Turns and Turnarounds

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 13 minutes

Equity markets had their worst weekly performance in seven months. The Q4 slowdown has become a consensus view — with the U.S. blamed for policy uncertainty and ongoing government shutdown, which has raised doubts about holiday travel and spending. The Challenger, Gray & Christmas job layoffs report, the worst in 20 years, was linked to cost-cutting, while the University of Michigan flash survey for November cited prices and the economy as drivers of weaker consumer sentiment. The bond market was unable to bounce amid shifting views on Fed rate cuts and ahead of $125bn in U.S. Treasury coupon supply this week, following $55bn in new investment-grade supply this week. Concerns about a technology bubble and risk of larger correction dominated risk-taking. Tech pain spread as Bitcoin reversed 8%, emerging market equities declined, and oil fell 2% on the week.

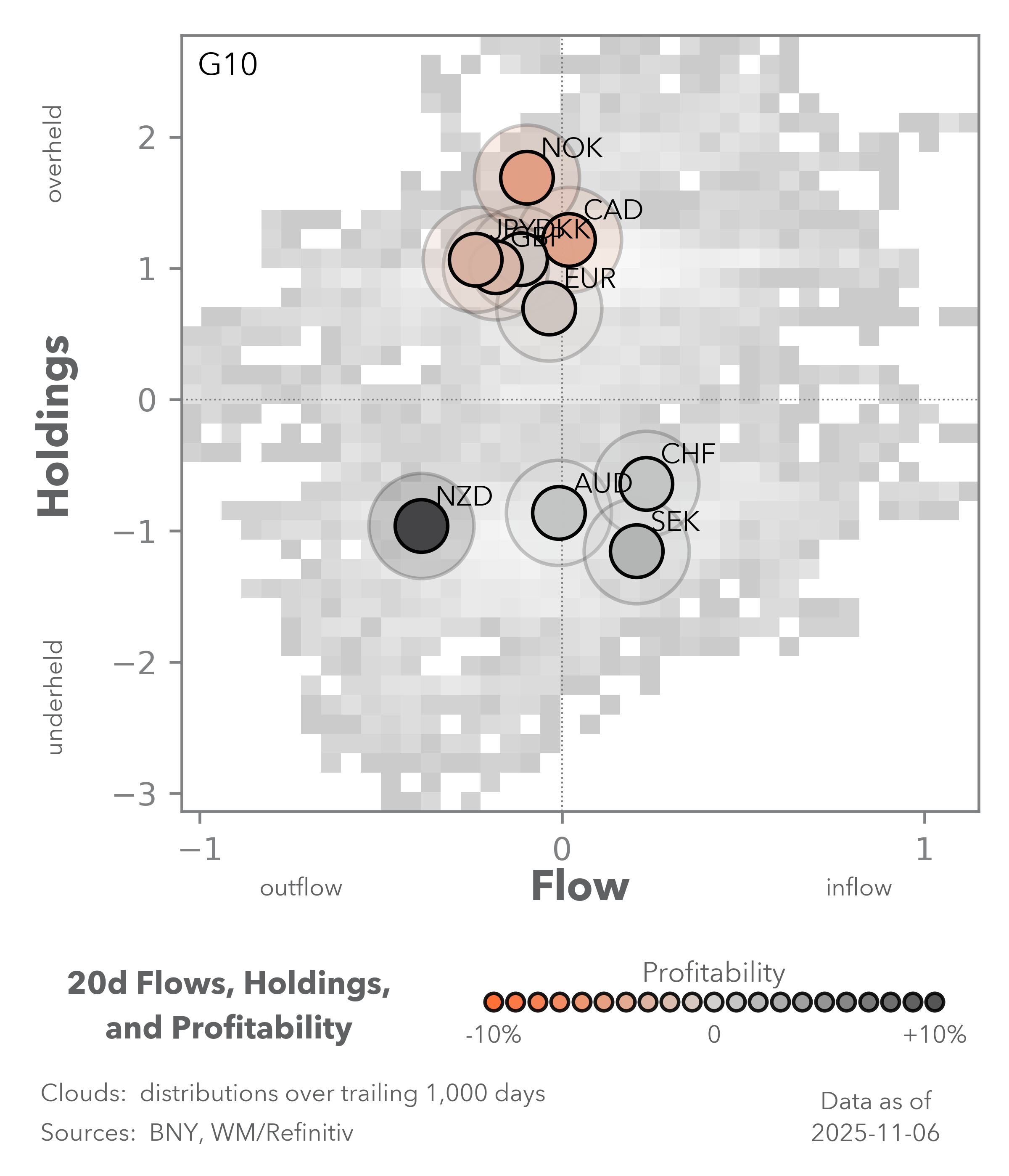

Looking ahead, investors are focused on when and how the U.S. government reopens, and what it means for growth. The U.N. COP30 in Brazil will return focus to climate issues as views shift. Meanwhile, several Fed speakers plan to address the topic of their dual economic mandates. Q3 earnings will also continue, with just 10% of S&P 500 companies left to report, driving attention outside the U.S., with Japan and Canada notable. The U.S. dollar (USD) also failed as a shock absorber, as the index reversed from over 100 earlier in the week to 99.58 following weaker economic data.

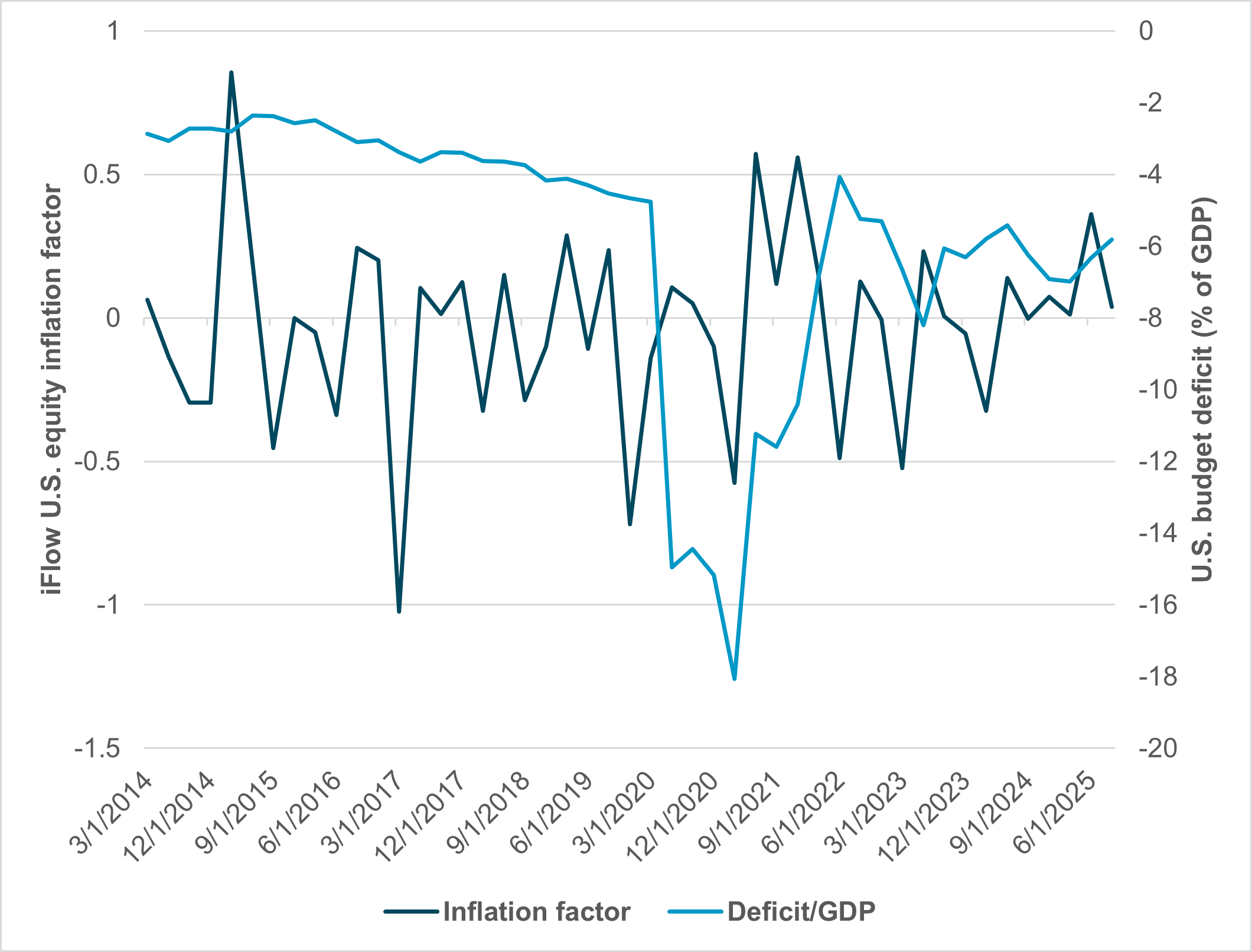

Are investors worried about budget deficits more than the global economy?

EXHIBIT #1: U.S. EQUITY INFLATION FACTOR VS. U.S. BUDGET DEFICIT

Source: BNY, CBO

Our take: Over the past week, the global focus turned to budgets, starting with the appointment of Abenomics acolytes in Japan, continuing with U.K. Chancellor Rachel Reeves’ speech on her budget plans, and ending with ongoing budget debates in France. In the U.S., prospects for a government reopening and rising cash needs sparked some concern. However, the Supreme Court hearing on tariffs weighed more heavily, as investors were forced to consider the odds of the government returning $125bn in tariffs to companies and pressuring the deficit. Rates and budget debates have long been correlated, but the link to equities is newer. Inflation lessons from COVID-era spending are now part of the risk equation, as Exhibit #1 shows. Investors see greater inflation risk when the government spends. The lack of inflation fears in U.S. equity flows in 2025 was the surprise of the summer, but that could be shifting quickly into year-end.

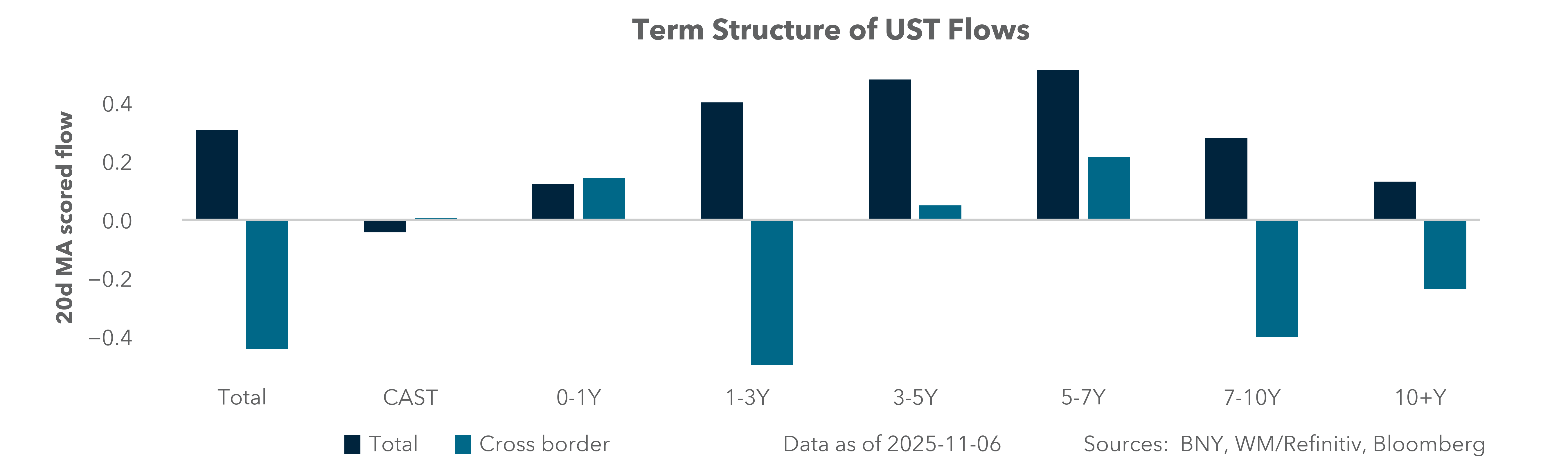

Forward look: For the U.S. government to avoid squeezing out investment amid rising borrowing, foreign flows are needed, and those have been notably weak in October and early November. Foreign interest in U.S. markets has been weak since the end of Q3, and the bounceback in bond buying after the Fed cut was short-lived. The weakness this week in Big Tech adds to concerns that U.S. money flows will be a domestic story, dependent on solving the government shutdown, renewed Fed liquidity backstops, and investor confidence that productivity gains will follow from AI. Further volatility seems likely if markets don’t get what they need to sustain the typical seasonal risk appetite.

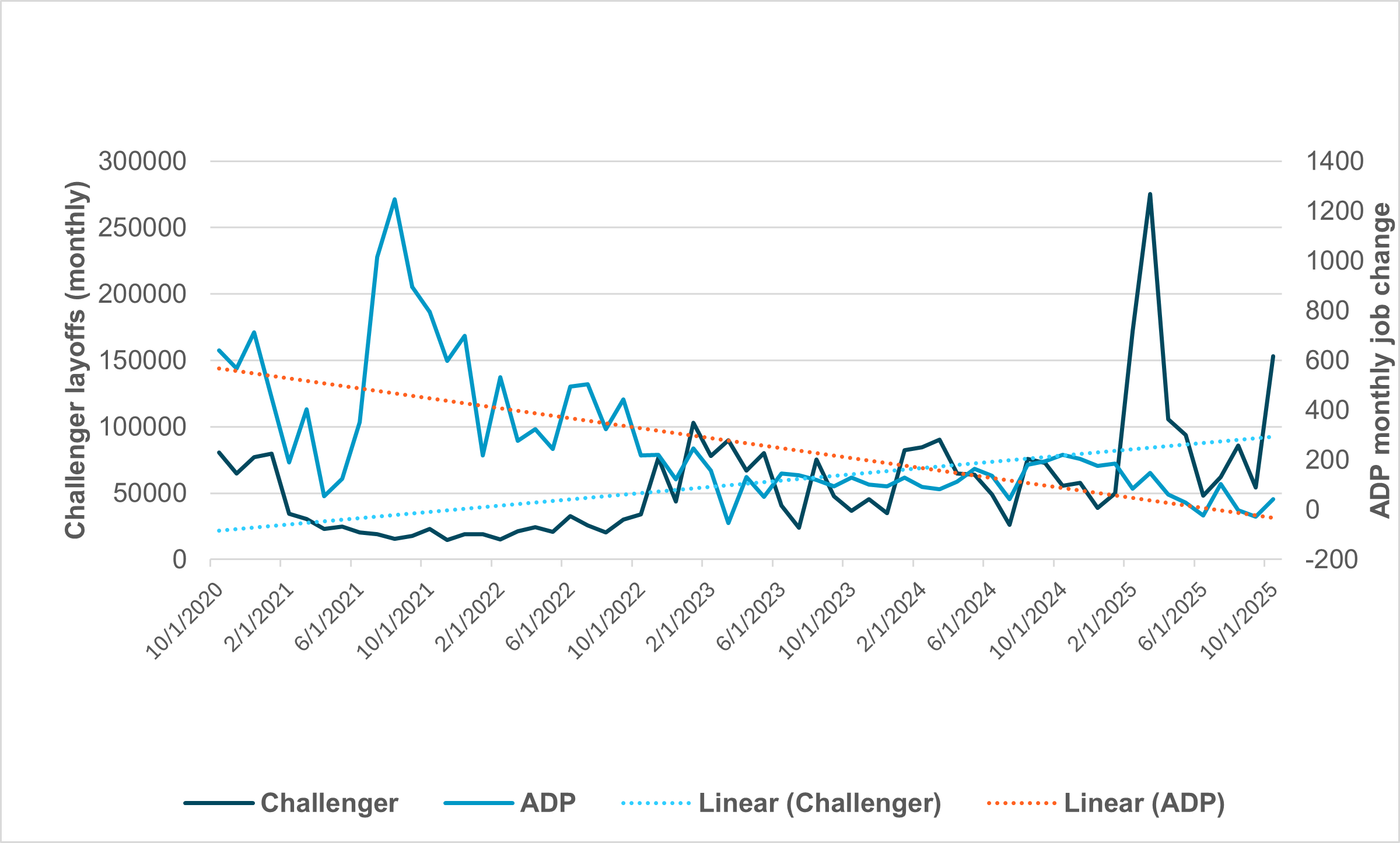

U.S. markets focused on government shutdown, bond supply

EXHIBIT #2: U.S ADP TREND FOR HIRING LOWER, U.S. FIRING HIGHER, ACCORDING TO CHALLENGER

Source: BNY, Bloomberg

Our take: Whether jobs remain stable or tilt lower toward recession remains the essential question for investors and the Fed. Last week’s data changed some views on the U.S. labor market. However, the Federal Open Market Committee (FOMC) speakers remain divided. The lack of data matters more in the week ahead. State-level jobless claims and ADP weekly data will be areas of focus offsetting the Challenger report. As shown in Exhibit #2, job gains are slowing while job cuts are rising. A jobs turning point may require confirmation from official data once the government reopens, but markets aren’t likely to wait, and pricing in of further Fed easing and economic weakness seems likely.

Forward look: This week brings $125bn in 3y, 10y and 30y bond supply, alongside the usual heavy supply of Treasury bills. Markets will watch for squeezing out risk between U.S. government paper and ongoing investment-grade borrowing, which hit $55bn last week and is expected to slow to $30bn this week. Many see the connection between borrowing needs and liquidity as a risk, especially with the Nov. 11 Veterans Day holiday seen as another “turn-like” test, as investors require cash to settle bills and bonds. The lack of government data will also shift attention to Fed speakers and their reactions to the rest of the world. What remains most important is clear: how and when the government reopens.

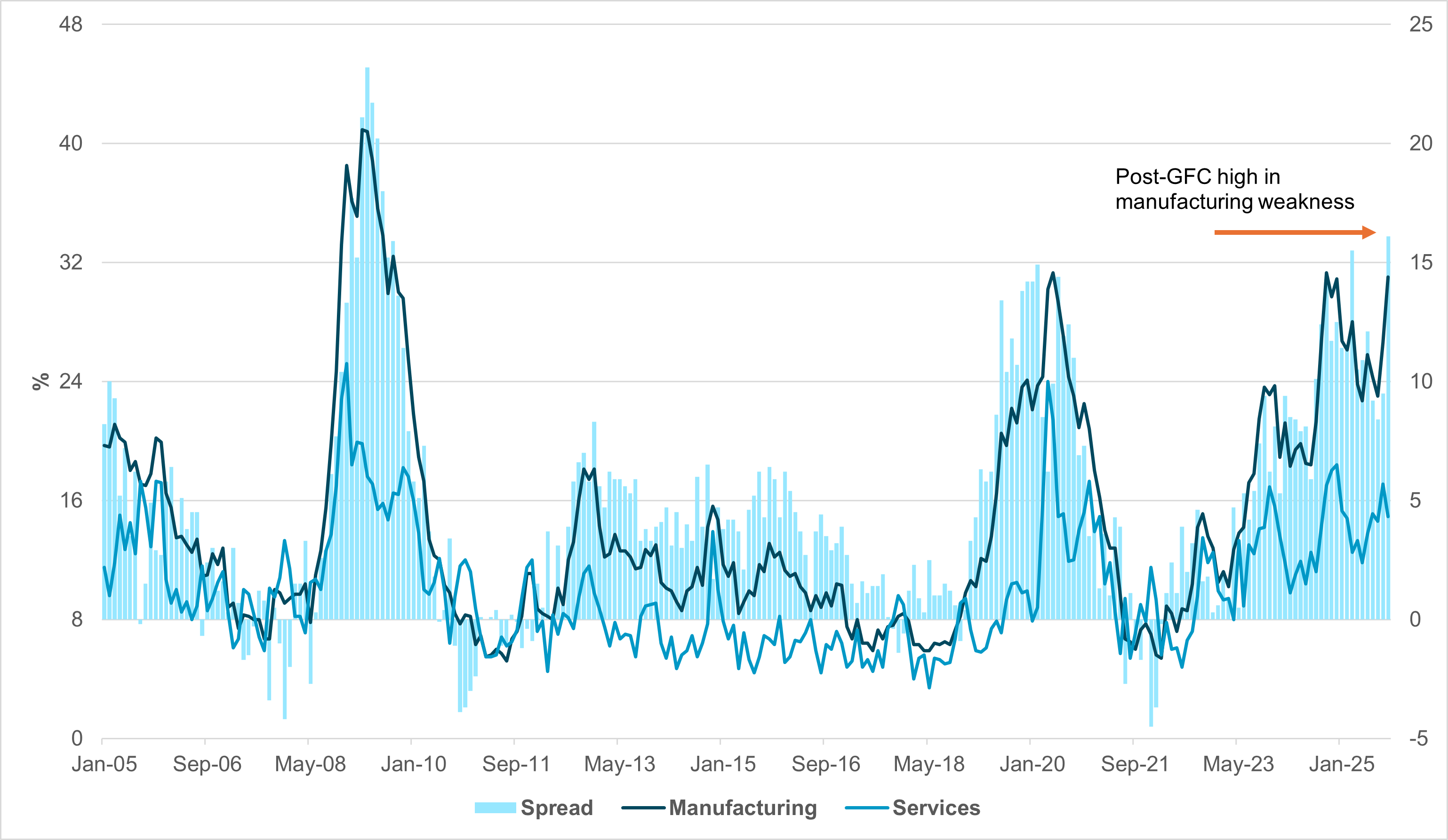

EMEA: Inflation in “a good place,” but not much else; U.K. earnings a key release for MPC

EXHIBIT #3: GERMAN IFO SURVEY, % OF RESPONDENTS EXPECTING LAYOFFS

Source: BNY

Our take: At the last policy meeting, European Central Bank (ECB) President Christine Lagarde highlighted the prospect of supply chain disruptions, particularly in the automotive industry, as one of the idiosyncratic factors for Eurozone growth, citing tensions with China. Seven months after the U.S. imposed “Liberation Day” tariffs and escalated tensions with the key trading partners, it may surprise markets that Sino–European Union (EU) trade relations are in a worse place. The past week brought some initial signs of progress in resolving an dispute over Dutch government controls on a Chinese-owned chip producer, but the episode also revealed some exposures in the Eurozone’s own supply chains. Rare earths are another area where European manufacturers must diversify input sources. But arguably the EU isn’t even part of the current conversation, especially as the U.S. turns to Australia, Central Asia and Latin America to boost its own resilience. The EU’s own capabilities are limited and unlikely to take priority over U.S. needs. As in the U.S., public sector funding will be needed to complement industry efforts to build resilience, but we doubt the EU will be able to match the U.S. in developing a common strategy, let alone deploying funds.

In the near term, manufacturing is unlikely to face fresh disruptions. However, without greater supply chain certainty, higher levels of investment may fall short, potentially worsening labor market conditions already indicated by recent surveys. Based on the latest PMIs and the German ifo Business Climate Index, the divergence between the manufacturing and services sectors is becoming extreme: Measured by the percentage of firms looking to reduce employment, the spread is now at the widest level since the global financial crisis (Exhibit #3). Even on an outright basis, deterioration in labor expectations among manufacturers could reach a post-global financial crisis high, while trends in services remain problematic. The ECB, lacking an employment mandate, may be reassured that such trends will continue to limit demand-based inflation. But from a real economy perspective, we believe the Eurozone, particularly its manufacturing sector, is heading towards a more troubling outlook.

Forward look: Final October Consumer Price Index (CPI) figures are the main releases across Europe this week, with few adjustments expected. Rate path guidance toward year-end is firm across Continental Europe, leaving the U.K. as the only major economy where the December decision remains on a knife edge. In our view, Governor Bailey is likely to cast a swing vote in favor of a December cut, unless wage and inflation data deliver significant upside surprises. The September U.K. labor market report is due this week, with the unemployment rate expected to tick up to 4.9%, the highest since early 2021. However, the rise in unemployment is unlikely to affect wage growth, which is seen holding at 5.0%. Public sector wage growth may even exceed 6%, underscoring the need for spending restraint, which remains conspicuously absent from current budget discussions. iFlow shows cross-border demand for gilts declining again, and we expect U.K. government paper to continue trading cautiously through month-end.

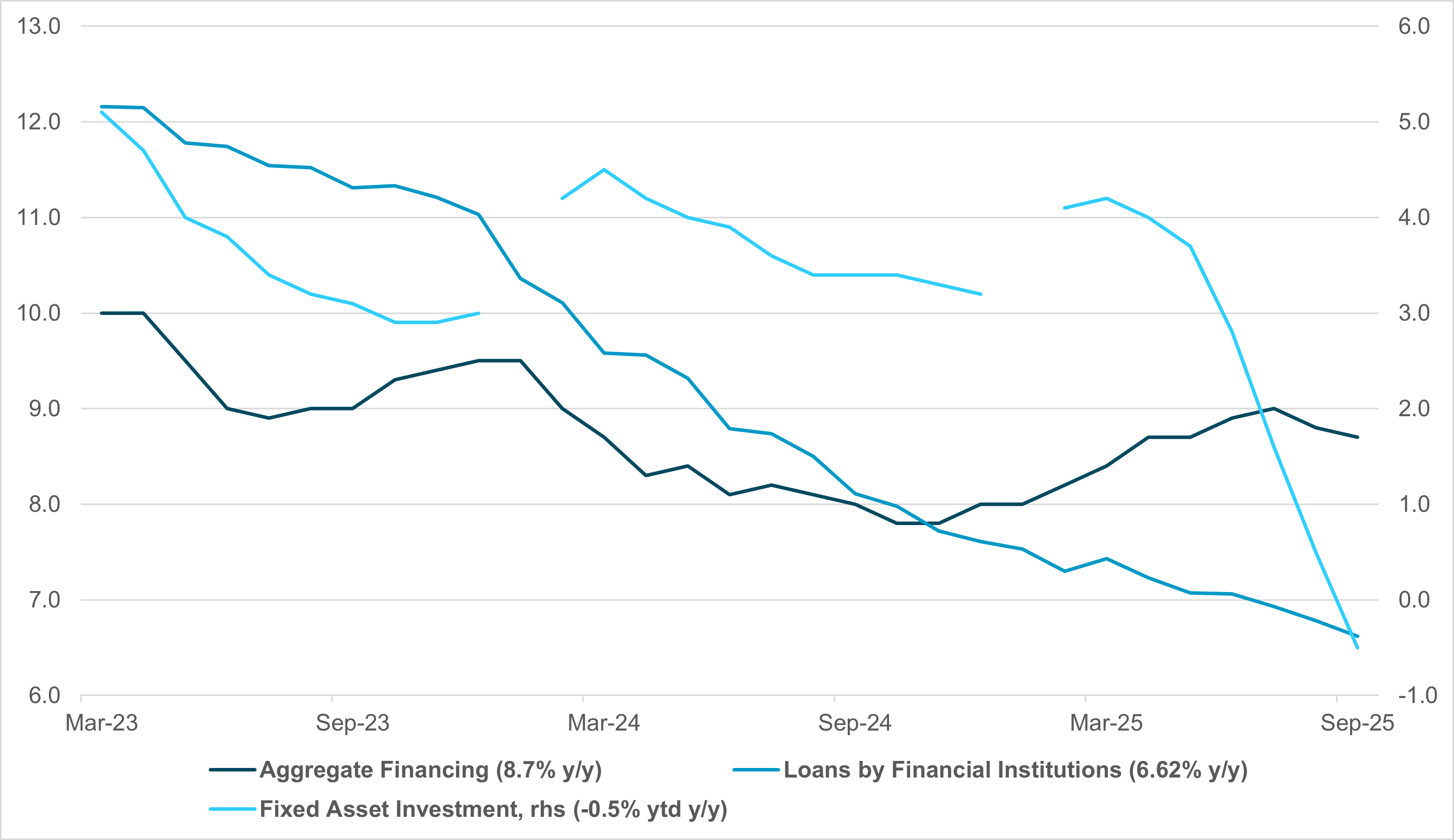

APAC: China credit, fixed asset investment, home prices and South Korea exports

EXHIBIT #4: CHINA CREDIT GROWTH, BANK LOANS AND FIXED ASSET INVESTMENT

Source: BNY, Bloomberg

Our take: In the Asia-Pacific (APAC) region, focus this week will be on China’s October credit, financing, activities and investment, and housing data. Additional highlights include South Korea October bank lending, jobs data, and the first 10 days of November exports; India’s October exports, trade and inflation data; consumer confidence from Thailand and Indonesia; and Malaysia’s Q3 GDP releases.

China’s October credit data will be closely scrutinized given the reversal in the growth trend of aggregate financing, which peaked in July at 9.0% y/y, before slowing to 8.7% y/y in September. The ongoing decline financial institution lending remains a gauge of domestic sentiment. September loans by financial institutions totaled ¥1292bn, marking a new low growth rate at 6.62% y/y. Domestic loans to households stood at ¥392bn (2.3% y/y), with short-term loans at ¥142bn — the first negative y/y rate at -0.5% — and medium- to long-term loans at ¥250bn (-3.28% y/y). China investment data showed little sign of recovery. China’s September fixed asset investment fell to -0.5% YTD y/y, marking the first YTD contraction since August 2020. Property investment at -13.9% YTD y/y approached the all-time low of -16.3% YTD y/y recorded in February 2020. One positive is the sustained growth in the high-tech sector, led by industrial robots (+29.8% YTD y/y), service robots (16.3% YTD y/y), new energy automobiles (29.7% YTD y/y) and integrated circuits (8.6% YTD y/y). Domestic consumption has slowed to 3.0% y/y, matching the pace of November 2024 but off the highs of 6.4% in May 2025. October housing data will be closely watched following the accelerated month-on-month declines in new and used home prices, at -0.41% m/m and -0.64% m/m, respectively.

South Korea’s October bank lending release will be a key financial stability indicator, with policymakers on high alert over excessive household borrowing and elevated home prices. Exports data for the first 10 days of November will be closely monitored for positive momentum following the Asia-Pacific Economic Cooperation (APEC) summit.

Malaysia’s Q3 GDP is likely to beat on the upside, with the recent positive run on data. India’s October CPI is expected to further decline (consensus: 0.4% vs. 1.54% in September), which could increase the likelihood of a Reserve Bank of India rate cut when it meets in early December. Elsewhere, inflation expectations are the key data in Australia and New Zealand, alongside Australia’s October labor market update.

On the monetary policy front, there is no regional central bank meeting this week. Bank Indonesia will convene the following week.

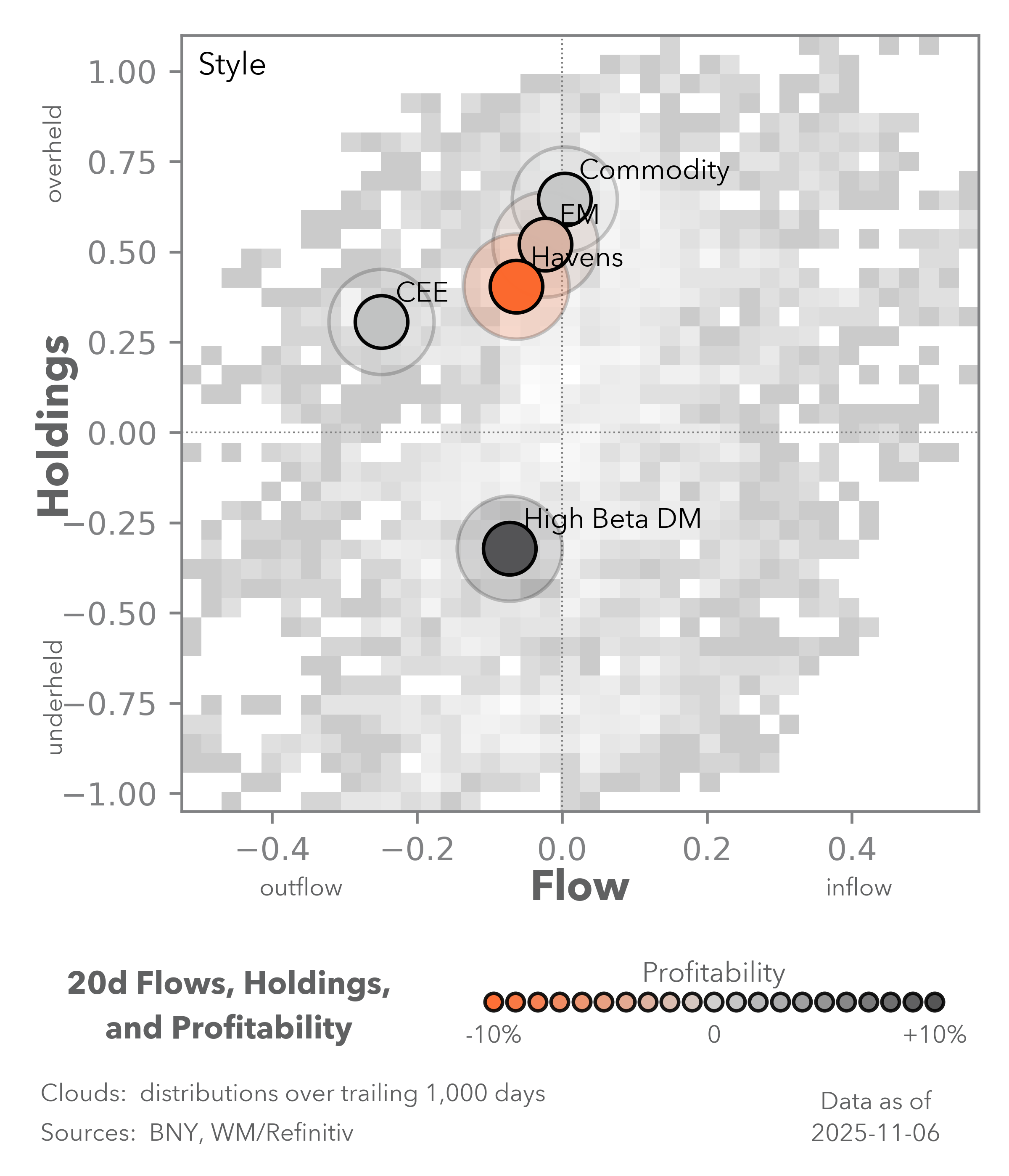

Forward look: APAC risk assets are navigating a challenging period, influenced by the renewed strength of the USD while markets reassess expectations for the U.S. federal funds rate, a sudden equities sell-off amid concerns over an AI bubble, and aggressive profit-taking by foreign investors. Korean assets bore the brunt of the sell-off with the KOSPI closing 5% lower week over week and KRW nearly 2% lower at 1,457. Meanwhile, Chinese domestic investors continue to demonstrate confidence in the equities market, as indicated by the ongoing increase in margin balances at stock exchanges, despite the deteriorating macroeconomic data. Notably, China’s October exports unexpectedly fell -1.1% y/y, marking the first decline since March 2020. The October manufacturing PMI dropped to 49.0, its lowest since April 2025. Although the potential for further profit-taking toward year-end remains, we maintain a constructive medium-term outlook on Asian risk assets and will continue to closely monitor shifts in investor sentiment.

Global markets enter the final stretch of 2025 under significant strain from policy uncertainty, fiscal stress, and weakening growth signals. The interplay between government shutdown risks, heavy Treasury issuance, and fading foreign demand for U.S. assets has created a fragile liquidity backdrop. Investors are increasingly questioning whether rising deficits could reignite inflation concerns, especially if fiscal policy crowds out private investment. Abroad, Europe’s manufacturing malaise, China’s slowing credit impulse, and currency pressures in emerging markets all point toward softer global demand into year-end. Nonetheless, selective opportunities remain. If the U.S. government reopens smoothly and the Fed signals readiness to stabilize liquidity, risk appetite could recover, particularly in quality growth and AI-linked productivity stories. Professional investors should remain cautious but agilely positioned for near-term volatility while seeking longer-term value in dislocations across rates, currencies and technology as 2026 policy frameworks come into view.

Central bank decisions

Central Reserve Bank of Peru (BCRP) on Thursday, Nov. 13: The BCRP has room to cut rates to 4.0% at its upcoming meeting, as inflation fell sequentially October. Narrowing the rate differential with the Fed is a challenge for most Latin American central banks. However, we believe Peru still has a strong real rate anchor for now, and domestic activity remains manageable. On a quarterly basis, Peruvian bonds have been among the strongest-performing markets in iFlow. Some profit-taking has emerged, suggesting that duration gains from anticipated BCRP easing have been front-loaded.

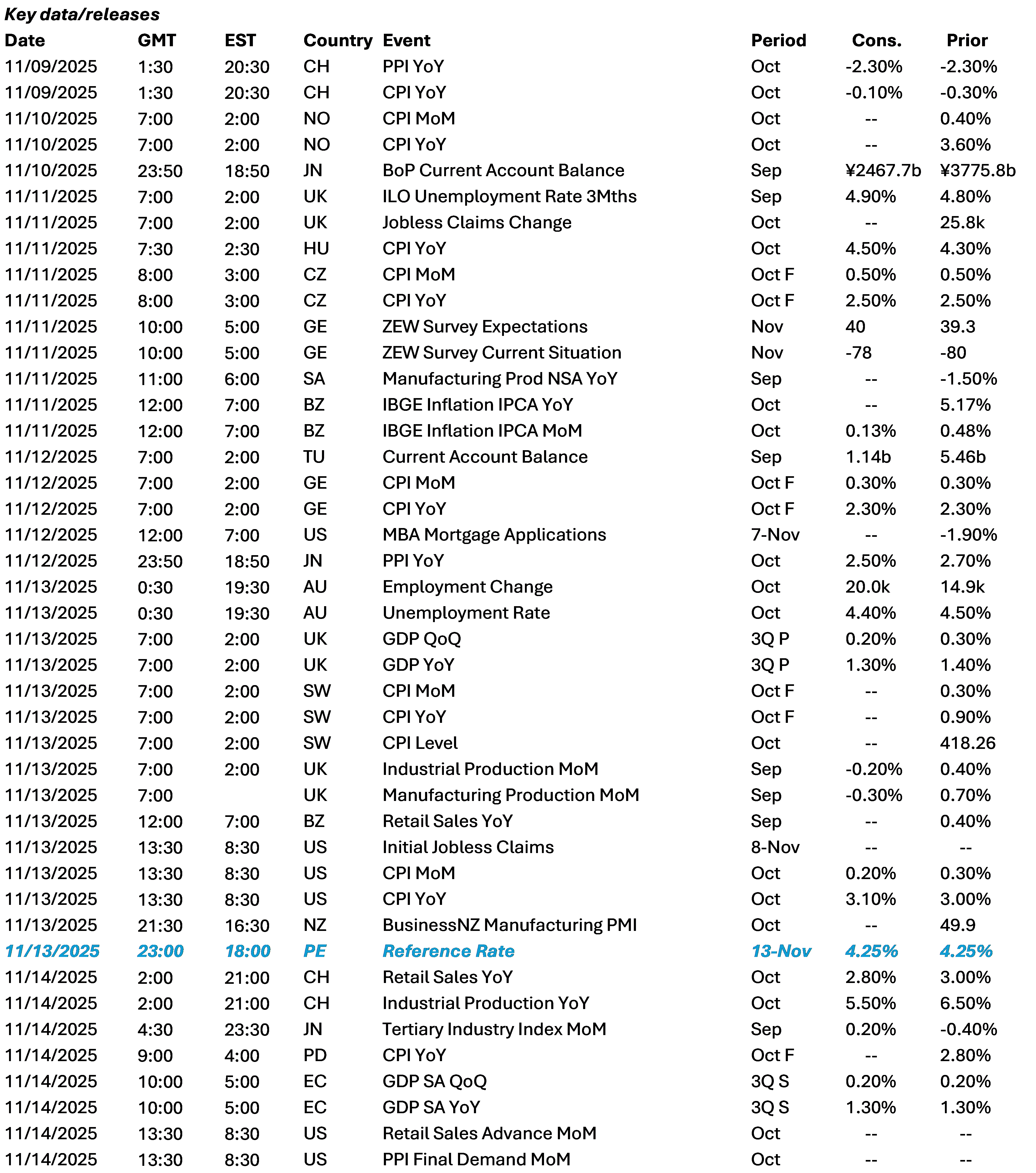

Data Calendar

Event Calendar