Market lions and lambs

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 8 minutes

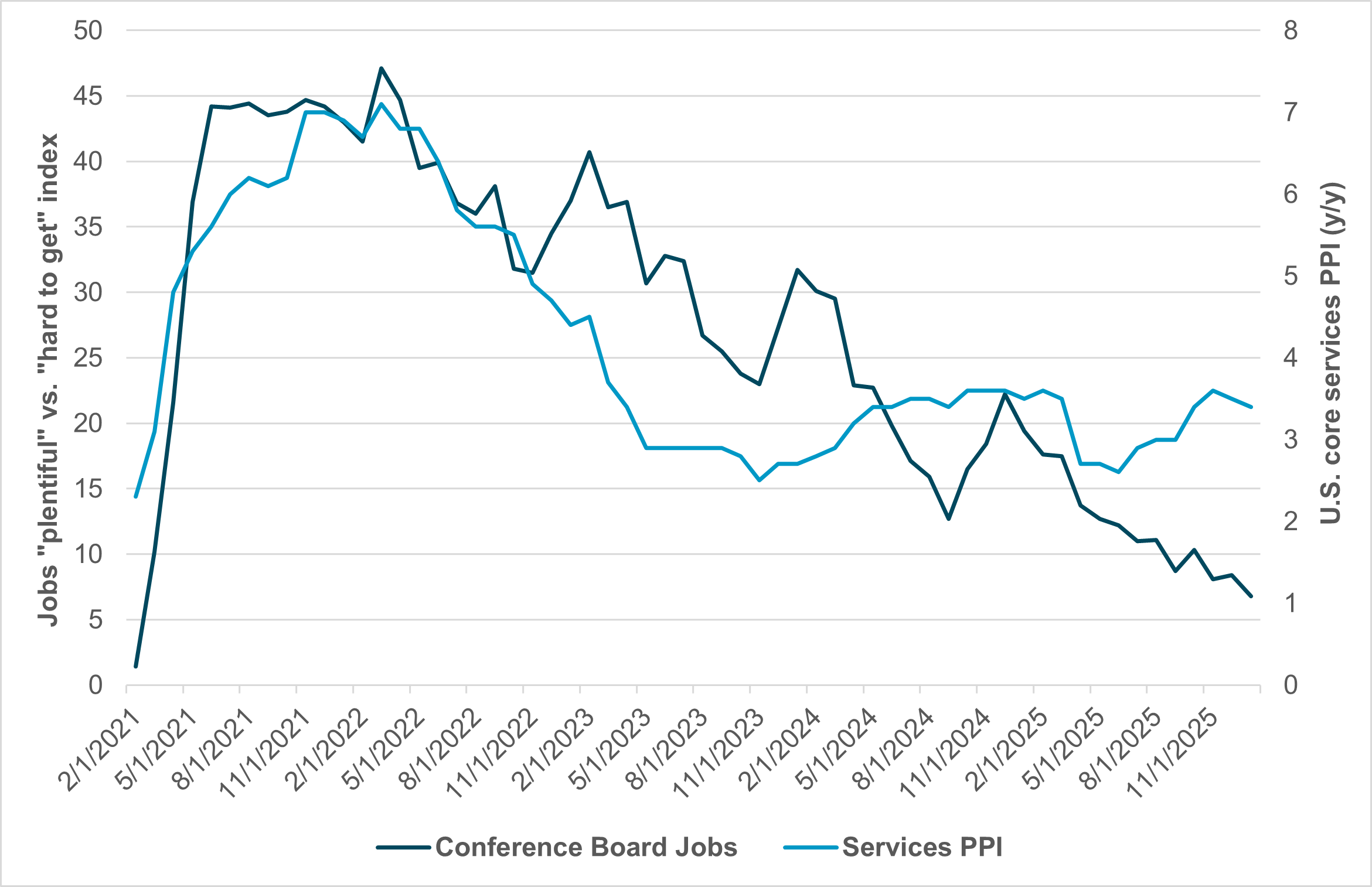

EXHIBIT #1: U.S. CORE SERVICES PPI VS. JOBS “PLENTIFUL” – “HARD TO GET” INDEX

Source: BNY, Bloomberg, The Conference Board

March has come in like a lion. The U.S. and Israel actions in Iran are changing markets globally. Oil is the short-term risk barometer, with gold and bonds the safe havens. Volatility is the watchword after February delivered a down month for U.S. equities, mixed results for the USD and lower bond yields, despite still-elevated inflation and firmer growth. AI-driven rotation trades, global diversification and emerging markets (EM) were dominant themes. There has also been a notable shift in how markets react to news and risk since COVID. We live in a new era of analysis, where AI delivers instant reports, governments spend money without clear limits and economic conflicts are no longer settled by market forces.

We come full circle back to political economics. Elections this month should be front and center for investors. These begin with the Texas, North Carolina and Arkansas primaries on March 3; the Colombia national parliamentary election on March 8; French local elections on March 15 and 22 (first and second rounds, respectively); and Denmark’s parliamentary election on March 24. U.S. primaries and national elections are already shaping how policy may unfold in the month ahead. That matters for Q1 rebalancing, particularly with Colombia and EU holdings of equities and bonds sitting multiple standard deviations above normal.

The ides of March also deliver key central bank decisions, including the Bank of Japan and FOMC meetings. Add pressure on U.S. budgets, uncertainty around tariff revenues, the partial government shutdown, the role of tax returns in driving consumer confidence and renewed talk of another budget reconciliation bill aimed at running the economy hotter.

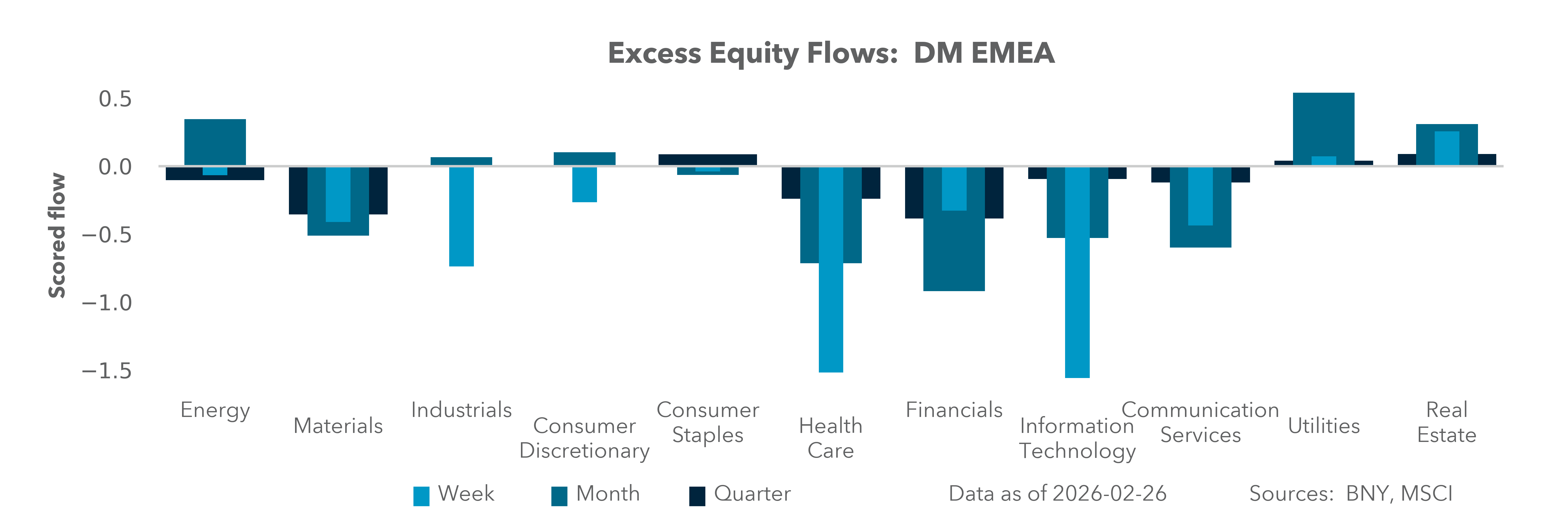

The week ahead delivers the usual start-of-month economic focus, with global PMI reports, U.S. ISM and U.S. jobs data critical to the global recovery narrative. Expectations that U.S. rates remain stable rather than ease next quarter are key for FX markets and hedging decisions. How AI affects productivity and job losses has become part of the scare trade across service industries. Investors will also watch ongoing private credit wobbles as fears of contagion persist following last week’s Market Financial Solutions collapse in the U.K. All of those worries pale in comparison to the U.S. military buildup and ongoing talks about nuclear ambitions and ballistic missiles in Iran. Markets are watching oil and gold as barometers of trouble. That leaves the Materials sector the most held, with ongoing positive flows across global equity markets.

Our take: The worry about AI taking jobs has been ongoing since mid-2025. The latest February surveys from Pew, Mercer and others suggest about 50% of workers believe AI could replace them. All headlines were a key part of last week’s trading, from the dystopian Citrini Research report to the Oaktree newsletter. Investors have rebalanced technology exposures and now see fewer inflation fears and more job worries. This matches the Conference Board’s consumer views on labor markets, but not on services costs, as core services PPI has continued to rise, linked to U.S. tariffs (Exhibit #1). Hope remains that the FOMC will look through inflation as a one-off effect, as does the usual expectation of Fed cuts should equities drop 10% or more. Financial conditions play a key role in shaping market mood, and February delivered a winter of worry rather than a spring of hope.

Forward look: The split between job expectations and services inflation widened with the Trump policy shifts in 2025. The key question for investors now is whether ongoing AI-related job worries will translate into political resentment. The administration’s deregulation and tax agenda will be tested in this week’s primaries in Texas, North Carolina and Arkansas. Expect current politics to reflect frustrations over affordability and the sustainability of labor markets in this new world of AI-driven productivity.

North America: ISM, jobs and Fed speakers in focus

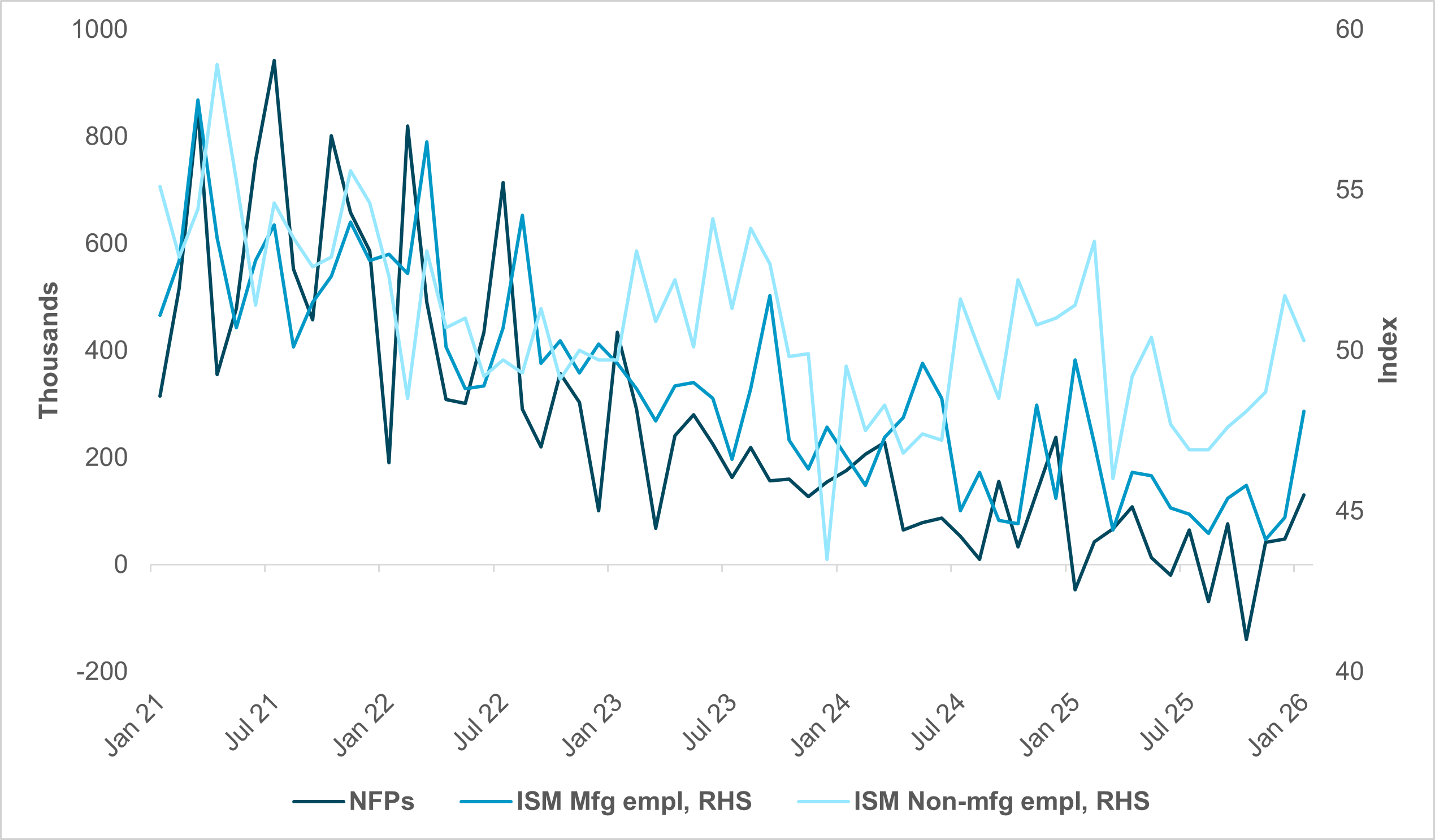

EXHIBIT #2: U.S. ISM EMPLOYMENT AND NFPS

Source: BNY, Bloomberg

Our take: The first week of the month is often busy on the data front, and March is no exception. It’s jobs week, with nonfarm payroll (NFPs) data released Friday, but before that we’ll see several other important releases. ISM manufacturing and services PMIs come out on Monday and Wednesday. Regional PMIs last week suggest that services could wane, while manufacturing indicators have been more equivocal.

With the jobs report Friday, we’ll also get the usual precursors, including ADP on Wednesday and Challenger job cuts data on Thursday. Several large firms have recently announced layoffs, and we will be watching to see whether these cuts begin to show up in the data. We remain concerned about the lack of breadth in job creation, as well as its generally moribund pace. Last month produced a strong headline number for NFPs at 130k, but almost all job creation was in the noncyclical health care sector.

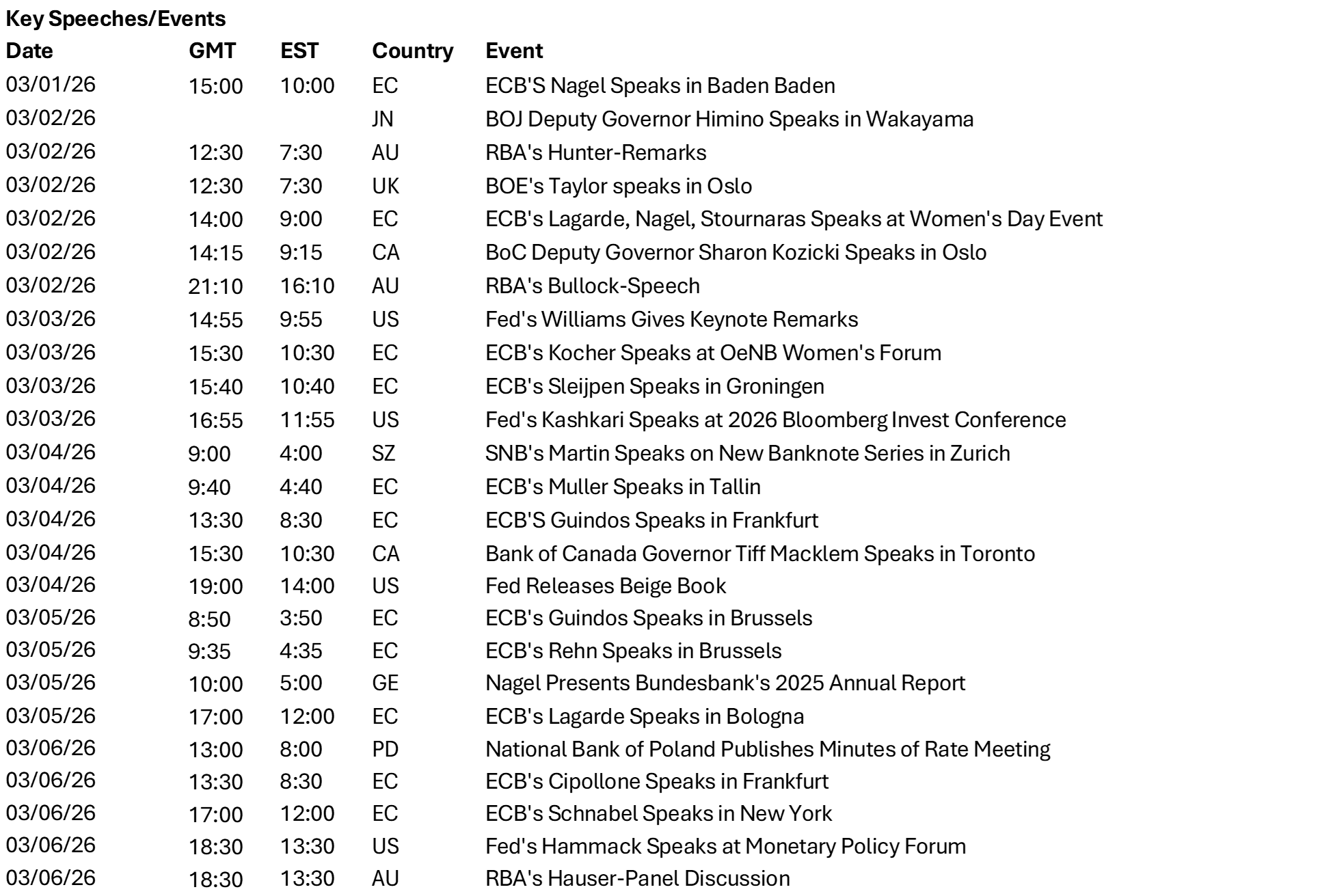

Forward look: Fed speakers scheduled before the communications blackout Friday include three FOMC voting members: New York Fed President John Williams, Minneapolis Fed President Neel Kashkari and Dallas Fed President Lorie Logan. Speakers have been on the hawkish side lately, and last week’s PPI indicated inflation is still warm.

The March Beige Book is also released Wednesday. Last cycle’s report was downbeat, and we’ll be keen to absorb qualitative data from the release. Overall, the focus on jobs as a key factor in sustaining FOMC rate-cut expectations continues to drive market volatility and cross-asset value shifts.

EMEA: Convergence in growth, divergence in policy

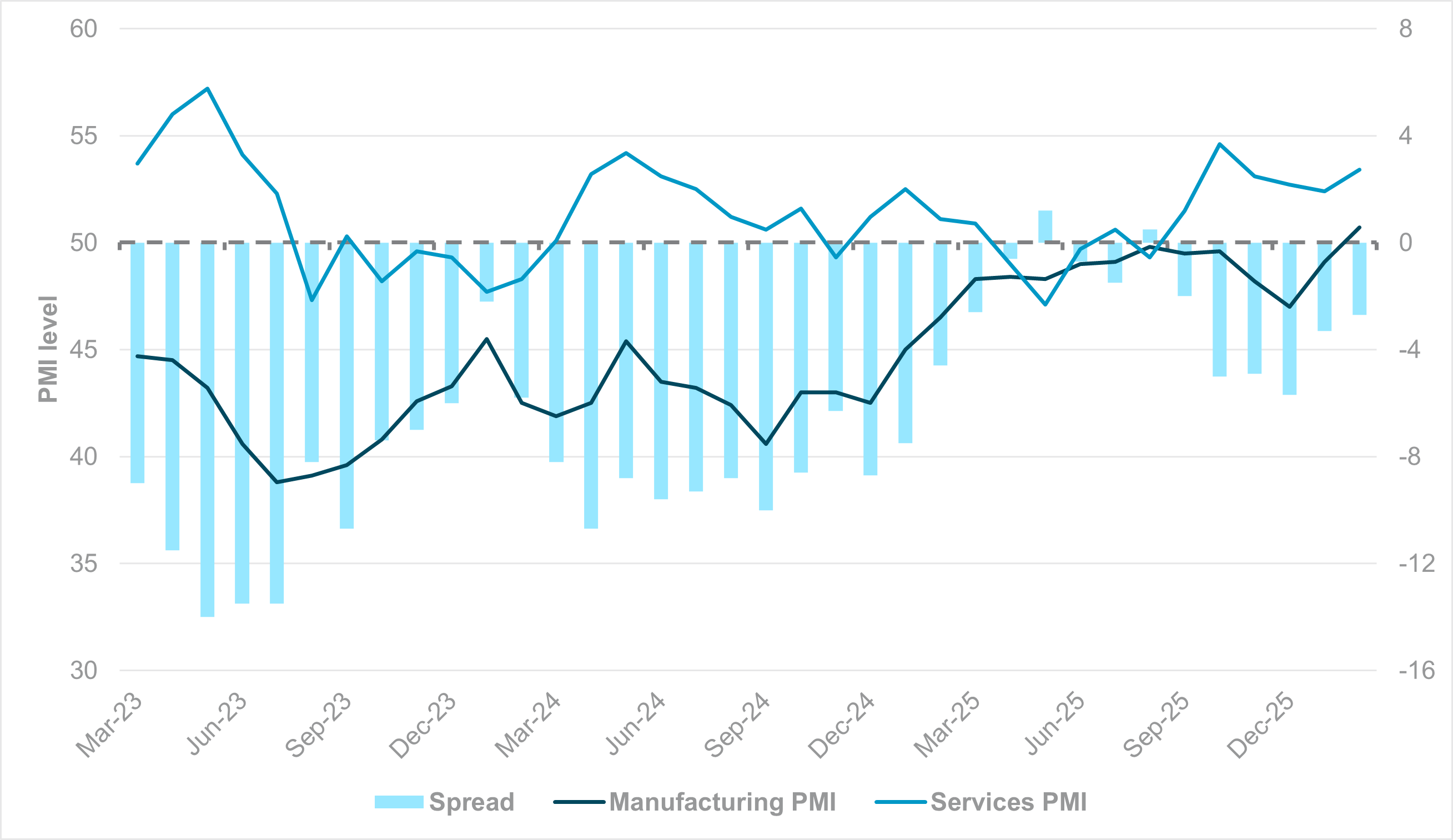

EXHIBIT #3: GERMANY MANUFACTURING AND SERVICES PMIS

Source: BNY

Our take: Depending on the scale of the oil price impact in the coming days and weeks, we expect a strong pivot by central banks in EMEA towards inflation vigilance. The closure of the Strait of Hormuz is material for European liquefied natural gas imports as the continent has pivoted supply sources to Qatar over the last few years away from Russia. As we highlighted in prior publications, the ECB is highly sensitive to upside energy price shocks. In their December projections, the 75th percentile for energy prices in the Eurozone means a 14.2% rise in oil prices, 20% gain in gas prices, equivalent to 15.2% gain in synthetic energy price indices from baseline. Even at the 75th percentile, inflation is expected to remain clearly above target over the forecast horizon. Combined with some early signs of cyclical recovery and strong fiscal impulse, the ECB’s February communication on downside price risks emerging should be discounted for now.

Domestically, final PMIs are due across Europe in the week ahead, in addition to the remaining preliminary February CPI releases for Eurozone economies. The wider risk environment remains unstable, but activity levels look set to confirm that growth momentum is finally gaining ground in Europe.

After near-crisis readings throughout 2025, February’s flash German PMI hit a four-month high. The headline manufacturing index returned to expansion for the first time in three and a half years. Even exports were growing, and Chancellor Friedrich Merz’s recent visit to China is expected to have secured a marginal improvement in the current Sino-European trade détente. Domestically, orders are flowing as fiscal impulse picks up, but it remains to be seen whether multiplier effects will be strong enough at the European level.

Crucially, growth is becoming far more balanced. Services continues to perform well. We have long been concerned about the gap between German manufacturing and services PMI, with inflation increasingly attributed to the latter – an area where ECB policy has limited impact in either direction. For the first time in this cycle, there is a sign that convergence is taking place in expansion territory (Exhibit #3).

Manufacturing productivity remains Europe’s core strength, and this should help lift overall productivity in support of growth. The European Central Bank (ECB) will welcome such developments and likely remain on autopilot. Conditions are not yet in place to move decisively in either direction, particularly given the asymmetric policy response to price shocks. Any escalation in the Middle East could derail progress, although Europe would likely remain a bystander.

Forward look: With core European inflation prints largely complete, the ECB will begin laying the groundwork for its next policy assessment. However, ongoing divergence in price growth across the Eurozone remains a major challenge.

French inflation is currently running at almost half of the level of Germany’s, underscoring the difficulty of having uniform monetary policy for economies with very different fundamentals. If French output fails to match a German recovery – partly due to limited domestic resources to drive public sector demand – calls for monetary policy to ease financial conditions and create fiscal space will grow.

This is particularly relevant as discussions over the timing of ECB President Christine Lagarde’s exit move up the agenda. The political dimension behind her potential early departure is clear. Questions have even been raised about early exits for other key Commission officials to ensure a new leadership team is in place well before the next French election. In the ECB’s case, given the direction of the French economy, a “lowest common denominator” approach appears to be emerging. That would limit policy differentials and could undermine the currency, even if the growth-support rationale is clear.

Meanwhile, politics will also likely remain at the top of the agenda in the U.K. in the wake of the Gorton and Denton by-election victory for the Green Party. We don’t see any major changes before the local elections in May, but a pivot toward more expansionary fiscal policy by the ruling Labour Party is widely anticipated as Prime Minister Keir Starmer seeks to reverse political fortunes.

Some fiscal space has emerged, surprisingly, while the Bank of England is viewing productivity more positively, potentially supporting additional headroom in government assumptions. We continue to see a risk of more cuts than currently priced in the U.K., and the resilience of real yields suggests any plans will be measured, even if the direction of travel is clear.

The National Bank of Poland is expected to cut rates by 25bp to 3.75%, and current positioning levels in the PLN mean the risk of additional hedging flows could increase. Valuations based on real rates and policy differentials versus the ECB are less extreme than in the HUF.

However, EMEA is losing ground to LatAm in carry trades, and conviction in hedging flows is increasing. We expect the RON to be the first pure carry currency in either region to move toward underheld territory.

APAC: Data momentum and policy catalysts

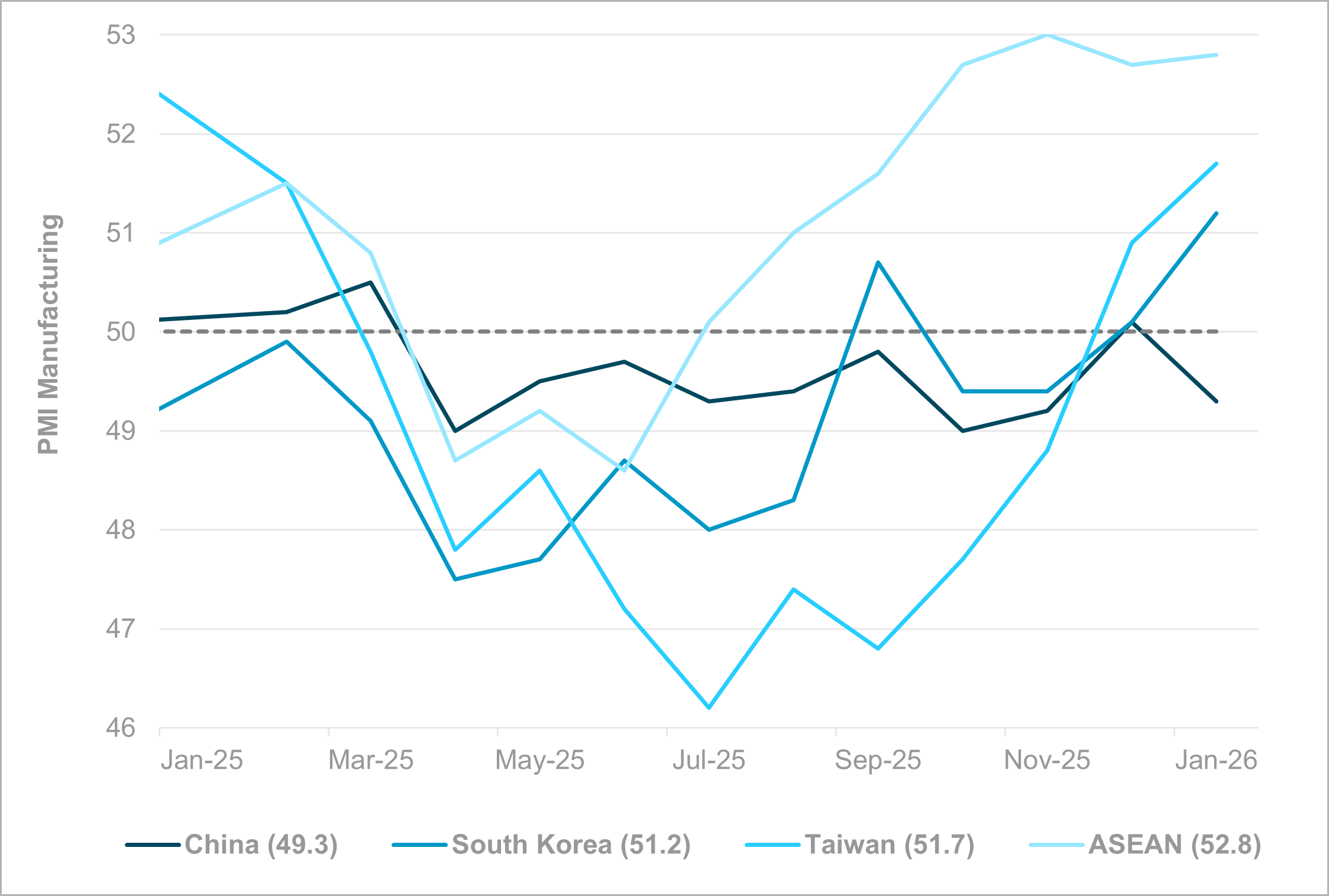

EXHIBIT #4: REGIONAL APAC PMIS

Source: BNY

Our take: The high exposures of Japan and Korea to imported oil from the Middle East will be highly destabilizing to balance of payments in the near-term. Already facing high inflation and inflation expectations, an energy-supply shock represents serious challenges to the Bank of Japan and could also derail Prime Minister Takaichi’s upcoming spending plans, which were already required a strong fiscal offset. During energy shocks, APAC FX rarely serves as save havens as balance of payments deteriorate.

It is too early to expect a repeat of the severe weakness in 2022-2023 in regional currencies, but considering current developments we will be far more cautious in our general view that APAC FX can continue to strengthen. We expect all relevant bodies in the region will step up volatility managing in the meantime. The market will also be highly focused on China’s response to weekend events as Presidents Xi and Trump are still scheduled to meet in Beijing at the end of March.

Otherwise, APAC data will drive near-term risk and rates pricing. China’s February PMIs are key. Stabilization would support cyclical positioning in Asian equities and FX, while renewed contraction would pressure higher-beta and commodity-linked currencies. South Korea and Taiwan PMIs will test export momentum and tech demand, while CPI prints in both economies are critical for front-end rate expectations and KRW and TWD carry dynamics. In Japan, capex, profits and labor data will shape JGB steepening risk and JPY positioning as markets assess further normalization.

In ASEAN and Australia, focus shifts toward growth and inflation impulses. Australia’s Q4 GDP and CPI feed directly into Reserve Bank of Australia pricing and AUD volatility. Indonesia’s and India’s external balances will guide EM FX risk appetite, while Singapore PMI and retail sales are relevant for central bank expectations and SGD bias.

Forward look: Flows remain broadly supportive. Equity allocation continues to rotate from developed markets into EM APAC tech, particularly hardware, underpinning strength in the KOSPI and TAIEX. Watch the South Korea-to-Taiwan rotation – so far, KRW resilience suggests orderly rebalancing rather than capital flight.

China’s NPC should reinforce pro-growth fiscal and monetary guidance, anchoring sentiment. Upcoming central bank meetings (Malaysia, Japan, Australia, Indonesia and Taiwan) create event risk across rates and FX. We remain tactically constructive on KRW and TWD. The People’s Bank of China’s removal of the CNH forward reserve requirement should be viewed as a volatility-management tool rather than a trend shift, with underlying flow dynamics still USD-negative across Asia.

The week ahead is data- and policy-heavy, with volatility likely to remain elevated across rates, FX and equities. U.S. ISM surveys and NFPs will be pivotal in shaping Fed expectations, particularly as markets debate stable versus restrictive policy into Q2. Breadth in job creation and services inflation dynamics remains key for duration positioning and equity sector rotation.

In Europe, improving PMIs support a cyclical rebound narrative, but political risk and ECB leadership uncertainty limit conviction in EUR upside.

In EM, rate decisions in Poland and Malaysia highlight ongoing carry differentiation, with EMEA increasingly vulnerable relative to LatAm. In APAC, China PMIs and capital flow trends will determine whether tech-led inflows remain durable.

Geopolitics – particularly Iran – and private credit stress remain tail risks. Into month-beginning flows, positioning discipline is critical as cross-asset correlations remain unstable and political economics increasingly override traditional macro signals.

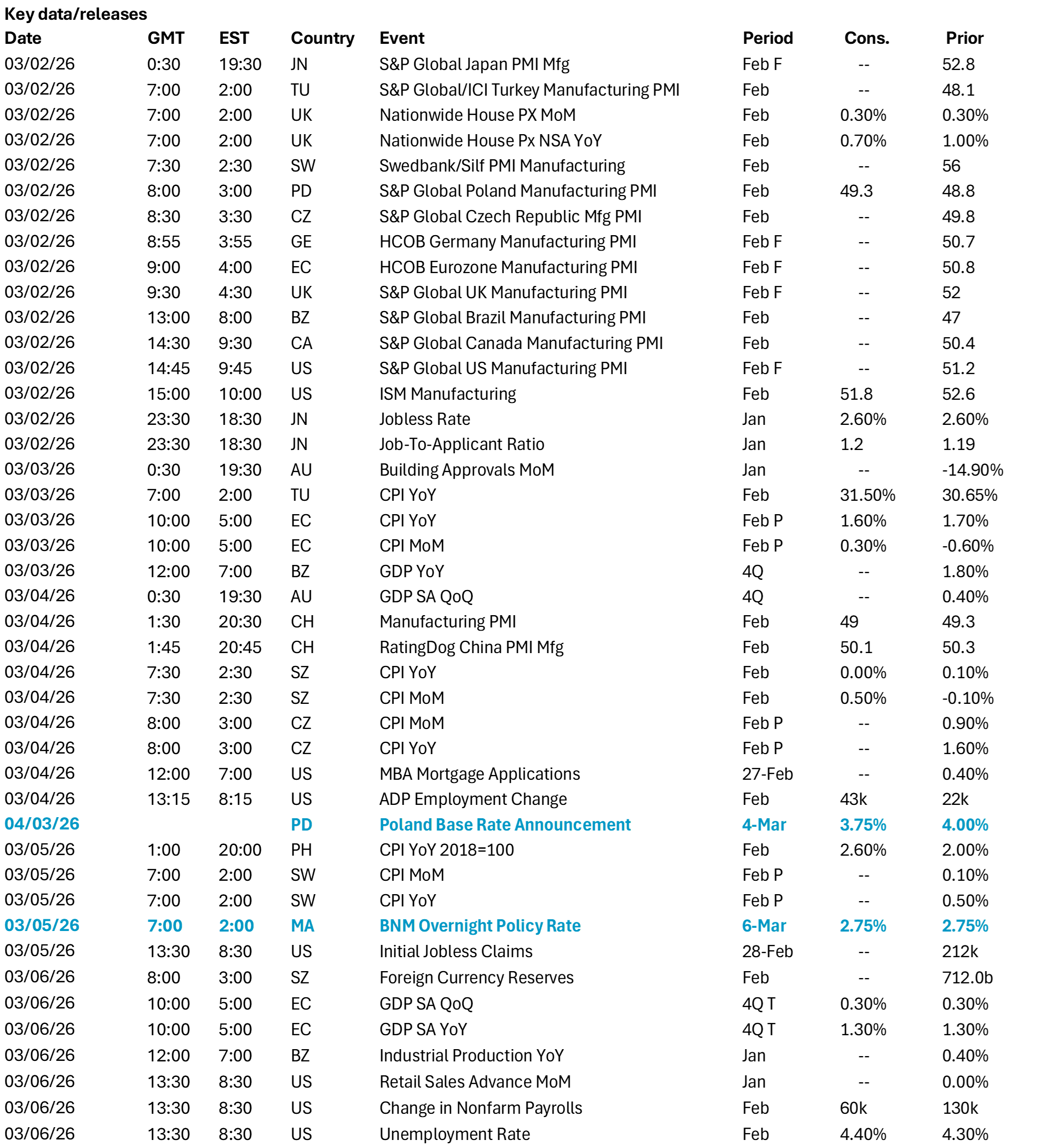

Central bank decisions

Central Bank Decisions

Poland, Narodowy Bank Polski (Wednesday, March 4): The NBP is expected to cut rates by 25bp to 3.75%. Despite inflation surprising to the upside in January and ongoing fiscal pressures, the broader economic outlook is soft, and softening wage growth will have a material bearing on the policy outlook. The labor market is also weakening, and we believe the NBP sees this reflected in domestic demand. Real rates are currently holding at around 150bp, but EURPLN appears to have based for now. Vigilance around FX pass-through remains warranted.

Malaysia, Bank Negara Malaysia (Thursday, March 5): We expect BNM to keep its policy rate unchanged at 2.75% at the March meeting and throughout the year, maintaining an upbeat assessment supported by solid GDP growth and stable inflation. BNM projects 2026 GDP growth of around 4.0% to 4.5%, with inflation expected to remain “moderate” after headline and core averaged at 1.4% and 2.0%, respectively, in 2025.

Source: BNY

Source: BNY

*Day before