Positioning Beats Predictions

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 11 minutes

Welcome to 2026, the Year of the Fire Horse – one that is expected to deliver another strong global equity market performance, alongside a weaker USD and a mixed bond market dominated by yield curve-steepening expectations. More volatility is widely expected, making the signal-to-noise ratio less compelling for passive investing over any active management for money.

The broader 2026 outlook contrasts with a more modest view for the week ahead. These two narratives may start to collide with Friday’s U.S. jobs report. Softer U.S. labor markets remain a key concern and could temper recent market optimism. The consensus view favors global growth driven by reduced recession fears in the U.S. and signs of recovery elsewhere.

Geopolitical risk is expected to remain a key market driver as the unknowable meets the untradeable. Investors remain divided on safe havens, whether gold, industrial metals or the USD. Most see risk shifting away from tariffs and toward fiscal policy and election outcomes.

Big-picture themes for 2026 revolve around global fragmentation, resource-constrained supply chains, ongoing investment optimism and deficit financing. Political unease continues to rise, with a search for the silent majority across the U.S., Brazil and Europe. While next week is unlikely to resolve these market uncertainties, it may provide investors with some footholds in the wall of worry following a lively start to the new year on Friday.

Dutch pension reform puts $1.8tn in motion, as demographic and economic shifts move the system from defined benefit to defined contribution plans. This may encourage more risk-taking in the European Union (EU), favoring equities over long-dated assets like bonds. The key question is how other European pensions follow. The shift could trigger significant liquidity needs, while life-cycle swap strategies may add to yield curve-steepening pressures.

Economic data surprises: inflation or jobs? Fed easing is assumed in 2026, but timing remains data dependent. A January cut appears off the table, while March or June are in play. Tariff-related goods inflation is expected to peak in Q1, making CPI reports as important as jobs data. In Europe, disinflation is expected to persist, though early flash data may support further European Central Bank (ECB) rate holds.

AI investments: China vs. U.S. flows in focus. A surge in Chinese tech and AI IPOs has opened 2026 with a bang. Whether this momentum continues hinges on anticipated OpenAI and SpaceX deals in Q1. In the U.S., M&A pressures highlight late-cycle risks, with horizontal takeovers aimed at market and pricing power more prominent than supply-chain integration. Investors will be watching for divergence between U.S. and China value trades.

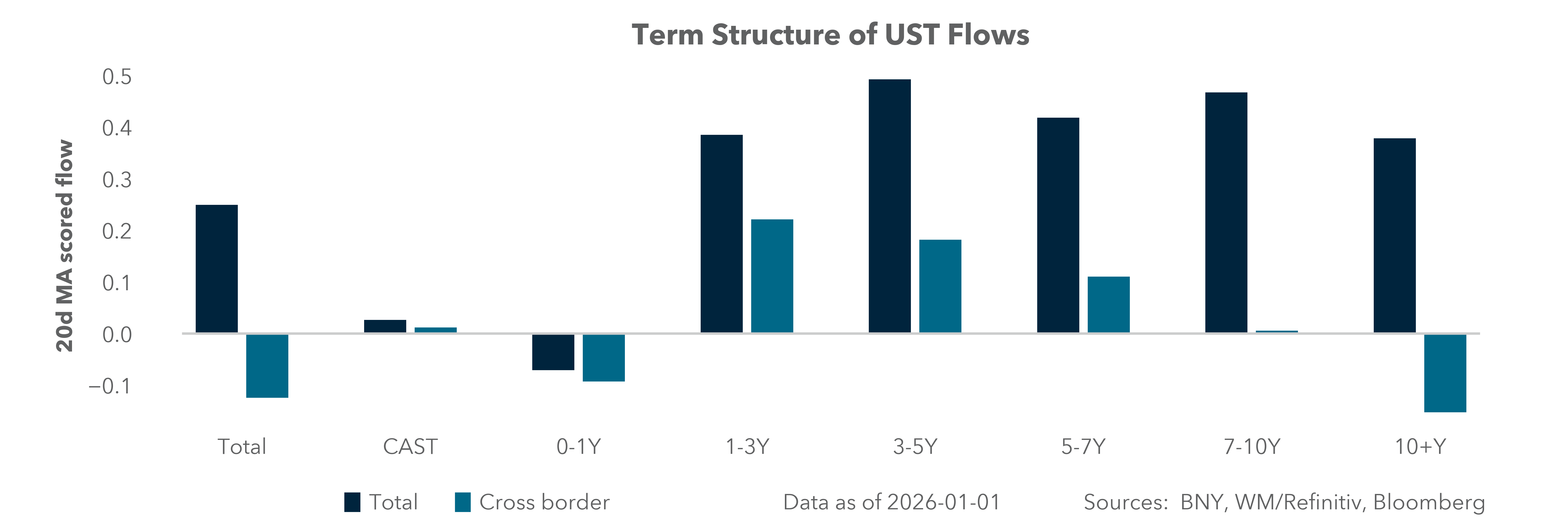

Supply pressure builds as investment grade (IG) meets governments. No U.S. Treasury coupon issuance is scheduled next week, while U.S. IG supply is expected to reach $65bn, part of a projected $200bn for January. In the EU, IG issuance could top €40bn despite the Epiphany holiday on Tuesday, with €38bn in government issuance also expected. Markets will be watching how supply matches demand, especially amid pension reform-driven shifts.

Geopolitical tension and energy are in play. Markets are watching Iran protests and Ukraine peace talks this week, with Venezuela in focus for the month. Whether President Nicolás Maduro steps down will test U.S. policy. Oil supply from Venezuela may be critical as the administration eyes lowering gasoline to $2 per gallon. OPEC+ is expected to hold production steady in Q1. A $55–$75 per barrel range is unlikely to ease inflation or improve consumer sentiment.

Is 2026 about positioning or rotations?

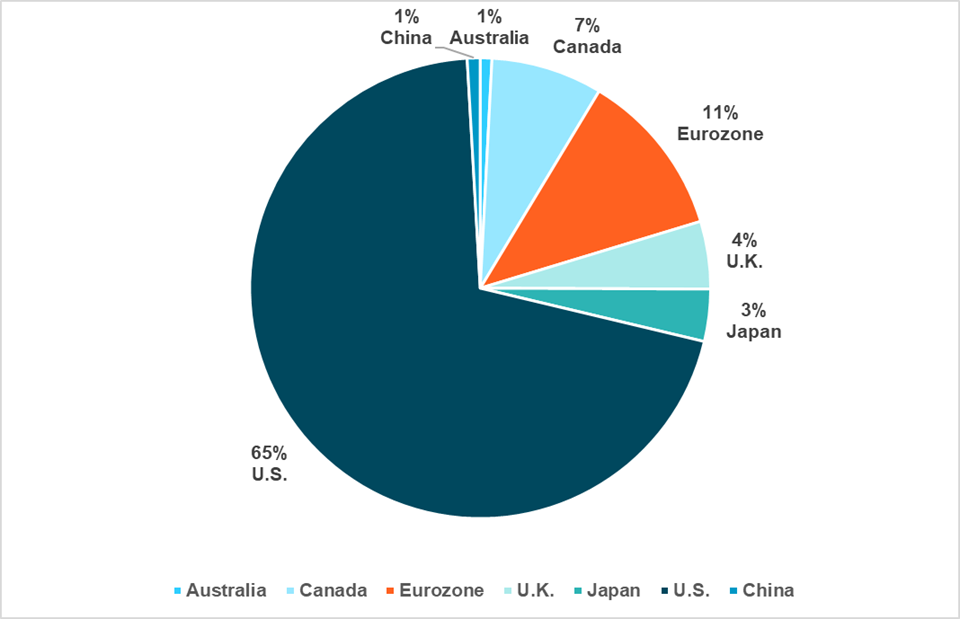

EXHIBIT #1: EQUITY POSITIONS BY NATION

Source: BNY

Our take: The U.S. share of global market equity capitalization is over 65%, as reflected in iFlow data. Notably, investor holdings in China have declined over the past two years. The MSCI ACWI Index (developed and emerging markets) weights the U.S. at just over 60%, while Australia at 1.5%, Canada at 3%, China at 4%, the U.K. at 4%, Japan at 7% and the Eurozone at 14%. Rebalancing into Q1 will depend on how earnings and volatility-adjusted returns perform in the first month. Most expect U.S. markets to maintain their dominance.

Forward look: A potential 5% reallocation from the U.S. and Canada to China and Japan should be on the radar in January. Earnings over the next two weeks will set the tone for a broadening of U.S. sector rotations. This may increase pressure on international investors to reassess U.S. concentration risks. The USD trend during January will also be a factor, with expectations for another 5% annual decline adding to case for reallocation. However, equity FX hedging and continued foreign investment into the U.S. may help offset some of the dollar-related pressure. The role of volatility and safe havens in 2026 will shape investor focus on risk-adjusted returns. In 2025, the U.S. volatility-adjusted return was 1.0, while many other markets offered better risk–reward profiles.

U.S. jobs reports and ISM will dominate next week

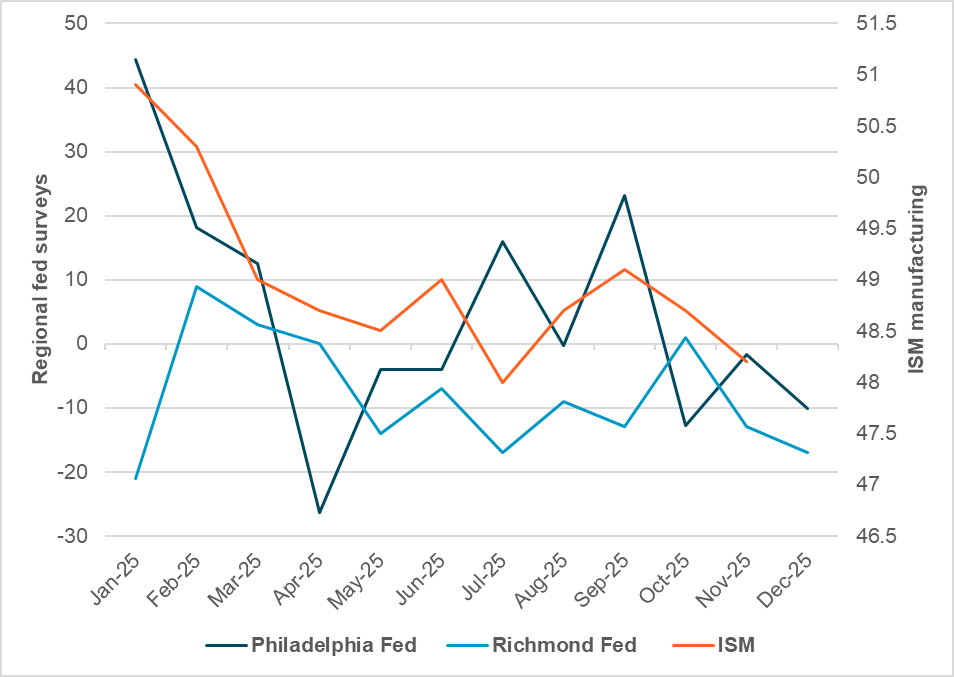

EXHIBIT #2: U.S. MANUFACTURING ISM AND REGIONAL FED SURVEYS

Source: BNY, Institute for Supply Management, Philadelphia Federal Reserve and Richmond Federal Reserve

Our take: The coming week marks a return to a more typical economic calendar after nearly a quarter of disruptions. The Institute for Supply Management (ISM) reports for manufacturing and services – due Monday and Wednesday, respectively – will set the growth tone for Q1. Investors are anticipating a Q4 slowdown, but this week’s data could challenge that view.

Further, U.S. labor data – ranging from Wednesday’s Jobs Openings and Labor Turnover Survey (JOLTS) to the December ADP employment report – will build the foundation for Friday’s all-important nonfarm payrolls and unemployment data. Whether the U.S. sheds jobs has become critical to how FOMC rate cuts unfold in the year ahead. Also in focus: wage cost stickiness and sector-level shifts in job creation and contraction. The role of AI in labor productivity and job demand is also part of this story. These themes will be part of Thursday’s release of Q3 productivity and unit labor cost data.

Forward look: We expect weaker nonfarm payrolls and ongoing concerns about Q4 growth. The ability of the U.S. economy to grow at a nominal 5%, driven by 2.5% real growth and 2.5% inflation, is part of the equation for 2026 investment return expectations. ISM reports should be as important as jobs data in shaping market reactions during the first week of the new year. Investors will watch whether manufacturing activity bottoms out while service-sector growth continues.

Regional Federal Reserve surveys, particularly from Philadelphia and Richmond, have closely correlated with ISM trends. These signals suggest that December was likely another weak month for both manufacturing and services. The ability of investors to look through soft-patch Q4 economic data, whether in jobs or business conditions, will be key to how emerging U.S. investment flows are supporting U.S. stock broadening trades, Fed easing expectations and USD stability within the recent 97–99 index range.

EMEA: ECB pivot seeks validation from year-end inflation and PMI figures

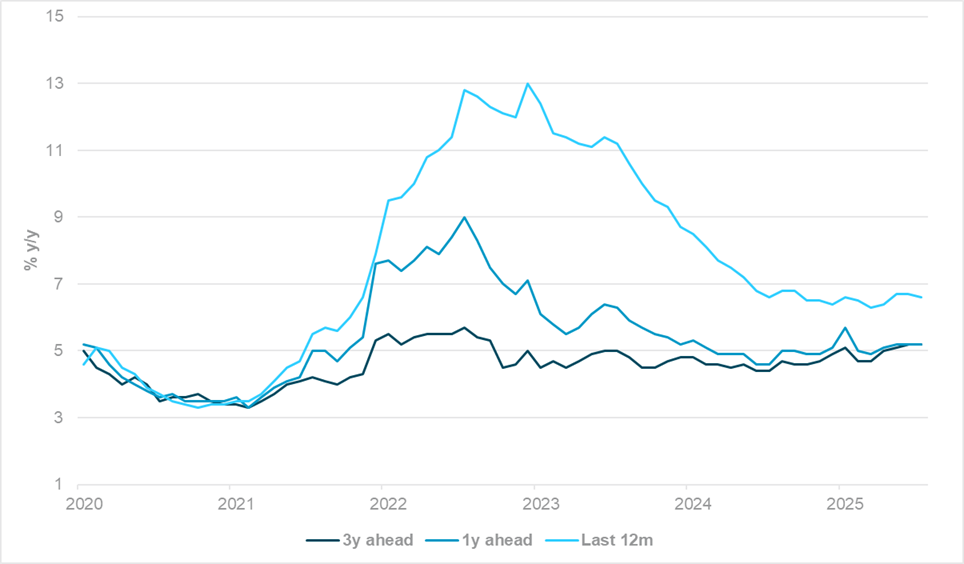

EXHIBIT #3: ECB SURVEY INDICATES RISK OF UPWARD SHIFT IN PRICE EXPECTATIONS

Source: BNY

Our take: Europe begins 2026 with the same supply-based challenges, as year-end talks yielded only limited progress on the Ukraine conflict. The geopolitical “risk premium” will remain embedded in local assets, and the ECB has identified related factors as a contributor to structurally higher inflation and inflation expectations. More recently, new supply-based input cost stress has emerged. The rally in prices – ranging from precious to industrial metals – will raise costs for the export- and manufacturing-dependent eurozone economy, which is already suffering competitiveness losses to China across the industrial value chain. December PMI data highlighted these pressures, with the eurozone survey noting:

“Industrial metals such as copper and tin saw a sharp rise after already increasing in price at double-digit rates over the course of the year. Nevertheless, it is surprising that, despite the weak economic situation, companies are apparently unable to enforce lower prices for goods with prices that are less dependent on the global market. One explanation could be supply-chain problems, as indicated by longer delivery times. In short, things are not running smoothly.”

These upward price factors exist even before incorporating upside risks from labor costs. Although surveys such as the Germany Ifo report point to material labor market weakness in manufacturing, skilled labor shortages continue to limit productivity gains in the sector. Meanwhile, wage growth in services continues to pose upside risk to broader eurozone inflation. It is perhaps no surprise that inflation expectations appear to be unanchoring, with household perceptions of inflation trending higher at the end of 2025 (Exhibit #3).

Furthermore, unlike in Asia-Pacific (APAC), current supply challenges in the eurozone mean that a stronger currency is insufficient to generate disinflationary pass-through. At best, in EUR terms, the rate of change in industrial metals and other commodity prices may ease slightly – but these are peripheral factors compared to the broader supply issues identified in the PMI report. We expected renewed calls for regulatory reform and removal of internal barriers identified in the Draghi and Letta reports from 2024. Rebuilding confidence swiftly is a political imperative in core Europe, as local and regional elections pose growing challenges to incumbents.

APAC: China aggregate financing, Regional CPI and Japan household spending

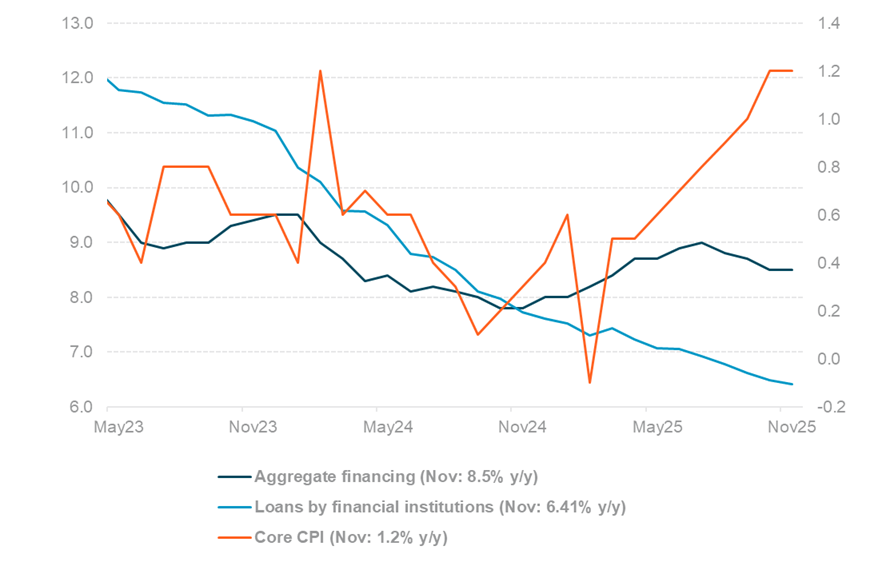

EXHIBIT #4: DECLINING CHINA CREDIT GROWTH AND IMPROVING INFLATION TREND

Source: BNY, Bloomberg

Our take: In APAC, key focus areas include China’s money and credit data, regional inflation and FX reserves, South Korea’s bank lending, and export figures from Taiwan and Australia. Japan will release cash earnings and household spending data, Malaysia will provide manufacturing and industrial production numbers, and Thailand will report on consumer and business confidence.

December loan data from China is expected to remain in focus as markets look for signs of stabilization following several years of declining credit growth. In November, loan growth by financial institutions fell to a new low at 6.41% y/y, down from 7.61% at the end of 2024, reflecting subdued domestic borrowing demand. Notably, household loans fell by ¥206bn in November, as consumers prioritized debt repayment, marking the first time on record with two consecutive years of contraction in household borrowing. Aggregate financing held steady at 8.5% y/y, driven primarily by government and local government borrowing, offering limited reassurance about broader credit conditions. Additionally, foreign currency deposits surged to a record $1.059tn in November 2025, up 28.3% y/y and surpassing the previous high of $1.054tn set in February 2022.

China’s December inflation figures are under scrutiny, following a recent upward trend. Both headline and core inflation turned positive and maintained upward momentum at 0.7% y/y and 1.2% y/y, respectively. Improved consumer sentiment and ongoing stimulus programs designed to boost domestic demand are expected to encourage consumption and, in turn, help alleviate disinflation concerns.

In contrast, Thailand’s headline CPI for November (–0.49% y/y) likely remains negative, influenced by weak domestic demand, low crude oil prices and a strong currency. The upward inflation trend observed in Taiwan (1.23%), the Philippines (1.5%), and Indonesia (2.72%) is well within the central bank target range, suggesting no imminent change from their current neutral or dovish policies.

Meanwhile, Australia’s inflation data will be closely watched for its significant influence on short-term interest rates expectations. The consensus for November’s trimmed mean CPI is 3.2%, down slightly from 3.3% in October. Persistent inflation and a tight labor market have led markets to anticipate a possible rate hike from the Reserve Bank of Australia as soon as June 2026.

Japan’s cash earnings are projected to remain elevated, with consensus estimates at 2.3%, down from 2.5% y/y in October. Household spending is expected to improve but remain negative at –1% (October: –3% y/y). Market attention will center on upcoming wage negotiations in Japan, which could influence the timing of future policy tightening following the 25bp rate hike anticipated in December 2025.

Additionally, final December PMI readings for Japan, Australia, and India are set to be released.

No central bank policy meetings are scheduled for this week. Central bank activity in the region will remain limited throughout January, with attention primarily directed toward the Bank of Japan, Bank of Korea, Bank Negara Malaysia, and the Monetary Authority of Singapore. Markets will also watch China’s monthly Loan Prime Rate and Medium-term Lending Facility announcements.

Forward look: The year 2025 yielded favorable returns for the APAC region, with both the Asia Dollar Index and MSCI Asia ex-Japan posting gains of over 3% and nearly 30%, respectively. Robust December PMI readings – China manufacturing at 50.1 and non-manufacturing at 50.2 – along with South Korea, Philippines and Taiwan returning to the expansion zone in manufacturing, have set a positive tone entering 2026.

Looking ahead to 2026, we maintain an optimistic outlook on APAC risk assets, supported by ongoing foreign capital inflows, continued GDP growth driven largely by exports in technology and semiconductors, a broad recovery in tourism, and accommodative monetary and fiscal policies. We anticipate that positive growth and investment trends will likely outweigh fiscal-related currency headwinds.

Within APAC, our preferred currencies are CNY, KRW and TWD, followed by IDR and MYR. We hold a neutral stance on SGD and a negative bias toward INR, THB and PHP. 2026 will kick off with a series of IPOs in Hong Kong, capitalizing on buoyant sentiment. South Korea’s President Lee Jae Myung will meet with President Xi Jinping in an inaugural state visit to China from January 4 to 7. Key events in Q1 2026 include the Thailand general election scheduled for February 8, as well as China’s 14th National People’s Congress, and the Chinese People’s Political Consultative Conference meetings on March 4 and 5.

Looking ahead, 2026 is shaping up less as a single-direction market and more as a year defined by dispersion, rotation, and selective risk-taking. Earnings resilience, policy credibility, and volatility-adjusted returns will increasingly matter across regions and asset classes.

For investors, the opportunity lies not in predicting every macro outcome, but in dynamically positioning portfolios to capture relative value as growth, inflation and liquidity paths diverge. Active management, disciplined risk budgeting, and an openness to rebalance long-held concentrations will be essential tools as global markets navigate a more fragmented but opportunity-rich landscape.

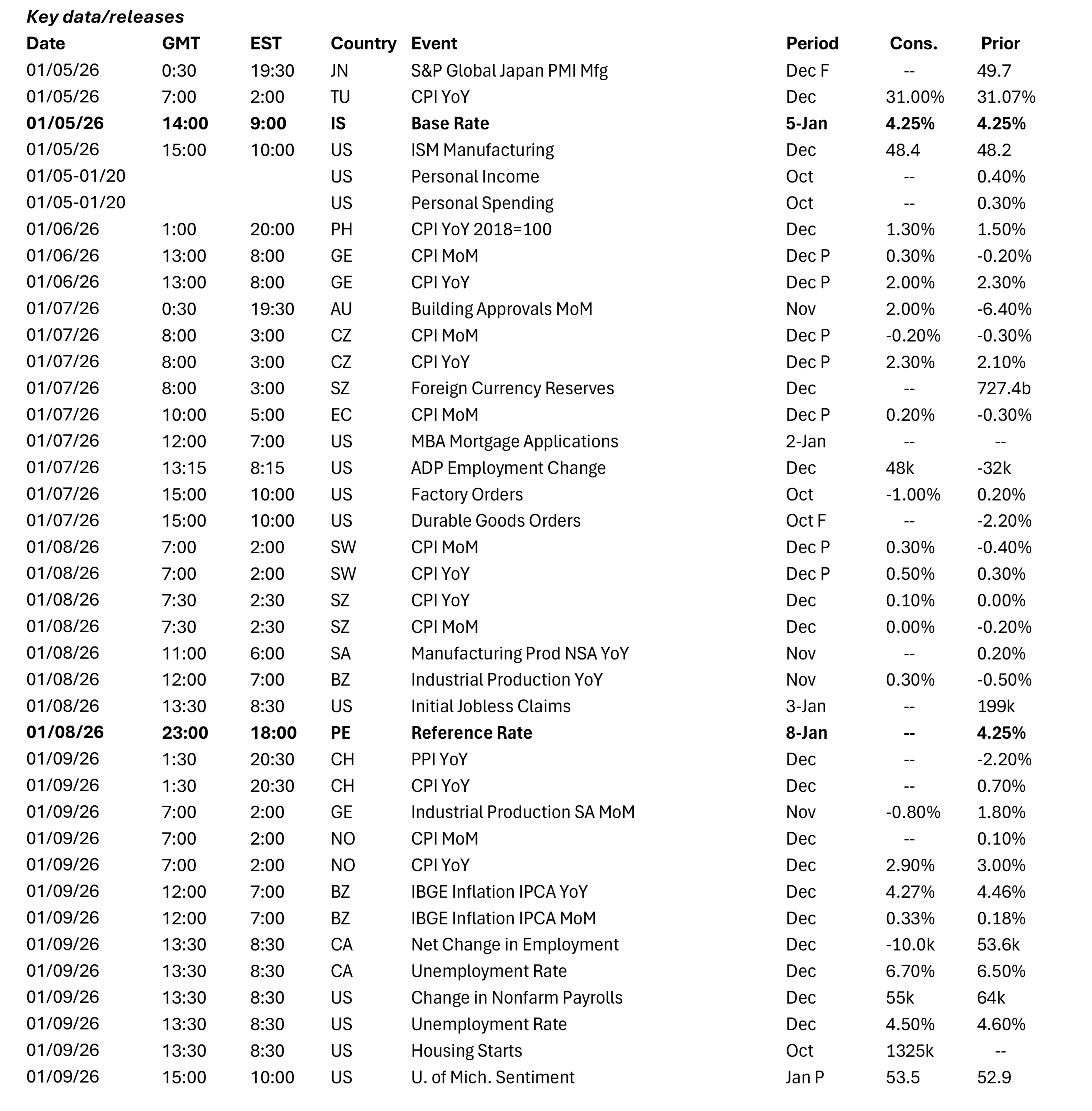

Central bank decisions

Israel, BoI (Monday, January 5): The BoI is expected to keep rates unchanged at 4.25%, as Governor Yaron made it clear in the November meeting that further easing would be extremely limited since the residual effects of strong fiscal impulse over the last few years remains very strong. However, this does mean that some additional restraint on inflation arising through the FX channel would also be welcome and perhaps open the way for additional easing. Much will depend on the rate differential outlook vs. the U.S., but iFlow suggests that the extent of ILS underheld positions are at extremes such that the bar for material accumulation is very low.

Peru, BCRP (Thursday, January 8): The Central Reserve Bank of Peru (BCRP) may hold rates for a fourth consecutive meeting as underlying conditions since the December meeting have not changed much. Inflation on a sequential basis is now running at a slightly faster pace, which may require some additional vigilance. Had the December FOMC meeting been more dovish, Latin American central banks would have commenced 2026 with more policy space. At this rate, we expect a more cautious approach toward easing, and holding real rates at closer to 3% should also help the sol (PEN) perform.

Source: BNY

Source: BNY