Risk, rates and rotation drive 2026

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

Investors closely watch the first week of the new year for signals on how the full year will trade. Trends from the holiday weeks continued into January: strength in emerging markets and carry trades, AI and technology investments, tightening spreads in credit, and steady demand for commodities – from gold and silver to copper and oil. Surprise U.S. actions in Venezuela added another twist, though political and geopolitical developments appear less concerning to investors than anticipated.

The focus this week will shift to the Supreme Court ruling on tariffs, ongoing protests in Iran and rising election risks from Thailand to Hungary.

Expectations for a fourth consecutive year of stock gains are rising, supported by a positive, though volatile, start to the year. This week will test investor sentiment as Q4 earnings begin, with banks leading and financials primed to benefit from a rotation out of technology.

A surprising development in bonds has been the lack of volatility, despite significant shifts in growth expectations. The U.S. labor market has shown limited job creation but remains tight, with unemployment at 4.4% in December. Expectations for just two rate cuts from the FOMC dominate. However, supply was met with strong demand, as over $90bn in investment-grade issuance traded better on the secondary market. This week, coupon supply will test investor optimism about rate stability.

The USD rally has regained momentum. A technical breakout in the dollar index above 99.0 reflects surprising weakness in the JPY and EUR, with shifting Fed views and U.S. growth just part of the explanation. The Bank of Japan is expected to hold rates steady at its January 23 meeting, while political risk is rising as Prime Minister Sanae Takaichi considers dissolving parliament to secure a mandate for her new budget. The 158 JPY level is seen as the intervention threshold for Japan’s Ministry of Finance. In Europe, Russia’s war in Ukraine, emerging tensions over Greenland, and mixed economic data – marked by lower growth and slowing inflation – have reignited concerns about renewed European Central Bank (ECB) policy responses. Interestingly, the CNY was up for the fourth straight week, as were gold and silver, suggesting a more barbelled approach to currency risk.

Volatility has remained surprisingly low since the April “liberation day” across markets. The divergence in 2026 will be important to watch, as the MOVE index remains 30% below early 2025 levels, while FX CVIX is down 25%, and the equity VIX is just 15% lower. Clearly, investors are sanguine about FX and bonds, which could shift, given a news agenda ranging from U.S. CPI and China trade to ongoing political and geopolitical risks.

Is the USD going to hold its bid?

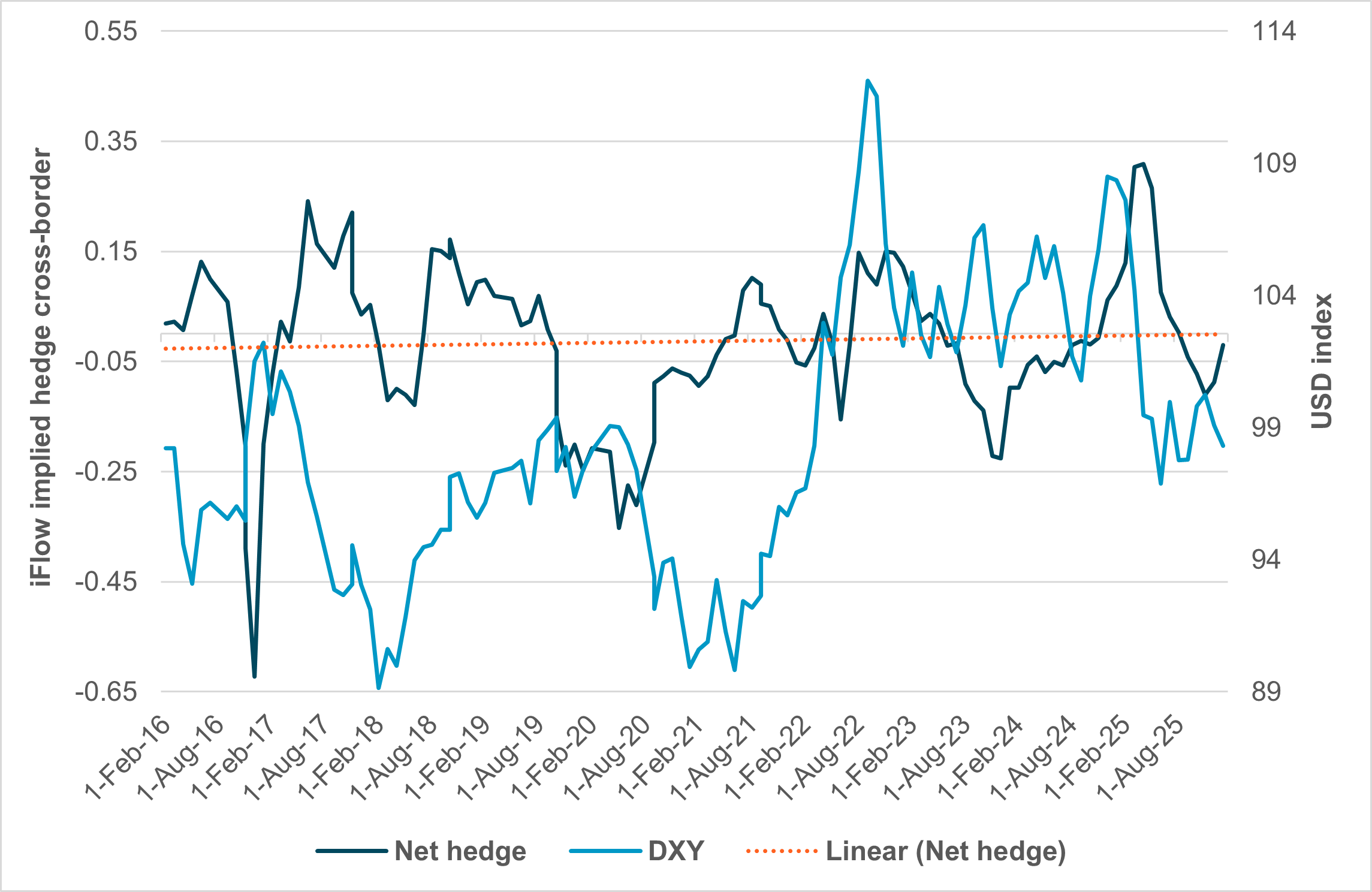

EXHIBIT #1: PROPENSITY TO HEDGE HAS INCREASED SINCE NOVEMBER

Source: BNY

Our take: Rising U.S. exceptionalism remains a dominant theme in markets as 2026 begins, echoing 2025. Strong U.S. Q3 growth, modest Q4 softness despite the government shutdown, investor appetite for corporate debt, and global AI progress have prompted foreign investors to reconsider home bias and global allocations. The U.S. and China remain the two least-held equity markets. However, the propensity to hedge both USD and CNY remains a key factor in 2026 market performance.

Recent gains in both Chinese and U.S. equities and currencies suggest investors are reweighting portfolios toward stocks and corporate debt, often without new hedging. Since November, we’ve seen a sharper increase in hedging interests for U.S. holdings from cross-border investors – a trend that may pause as the new year begins.

Forward look: The USD’s role in portfolio allocation was clear in 2025, as investors in Europe and AI tech-focused countries like South Korea and Taiwan outperformed without a hedge. Early 2026 looks similar to 2025, with all the same ingredients for more volatility. Bonds remain a critical part of risk sentiment, with the 10y yield at 4.20% now a breakout zone to watch this week.

Financial conditions support the view that the Fed holding rates steady will have little impact in January or even March. USD hedging may pause if expectations for rate cuts shift further. Policy tweaks in the U.S. housing sector may play an important role in shaping correlations between bonds, stocks and the dollar. These shifts could also influence how U.S. investors allocate abroad into the second half of January.

U.S. data focus shifts to prices as tariff noise lingers

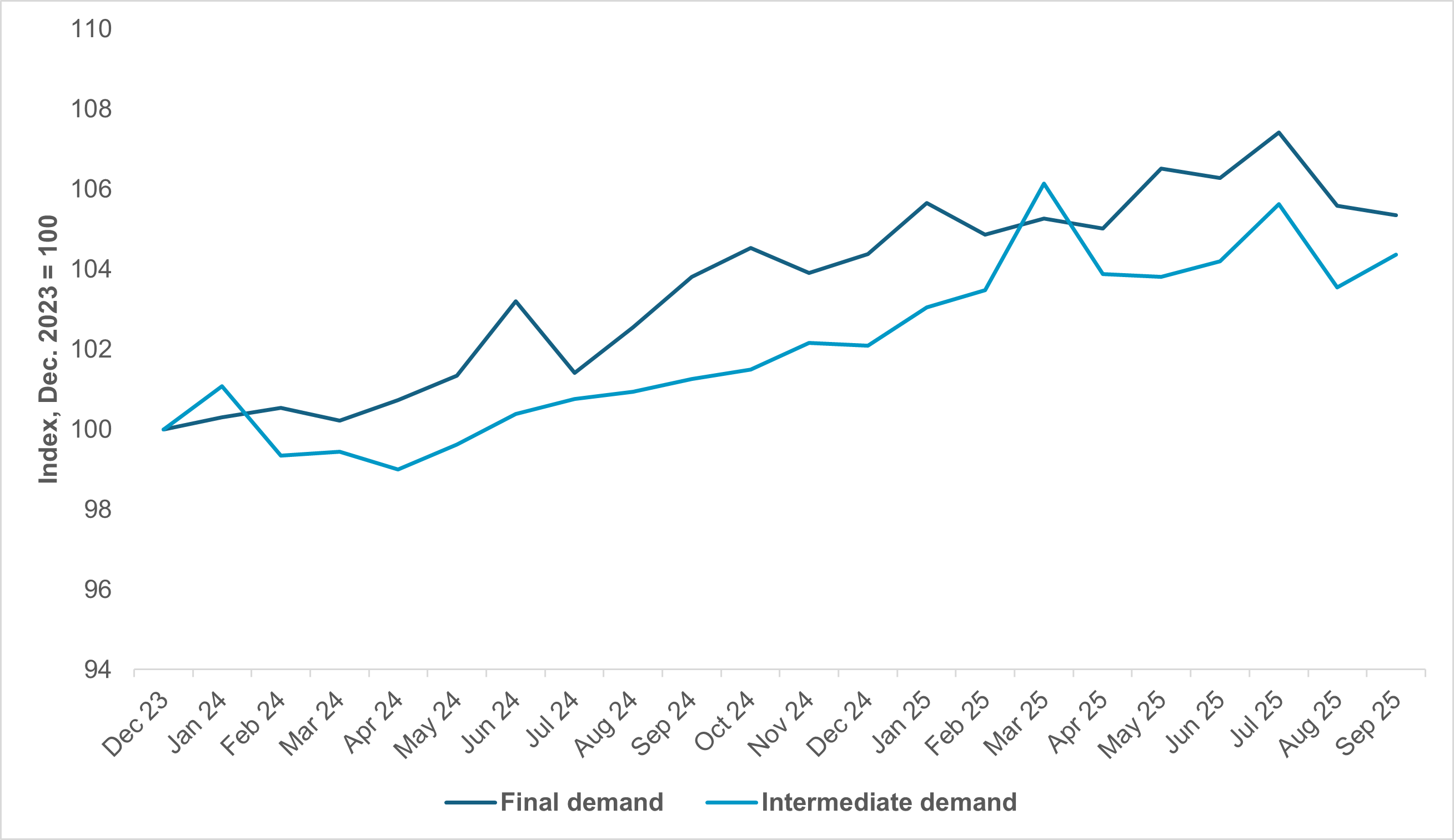

EXHIBIT #2: U.S. PPI TRADE SERVICES

Source: BNY, Bloomberg

Our take: With the first week of the year in the rearview mirror, the economic data focus shifts from the labor market – where several releases received mixed results – to prices. The consumer price index is due Tuesday, followed by producer prices the next day. Tariff effects have been modest so far, with core goods prices in the CPI basket up 1.5% in the 12 months ending November, following a prolonged period of modest price declines. Goods represent around one-third of the aggregate index.

The real stickiness in inflation is observed in non-housing-related services, which are up 3.5%. It remains unclear whether inflation data will continue to reflect tariff-induced cost pressures, as inflation pass-through from higher customs duties typically takes as much as a full year to peak.

Forward look: Much of the tariff hit has been absorbed by U.S. producers. The PPI offers a useful – if obscure – measure of margin growth: the so-called trade services subindex. This index has fallen from its peak a few months ago, suggesting that firms are not fully passing price increases on to end users.

Other notable data release this week include retail sales – important for gauging consumer demand – along with the New York Fed’s Empire Manufacturing PMI and industrial production. Fedspeakers on the schedule include New York’s John Williams and Minneapolis’s Neel Kashkari, both voting members on the 2026 FOMC.

The most important event of the week, aside from inflation data, is the Fed’s Beige Book, due Wednesday afternoon. Fed Chair Jerome Powell pays close attention to this qualitative survey of business contacts across Fed regions to assess how Main Street is faring.

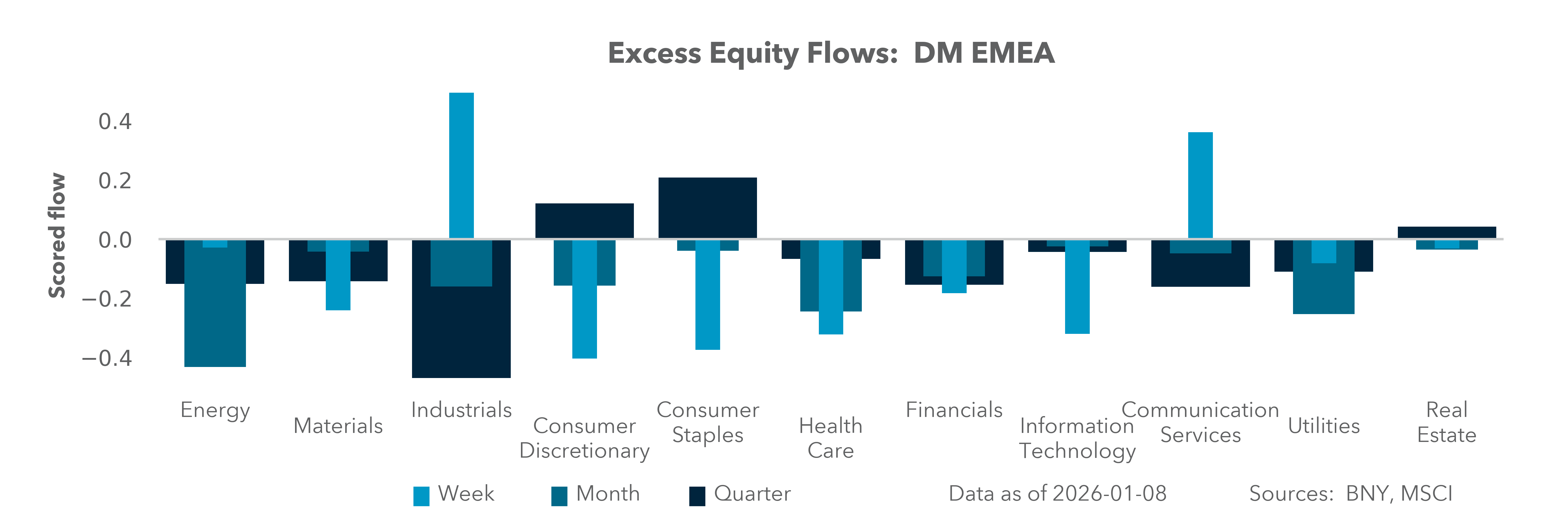

EMEA: Geopolitical stress underscores the need to accelerate fiscal pushs

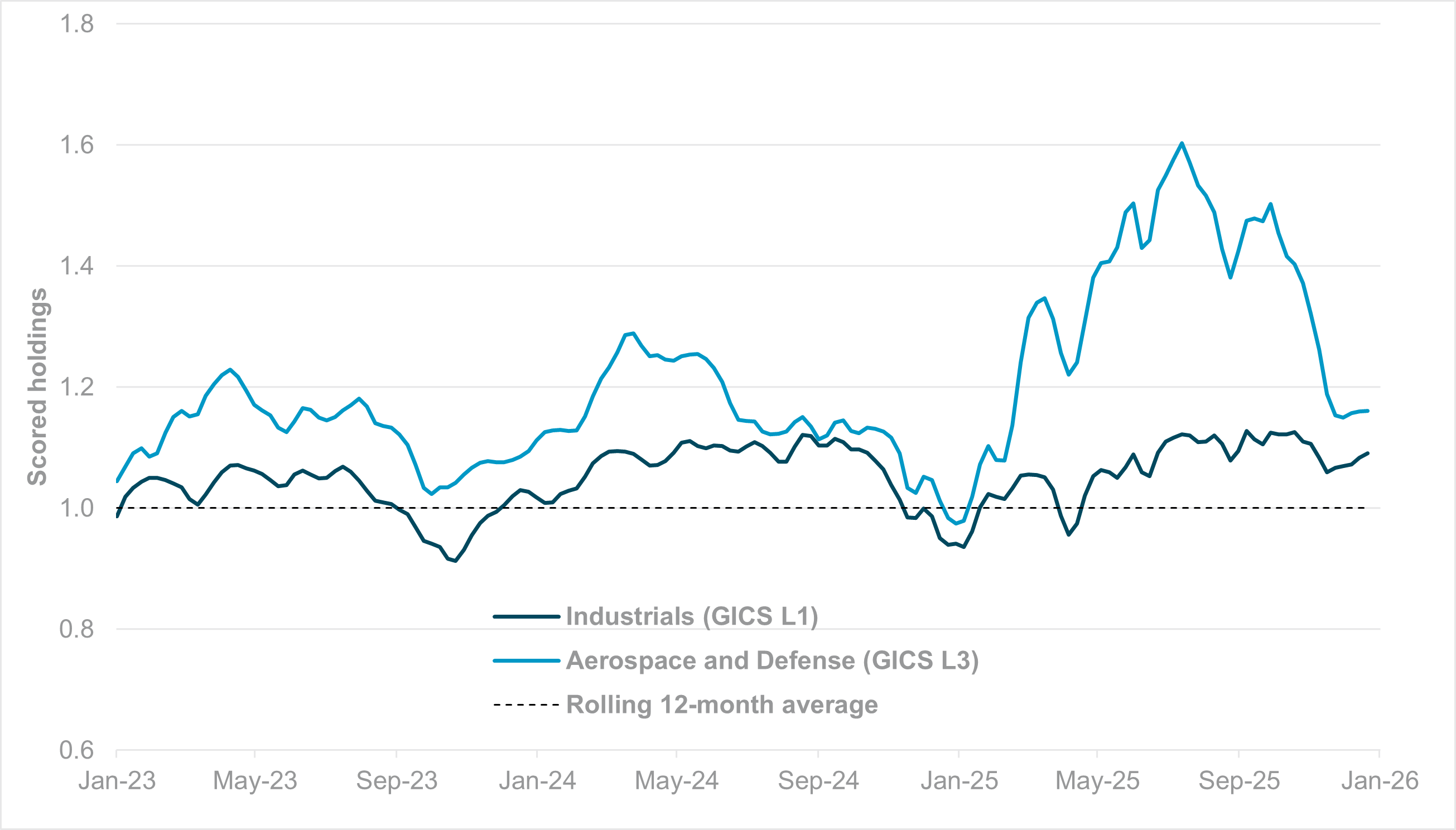

EXHIBIT #3: SCORED HOLDINGS – DEVELOPED EUROPE AEROSPACE AND DEFENSE (GICS LEVEL 3) VS. INDUSTRIALS (GICS LEVEL 1)

Source: BNY

Our take: Europe starts 2026 facing the same geopolitical challenges – managing the war in Ukraine and navigating relations with the U.S. The Trump administration has indicated that talks over Greenland’s future will take place in the week ahead. But beyond the headlines, we expect behind-the-scenes diplomacy to prevail, given the practical constraints that limit more dramatic action. German Foreign Minister Johann Wadephul’s meeting with U.S. Secretary of State Marco Rubio on Monday will be a key indicator of how transatlantic relations may evolve in the near term.

Even so, recent developments have underscored the need for Europe to accelerate plans toward strategic autonomy. Still, markets remain cautious about the prospects for sustained fiscal impulse into defense. Our data show that after a surge in Q2 2025 – which led European defense to become one of the best-bought and best-held industries (GICS level 3) globally – the “premium” versus the broader European industrial sector has largely closed. Still, in absolute terms, overall holdings remain relatively high, at around 20% above the rolling 12-month average.

The trajectory is more concerning than the convergence itself. Following last year’s seismic shift in Europe’s defense outlook – led by Germany’s adjustment to its constitutional debt break – many hoped for a fiscal injection with productivity multipliers for industry, especially in infrastructure improvements and sectors aligned with the Draghi Report on European competitiveness. However, equity holdings suggest no rerating is in store for industrial firms. Defense is now reverting to the broader European industrial norm – a weak position, given the current outlook from the latest PMI survey.

Year-end data continue to point to a mixed picture. Industrial production showed robust expansion, but the export outlook is deteriorating, and Europe has yet to focus on trade relations with China, which we still expect to be a major flashpoint this year.

Europe began the year with strong bond issuance results, indicating loose financial conditions and robust duration demand. This is not surprising, given that key economies such as France and Italy still have inflation well below target – a dynamic that may limit hawkish voices within the ECB. However, funding must be deployed quickly, as results are now expected after a year of competitiveness pledges and against an increasingly febrile geopolitical and trade backdrop.

Forward look: On the policy front, the speech calendar remains sparse. Key ECB officials are expected to reserve their first comments of the year for Davos, while the National Bank of Poland (NBP) is the only central bank decision of the week in the region. In contrast to the Eurozone, we see a much greater need for a hawkish pivot in Central and Eastern Europe (CEE) driven by stronger fiscal impulse and structural labor market constraints. There are domestic constraints to that effect, and any dovish surprise will challenge the region’s rich currency valuations. A weaker currency, and the resulting inflation pass-through, may be required to force a policy shift.

The U.K. will release core activity data, though the figures still pertain to November, and it remains to be seen how the reaction to the budget is playing out in the real economy. The Bank of England’s December decision indicated insufficient downside inflation risk to justify further rate cuts being priced in.

Nonetheless, GBP faces challenges on other fronts. Reports suggest fiscal strain is re-emerging as defense funding gaps widen, while upcoming changes to business rates for parts of the hospitality industry could prompt broader calls for relief and fiscal slippage. Following a surge in domestic purchases of gilts after the budget, positioning challenges are rising. A weaker sterling may be needed to attract international buyers back to the gilt market.

APAC: China and regional trade, Australian inflation, India CPI and BoK

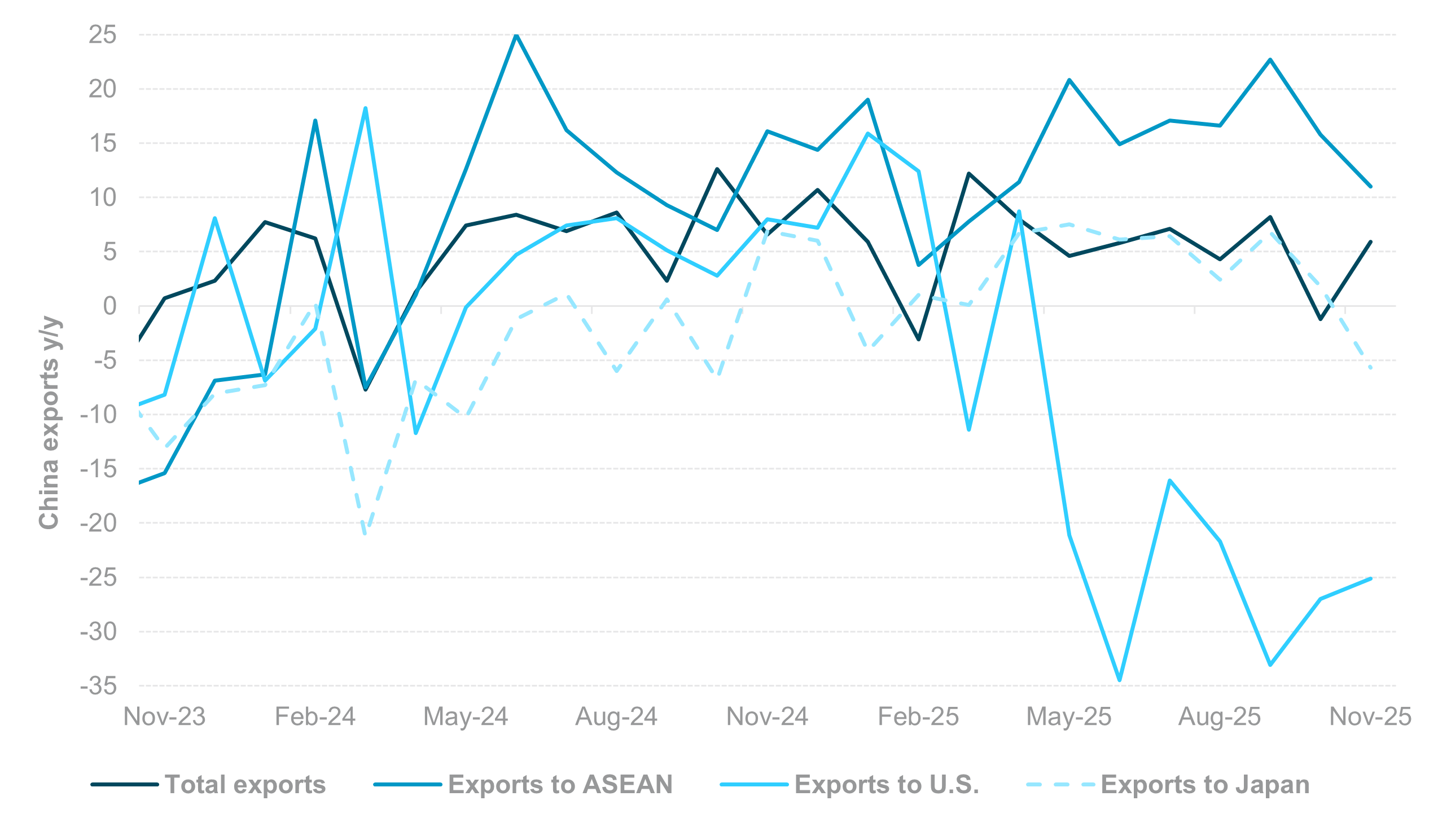

EXHIBIT #4: CHINA EXPORTS AND DESTINATION GROWTH

Source: BNY, Bloomberg

Our take: In the Asia-Pacific (APAC) region, the key focus this week will be on trade data from China, India and Singapore, consumer spending and inflation expectations in Australia, and the Bank of Korea’s (BoK) policy meeting. Malaysia is set to release its Q4 GDP, while India reports inflation data. New Zealand will publish updates on food prices and jobs, and bank lending data are expected from Japan and the Philippines.

China’s December export data will be closely monitored for signs of further trade recovery with the U.S., potentially offsetting recent exports declines in exports to ASEAN countries and Japan. Australia’s consumer confidence and inflation expectations will be closely scrutinized after Deputy Governor Andrew Hauser of the Reserve Bank of Australia stated that inflation over 3% is “too high” and suggested the last rate cut in the cycle may have already occurred. An upside inflation surprise may accelerate market expectations for the timing and size of future rate hikes. Markets are currently pricing in one full hike by Q3 2025 and fewer than two hikes by the end of 2026.

India is set to announce December CPI, and we will be watching to see whether headline and core inflation normalize. As of November 2025, headline and core inflation stood at 0.71% y/y and 4.42% y/y, respectively. In the near term, focus in India will shift to the Union Budget in early February, where the government’s fiscal strategy will be key. Deficit and bond supply concerns have kept Indian government bonds at elevated levels, with 10y IGB at 6.65% versus 6.5% at the end of November, despite a Reserve Bank of India rate cut and a series of OMO bond purchases.

On central bank development, the BoK is expected to maintain the status quo and focus on financial stability risks. Overall, APAC monetary policy is likely to remain stable as we approach the end of the easing cycle, with government fiscal measures playing a greater role in stimulating growth.

Forward look: The year 2026 has commenced positively, with the AI and semiconductor sectors continuing to drive market momentum. This trend is evidenced by sustained foreign capital inflows and robust demand for IPOs in Hong Kong. Price movements have been notable, with the Shanghai Composite, Taiwan’s TAIEX, and South Korea’s KOSPI indices gaining 3%, 4%, and 8% year-to-date, respectively. While upcoming earnings may support this momentum, technical overbought conditions across regional equities warrant attention. Global geopolitical risks and moves in the U.S. dollar and Treasurys should be monitored as potential downside factors, though for now, these are unlikely to significantly alter prevailing market sentiment.

Looking ahead to the first quarter of 2026, we maintain a constructive outlook on APAC markets. Financial stability will remain a focus for regional central banks, especially in efforts to limit currency depreciation. Export growth should continue recovering, though trade relationships remain fragile. Within the region, our top currency preferences are CNY, KRW and TWD, followed by IDR and MYR. We hold a neutral position on SGD and a negative bias on INR, THB and PHP. Key events in Q1 include the Thailand general election on February 8, India’s Union Budget in early February, and China’s 14th National People’s Congress (NPC) and People’s Political Consultative Conference (CPPCC) on March 4 and 5.

As 2026 begins, markets are reaffirming themes familiar from 2025: U.S. exceptionalism, technology-led growth, resilient credit demand, and a structurally important role for the dollar. The near-term outlook hinges on whether subdued volatility can persist as the data calendar intensifies, with U.S. inflation, bond supply and global political risks testing investor complacency. The USD remains the central transmission channel across assets – supportive of unhedged equity returns but a potential headwind should rate expectations or fiscal dynamics shift. Bonds are deceptively calm, with 10y Treasury yields near key technical levels that could quickly reprice risk sentiment if breached. In equities, earnings, particularly from financials, may broaden leadership beyond technology, while emerging and APAC markets remain sensitive to trade, currency stability and capital flows. Policy decisions in housing, tariffs and geopolitics will increasingly influence correlations across stocks, rates and FX. Investors should expect greater dispersion, episodic volatility and renewed emphasis on dynamic hedging as Q1 unfolds.

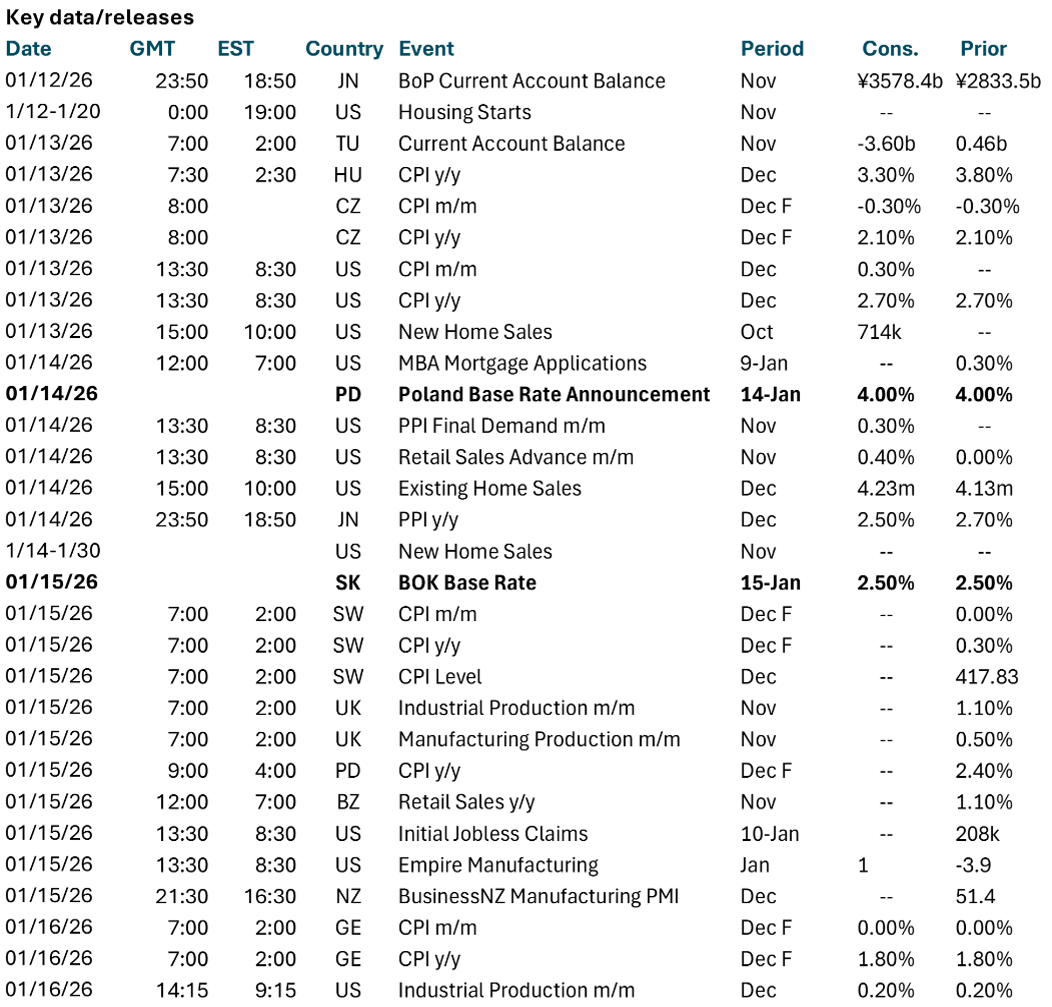

Central bank decisions

Poland, NBP (Wednesday, January 14): The NBP decision is the first major central bank action in Europe this year, and no change is expected. CEE was one of the best-performing regions for asset allocation in 2025. However, a bout of fiscal dominance concerns toward year end led to adjustments in asset holdings, though currencies have not yet been materially affected. To sustain current asset performance, we believe a pivot by NBP to better align with the ECB is needed to avoid erosion in real rates as the PLN struggles to sustain current valuations. Inflation is expected to accelerate this year to around 3%, with upside risks given the fiscal impulse.

South Korea, BoK (Thursday, January 15): The BoK is expected to keep its policy rate unchanged at 2.5%. South Korea’s expansionary fiscal policy continues to support economic growth. However, the recovery remains uneven (K-shaped) and is primarily concentrated in the technology sector. With stable inflation near 2% and the BoK’s emphasis on financial stability risks, the likelihood of an imminent interest rate cut remains low. We expect the BoK to hold rates steady at 2.5% in the January meeting and maintain this stance through the first half of the year. The bank’s immediate priority is addressing volatility in the FX market.

Source: BNY

Source: BNY