Valediction and celebration

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Geoff Yu

Time to Read: 8 minutes

What You Need to Know

Supply constraints in the memory and storage chip industry are lifting earnings and margins, but the associated costs are beginning to spill over into the broader economy – and the sector itself is struggling to reconcile lofty valuations with mounting idiosyncratic pressures. Meanwhile, markets are starting to see tangible relief from the extended ceasefire in the Middle East. As the world’s central banking elite gathers at the ECB Forum in Sintra, discussions are likely to gravitate toward longer-term structural issues such as productivity and the role of AI, rather than the appropriate policy response to energy shocks. Markets continue to price out further rate hikes across developed economies, but easier inflation alone is unlikely to restore sentiment.

In focus this week:

Semiquincentennial. The U.S. marks its 250th anniversary this week with nationwide celebrations. Philadelphia, New York and Washington, D.C. will host many of the commemorative ceremonies, which include concerts, fireworks, and military and maritime displays. U.S. financial markets will be closed on Friday, July 3, in observance of the Independence Day holiday.

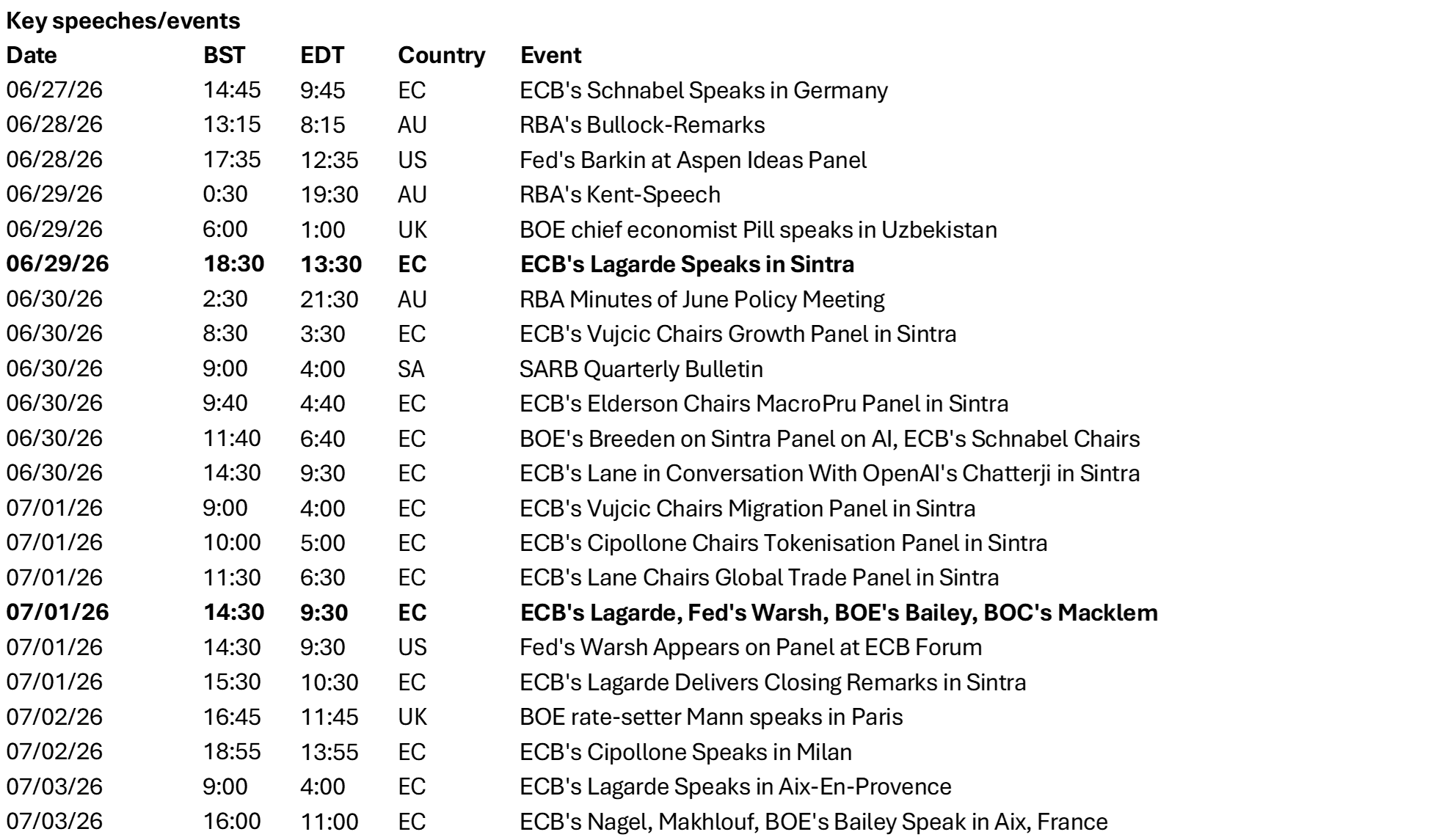

Sintra. European Central Bank (ECB) President Christine Lagarde will give what may be her valedictory speech on Monday, opening the three-day symposium with the theme “Shaping Europe’s future: innovation, growth and stability.” The ordering is probably right: Europe has realized that without innovation and productivity gains, growth stalls – and stagnation breeds broader socioeconomic instability. The highlight of the sessions is a policy panel she will share with Fed, Bank of England (BOE) and Bank of Canada (BOC) counterparts.

Labor markets. The U.S. June nonfarm payrolls report will be released on Thursday ahead of the holiday, alongside a broader run of labor market indicators. Payroll growth is expected to remain above 100,000, but stabilizing wage growth will be more important in shaping policy expectations. Like many of its developed market peers, the Fed will likely judge that its earlier pivot toward inflation vigilance has reduced the need for further tightening, although the continued resilience of the U.S. economy means that view will still require validation.

European PMIs and CPIs. Final inflation and business surveys are due across Europe, and the outlook remains poor, even though the worst-case scenarios regarding the conflict-driven supply shock look set to be avoided. The initial release relied on responses before the signing of the memorandum and business conditions have likely improved further. However, structural challenges are no less pressing – the June preliminary report for Germany warned that output expectations had weakened again for the next 12 months, well below their long-run trend.

APAC equity markets may need to start caring about the economy. China’s June PMIs, South Korea’s exports, and Japan’s Tankan survey will test whether improving trade and manufacturing momentum is translating into stronger domestic demand. Even if the data surprise positively, markets are so focused on AI-related semiconductor and memory stocks that an improving macro backdrop may not lift broader risk sentiment.

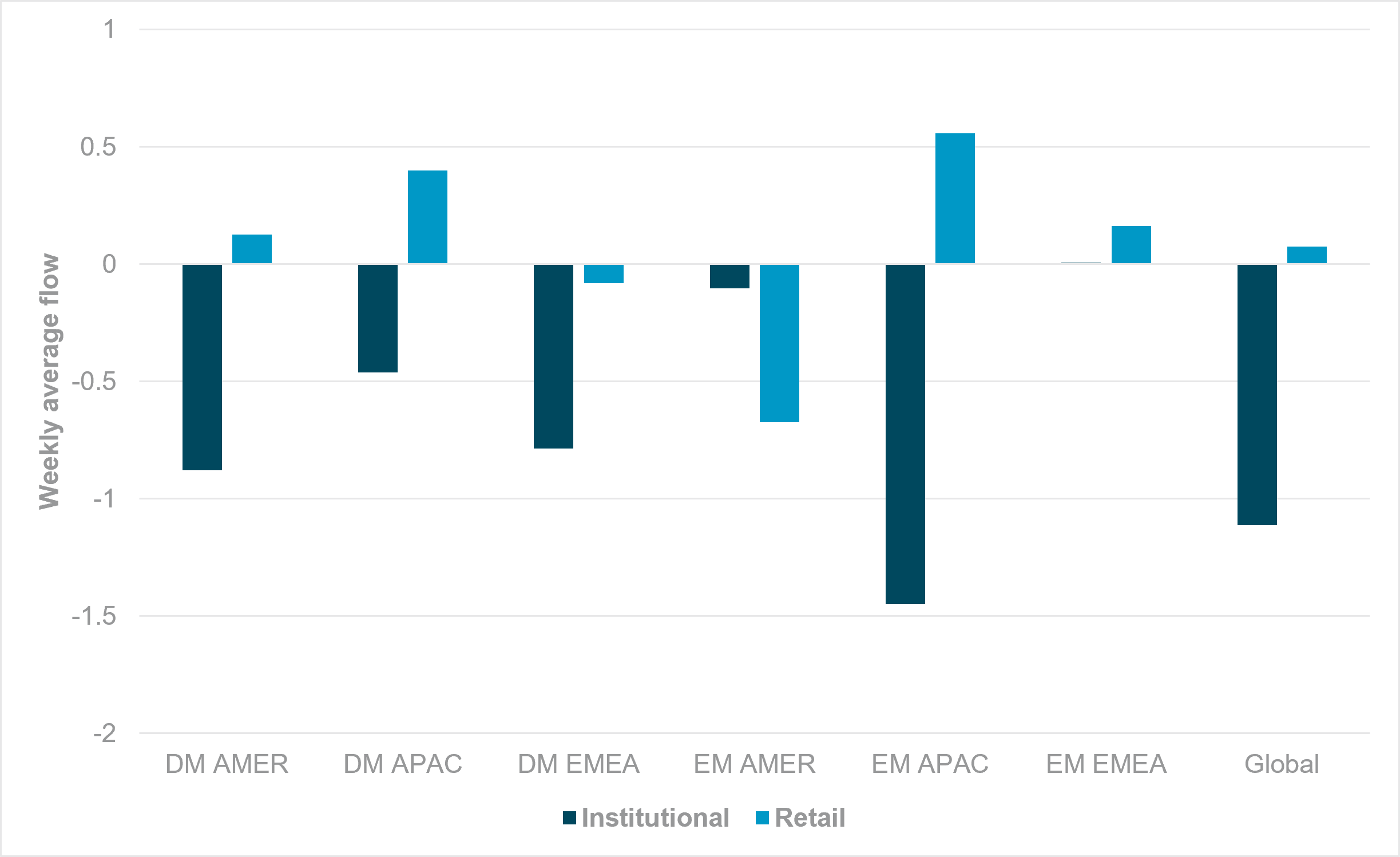

Retail vs. institutional: A widening divergence

EXHIBIT #1: RETAIL FLOWS SHOW COMPREHENSIVE DIVERGENCE VS. INSTITUTIONAL

Source: BNY, week ending June 25

Our take: Risk sentiment will seek to start the week on a stronger footing but questions over the distribution of participation will likely rise, especially in APAC markets and the broader technology complex. We have highlighted that technical limits on single-stock ownership have driven selling by institutional investors out of South Korea and Taiwan – two key markets in the current AI and semiconductor theme. These figures are corroborated by official data that show high levels of cross-border institutional outflows. Yet, retail remains resolutely on the other side of these flows – buying the dip at every opportunity. The phenomenon extends beyond APAC, as our data indicate that retail has been net buying in every region apart from EM Americas, and even there the outflow was marginal. The divergence is clear even when there is directional alignment: during the major communications IPO over a week ago, institutional purchases were moderately strong, but retail had a record seven-standard deviation move.

Forward look: Questions over the sustainability of divergence persist. The easy answer is retail capitulation in a falling market, especially where leverage is involved. However, through May and June, we have seen various instances where institutional flow is also “stopped” back into the market due to underperformance, especially in South Korea. If so, then depending on hedge ratios, there could be significant inflows back into developed Americas, EM APAC and DM APAC markets, where there is directional divergence and a large flow gap. Meanwhile, we note that EM Americas is the only region where retail interest is poor. Given our view that carry currencies in the region may start performing and the market is increasingly worried about soft commodity prices, LatAm may generate some rare retail “catch up.”

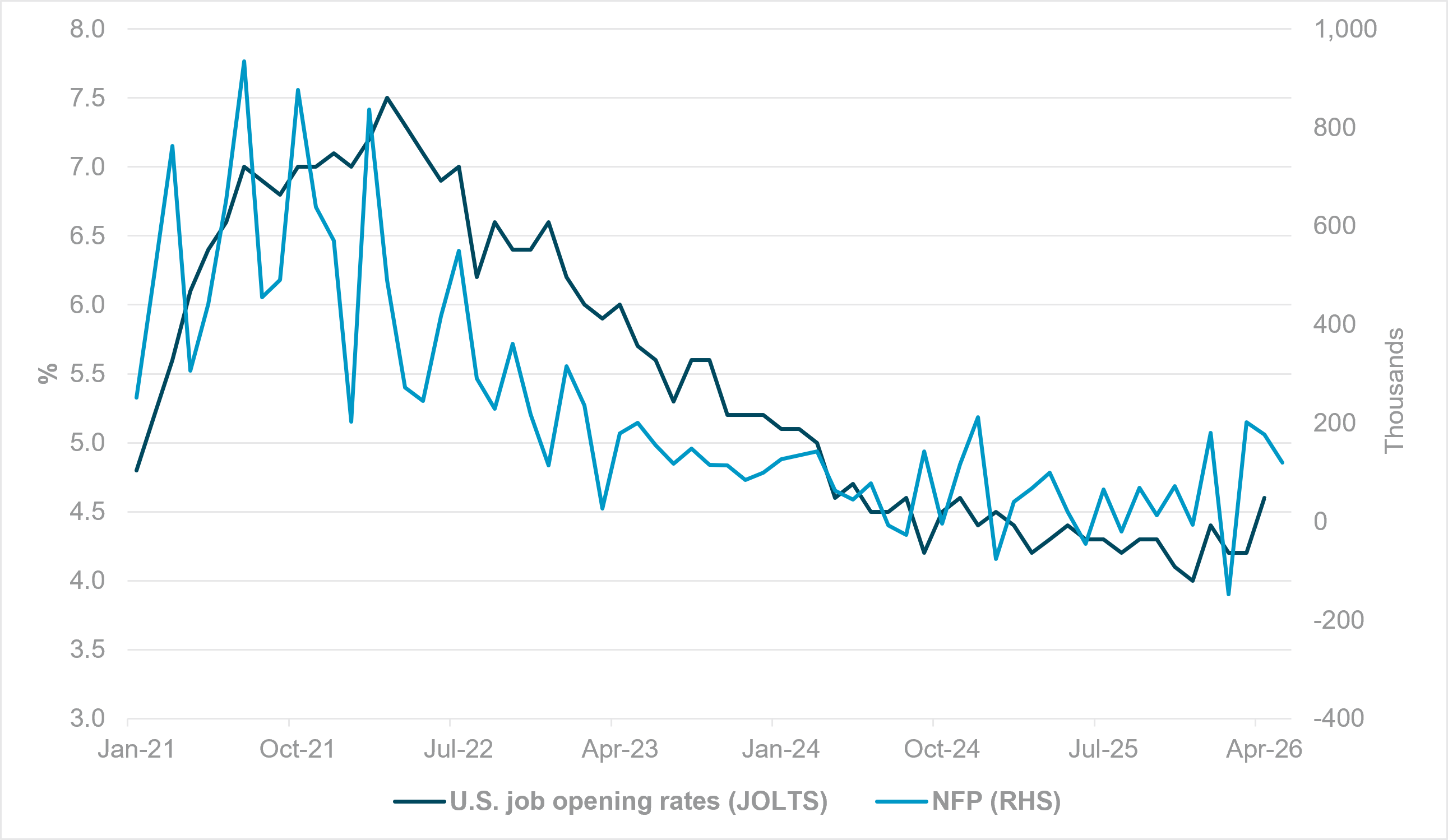

North America: All eyes on payrolls

EXHIBIT #2: JOLTS VS. NONFARM PAYROLLS, MONTHLY CHANGE

Source: BNY, Bloomberg

Our take: Last week’s slightly softer-than-expected May headline PCE print moderated some of the most pronounced concerns of accelerating inflation, and markets have already responded by trimming some of the year-end hike pricing that had built up around firmer data. That keeps the Fed reaction function in focus heading into a holiday-shortened U.S. week.

Despite the short week, the domestic calendar is quite busy; the labor market taking center stage with JOLTS on Tuesday and nonfarm payrolls on Thursday. On the Fed speaker side, there is little to challenge the macro narrative directly, though Warsh’s appearance at the ECB forum on Wednesday could offer a useful read on his policy framing.

Canada is similarly light, with only GDP and PMI on deck, alongside Governor Tiff Macklem’s appearance at the same ECB forum.

Forward look: The most important release is unquestionably the NFP report on Thursday – but JOLTS on Tuesday will set the tone heading in, providing the first hint as to whether labor demand is continuing to normalize or is still running hot enough to keep the Fed cautious. In the current environment, where markets are actively recalibrating the Fed path, a stronger-than-expected payrolls number would likely reprice front-end rates higher and support the case for tightening later in the year. Conversely, a clear softening in hiring, or a material rise in unemployment, would support the view that policy will remain on hold and could further compress hiking odds. For rates markets, the NFP print will set the tone.

Canada’s GDP and PMI should be market relevant only if they materially alter the growth narrative, but they are unlikely to rival the U.S. labor data in importance.

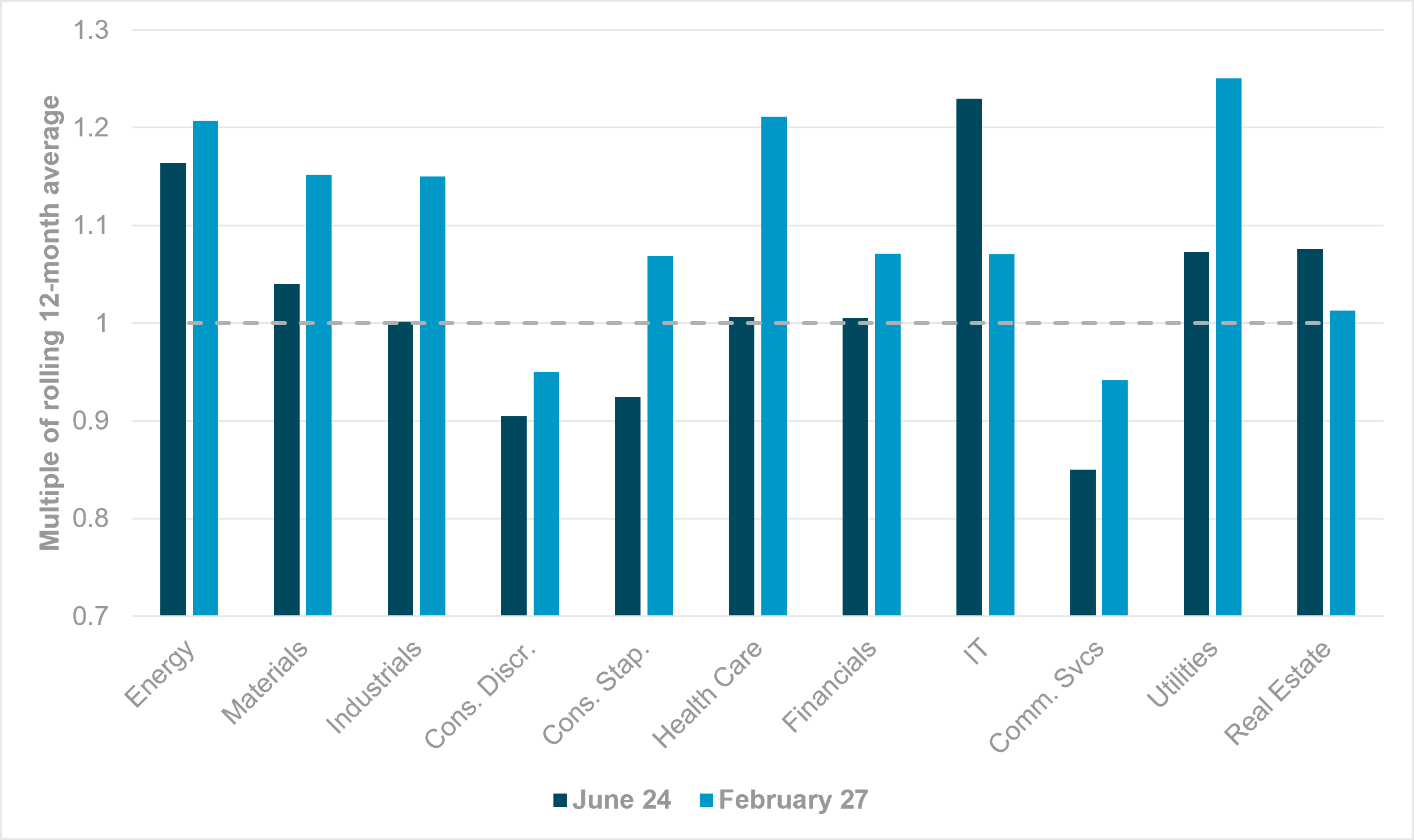

European growth debate is needed at Sintra

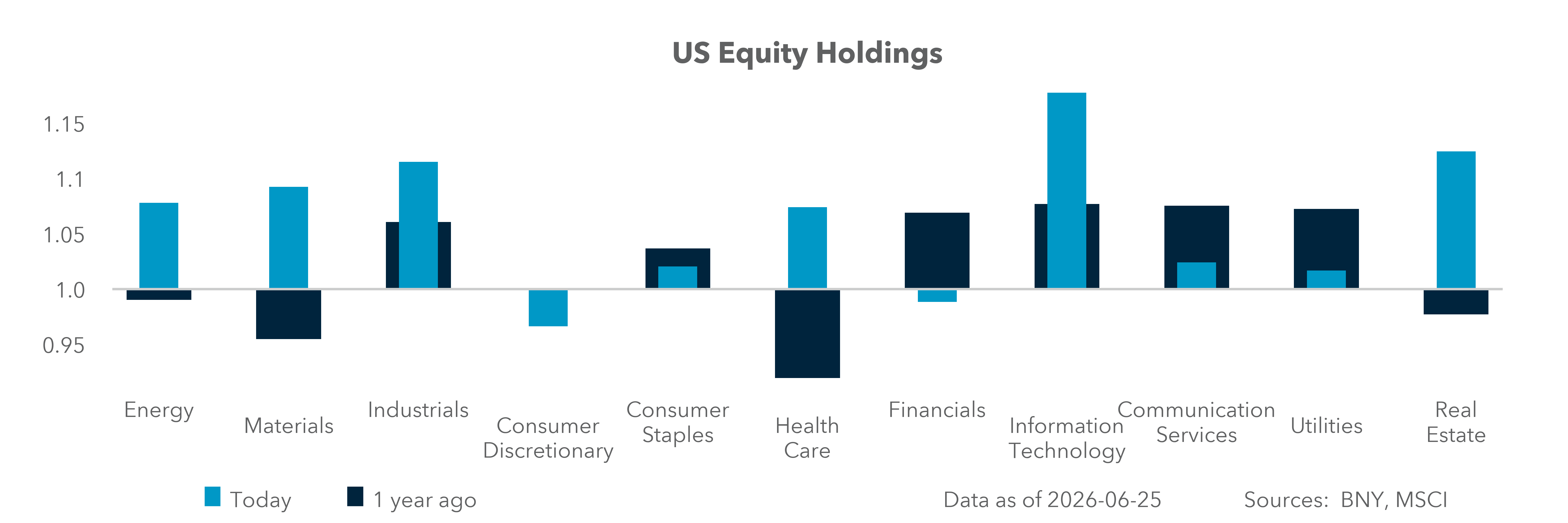

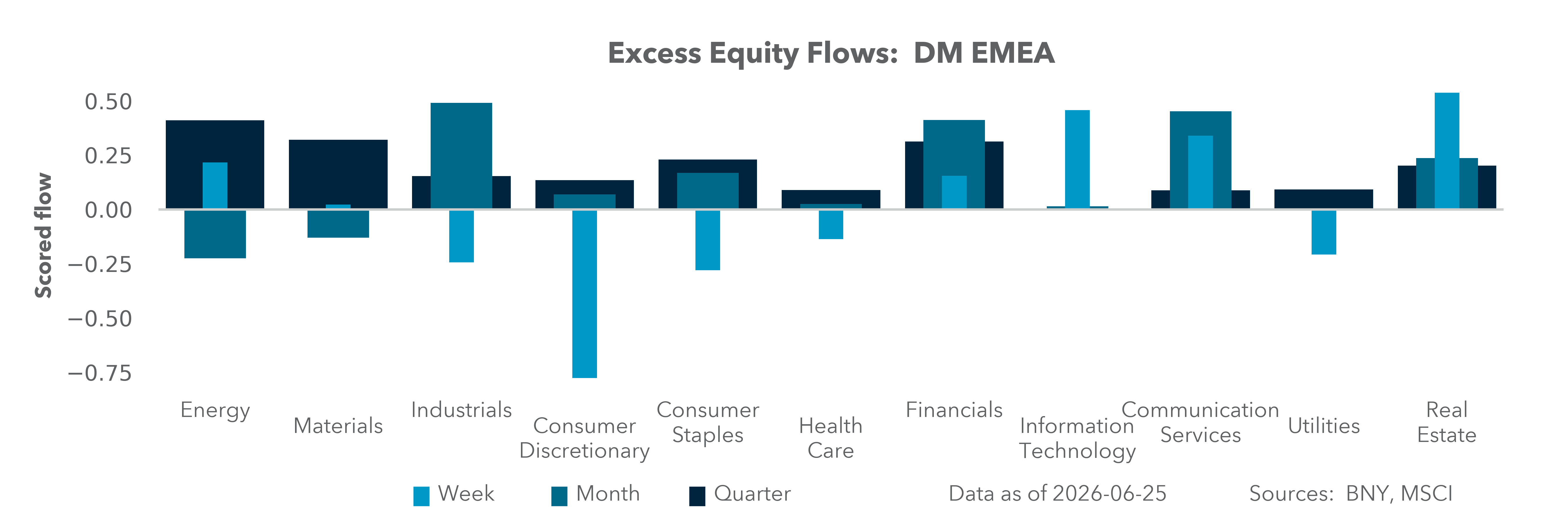

EXHIBIT #3: EUROPEAN SECTOR HOLDINGS AS MULTIPLE OF ROLLING 12-MONTH AVERAGE

Source: BNY

Our take: The ECB’s flagship Sintra symposium (equivalent to the Fed’s Jackson Hole sessions) kicks off in Portugal this week. It’s possible this will be ECB President Lagarde’s final forum amid reports that she may step down this year to ensure her successor is in place before the French presidential elections next April, even though she has indicated a desire to remain in office until October 2027.

Sintra also marks Warsh’s first public appearance among global peers. He leads the only central bank in this group with a dual mandate – as much as the topic of how a central bank can influence growth remains off-limits at the ECB. Warsh’s task force on productivity and jobs sits in the context of AI and new technologies. But linking its findings to monetary policy reaction functions would likely be seen as a mandate breach by more hawkish members. Whenever growth is brought up, even Lagarde defers to the Draghi and Letta reports.

Whether the neglect is by choice or by design, it’s no longer sufficient for Europe, and equity allocations reflect that lack of confidence. Out of the 11 GICS Level 1 sectors we track, developed Europe shows that only two – Real Estate and IT – have seen holdings levels recover to pre-conflict levels (Exhibit 3). In absolute terms, U.S. sectoral holdings are ahead of Europe in eight of the 11: Energy, IT and Utilities. Crucially, the weakest performers in Europe at present are Industrials, Consumer Discretionary, Consumer Staples and Communication Services, indicating that private sector demand and the sectors of past and future are all lagging.

Forward look: The euro’s ongoing slide is further evidence that current policy settings are hurting asset allocation, and the ECB will need to look at current financial conditions in this respect. At his press conference last week, Warsh said the task forces “start with first principles, ask hard questions, examine current practice, consider alternatives, and ultimately propose next steps for policymaker consideration.” Perhaps the ECB isn’t asking itself the hard questions about its current framework, which means the same hard questions won’t be asked of the ECB’s policy response. Investors would prefer that changes are organically led by a central bank rather than imposed. Without change, asset allocation into Europe will continue to erode. The growth narrative is increasingly elusive on institutional factors – and that’s before any China-related shock. Preliminary inflation figures are also expected to show broad declines to below 3% y/y, and downside surprises may strengthen the case for a July pause.

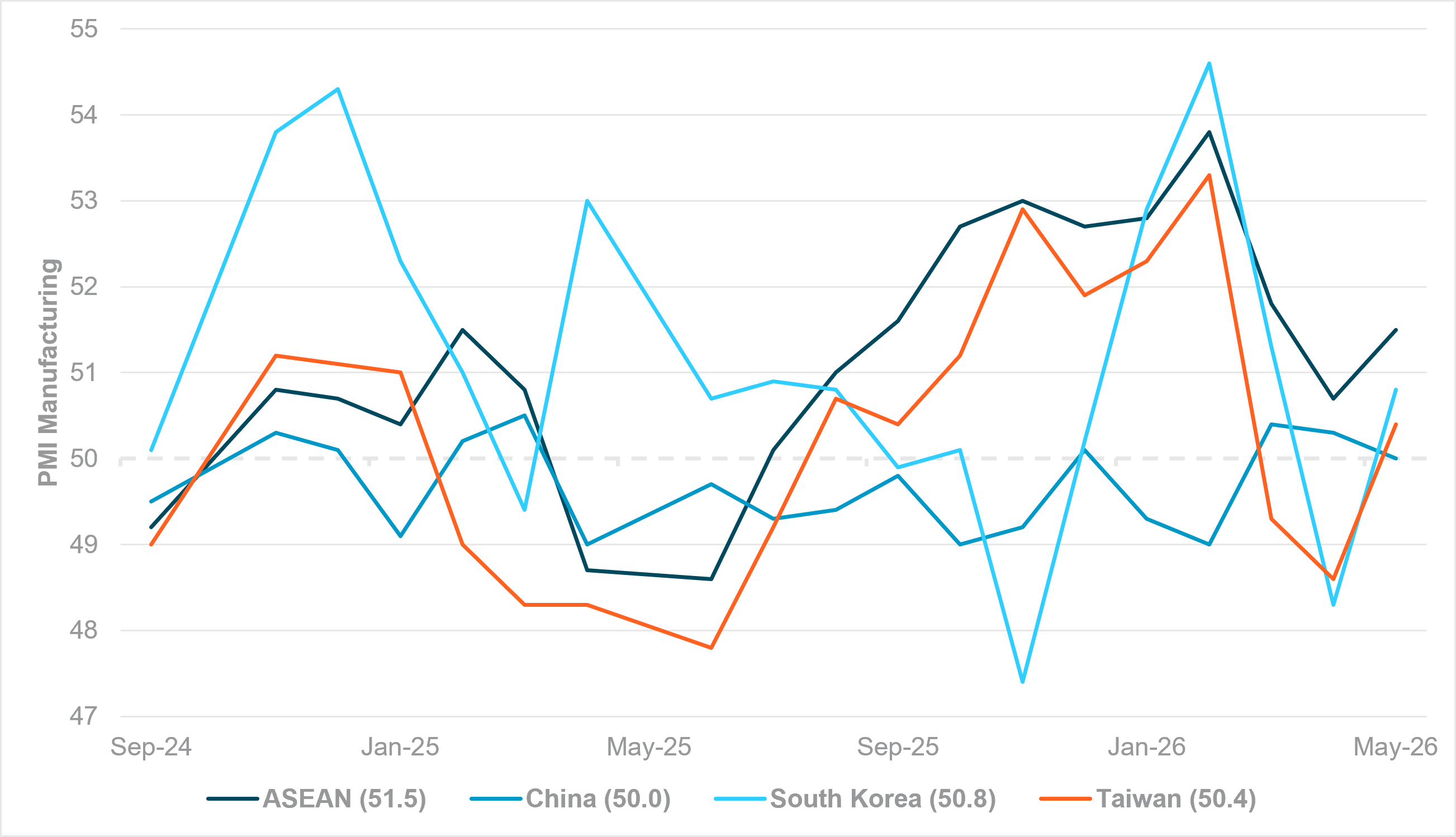

APAC: Macro data test the domestic demand story

EXHIBIT #4: APAC MANUFACTURING PMI – ASEAN LEADS, BUT THE GAP IS NARROW

Source: BNY, Bloomberg

Our take: A dense run of activity and inflation indicators dominates the APAC calendar this week, with China’s June PMIs setting the regional tone amid ongoing questions over the strength of domestic demand and manufacturing momentum. Markets will also focus on South Korea’s June exports, CPI and PMI releases, which will provide one of the earliest reads on global trade conditions and semiconductor demand. Japan’s Q2 Tankan survey, alongside May industrial production, retail sales and labor market data, will be closely watched for signals on corporate sentiment and the sustainability of domestic demand.

Indonesia’s June CPI and May trade data will also be key for assessing the policy outlook, while Thailand’s exports and manufacturing figures, and India’s industrial production and bank credit data, will offer further insight into regional growth dynamics. Singapore’s PMI and electronics sector index will be monitored as a gauge of the technology cycle, while Australia’s focus will be on private sector credit, trade figures and final June PMI readings for clues on domestic demand and external sector resilience. In New Zealand, business confidence, activity outlook and consumer confidence surveys will provide a timely assessment of economic momentum.

Overall, the week’s releases should help investors gauge whether Asia’s growth backdrop remains supported by trade and manufacturing recovery or whether softer domestic demand continues to constrain the region’s expansion, with implications for both regional FX and rates markets.

Forward look: The relief from lower crude oil prices proved short-lived. Asia is now facing a renewed headwind from the resurgent U.S. dollar as markets reprice Fed rate expectations, adding to persistent foreign outflows and fragile equity sentiment. For example, foreign investors sold a record $5.9bn of Taiwan equities in a single day last week, while cumulative index rebalancing-related foreign selling of South Korean equities has reached roughly $85bn year to date. Macro data is likely to take a back seat as investors focus on managing portfolio FX hedges amid broad USD strength. USDJPY remains the key market to watch. A decisive break above 162 technical resistance would raise the risk of negative spillovers across APAC currencies, equities, and rates.

The Chinese yuan remains the regional outlier. iFlow scored holdings indicate CNY hedging demand is still near historical lows despite the stronger dollar. The offshore yuan (CNH) has shown relative resilience, but that’s increasingly difficult to sustain, suggesting investors have room to rebuild USD hedges if dollar strength persists.While the worst of the recent market stress may be behind APAC, the recovery path is likely to be gradual as policymakers continue to address fiscal vulnerabilities, external financing needs, and broader deficit concerns.

Valediction and celebration may define the week’s calendar, but markets will be looking beyond the symbolism. While Sintra is likely to shift the policy debate toward productivity, innovation and AI, a busy run of labor market, inflation and global business survey data will test whether easing price pressures are being matched by stronger economic momentum. Relief from conflict-driven inflation is giving central banks greater flexibility, but the harder questions now concern the economics of AI investment, Europe’s structural growth challenges and whether domestic demand is strong enough to sustain global expansion.

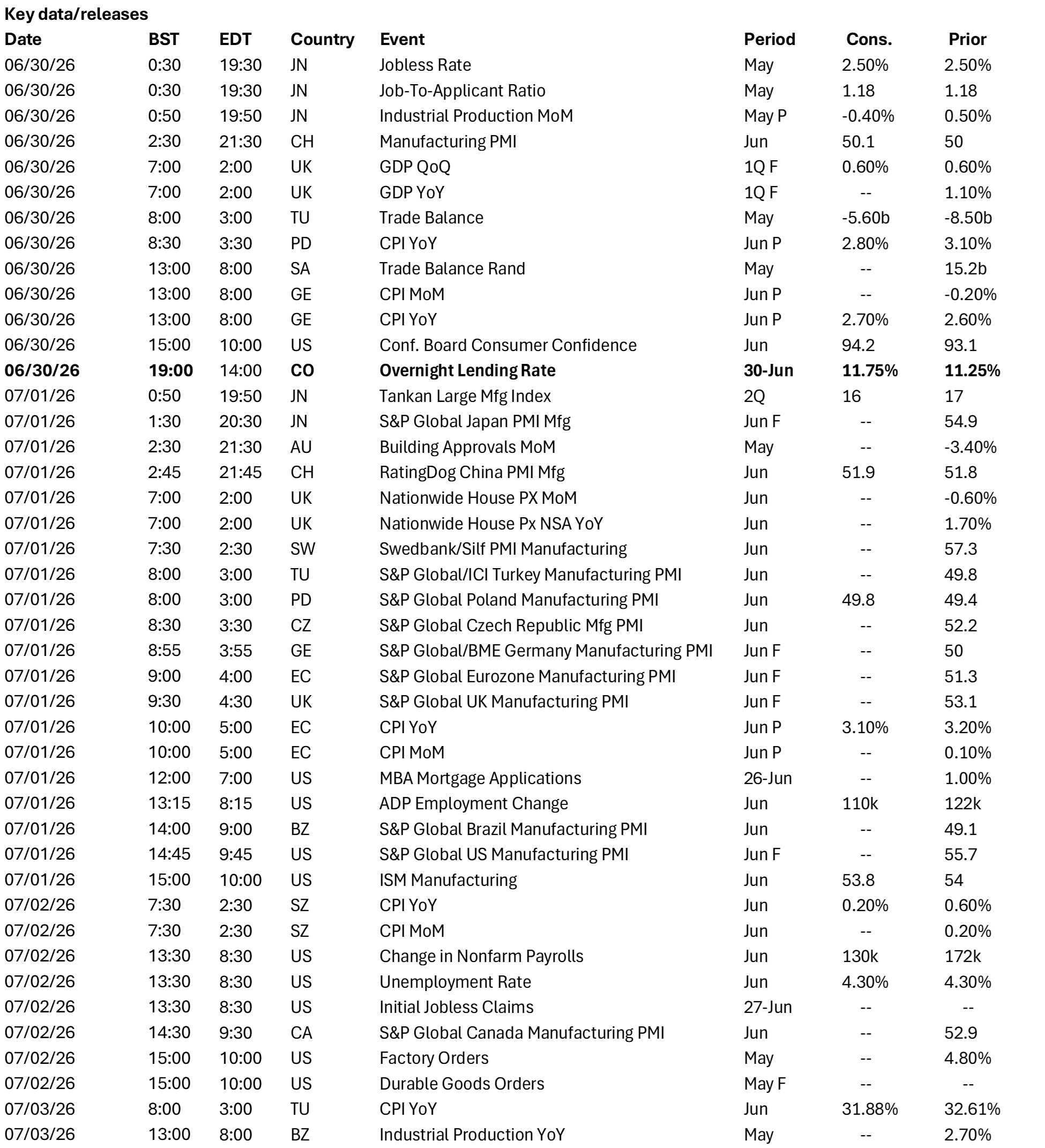

Central bank decisions

Colombia, Banco de la República (Thursday, June 25): The BdlR will solidify its status as the most aggressive LatAm central bank with another 50bp hike to 11.75%. Maintaining real rates close to 6% is supportive for assets, complementing the rerating that has been ongoing since the presidential election outcome. COP is currently the best-positioned Latin American currency in iFlow, though recent flow momentum has lagged.

Source: BNY

Source: BNY