Warsh testifies, Burnham takes over

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Geoff Yu

Time to Read: 11 minutes

Bottom line: Disinflation hopes are still carrying sentiment. Growth, earnings and policy risks are harder to ignore. Lower energy prices should soften headline U.S. inflation, but core CPI, producer costs, Fed communication and bank earnings will decide whether policy and cycle risks stay contained.

The global story is shifting from relief to credibility. In the U.S., the test is whether underlying inflation is tame enough for the Fed to stay patient, while financials will offer a cleaner read on credit quality, demand and the real-economy impact of tighter financial conditions after Q2 volatility. The focus in Europe returns to fiscal sustainability and weak demand: the U.K. political transition matters through the chancellor choice and gilt confidence, while the ECB faces evidence that inflation risk is fading faster than growth risk.

Asia ex-chips is the main growth check. China’s data need to show that exports and policy support are offsetting property weakness and soft domestic demand. Without that, pressure builds on regional exports, electronics and stimulus expectations. APAC FX divergence should persist, driven more by capital flows than the dollar.

Across EM, high real-rate and low-volatility support remain strongest in Latin America, but weaker commodity backing leaves returns more exposed to Fed repricing, softer demand and policy execution risk.

Call to action: Focus on carry, credibility and diversification. Rotation should favor economies where policy is actively supporting the growth case, especially China and the U.K., as elevated USD positioning and valuations strengthen the case for diversification.

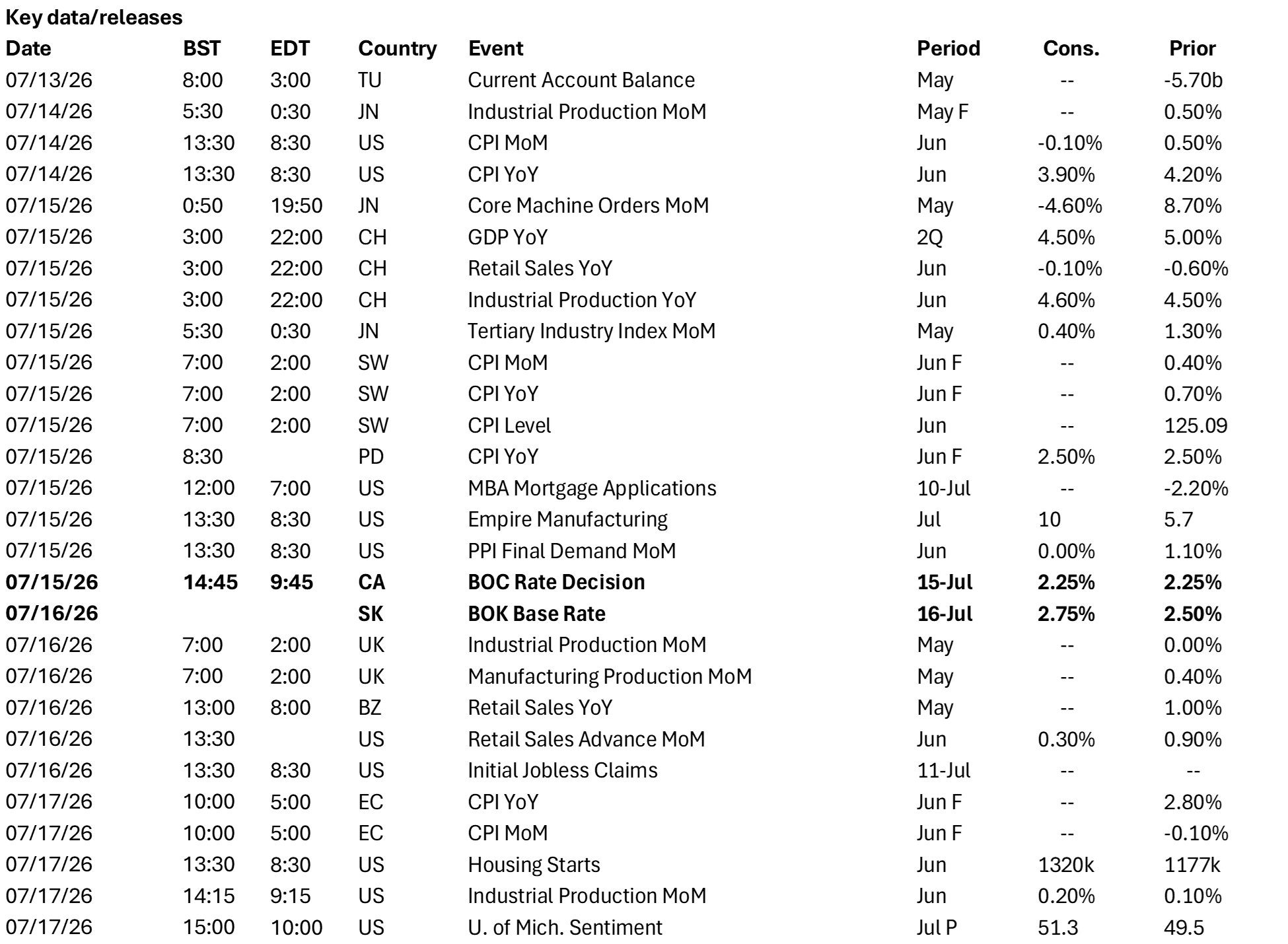

In focus this week

U.S. CPI. This is a key signpost for U.S. inflation, especially for components independent of conflict-driven supply constraints. Fed members are focusing on the price impact of tech-driven investment on domestic demand. Core inflation is expected to maintain a 0.2% m/m expansion pace.

Warsh’s first Humphrey–Hawkins testimony. Congressional questioning differs from journalistic scrutiny as investors adapt to Fed Chair Kevin Warsh’s communication style. Tone on inflation should remain measured but possibly divergent from other FOMC members.

U.S. earnings season. Financials leads the U.S. earnings round. Banks’ forward-looking views on the U.S. economic cycle through a credit quality lens are also informative for markets and the lens. Q2 volatility has already tightened financial conditions, and the economy may not need additional forms of restraint.

China’s national accounts. GDP is expected to remain on track at 4.5% y/y but deceleration for Q2 is expected. Further contraction in retail sales and fixed asset investment will only increase urgency for stimulus for H2.

U.K. Labour Party leadership vote. Nominations end on Thursday, and a special leadership conference on Friday is expected to coronate Andy Burnham as the party’s new leader and next U.K. prime minister. U.K. assets will swing on the chancellor appointment.

North America: CPI, Warsh testimony and BOC the next signposts

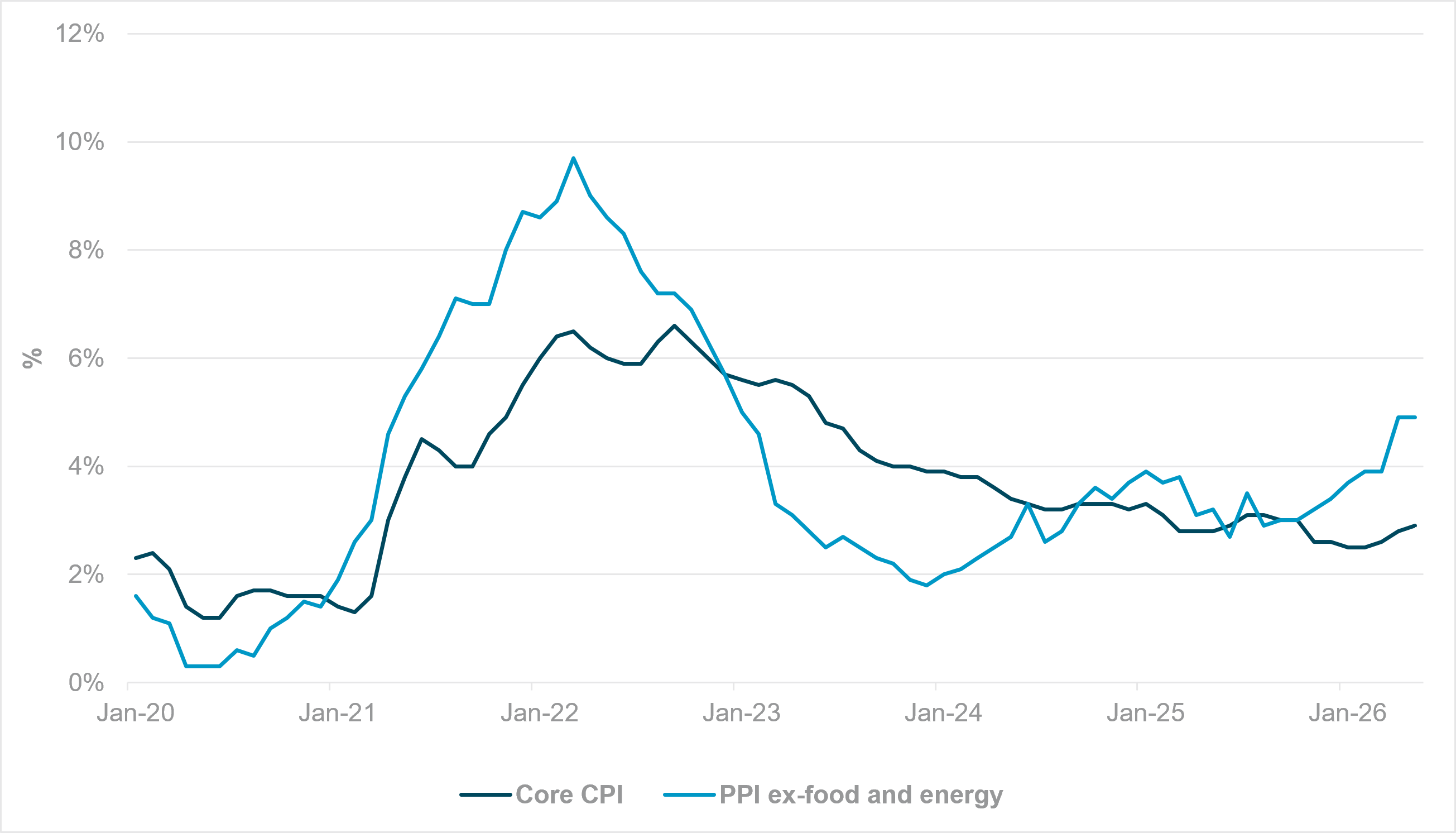

EXHIBIT #1: CORE CPI AND PPI EX-FOOD AND ENERGY, Y/Y

Source: BNY, Bloomberg

Our take: This week’s U.S. data calendar is materially busier than last week’s, led by CPI, PPI and University of Michigan sentiment. Also featured will be the first heavy slate of Fed speakers in the Warsh era, with 11 committee members making appearances, highlighted by Warsh’s first Humphrey–Hawkins testimony. Headline CPI and PPI final demand are both expected to print at -0.1% m/m, reflecting lower oil prices after an easing in hostilities with Iran last month, with core CPI holding at 0.2% m/m and PPI ex-food and energy at a firmer 0.4%. The Bank of Canada (BOC) meets on Wednesday in what is widely expected to be a pro-forma event where it’s expected to hold at 2.25%.

Forward look: The most important print this week will be core CPI, not headline, since markets will look through the oil-driven downside in energy-sensitive components and focus on whether underlying inflation is still running hot enough to limit Fed flexibility. A 0.2% core CPI print would probably be treated as orderly, but any upside surprise would reinforce the view that services inflation remains sticky and could push rates markets to continue to price a more hawkish Fed path.

PPI ex-food and energy at 0.4% also matters because it would signal that producer-side price pressures are not yet fully contained, even if headline PPI is softened by energy.

While we don’t expect Warsh’s appearance before Congress to reveal much, the testimony will be closely watched given his communication style and the likelihood of some hostile questioning.

In Canada, a steady BOC should be market-neutral unless the statement tilts materially more cautious or more hawkish than expected.

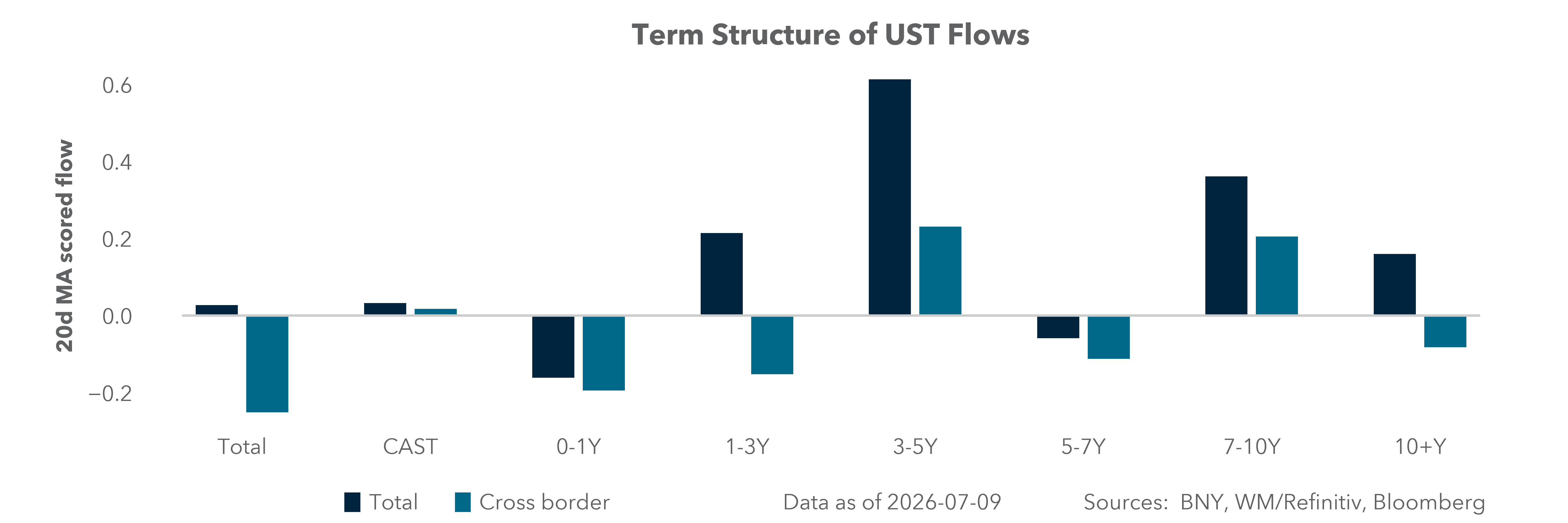

EMEA: Proof in the new PM’s gilt pudding

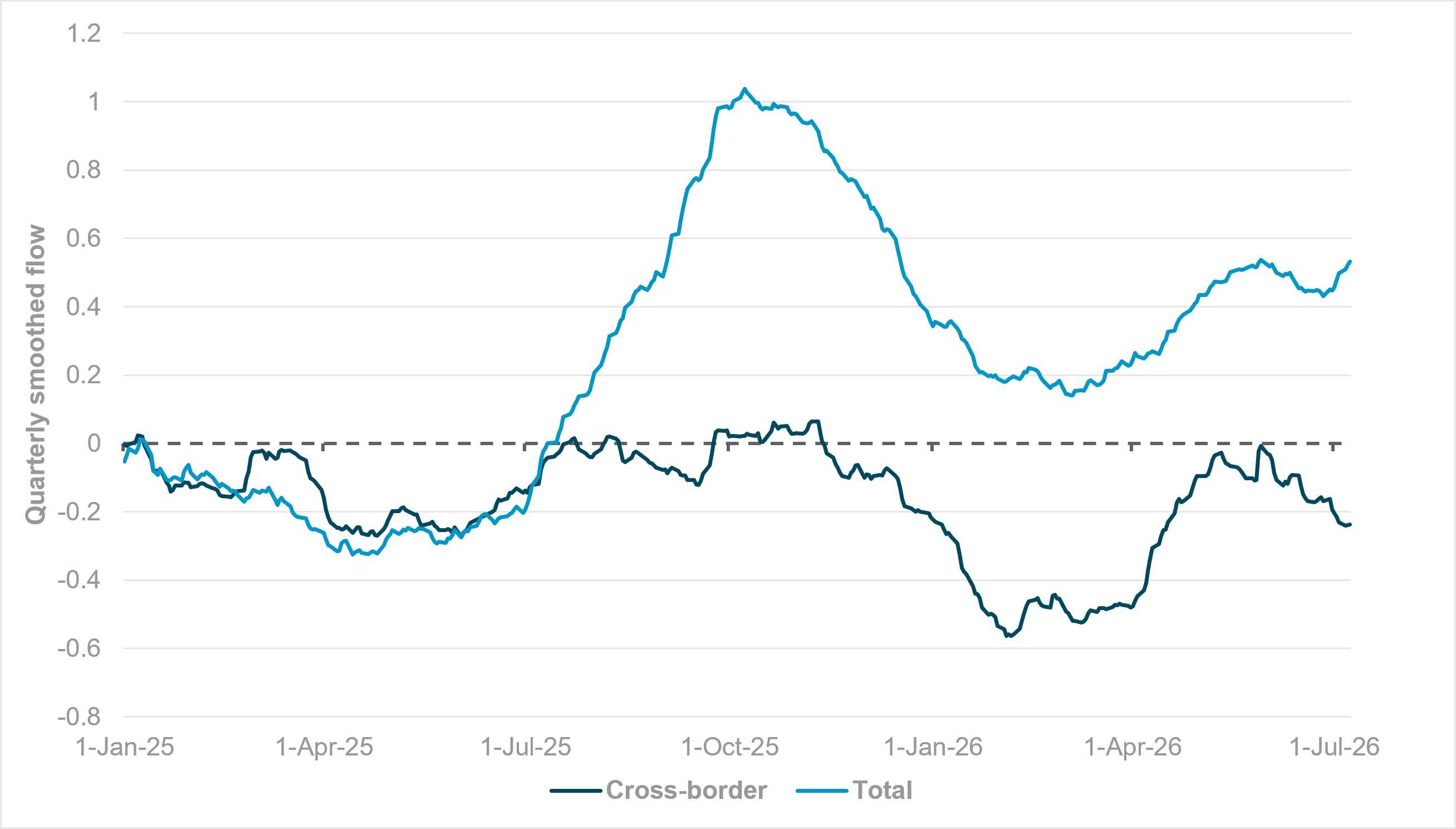

EXHIBIT #2: TOTAL AND CROSS-BORDER GILT FLOWS

Source: BNY

Our take: Andy Burnham will likely be confirmed as the U.K.’s seventh prime minister in 10 years in the coming days, and he would take office the week of July 20. For GBP and gilt markets, the identity of the next chancellor is far more significant, as they’re looking at binary outcomes with respect to a significant deviation from the November budget or the broad status quo. Several commitments from the Labour Party’s 2024 election manifesto will remain, such as the controversial “triple-lock” for state pensions, but in his recent speeches Burnham has acknowledged limits to current spending pledges and understands that markets will demand a path forwards fiscal sustainability.

The political challenges involved mean that “early” doesn’t mean major changes until the next general election – a new mandate for adjustment is required first. The OBR’s July 7 Fiscal Risks and Sustainability Report makes the stakes clear: “debt moves onto a steep upward trajectory in the 2040s in our baseline scenario, while in plausible alternative scenarios this happens earlier. It’s almost certain that future governments would have to take action to prevent this from happening. Acting early would reduce risk and would likely require a less costly fiscal adjustment than waiting.” For gilt investors, we do not expect a major change in current flow dynamics: real rates are attracting strong domestic buying, but international interest is nonexistent (Exhibit 2).

Forward look: Summer market conditions prevail across Europe, but as the ECB approaches its July decision, the divergences versus policy paths in the entire region are starting to show. There is a small chance of another move in July, even as the Eurozone’s final June CPI print on Friday is expected to show sequential contraction. A look at pivots elsewhere underscores the risk of the Governing Council’s current path, with Poland the latest Eurozone-integrated economy contemplating rate cuts.

The Governing Council needs to see what the rest of the continent is seeing in the lack of inflation risk. Supply constraints can only go so far if demand continues to deteriorate. China aside, European demand weakness is part of the global growth problem outside of tech.

The success from the recent NATO summit in Ankara and German fiscal plans have finally provided some momentum for Europe to push again for competitiveness and productivity. As valuations are now seen as attractive through FX and equities, cross-border investors looking for diversification away from U.S. and Asia tech may notice Europe a bit more.

APAC: China GDP, regional exports and the BOK

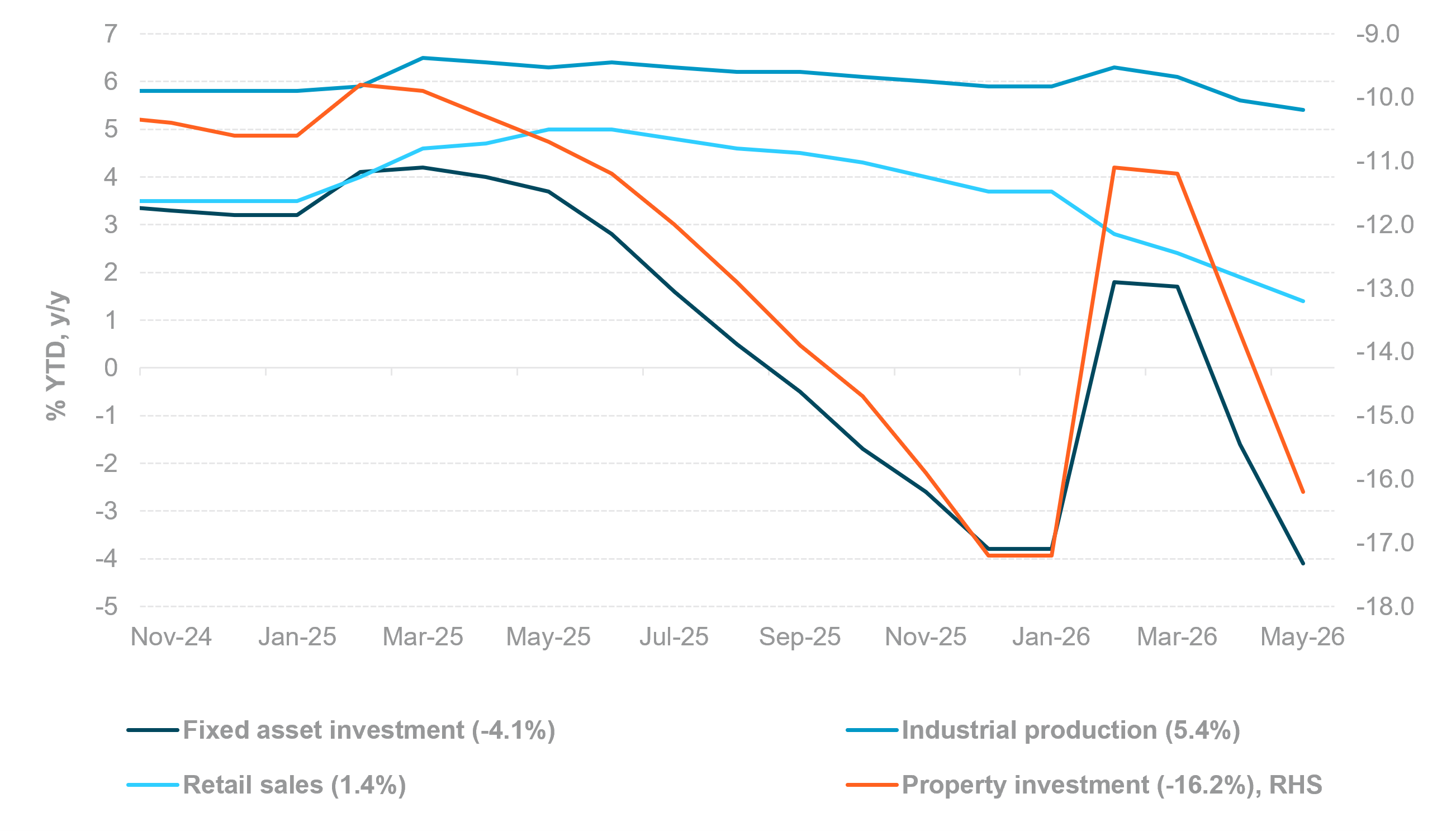

EXHIBIT #3: CHINA’S ACTIVITY, INVESTMENT AND CONSUMPTION NOT YET STABILIZING

Source: BNY, Bloomberg

Our take: Asia’s macro calendar is headlined by China’s Q2 GDP and June activity data, which will set the tone for regional markets. Investors will look for evidence that resilient exports and policy support are offsetting weakness in the property sector and domestic demand. Beyond the GDP print, retail sales, industrial production and fixed asset investment will indicate whether growth is stabilizing, while June home prices are likely to reinforce the need for further targeted property support.

Elsewhere, Q2 GDP from Singapore and Malaysia, together with Singapore’s export data, will provide another gauge of regional growth and the global electronics cycle. Policy and inflation are the other key themes. The Bank of Korea (BOK) is expected to raise rates to contain inflation, while India’s CPI, wholesale inflation and trade data will test expectations for further policy easing. In Australia, consumer confidence and inflation expectations will offer an early read on domestic demand ahead of the mid-August Reserve Bank of Australia meeting.

Overall, the week’s data will show whether Asia can continue to rely on exports as domestic demand remains soft, shaping both central bank expectations and regional market sentiment.

Forward look: APAC markets remained resilient despite renewed Middle East tensions, with country-specific developments dominating price action. Indonesia came under the most pressure after S&P Dow Jones Indices joined MSCI in reviewing its EM status. USDIDR broke above 18,000 for the first time since early June, while 10y INDOGB yields rose 10bp to 7.25% on capital outflows concerns.

South Korea also saw sharp volatility, with USDKRW plunging nearly 30 won toward 1,500 despite an unchanged DXY, driven by expectations of sizable KRW demand from the potential conversion of SK Hynix’s $26.5bn ADR proceeds. The KOSPI fell 7.5% on the week but remained 77% year to date.

TWD weakened through 32.00 for the first time since end-March on large dividend repatriation flows, while THB, PHP and INR edged lower alongside higher oil prices.

Japan’s Government Pension Investment Fund (GPIF) headlines are unlikely to alter the FX outlook. Finance Minister Satsuki Katayama’s call for higher domestic investment is unlikely to trigger a strategic asset allocation shift, with the GPIF's 25% allocation across domestic and foreign equities and bonds unchanged through 2030. A more effective policy lever to support the yen would be greater FX hedging of GPIF’s sizable foreign asset holdings rather than reallocating assets.

Overall, APAC FX divergence remains intact. We stay cautiously constructive on CNY, supported by capital inflows despite rising hedging demand, while remaining cautious on currencies facing capital outflows, persistent USD strength and weaker terms of trade.

Latin America: Carry interest helps overcome dollar concentration

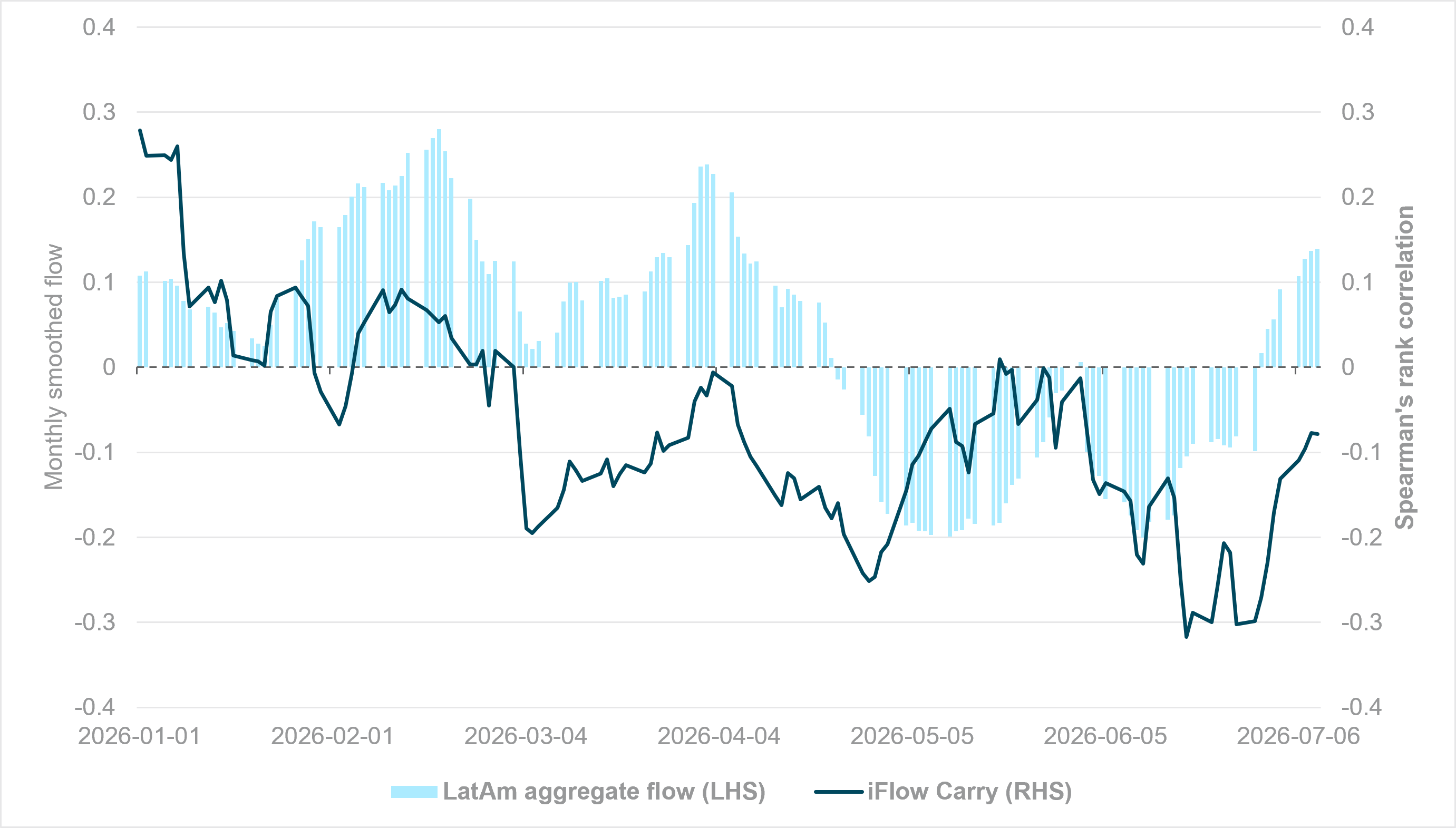

EXHIBIT #4: LATIN AMERICA AGGREGATE FX FLOW VS. IFLOW CARRY

Source: BNY, Bloomberg

Our take: Latin American currencies are now leading the way for a carry recovery. We identified a potential turn in our carry mean-reversion index around mid-June, and its current upward momentum is clear. This means that further alignment is due between bond yields and realized currency flows.

Political events have passed and markets will now turn to policy and appointments in Colombia and Peru. In both countries and across the region, credibility has been banked by central banks beforehand and real-rate buffers are sufficient. In Q2, the region was initially seen as haven thanks to rates and terms of trade, before Fed expectations started to erode carry-to-volatility ratios. As the Fed’s Warsh helps markets establish a new equilibrium for policy expectations, the challenge for Latin American currencies is to maintain carry momentum in the face of further Fed risks, though without terms-of-trade support. The lackluster reaction in commodity prices to renewed supply chain risks arising from the Gulf suggests that demand prospects remain weak; even if China announces more stimulus toward month end, commodity support will be tepid. If anything, there is a stronger case for general carry should China export disinflation to help support real rates globally.

Forward look: The regional data calendar is light. We expect most price action to be determined by U.S. CPI and Warsh’s congressional testimony, while global equity risk remains an anchoring factor. Brazilian retail sales for May should indicate a slight recovery from April’s contraction, but the broader trajectory for COPOM cuts remains intact as inflation edges toward 4.5%, supporting a double-digit, front-end real-rate buffer.

In contrast, growth rates in Colombian retail sales (Wednesday) are expected to stay near the mid-teens and support its central bank’s current path. Nominal wages are due in Mexico and expected to remain in the high single-digits, serving as a constraint on further easing, confirming the majority view on Banxico’s board, which has emphasized upside risks to inflation.

Central bank decisions

Canada, Bank of Canada (Wednesday, July 15): The BOC is expected to keep rates unchanged at 2.25%. Markets are expecting no change at least until Q4, but easing could be on the agenda with any renewed downside surprises to inflation. The recent pick-up in core inflation and labor market improvements suggest the status quo is adequate, but as Governor Tiff Macklem noted, the BOC is prepared to “take action” if the situation changes on inflation expectations.

South Korea, Bank of Korea (Thursday, July 16): We expect the BOK to raise the Base Rate by 25bp to 2.75%, as resilient growth and persistent inflation warrant further tightening. Q1 GDP surprised at 3.8% y/y, leading indicators remain supportive, and headline CPI accelerated to 3.2% y/y – the highest since December 2023 – on higher commodity prices. The key focus is forward guidance. Markets are already pricing in an aggressive hiking path, with three-month and nine-month forward 3m rates at 3.31% and 3.93%, respectively, versus the current 2.91%. Any pushback from the BOK could trigger front-end repricing, while a more hawkish tone would validate current market expectations.

Source: BNY

Source: BNY