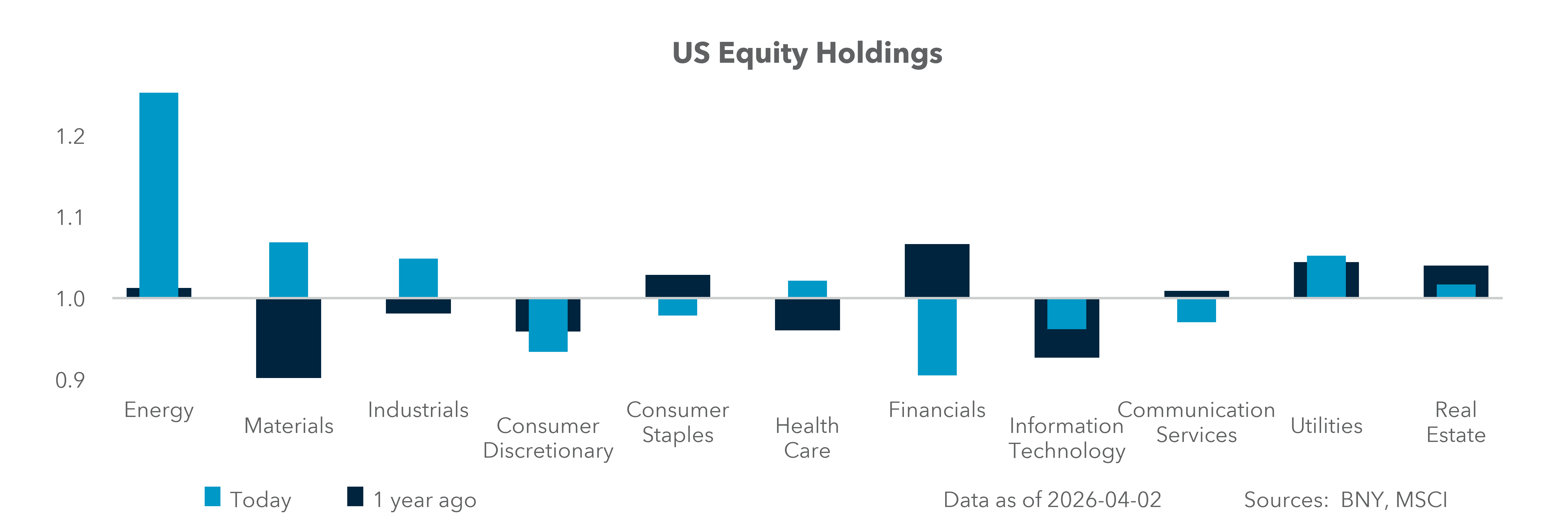

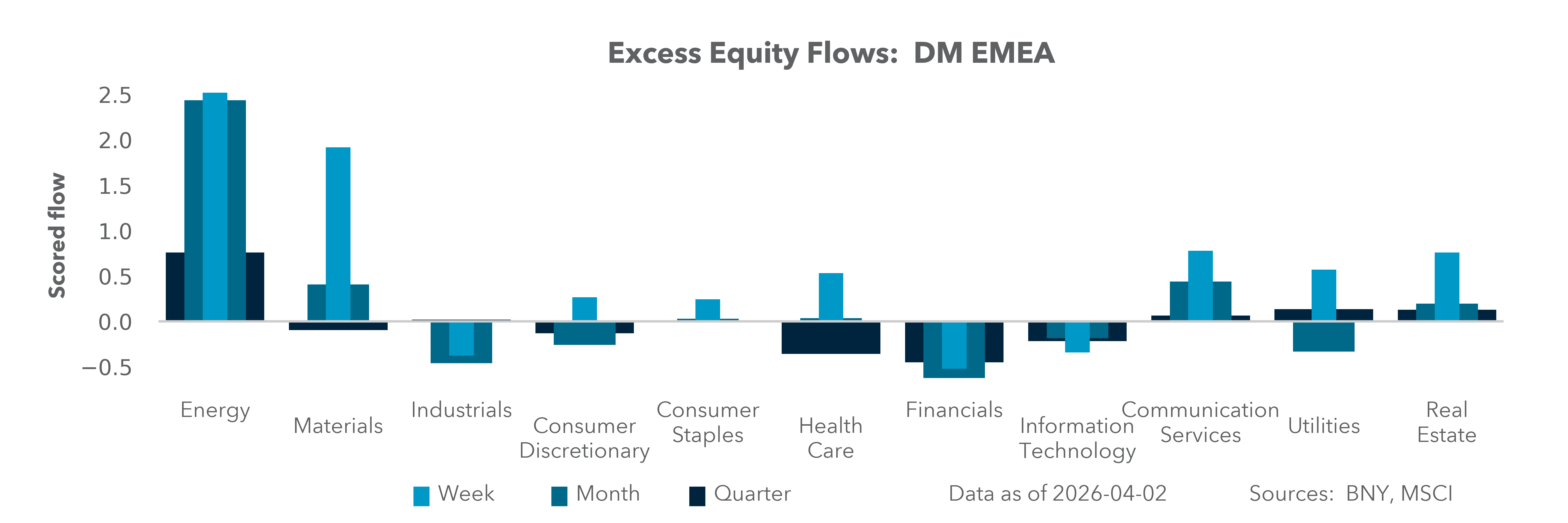

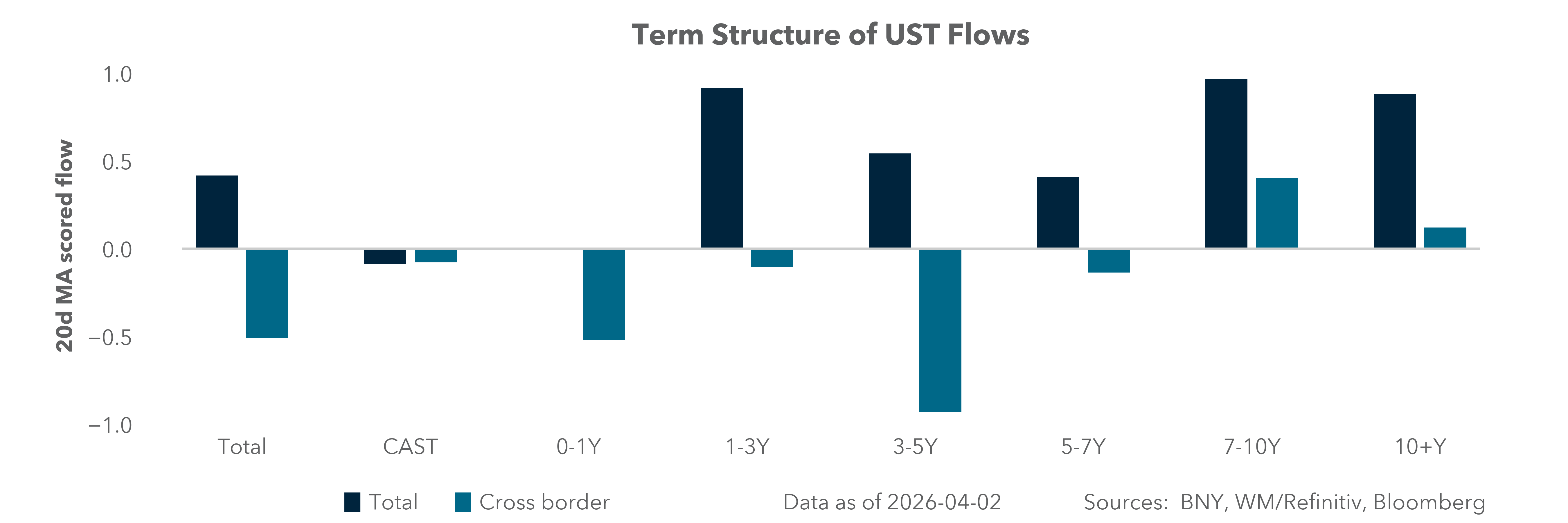

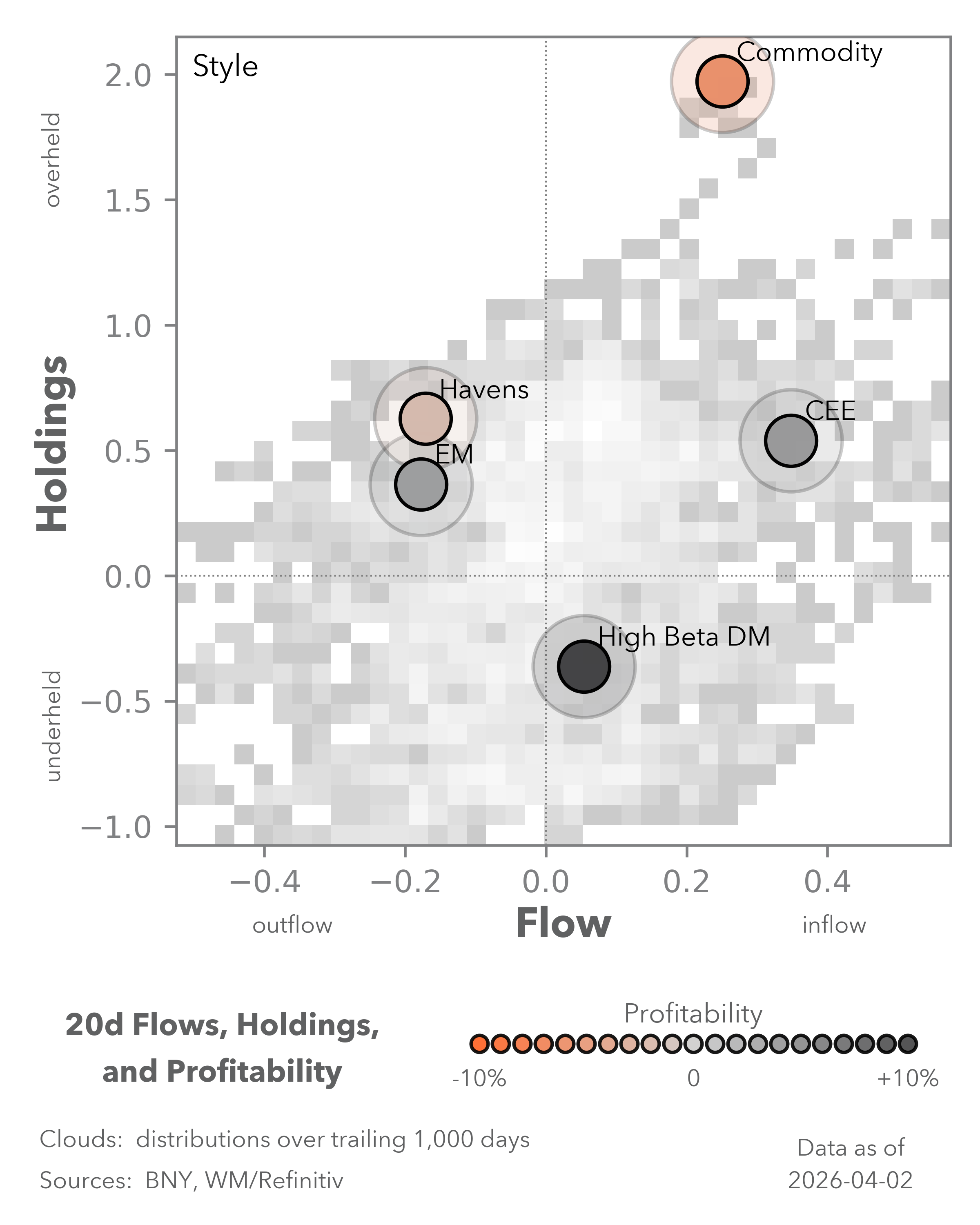

The great divergence

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 14 minutes

This week will be a holiday-shortened one but likely divergent in its effect across markets and regions. Investors will test whether April is the “cruelest month” or the season for renewed risk-taking. Despite “Liberation Day” volatility in 2025, they’ve seen positive equity returns in 11 of the last 15 years.

Many would like to think of the current conflict in the Middle East in the same vein. The war’s key effects on global markets have been the equity sell-down, a USD rally and higher rates. The performance of all assets correlates with energy prices, making volatility higher and headline reactions more dramatic.

Three key concerns dominated last week.

Economic data will matter to this list, with keen focus on U.S. CPI and the Fed policy response. Stagflation concerns globally will keep pressure on oil price reactions. The OPEC+ supply meeting will become a more significant market event.

This week is the last before Q1 earnings, making it the final window for confessional downgrades to corporate outlooks before the numbers hit. Q1 expectations did drop from December 31 but remain at 11.3% overall. Outlooks for Q2 will matter significantly more than Q1 results.

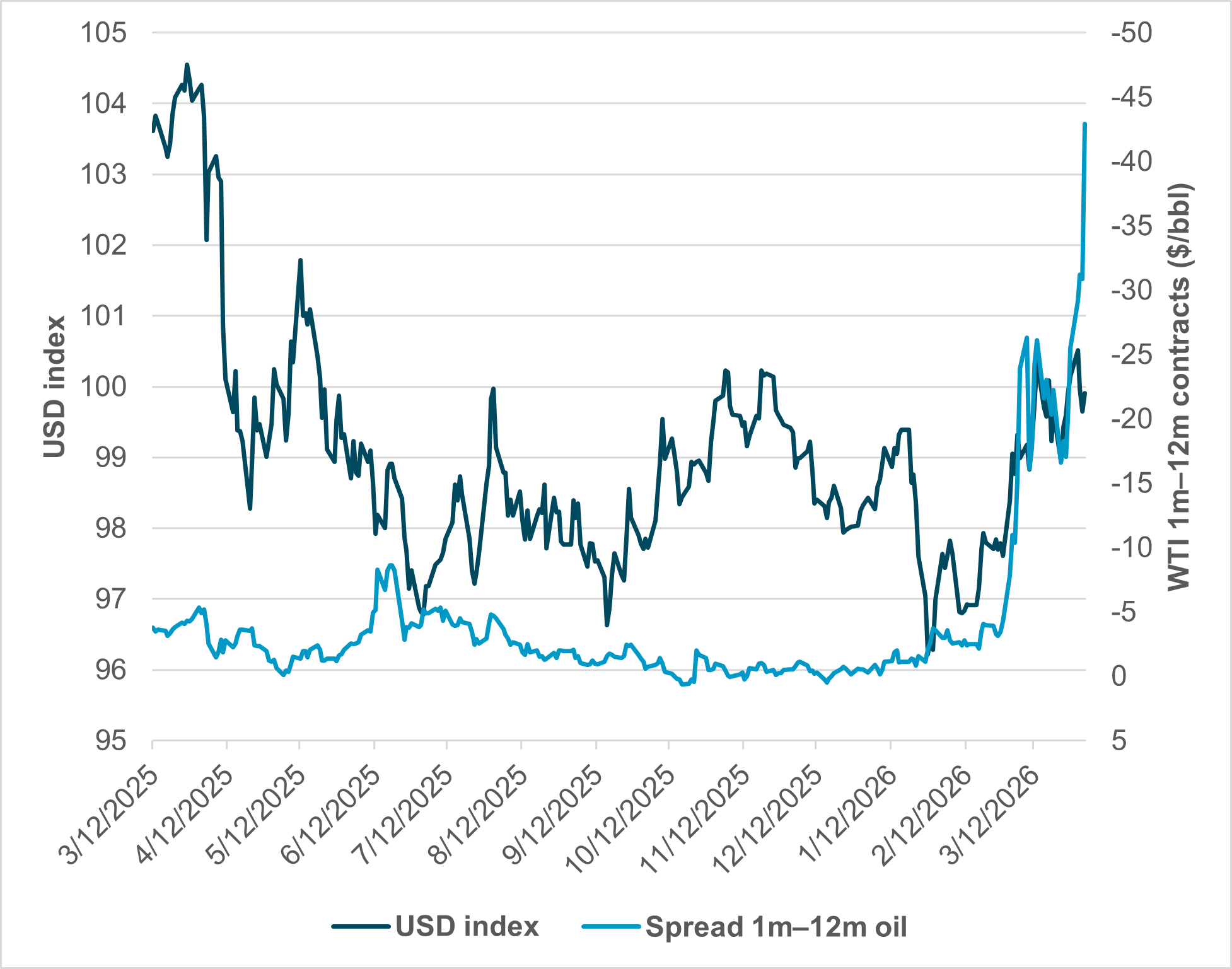

How much of USD rally comes from the oil shock?

EXHIBIT #1: U.S. WTI 1M–12M CONTRACTS VS. USD INDEX

Source: BNY, Bloomberg

Our take: Oil, or more importantly, the forward curve of oil, led the USD squeeze. The cost of physical goods is beating financial ones. Oil for delivery now touched $141.37 Brent this last week, while just one month forward it’s $109. The same is true for WTI as the world faces a supply shock.

The worry for investors is that skewed demand for oil and products moves all asset prices exponentially in April compared to March. A return to shipping by month-end is the alternative scenario and the binary risk for those being too pessimistic. A wait-and-see posture prevails for those managing VAR constraints.

Forward look: When we chart oil prices against the USD forward one year, we can see much of the dollar’s move was linked to oil shortages paid for in USD. If oil prices return to $60–$70, USD should logically decline.

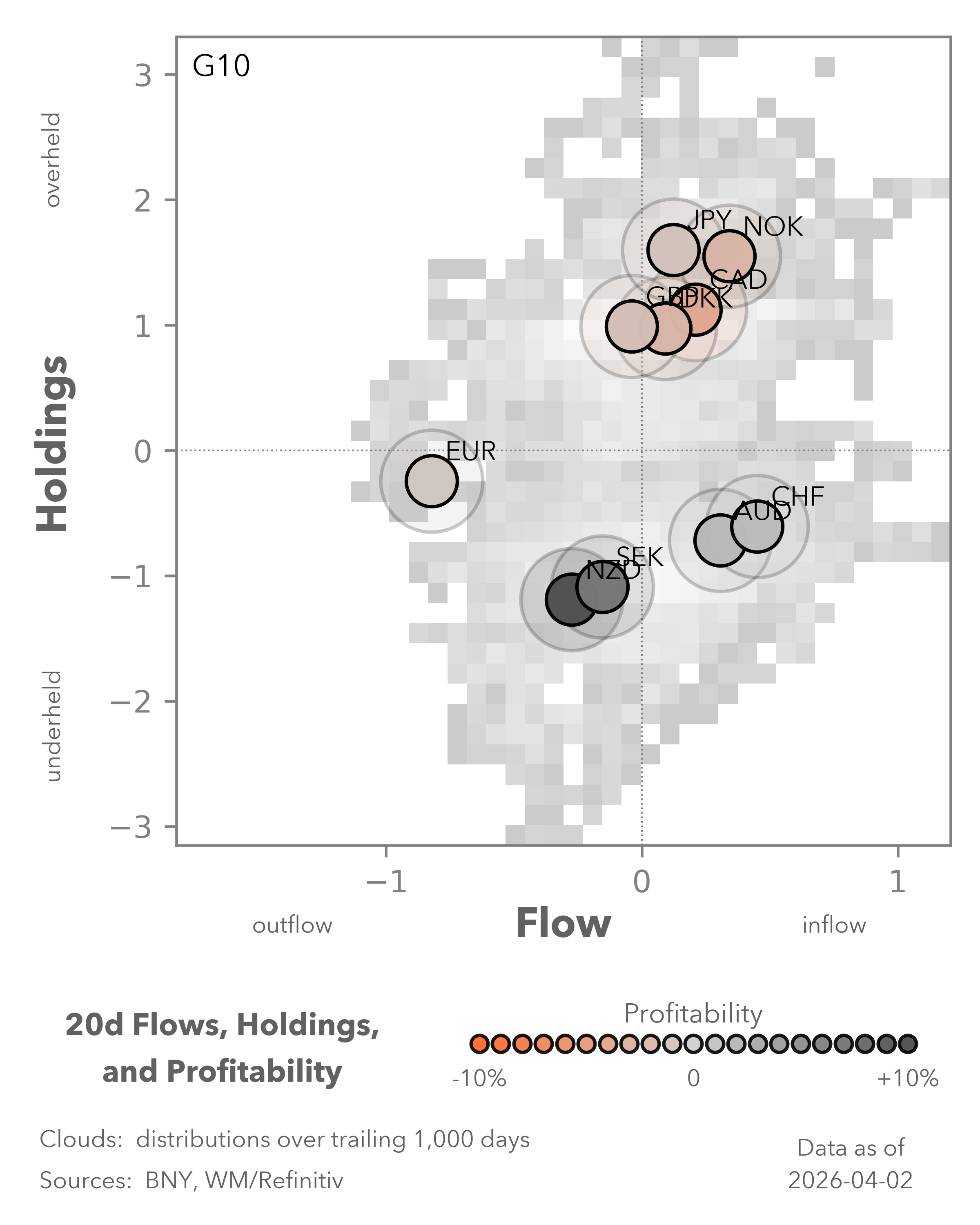

How central banks react to oil-linked inflation will be another consideration for the dollar in the months ahead as the Fed is more balanced in its mandates. Narrowing rate differentials will cap the dollar if the European Central Bank (ECB), Bank of Japan (BOJ) and others hike rates. There are further reasons that investors will hedge FX exposures amid this exponential rise in oil – expect them to view commodity-linked trades as safe-haven plays, though only once stagflation concerns ease and equity risk appetite returns. Until then, AUD, CAD and NOK could trade more to stock market stability than to oil price shifts, with the USD remaining dominant in a bear market.

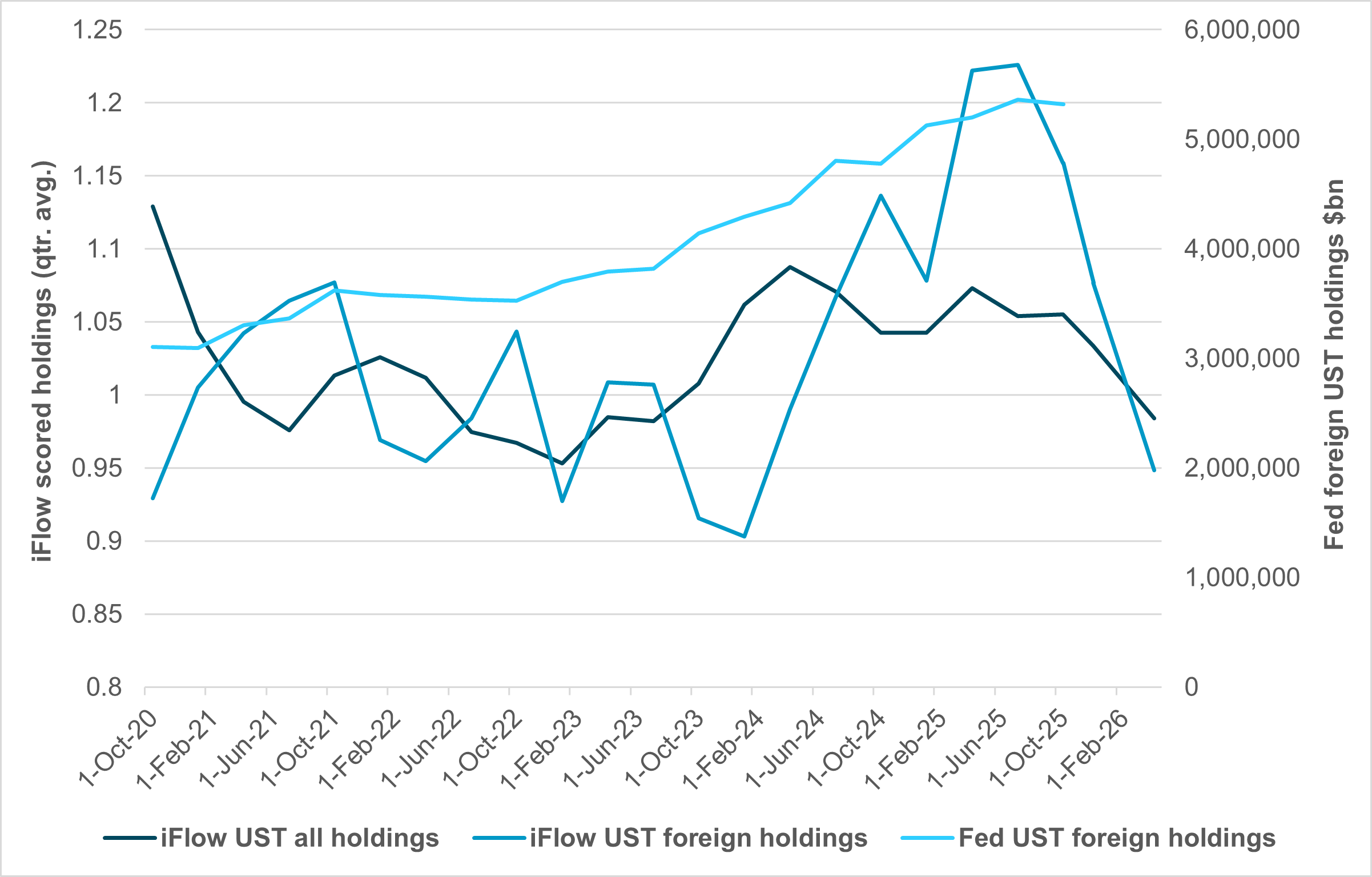

Are bonds no longer a safe haven?

EXHIBIT #2: U.S. BOND HOLDINGS IFLOW VS. FED DATA

Source: BNY, Federal Reserve Bank of St. Louis

Our take: While U.S. central bank holdings fell to 2012 levels on a weekly basis, holdings by asset managers, insurers and pension funds held steady. The war led to some bond selling, though more in the front end. Our data show that selling isn’t limited to foreign holders; it spans all investor types and represents a rethinking of bonds as a safe-haven tool in wartime. This obviously reflects the inflation fears and government offsets to fight energy shocks.

If we look at all bond holdings, the U.S. isn’t exceptional. Further, if we look at long -term average holdings across foreign and domestic investors, we’re not at 2012 lows – we’re near the long-run average. Trading bonds during the war so far is a front-end shock as inflation fears dominate the narrative.

Positioning against benchmarks is another factor for U.S. bonds, where their yields and decades of higher rates have kept foreign holdings elevated.

Forward look: U.S. government bonds do compete with corporate issues, and credit could become a factor again in how bonds trade globally. The focus on AI investments and investment-grade issuance is likely to matter if the fog of war lifts. Further, investors – particularly foreign ones – care about the easing cycle, and the Fed’s easing bias matters.

While markets price in rate hikes in Europe and some of Asia, that isn’t the case in the U.S. The relative trading volatility in the U.S. revolves around the curve more than a broader breakdown. The asset allocation pressure to own U.S. bonds remains significant, particularly when yields rise to 5%, as last week’s 20y and 30y moves demonstrated.

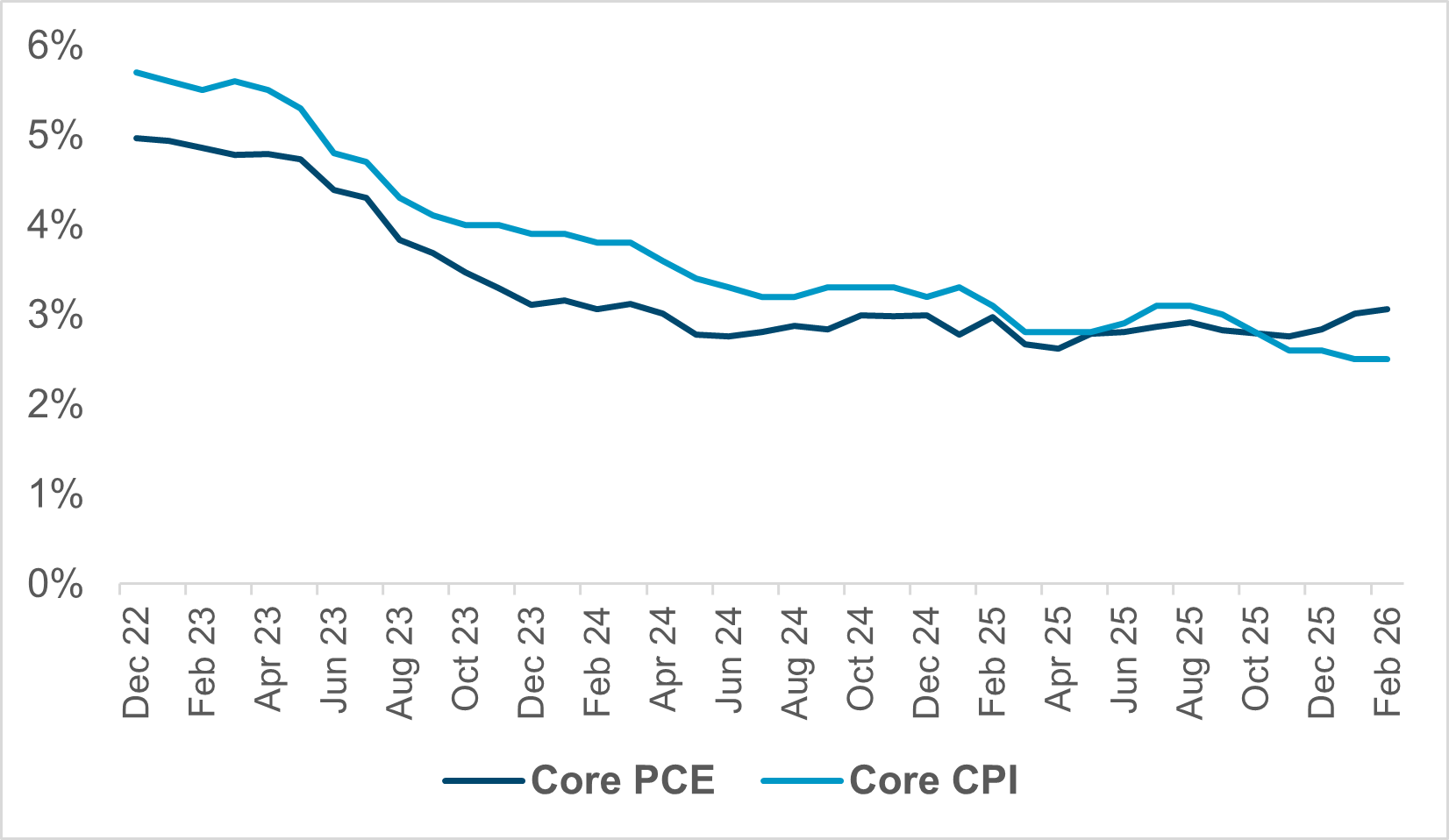

North America: CPI, Fed minutes and the Trump budget

EXHIBIT #3: U.S. CORE PCE AND CPI

Source: BNY, Bloomberg

Our take: Last week featured solid labor market data, capped off by a strong NFP print on Friday. This week, we’ll see if the strong data run can continue, as a variety of macro releases appear on the calendar – from inflation to factory orders and consumer sentiment to service sector confidence. With a light Fed speaker calendar, the week – which is likely to feature thin markets due to the spring holidays – will be focused on news flow regarding the conflict in the Middle East.

Forward look: PCE inflation for February (before the war) is out on Thursday, while March CPI comes on Friday. Inflation – even without incorporating war-related price effects – has been running hotter than desired lately, and the conflict promises to keep the price pressure robust. Markets are beginning to focus on the risks to growth (as much as to inflation) from demand destruction. We’ll get some important demand data as well, with the ISM services index on Monday, durable goods orders on Tuesday, and the Michigan consumer sentiment release on Friday.

Even though Fed officials will be mostly quiet next week, the minutes from the March meeting are published on Wednesday. We’ll be looking for information on the Fed’s view of the growth-inflation tradeoff given the war. We note that at the March press conference, Chair Jerome Powell acknowledged – on three separate occasions during his remarks – that when it comes to the expected rate path and economic outlook, “we just don’t know.” The minutes could reveal to what extent this uncertainty pervaded the Committee’s thinking.

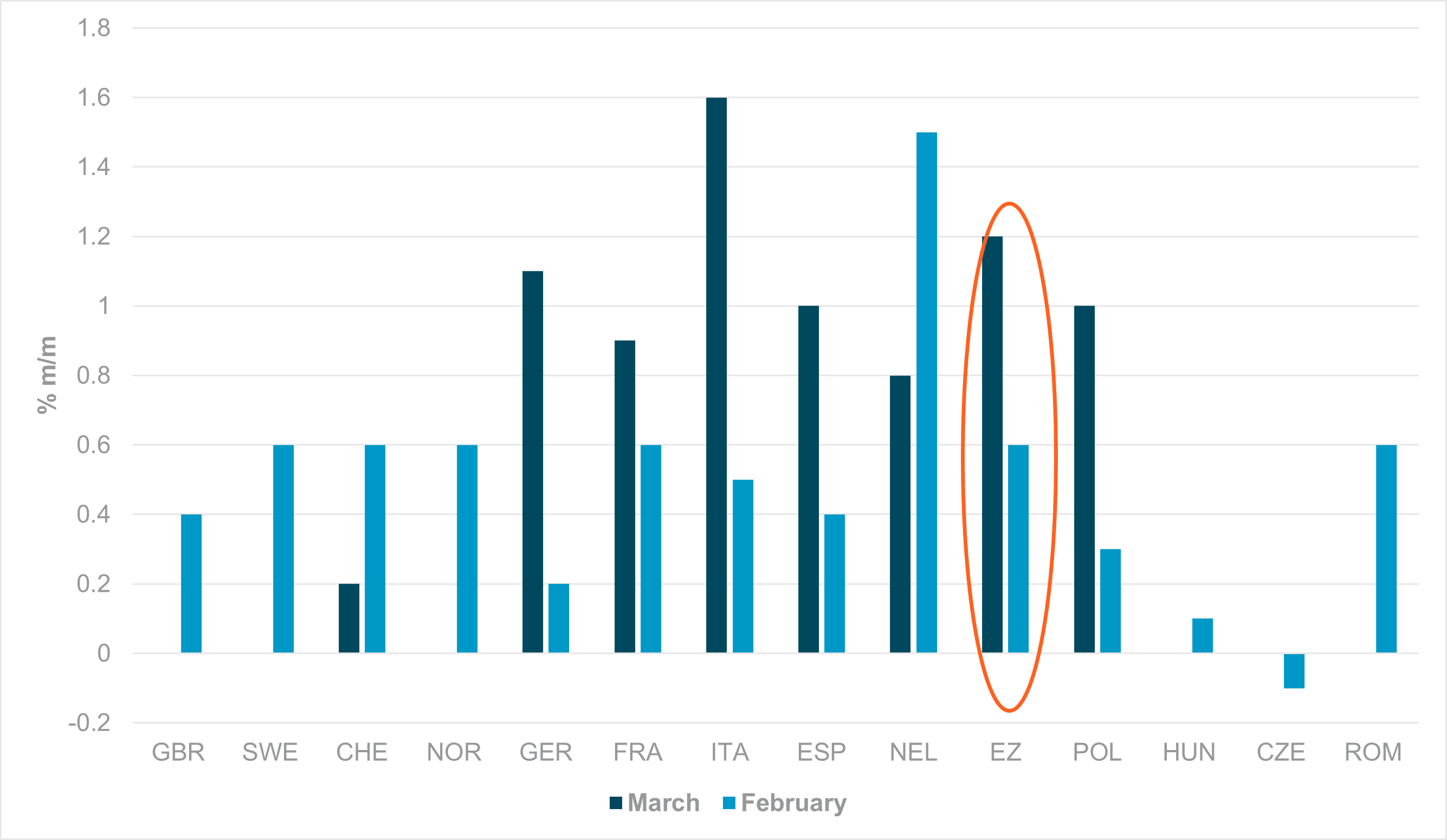

EMEA: Fiscal policy pushes back against inflation

EXHIBIT #4: EUROPEAN PRELIMINARY CPI: MARCH VS. FEBRUARY (M/M)

Source: BNY

Our take: The first round of preliminary March inflation numbers has arrived and the readings are unpleasant. Base effects clearly matter here, but across Europe central banks should be braced for 1% m/m gains in prices (Exhibit #4), driven by energy cost changes. Although crude prices appear to have found their peaks even in extreme escalatory scenarios, European governments have shifted attention to refined products – where outright supply shortages are the more pressing concern. European diesel prices have already surpassed $200/bbl – above 2022 levels – while EU diesel and jet fuel stocks at the end of 2025 averaged less than two months of supply.

Global supply exists, but there are widespread reports of U.S.-originating tankers turning south mid-Atlantic, as Asian governments can outbid their European peers. For this reason, the U.K. and EU are beginning to work on a framework for reopening the Strait of Hormuz, with some potential for alignment with proposals put forth by China and Pakistan. Yet, this is probably as far as transnational cooperation goes, and Europe in the meantime will remain a price-taker in markets, especially for refined products.

European governments have decided early that uncontrolled gains in fuel prices are not acceptable, and most central banks would likely welcome efforts to contain inflation expectations. Administrative measures such as capping distributor margins have been implemented, but the broader effort involves reducing excise taxes outright, or in the case of the U.K., delaying any planned hikes. Any other forms of support will be targeted. Beyond capping inflation, these measures will also help ensure demand does not fall off materially.

However, bond markets will be closely assessing fiscal credibility as a drop in fuel-related revenue will require offsets elsewhere. For example, fuel duty is not large as a share of total U.K. government receipts, but in absolute terms, the delay in the 5bp hike could cost over 10% of the £22bn fiscal headroom the Treasury has established, while total tax intake also faces significant downside risk.

Forward look: More inflation numbers for March will be released outside of the Eurozone over the coming weeks, giving central banks additional information to calibrate their response. For now, all upcoming decisions in the region are live but most are likely to remain non-committal due to the uncertainties surrounding prices and supplies. We continue to expect at most one hike from the ECB, Bank of England and Riksbank, while Norges Bank has already committed to one hike.

The Swiss inflation figures show that a strong currency is highly effective at generating disinflation and downward price pass-through, but not all European economies are in the position of Norway and Switzerland to lean into these flows. The only European central bank decision in the week ahead is in Poland, where there is a case for the Narodowy Bank Polski to even reverse the March cut. However, the consensus expects no change, as the real rate buffer remains relatively strong.

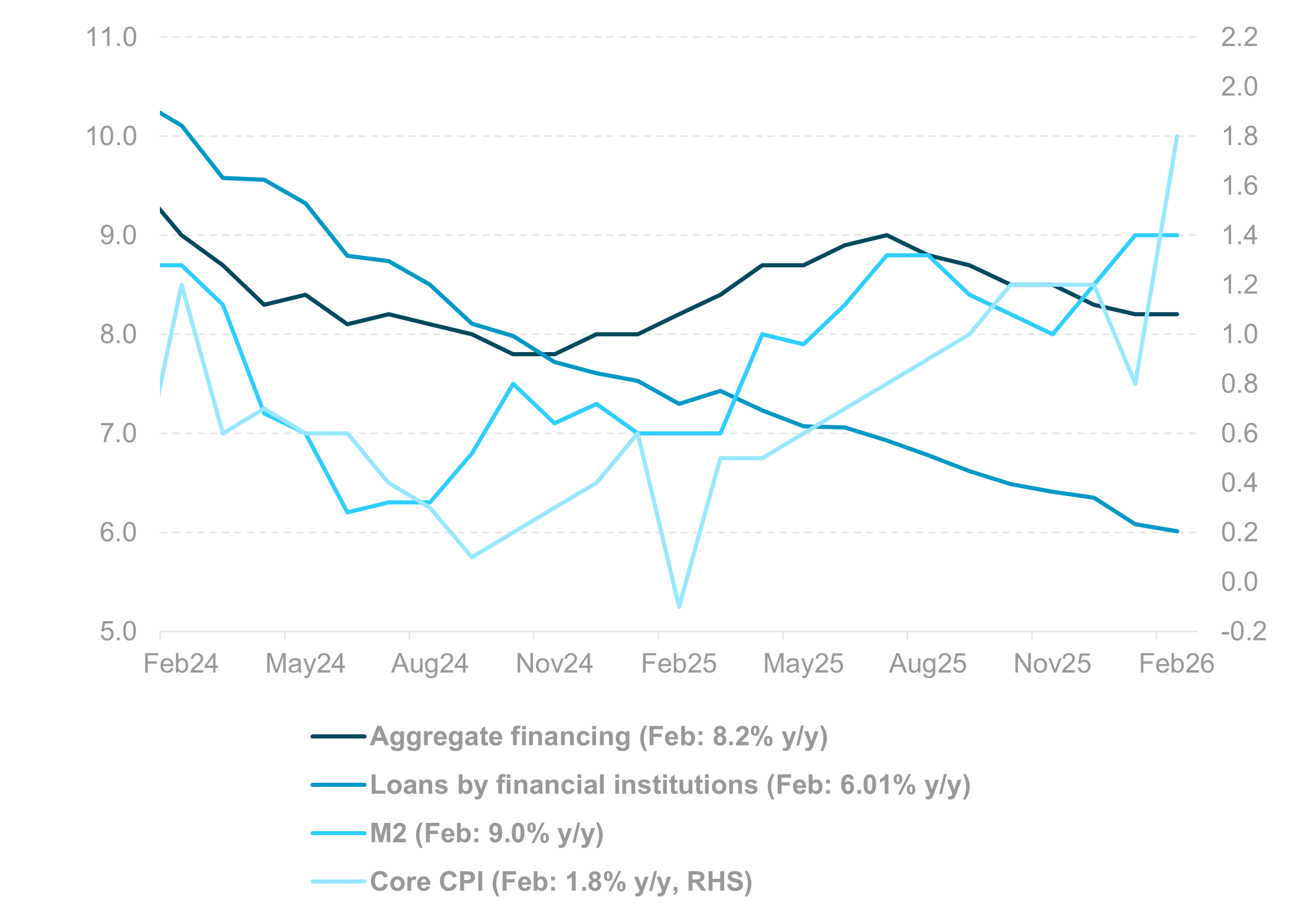

APAC: China credit, inflation, reserves and central bank decisions

EXHIBIT #5: CHINA CREDIT AND INFLATION PROFILE

Source: BNY

Our take: The focus this week centers on China’s March credit and inflation data (bank loans, aggregate financing, M2, CPI/PPI), key to assessing policy transmission and underlying demand. Regional inflation prints from Taiwan, Thailand, the Philippines and Australia will be closely watched for pass-through from elevated oil prices, while March foreign reserve data (Taiwan, Indonesia, Singapore and Malaysia) will gauge the scale of FX intervention.

Central bank meetings in South Korea, India and New Zealand are expected to deliver status quo decisions. Focus will be on policy bias – balancing upside inflation risks from oil against downside growth concerns – and any commentary on the Iran conflict.

ASEAN data are lighter but still relevant: Singapore’s Q1 GDP, PMI and retail sales will inform growth momentum and its central bank policy outlook, while Thailand’s and Indonesia’s March consumer confidence will underscore the conflict impact. In developed markets, Japan’s wage growth, PPI, household spending, and bank lending data will be key for assessing reflation sustainability and BOJ normalization, while Australia’s spending data will guide the Reserve Bank of Australia’s path.

Forward look: Sentiment remains fragile amid rising FX and equity volatility, driven primarily by geopolitical risks and elevated crude oil prices. Persistent foreign capital outflows are adding pressure to regional currencies and amplifying equity market swings. Notably, March saw record foreign net selling in South Korea, Taiwan, and India.

The Reserve Bank of India has responded with aggressive macroprudential measures to curb INR depreciation, including capping banks’ FX Net Open Positions and restricting onshore dealers from offering INR NDF contracts. These steps underscore growing urgency to safeguard financial stability before depreciation pressures become disorderly. Regionally, IDR, PHP, and KRW remain the most vulnerable, with currencies trading near all-time lows against the USD.

Rising hedging demand is evident in positioning data: iFlow scored holdings show IDR and INR have shifted from significantly overheld into underheld territory, while TWD remains deeply underheld. We advise caution in FX markets, as currencies may lag in any risk-on environment, with adverse terms-of-trade dynamics continuing to act as a drag.

The holiday‑shortened week will test liquidity and correlations as energy remains the central macro variable. Front‑loaded oil prices continue to tighten global financial conditions, elevating USD demand and keeping risk assets sensitive to headlines. Focus pivots to U.S. inflation prints (CPI) and Fed minutes for clues on growth vs. inflation trade-offs; any upside surprise risks extending the USD bid and pressuring equities and duration. OPEC+ signals and shipping developments around Hormuz are potential binary catalysts for oil curves and cross‑asset volatility.

In Europe, preliminary March inflation and fiscal adjustments argue for cautious rates guidance, with deficits and credibility driving bond differentiation.

In APAC, status quo decisions from BOK, RBI, and RBNZ are likely, but FX stability tools and reserve trends bear watching. Into Q1 earnings, guidance for Q2 will be more market‑relevant than reported results. Positioning should balance downside hedges, liquidity management, and selective commodity‑linked exposures until stagflation risks ease.

Central bank decisions

New Zealand, Reserve Bank of New Zealand (Wednesday, April 8): No change is expected from the RBNZ, but the market has shifted toward a more hawkish outlook, with close to 100bp being priced over the next four quarters. Given the uncertainties surrounding global growth, no central bank is in a position to pre-commit, and New Zealand will be in the category of countries which would worry more about a supply shock and its corresponding growth impact rather than immediate inflation risk. However, we acknowledge that positive terms-of-trade effects on New Zealand are limited, so price pressures are clearly to the upside.

India, Reserve Bank of India (Wednesday, April 8): We expect the RBI to remain on hold at 5.25% with a neutral bias. Policy focus is likely to stay on financial stability rather than reacting to oil-driven inflation. Rate hikes would be ineffective against supply-side pressures and INR depreciation, while further tightening financial conditions. Macroprudential measures remain the preferred tool. RBI had tightened FX rules, including a $100mn onshore position limit for banks effective April 10, 2026, and restricting onshore authorized dealers from trading non-deliverable INR.

Poland, Narodowy Bank Polski (Thursday, April 9): We remain of the view that the NBP’s rate cut in early March was not optimal. The war had already commenced at that point and supply risks were already clear, which was a sufficient reason to pause. The subsequent gains in general European rate expectations – even though we view them as extreme – would render any commitment to a dovish path as policy error, at least for the next quarter. Fiscal impulse should also require a monetary offset, so the near-term bias must shift decisively.

Peru, Banco Central de Reserva del Perú (Thursday, April 9): Out of all the Latin American currencies we track, PEN has struggled the most, whereas the rest of the region is even seeing some positive terms-of-trade adjustments from the current conflict. Peru’s commodity exposure is linked to silver, which has been struggling, while underlying rates also provide less of a buffer. While relatively removed from the conflict, Peru may prove more sensitive to balance of payments concerns and this would require a more forceful response from the BCRP, though the leap from managing expectations toward tightening remains large, but should not be discounted given the surge in March inflation – the biggest monthly jump in over three decades at 2.38% m/m.

South Korea, Bank of Korea (Friday, April 10):The BOK is expected to keep rates unchanged at 2.50%, maintaining a neutral stance with financial stability as the near-term priority. Policy focus is likely to tilt toward financial and FX stability, particularly amid elevated oil prices and supply disruptions linked to the Strait of Hormuz. Authorities are coordinating on energy and supply risks, while macroprudential tightening continues, including a 1.5% cap on household debt growth to curb housing-related leverage. The April meeting also marks Governor Rhee’s final policy meeting.

Source: BNY

Source: BNY