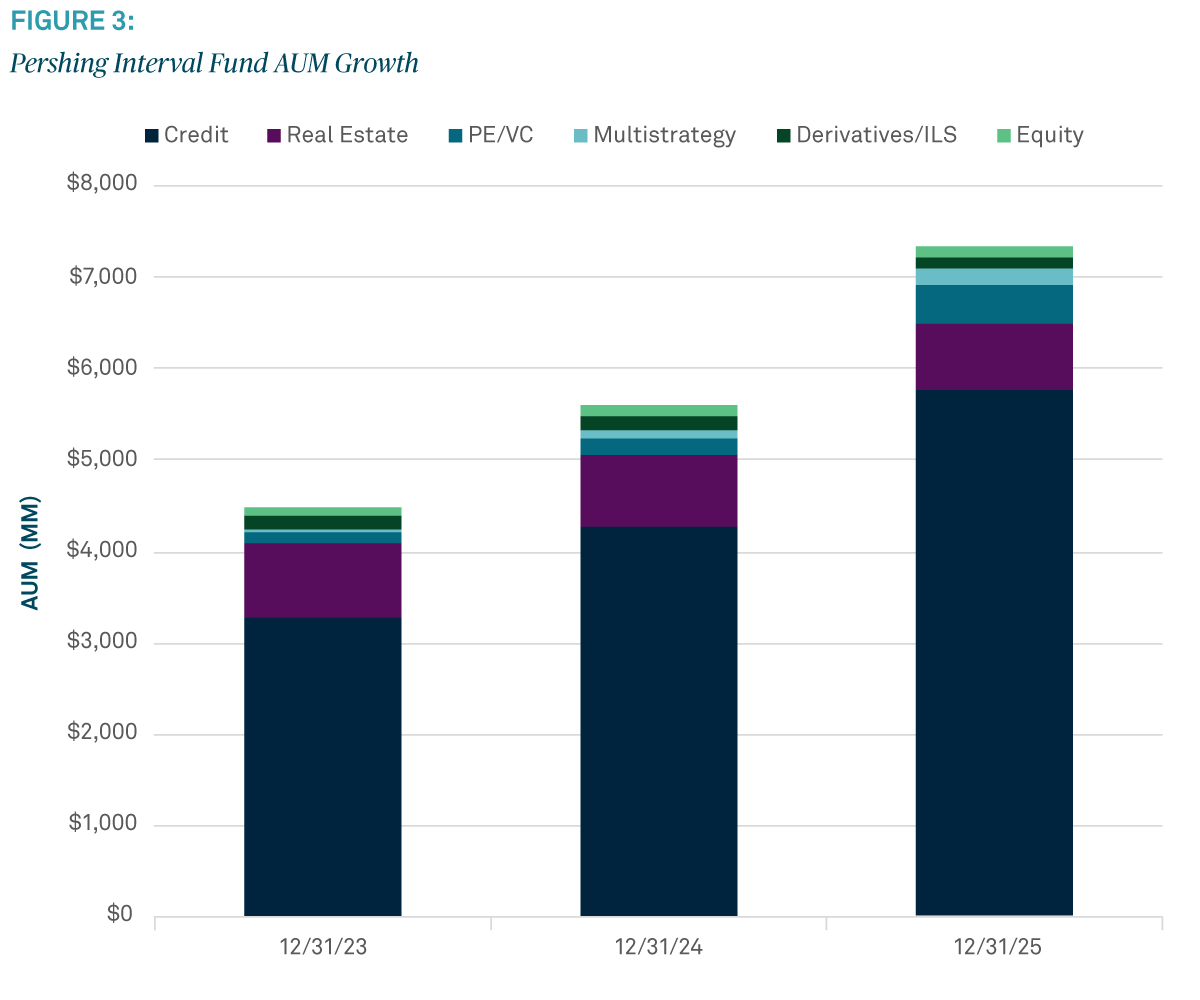

This momentum aligns with industry-wide interval fund growth, with AUM reaching $125 billion as of 4Q 20255 and Pershing interval fund AUM reaching $7.9 billion in 3Q 2025, driven primarily by +$1.3 billion in credit strategies (Figure 3) — highlighting private credit’s role in expanding interval fund adoption and the appeal of structured, periodic liquidity in wealth channels.

Source: BNY Growth Dynamics Trend Data as of December 31, 2025

Other emerging trends for new alts strategies that could present opportunity for alts managers include:

As the private wealth sector becomes the new growth engine for alts, solving the associated resourcing, operational, infrastructure and scaling challenges could prove increasingly imperative for alternative asset managers. The arena of alternatives is colorful and ever-changing; alongside rising awareness of the benefits for a broader investor base and their wealth managers, there is ample room for further creativity and dynamic deployment of new investment structures and strategies.

Sources

1Elisa Battaglia Trovato, “Alternative assets becoming key battleground for wealth managers,” Professional Wealth Management, FT Wealth Management, February 26, 2024, https://www.pwmnet.com/alternative-assets-becoming-key-battleground-for-wealth-managers

2 Hugh MacArthur, Rebecca Burack, Graham Rose, Christophe De Vusser, Kiki Yang, and Sebastien Lamy, “Global Private Equity Report 2024,” Bain; Bain & Company, Inc., https://www.bain.com/globalassets/noindex/2024/bain_report_global-private-equity-report-2024.pdf

3 Capgemini Research Institute for Financial Services Analysis, “World Wealth Report 2025,” Capgemini, Capgemini, 2025, https://www.capgemini.com/insights/research-library/world-wealth-report/.

4BNY Pershing, “Wealth Trends in Alternatives: Optimizing Opportunities,” February 10, 2025. https://www.bny.com/corporate/global/en/insights/wealth-trends-in-alternatives-optimizing-opportunities.html

5BNY calculation using IntervalFundTracker.com data, https://intervalfundtracker.com/data/active-interval-funds/

Disclaimer

BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally. This material and any products and services mentioned may be issued or provided in various countries by duly authorized and regulated subsidiaries, affiliates, and joint ventures of BNY. This material does not constitute a recommendation by BNY of any kind. The information herein is not intended to provide tax, legal, investment, accounting, financial or other professional advice on any matter, and should not be used or relied upon as such. The views expressed within this material are those of the contributors and not necessarily those of BNY. BNY has not independently verified the information contained in this material and makes no representation as to the accuracy, completeness, timeliness, merchantability or fitness for a specific purpose of the information provided in this material. BNY assumes no direct or consequential liability for any errors in or reliance upon this material.

This material may not be reproduced or disseminated in any form without the express prior written permission of BNY. BNY will not be responsible for updating any information contained within this material and opinions and information contained herein are subject to change without notice. Trademarks, service marks, logos and other intellectual property marks belong to their respective owners.

© 2026 BNY. All rights reserved. Member FDIC.

About BNY Pershing

BNY Pershing (member FINRA, NYSE, SIPC) is a leading provider of clearing and custody, trading and settlement, advisory and investment solutions, data insights, business consulting and other services to wealth management and institutional firms looking to grow their businesses. For more information, go to www.bny.com/pershing.

©2026 Pershing LLC. All rights reserved.