Oil, yields and the summer trade

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

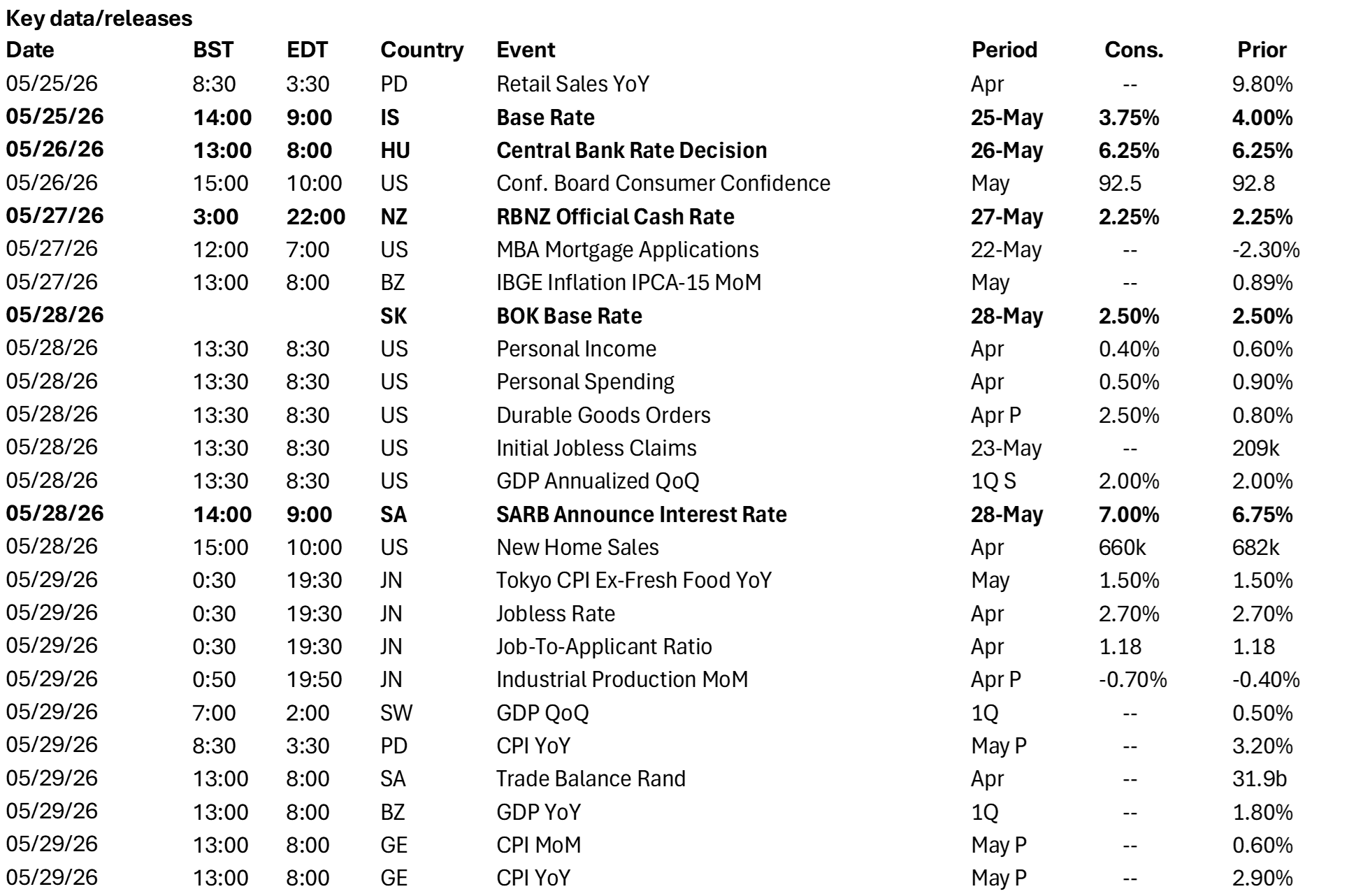

Last week delivered breakout moves in bonds, driven by inflation risk and amplified by oil shock fears globally – reviving talk of fiscal sustainability and higher-for-longer Fed policy. The U.S. market saw 30y yields rise to 5.10%–5.20% levels not seen since 2007, while 10y yields rose to 4.60%–4.70%. Financial conditions will face another test this week as month-end reallocations coincide with the early formation of summer trading themes.

Nvidia’s earnings beat on EPS and sales, reinforcing AI demand and capex, but the market sold off – with rising rates, tighter financing conditions and a stronger USD weighing on future growth expectations, and crowded sector positioning amplifying the move. Together, these pressures leave open the question of whether bond volatility will cap the tech-led equity rally.

In focus this week:

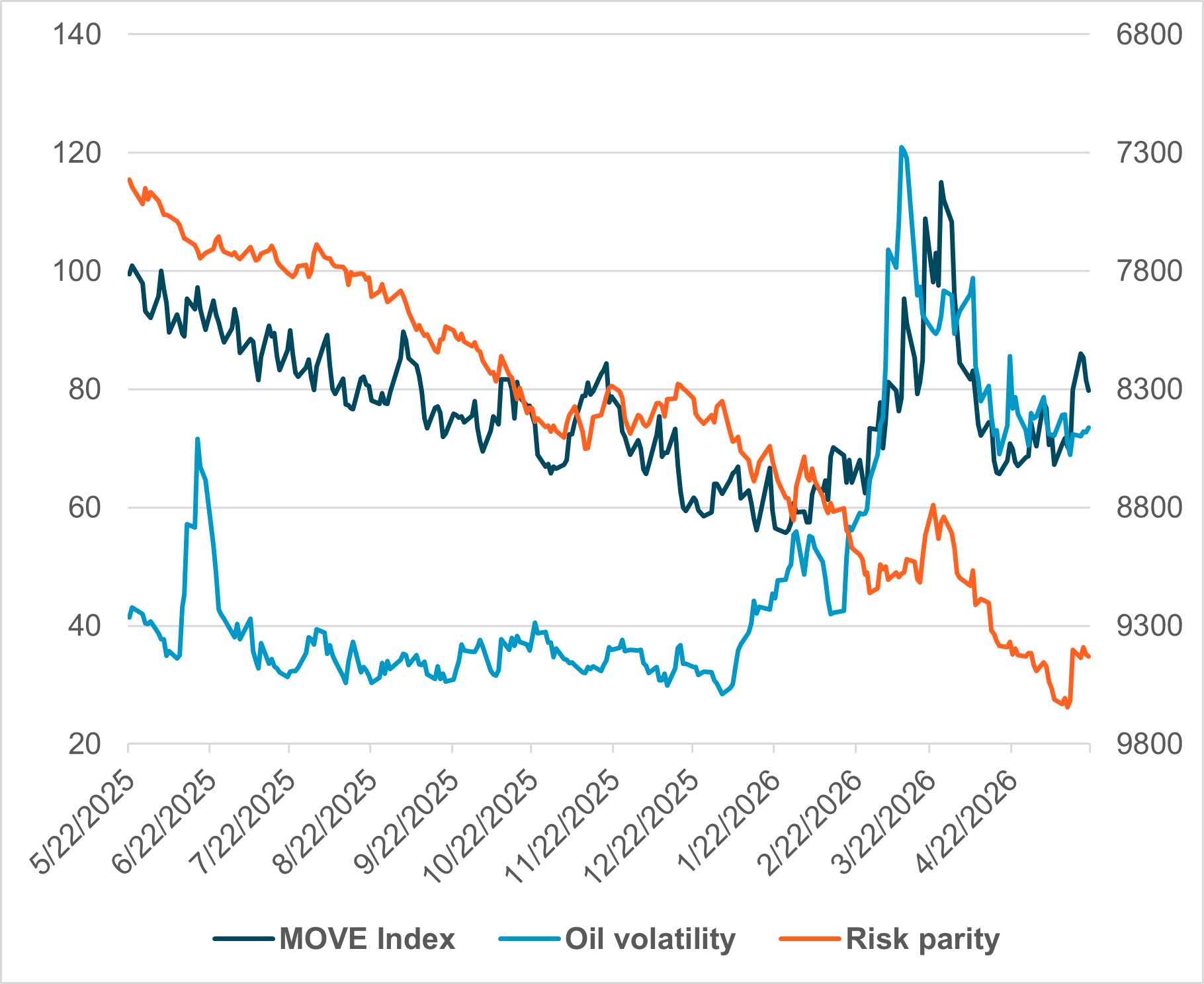

Risk parity: bonds now dominate oil

EXHIBIT #1: RISK PARITY RETURNS VS. OIL AND BOND MARKET VOLATILITY

Source: BNY, Bloomberg

Our take: Risk parity programs allocate assets by volatility, targeting returns to a fixed unit of risk. Exhibit 1 plots the performance of the S&P 10% Risk Parity ETF against the MOVE Index, a U.S. bond volatility measure across durations. Until the Iran conflict bond market volatility drove risk parity performance and oil volatility was largely irrelevant to both. Most notable is that oil and MOVE volatility in the last two weeks have decoupled.

Forward look: Oil’s role in determining the direction of stocks and bonds since February 28 has been the dominant barometer for trading markets. What happened in the last two weeks stands out as a shift in thinking about oil. The rate moves are now more important to markets. Risk parity programs continue to perform well despite pressure from both rates and oil, suggesting an additional factor is supporting equities. Energy costs passing through into the economy are lifting bond yields globally, but yields have yet to reach the threshold that typically turns equities lower. The return of negative bond-equity correlation is traditionally a signal that markets are normalizing after a crisis. This time, however, the war remains unresolved and oil prices stay elevated. Normalization may be premature.

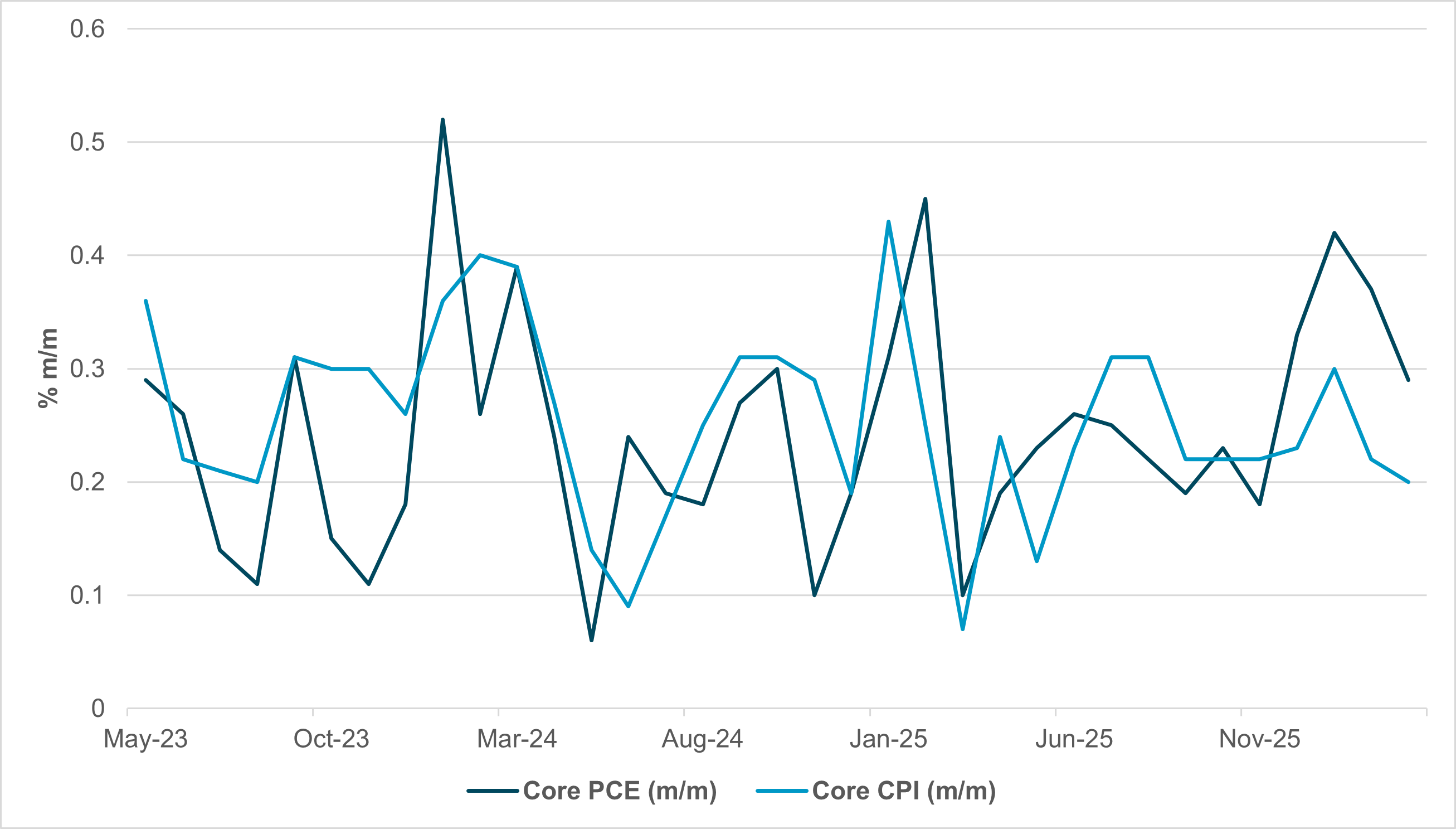

North America: PCE inflation and rates in focus

EXHIBIT #2: U.S. CORE CPI AND PCE PRICE INDEX

Source: BNY, Bloomberg

Our take: Much of the selloff in the long end of the curve last week was attributed to renewed inflation concerns and possible Fed repricing in a more hawkish direction. We’ll gain more insight into both this week with the release of Core PCE, the Fed’s preferred inflation metric, on Thursday.

The holiday-shortened week in the U.S. will also include GDP data, Conference Board Consumer Confidence, and personal income and spending data – together painting a picture of the American consumer. All releases are scheduled for Thursday. Data are lighter up north with only Canadian GDP coming on Friday.

Forward look: While CPI tends to be more impactful for rates markets, Core PCE carries greater policy relevance for the Fed. The expectation for Core PCE for April is 3.3% y/y after a 3.2% print for March. A firmer-than-expected print, as we saw for CPI and particularly PPI earlier this month, could reinforce concerns around sticky inflation and add more momentum to the Fed repricing we have seen over the past several weeks.

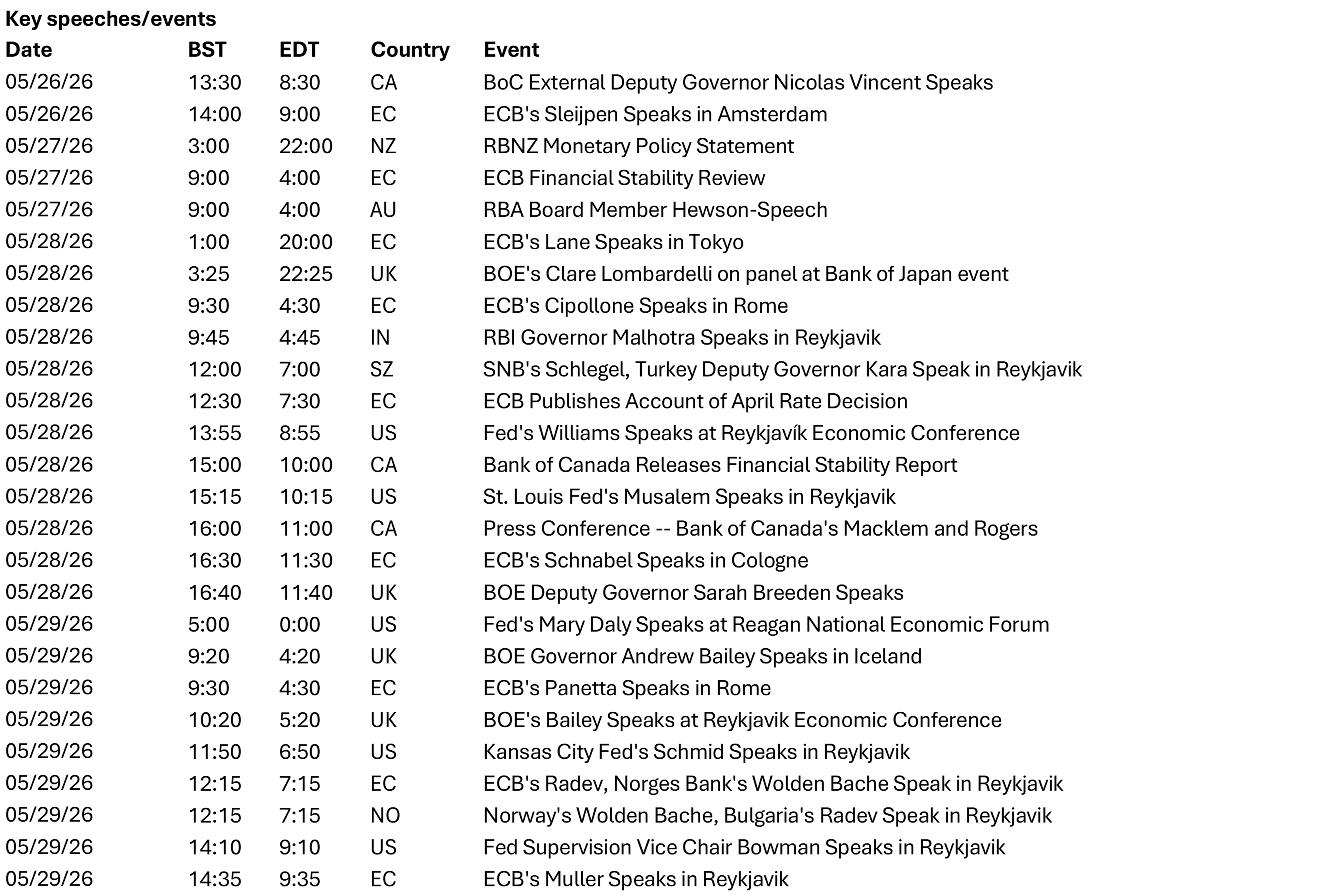

Fed Presidents John Williams (New York), Alberto Musalem (St. Louis) and Jeffrey Schmid (Kansas City), along with Vice Chair for Supervision Michelle Bowman, are all speaking at the Central Bank of Iceland’s conference in Reykjavik, though the event is closed-door and unlikely to generate market-moving headlines.

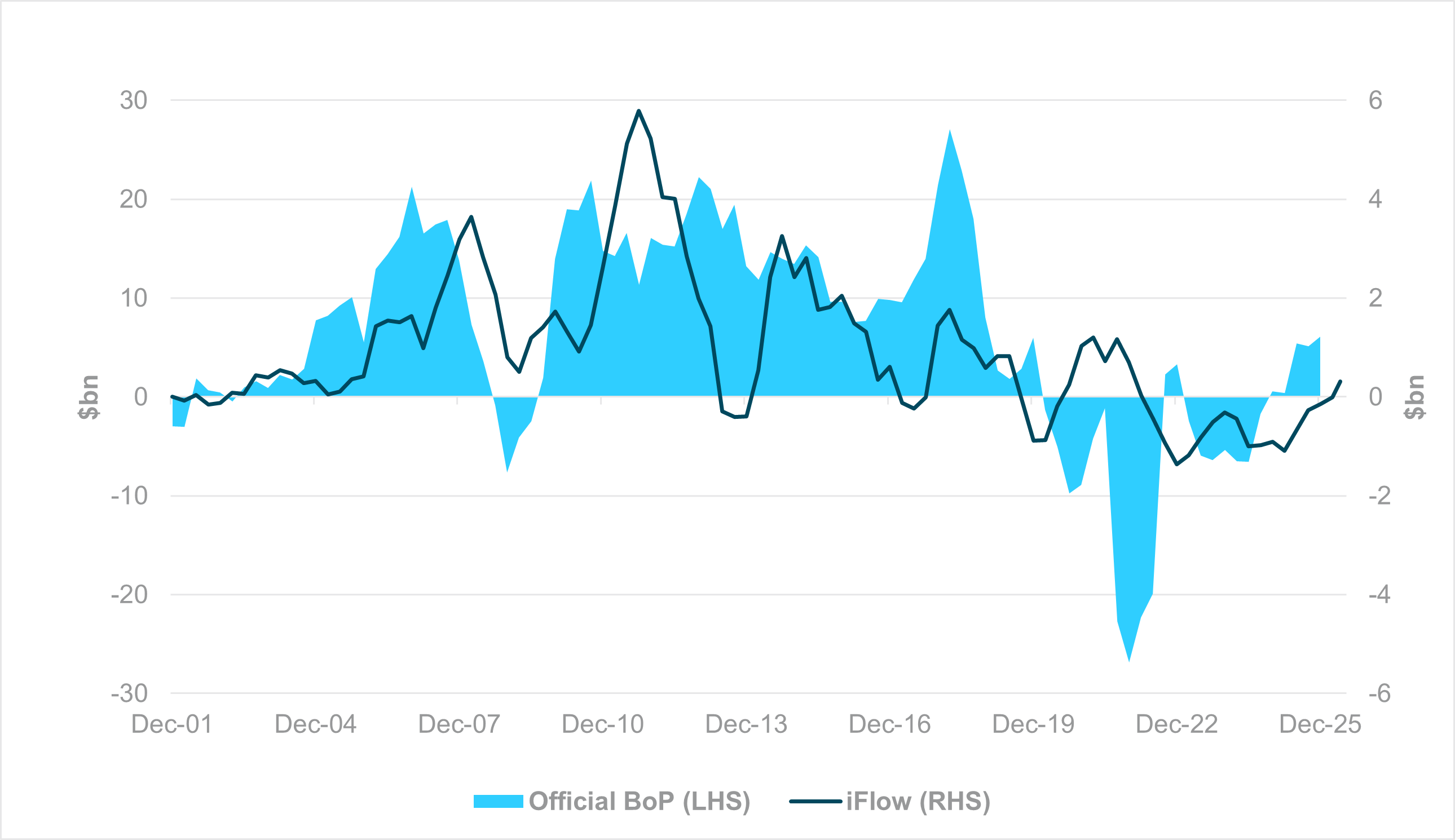

EMEA: SARB leads EM rate reversal as inflation bites

EXHIBIT #3: SOUTH AFRICA OFFICIAL INCURRENCE OF PORTFOLIO LIABILITIES VS. IFLOW PROXY

Source: BNY

Our take: The market’s base case for the Iran conflict remains for talks (and volatile headlines) rather than re-escalation, but the supply ramifications are now also expected to be more prolonged. A shift in the Fed’s policy stance has reset the benchmark for emerging market central banks. On the back of surprise hikes in Asia to defend currencies and avoid excessive outflows, there are many candidates in EM that can follow, especially if fiscal performance is also under pressure, or other idiosyncratic factors come into play. Turkey is seen as a candidate, especially with growing reserve stress, but South Africa is likely to take the lead this week as it reverses course and hikes the repo rate back to 7.0%. This marks a sharp reversal from the easing path the SARB had established before the conflict, which had been reinforced by a lower inflation target and an unexpected terms-of-trade boost from surging precious metals prices. There was even talk of new fiscal rules to strengthen credibility, but there will be little appetite for such steps at present. As core inflation rebounds above 3.5% y/y and headline inflation returns to the 4.0% handle, swift anchoring of inflation expectations is necessary.

On the positive side, our data indicate that markets have not totally shifted their view on policy credibility, and inflows have generally been improving year to date (Exhibit 3). Mining/materials equity flows can still benefit the ZAR and local markets selectively, while swift consolidation of the real-rate buffer will contribute to stabilization in SAGBs. The main challenge for EM countries’ financial accounts for the rest of the year is where U.S. yields and Fed rates stand. SARB and its peers will hope that no more than a handful of precautionary cuts are needed, but the bar is set by the Fed – any rate increases will require more forceful moves from EM peers.

Forward look: It will be a holiday-shortened week through much of Europe, but the speech calendar is very heavy due to the Reykjavik 2026 economic conference, hosted by the Central Bank of Iceland. Bank of England Governor Andrew Bailey, Norges Bank Governor Wolden Bache and Reserve Bank of India (RBI) Governor Shri Sanjay Malhotra will be among the keynote speakers, joined by several peers from the ECB and the Fed. Addressing monetary policy during a global supply shock will undoubtedly be the core topic, and there will be ample opportunity to assess the willingness of central bankers to shift toward tightening in response to a short-term inflation shock. The mixed round of Eurozone data has led to a small pullback in ECB expectations for June, but the market appears to have settled on a hike as the base case. European economic commissioner Valdis Dombrovskis has conceded that the central bank will need to move, despite the clear cost to growth and the budgetary challenges it creates at the EU level. Italy has already formally asked the commission to extend the National Escape Clause in the Stability and Growth Pact to energy spending.

While the EU remains mindful of long-term fiscal sustainability, the experience of the sovereign debt crisis and the 2022–2023 energy shock should provide greater scope for flexibility, lest the resistance cause political challenges at a national level. Furthermore, attitudes toward fiscal mutualization have shifted over the past decade, with Bundesbank President Joachim Nagel even admitting to developing “some sympathy” for European debt. Such a shift has helped suppress term premia in Eurozone debt, to the extent that even countries such as Romania and Hungary, which have established clear goals of euro entry, are seeing additional term premia declines on their own government debt. Hungary’s new finance minister is adopting a new fiscal policy with convergence as the clear goal, to the extent that the ministry’s attitude toward currency performance is much more relaxed, perhaps even paving the way for a standout dovish MNB stance for next week’s policy decision.

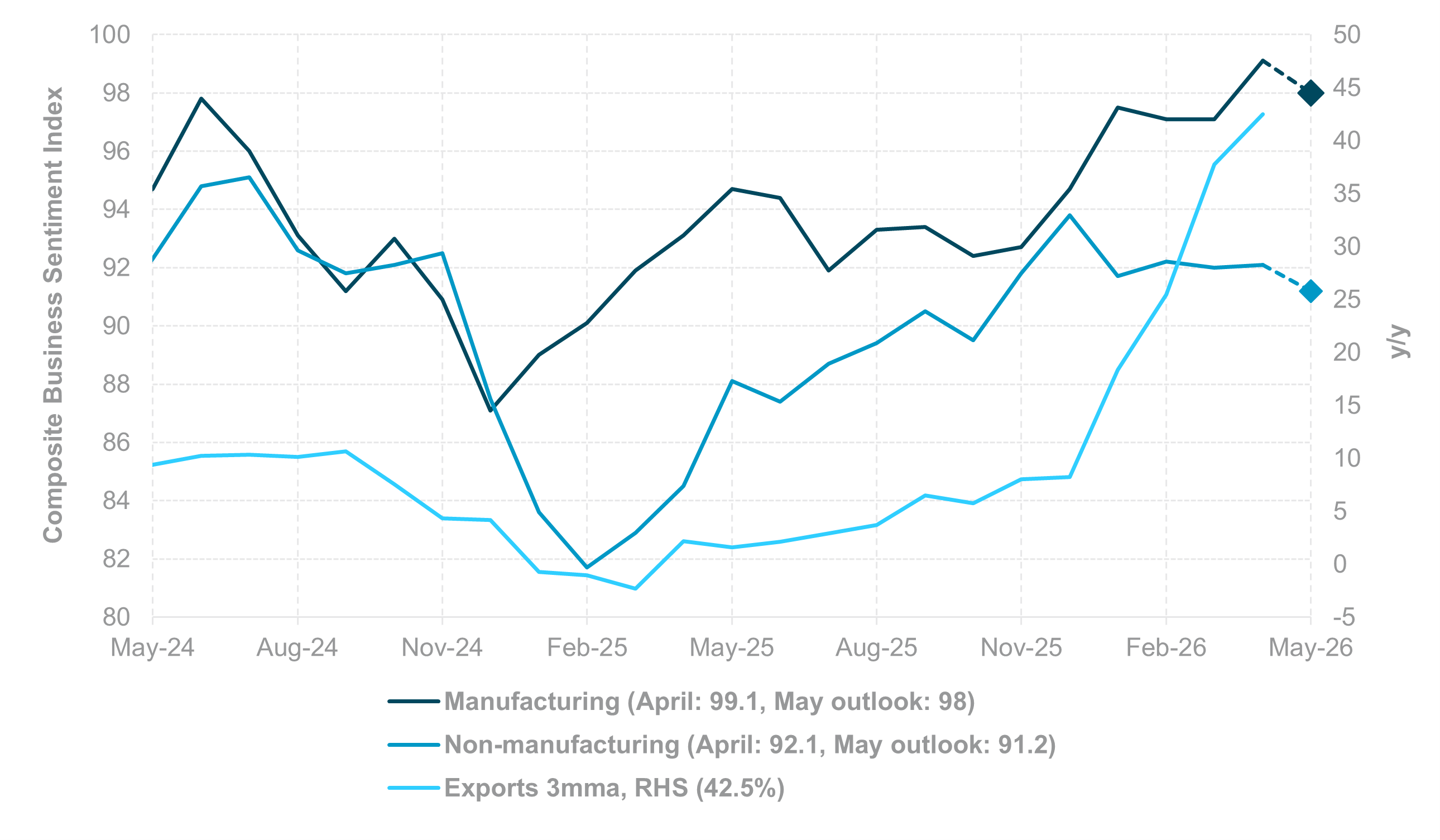

APAC: Central bank decisions and inflation data in focus

EXHIBIT #4: SOUTH KOREA COMPOSITE BUSINESS SENTIMENT INDEX AND EXPORTS

Source: BNY, Bloomberg

Our take: This week’s focus is on the RBNZ and BOK meetings, alongside regional inflation and industrial production data. In Australia, CPI and trimmed mean inflation will be key for reassessing the Reserve Bank of Australia’s outlook after the bank signaled a likely pause following three consecutive hikes. Japan’s May Tokyo CPI will be closely watched ahead of the June Bank of Japan meeting, while Singapore’s April CPI and Q1 final GDP should refine central bank expectations following April’s SGD NEER re-steepening. South Korea’s calendar is also active with the BOK decision, business sentiment, industrial production and retail sales.

Taiwan’s Q1 GDP and April industrial production should reinforce the tech and export upcycle. Thailand’s exports, trade balance and manufacturing production will gauge external demand after stronger-than-expected Q1 GDP (0.7% q/q, 2.8% y/y), while the Philippines’ exports, lending and money supply data will provide insight into domestic liquidity. China’s April industrial profits will be watched for signs of sustained earnings momentum after March’s strong 15.5% y/y YTD growth, despite persistent weakness in pricing power and uneven demand. Elsewhere, Japan releases retail sales, industrial production and labor data, while Australia publishes household spending and private credit alongside New Zealand confidence indicators. Both the RBNZ and BOK are expected to keep rates unchanged at 2.25% and 2.50%, respectively.

Forward look: The dominant APAC theme remains how central banks respond to persistent FX depreciation, rising inflation pressures, downside growth risks and lingering Middle East tensions. Bank Indonesia’s surprise 50bp hike, alongside Bangko Sentral ng Pilipinas’ tightening earlier this month, has raised the probability of similar moves in economies facing acute FX pressure. The RBI remains a potential candidate to tighten further, given the limited effectiveness of macroprudential measures and repeated FX intervention. The BOK is expected to stay on hold. So far, tighter policy has had limited success in stabilizing currencies, with terms of trade, fiscal concerns and capital flows remaining the dominant drivers.

We remain bearish on net oil importers and deficit-exposed currencies, particularly INR, THB, PHP and IDR. In contrast, CNY, SGD and MYR should benefit from stronger inflow dynamics, while TWD remains supported by sustained portfolio inflows. Despite foreign equity outflows and elevated oil prices weighing on KRW, we retain a constructive bias given strong export growth, a widening current account surplus and attractive valuation, with KRW REER at its weakest since early 2009.

Markets enter the coming weeks facing a more complex macro environment where bond volatility, rather than equity momentum, is increasingly setting the tone for cross-asset performance. The sharp rise in long-end sovereign yields across the U.S., Europe and parts of Asia reflects growing concern around persistent inflation pressures, elevated energy costs and the fiscal implications of sustaining higher rates for longer. While AI-related investment themes continue to support technology earnings and capital expenditure expectations, the ability of equity markets to extend gains may depend increasingly on the stability of global rate markets rather than earnings results alone.

At the same time, geopolitical risks tied to energy supply disruptions remain an important catalyst for inflation expectations, FX volatility and central bank policy recalibration. The interaction between oil prices, bond yields and USD strength will likely define market leadership through the summer trading period. Investors should expect higher cross-asset volatility, tighter financial conditions and increasingly selective opportunities across global markets.

Central bank decisions

Israel, Bank of Israel (Monday, May 25): The BoI is expected to cut rates by 25bp to 3.75% as fiscal impulse weakens due to the Iran conflict and the ILS has held at levels sufficient to prevent inflation pass-through. The market is not unanimous in its view; an on-hold decision and any associated guidance on fiscal spending could also provide some insight on the direction of the wider conflict. Annualized inflation has softened to below 2% but sequential numbers are as elevated as developed market peers, which require ongoing vigilance.

Hungary, Magyar Nemzeti Bank (Tuesday, May 26): The MNB decision is the first under the new government and we expect the market to seek guidance on when rate cuts could materialize. Despite broad-based inflation pressures generated by external price push and domestic fiscal impulse, the new administration has clearly signaled fiscal retrenchment up ahead to rebuild government finances. As the ministry is also less focused on HUF strength, there is perhaps some space to ease rates and provide borrowing relief. Successfully unlocking EU funding will further loosen financial conditions and help avoid a more pronounced currency decline.

New Zealand, Reserve Bank of New Zealand (Wednesday, May 27): Markets continue to price in RBNZ hikes as the labor market remains relatively tight, but the inflation outlook has probably not deteriorated sufficiently to justify a move yet. Governor Anna Breman stated that the bank will “act decisively” if core inflation picks up, but the uncertain global environment is ensuring sufficient demand retrenchment for now. The central bank warned in its April meeting that rate hikes carry the risk of “unnecessarily stifling an economic recovery,” underscoring the need to balance growth vs. rising inflation expectations.

South Korea, Bank of Korea (Thursday, May 28): We expect the BOK to leave rates unchanged at 2.50% and maintain policy continuity under incoming Governor Shin at his inaugural meeting. The BOK is likely to continue prioritizing inflation containment alongside financial and FX stability. While stronger growth and firmer inflation could justify tighter policy, growth remains uneven and heavily concentrated in semiconductors and technology sectors, while higher rates may prove ineffective against supply-driven inflation pressures. Front-end rates continue to price in near-term tightening risk, with three-month CD rates at 2.81% vs. the 2.50% policy rate.

South Africa, Reserve Bank of South Africa (Thursday, May 28): The SARB is expected to reverse course and hike to 7%, the first hike after delivering 150bp in easing since the end of 2024. The conflict has thrown the SARB off its highly credible path toward normalization. To maintain its lower inflation target, the SARB needs to act more assertively, especially as the risk of higher fiscal impulse out of necessity is strong. Inflation jumped sharply back to 4% y/y after a 1.1% m/m print in April and core inflation also responded strongly. Although tightening challenges the economy, allowing heavy outflows from heavy prior positioning would be a worse outcome for financial conditions.

Source: BNY

Source: BNY