Balance sheet plans and yield decomposition

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 5 minutes

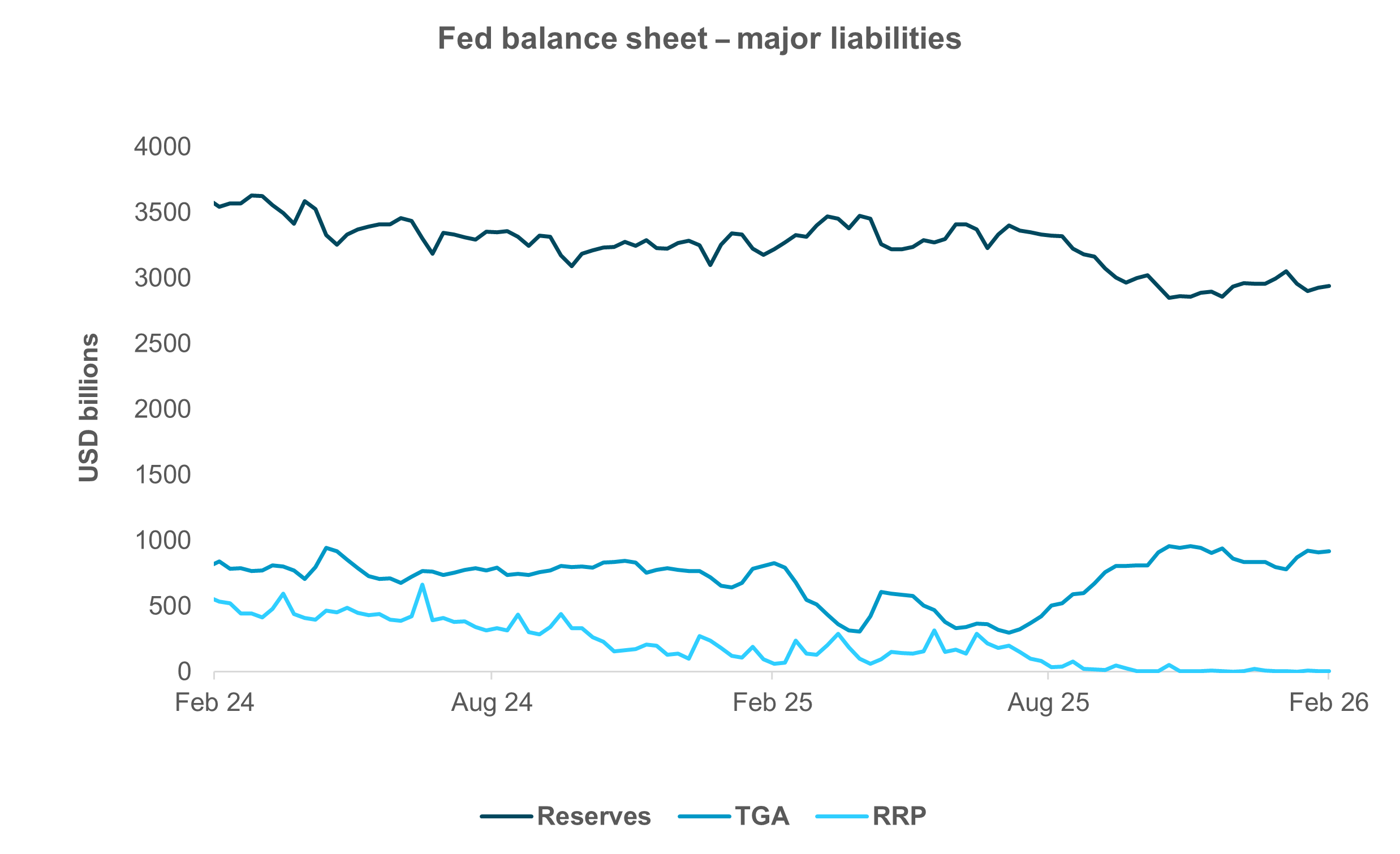

EXHIBIT #1: HIGHER TGA KEEPS RESERVES STEADY

Source: BNY Markets, Federal Reserve Board of Governors

Reserve management purchases (RMPs) by the New York Fed are about to turn three months old. Between the middle of December and the middle of March, the Fed will have purchased over $160bn in T-bills through RMPs and reinvestments of asset-backed security (ABS) proceeds. These purchases have helped stabilize funding markets and kept reserves from falling critically low.

In a recent speech, Julie Remache, Deputy Manager of the System Open Market Account (SOMA), which manages the NY Fed’s securities portfolio, discussed the future of the balance sheet. She indicated that RMPs will likely continue at “elevated levels” through April. Tax payments that month often drain reserves and swell the Treasury General Account (TGA). In its recent funding statement, Treasury indicated that the TGA could exceed $1tn in the next several months. As Exhibit #1 shows, the TGA is now over $900bn, above the targeted $850bn. Increases in the TGA, all things being equal, lead to drawdowns in reserves, potentially creating money market stress.

After April, Remache anticipates “the amount of purchases to be reduced substantially.” We don’t have a precise estimate of what that smaller sum will look like. For now, we simply assume that the monthly $40bn pace through mid-April will slow to half that amount. This means that between RMPs and reinvestments of ABS into bills, the Fed could be purchasing around, or even more than, $400bn in T-bills.

Interestingly, this increase in the SOMA portfolio is occurring at the same time Fed Chair nominee Kevin Warsh has been arguing in favor of balance sheet reduction, as we discussed last week. We don’t know when Warsh’s confirmation would occur, since Republican (and soon to retire) Senator Thom Tillis maintains that he will not allow any Fed nominations to proceed through the Senate Banking Committee until the Department of Justice’s investigation into the Fed is concluded or dropped altogether.

Nevertheless, when Warsh eventually assumes his position as chair, he will have to swing the FOMC toward balance sheet reduction, a full turnaround from what the committee currently supports. Warsh describes the balance sheet as “bloated,” arguing that the Fed’s financial market “footprint” is larger than desired. However, we have argued that a smaller balance sheet requires more frequent use of open market operations to contain repo volatility.

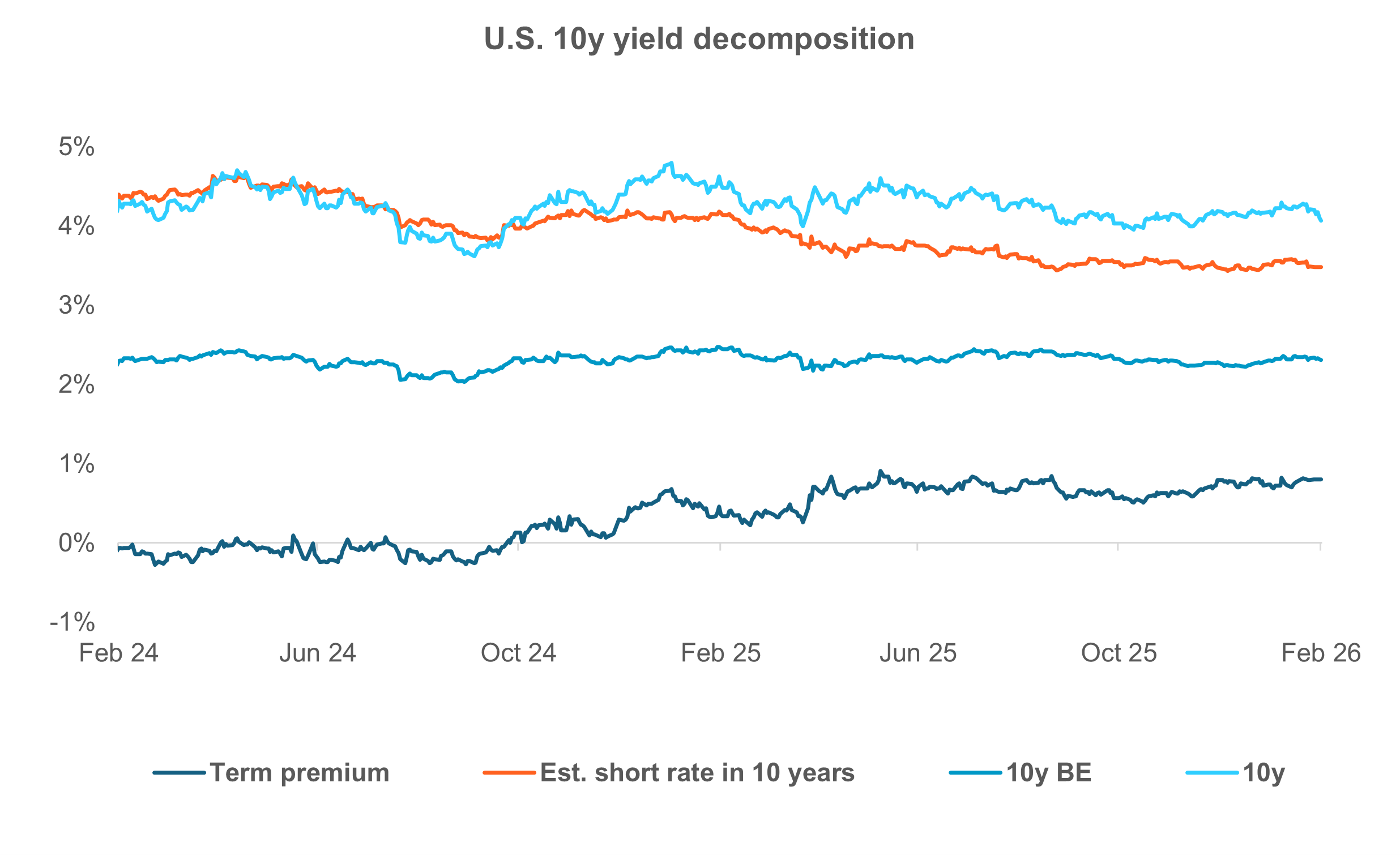

EXHIBIT #2: LOWER EXPECTED SHORT RATES, STEADY TERM PREMIUM

Source: BNY Markets, Bloomberg, Federal Reserve Bank of New York

After reaching 4.8% in mid-January 2025, the U.S. 10y yield has been relatively range-bound, especially since September 2025, fluctuating between about 4.0% and 4.3%. It recently flirted with the high end of that range but has come down to about 4.1% at the time of this writing. It’s not clear to us whether the yield’s recent retreat reflects Warsh’s nomination, given his dovish stance, or something in the macroeconomy weighing on its level. It’s probably a combination of both.

In Exhibit #2, we show different components of the 10y yield. The term premium measures the extra compensation a bondholder requires to lend. Term premium includes solvency and liquidity risk, forecast uncertainty, and inflation expectations. This variable has risen in recent years. It was negative as recently as mid-2024 and hovers between 70 and 80bp today, indicating elevated risk perceptions. However, during the 10y’s retreat from a recent high of 4.29% in late January to about 4.1% now, this premium didn’t really decline. Risk is still present in lending long to the U.S. government.

The bond’s breakeven (BE) inflation expectations are derived from the inflation-linked bond series. This should reflect how much inflation compensation is required to offset the real erosion of principal over 10 years. It has barely budged over the past few years. Inflation expectations are indeed well anchored and are not responsible for fluctuations in the nominal 10y yield.

Finally, we show the estimated short rate in 10 years’ time, derived from the New York Fed’s term premium model, which also provides the 10y term premium. It’s hard to see much of a change in this series, represented in orange. However, a closer look reveals that this measure is slowly falling. The decline has generally been offset by the term premium, keeping the net effect on overall yields to a minimum. The recent tick lower in yields has been accompanied by a similar drop in this estimated short rate.

Something – whether the Warsh nomination or recent weakness in labor data – is causing investors to anticipate lower equilibrium rates over the long term. However, we wonder if these measures (term premium, breakeven inflation and the estimated short rate), won’t start to pick up in the short- to medium-term. We expect equilibrium inflation expectations to rise eventually, especially if the Fed focuses on the labor market (which we expect to weaken further, despite last week’s encouraging data) at the expense of still-sticky inflation. We expect fiscal concerns to increase, driving the term premium higher and, in turn, pushing estimated short rates up.

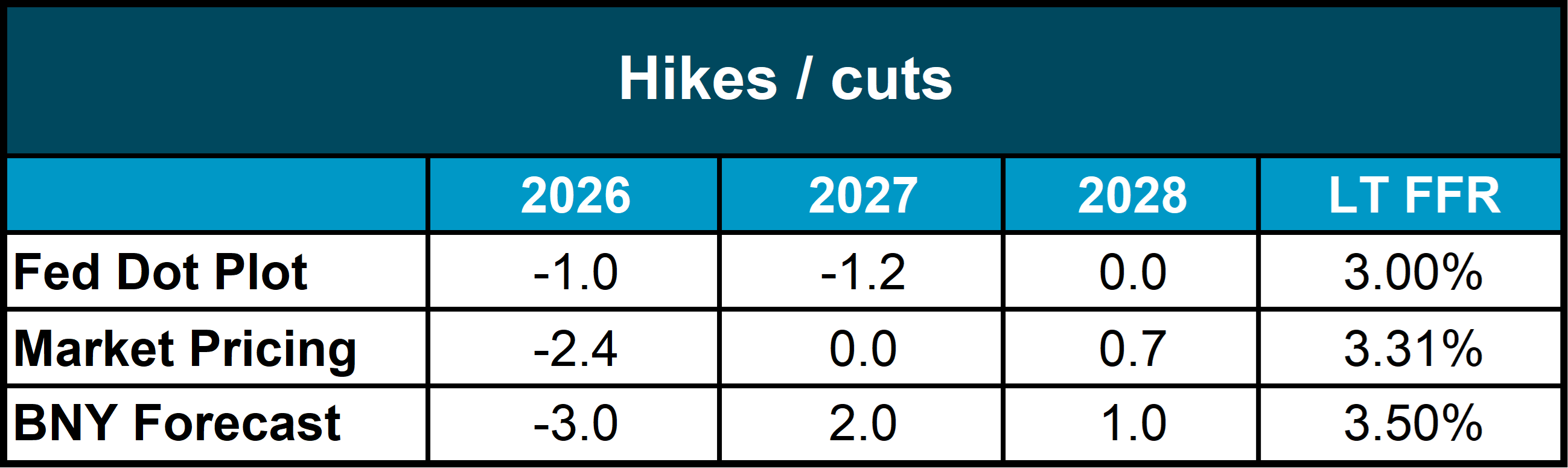

It was a rough week for our Fed view, but we decided to stick with calling for three cuts to the funds rate by year end, almost a full cut more than currently priced in. We can’t credibly claim that the labor data from last week was poor, but they weren’t as strong as they seemed on the surface. Almost all the job creation reported by the establishment survey was in one sector – Health Care. This acyclical sector has been responsible for almost all the job creation since 2024. The narrow employment base is worrying. Furthermore, a number of other labor-related data prints show increasing concern.

Inflation, which came out at the end of last week, looks much better than it did just a few months ago, although it remains above the Fed’s 2% target. Nevertheless, it is encouraging to see it not accelerate this month, suggesting that the committee’s hawks (namely Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan) might be on the back foot if this trend continues.

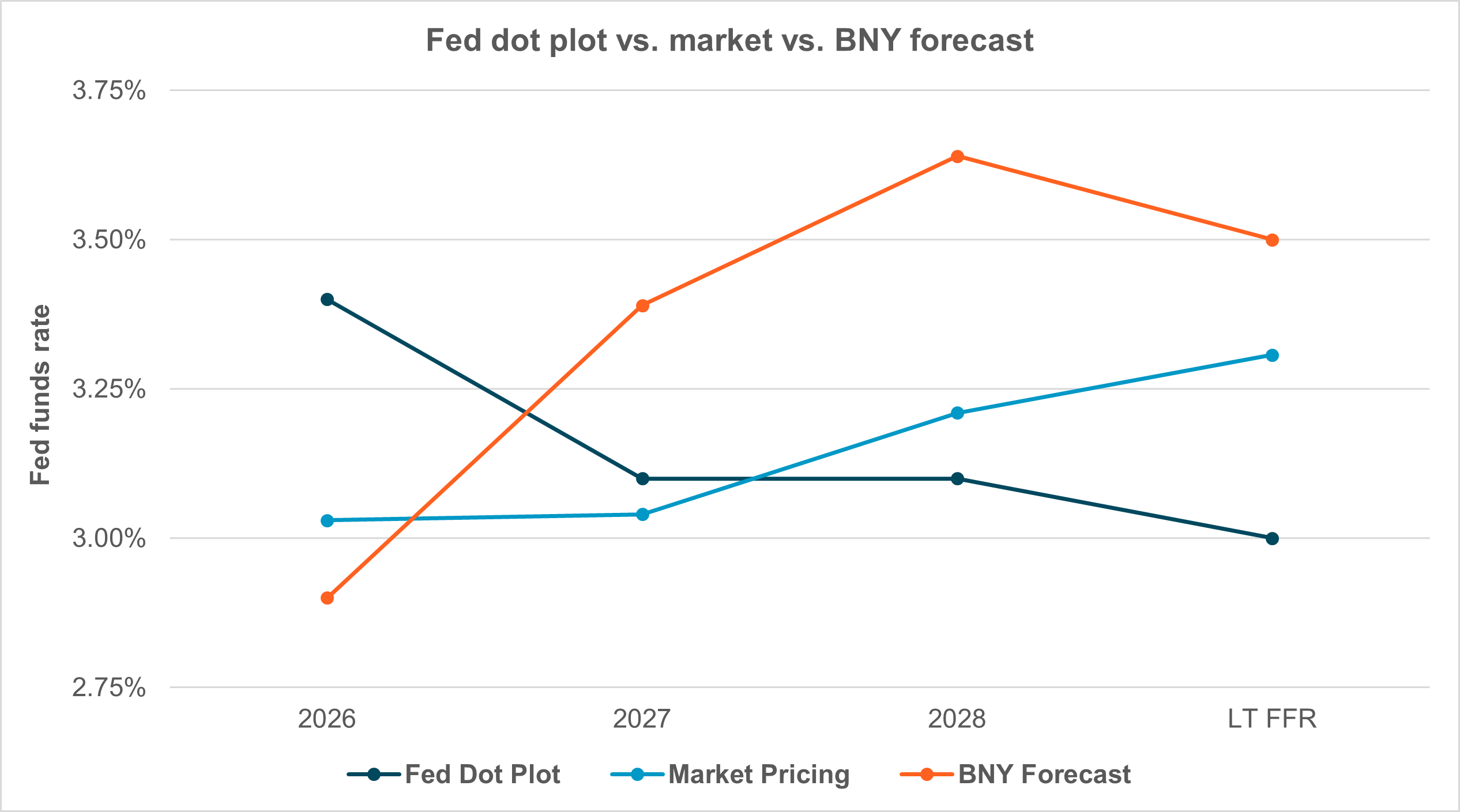

Market pricing still sees a little more than two cuts by year end, with the December OIS contract implying 56bp of easing. We won’t get a read on what the FOMC itself thinks until the March meeting, when another set of dots is published via the Summary of Economic Projections.