Lost in translation

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

The hope for real peace talks and the reopening of the Strait of Hormuz drove the holiday-shortened trading week. Even with ongoing military actions, the memorandum of understanding (MOU) for extending a 60-day ceasefire kept sentiment risk-on. Oil fell 20% in May and inflation reports from Europe to Japan were lower than expected. A hawkish bias remained clear, with the Reserve Bank of New Zealand and Bank of Korea the standout holdouts last week. Month-end rebalancing was modest despite U.S. asset outperformance. Technology led the equity rally, with the AI theme dominant.

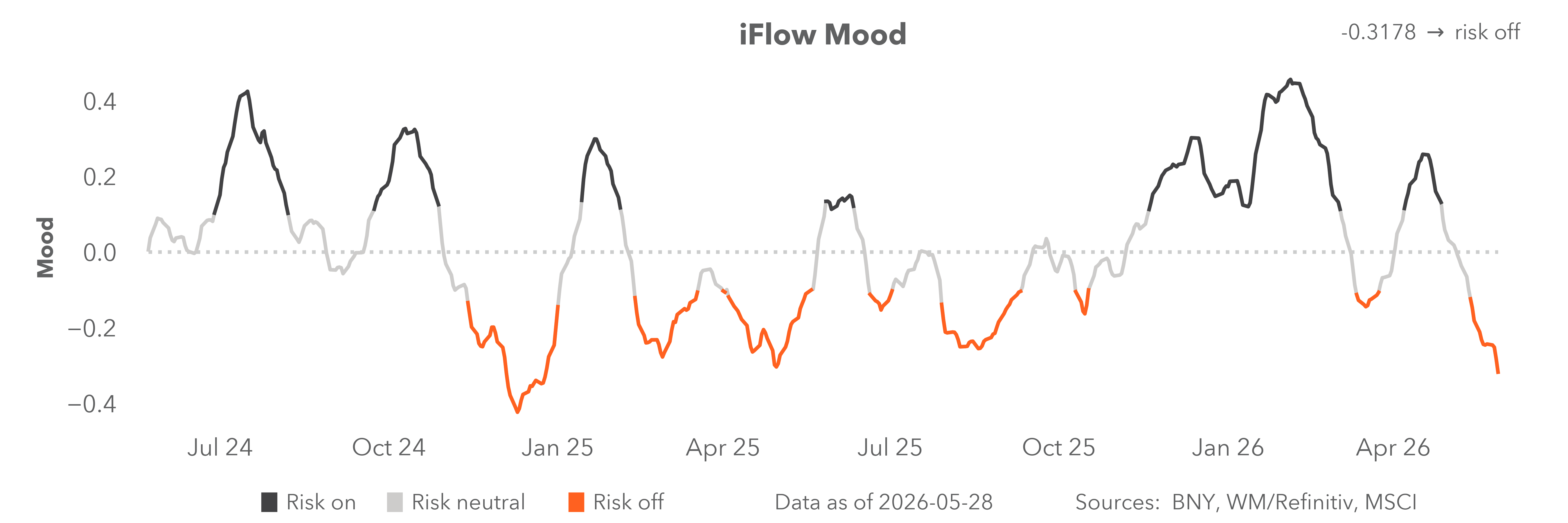

The rate markets recovered modestly, but data were mixed on growth. Canada’s technical recession in Q1 – with growth of -0.1% following -1% in Q4 – contrasts with the U.S.’s 1.6% in Q1 GDP revision. The link between trade and commodities highlights global demand concerns from the war. Our own mood index dipped to Liberation Day levels as investors harvest the rally higher in shares to diversify into fixed income. Something has been lost in translation between assets and peace deal credibility.

In focus this week:

Oil isn’t the only inflation driver

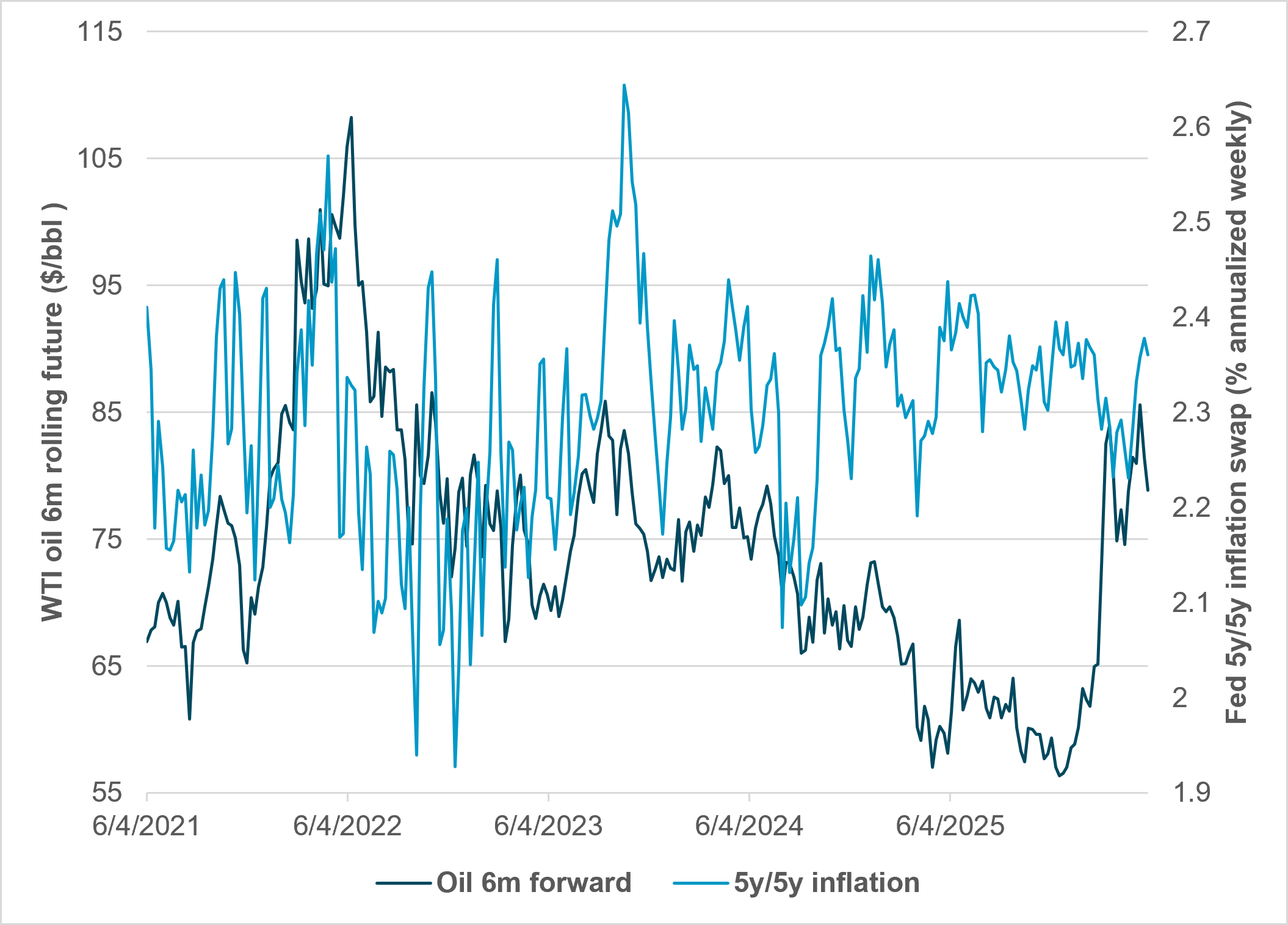

EXHIBIT #1: U.S. 5Y/5Y INFLATION B/E SWAP VS. 6M OIL FUTURES

Source: BNY, Bloomberg

Our take: While oil matters to inflation outlooks, it’s clearly not the only driver. Food inflation and ongoing service cost stickiness were also important in May. The role of higher investment driving up real growth and potentially shifting higher productivity will be critical in proving out the latest split between breakeven inflation and oil prices. Getting oil back to $70/bbl over the next six months will be an important factor in the Fed’s ability to look through the current supply shock.

Forward look: There are two other issues for investors to consider when it comes to inflation driving markets. One is the role of duration and fiscal credibility; the other is the role of real wages and consumer demand. The iFlow beta in equities to inflation is flat while the beta to a growth downturn is dominant. Bonds have managed to drop back below key breakout yield levels in the last week of May, reflecting the dueling pressures and the rebalancing from a furious equity rally. Many see June flows still dependent on oil, with the key test being no return to $100 WTI. Others point to the second-round effects of the three-month war driving up input costs, along with other potential supply disruptions – from weather shocks (El Niño, food production) to new geopolitical flashpoints (Ukraine/Russia, Cuba).

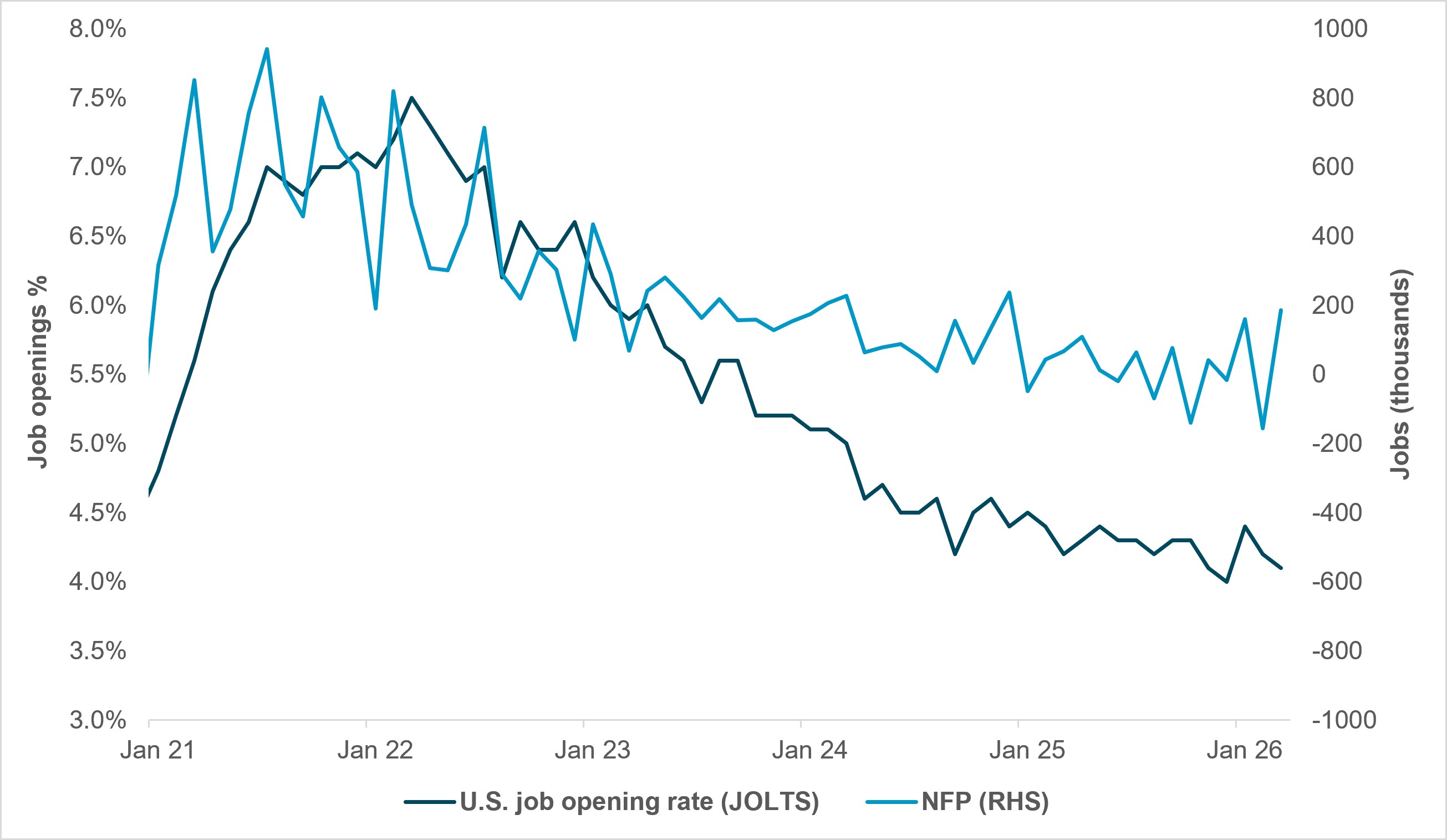

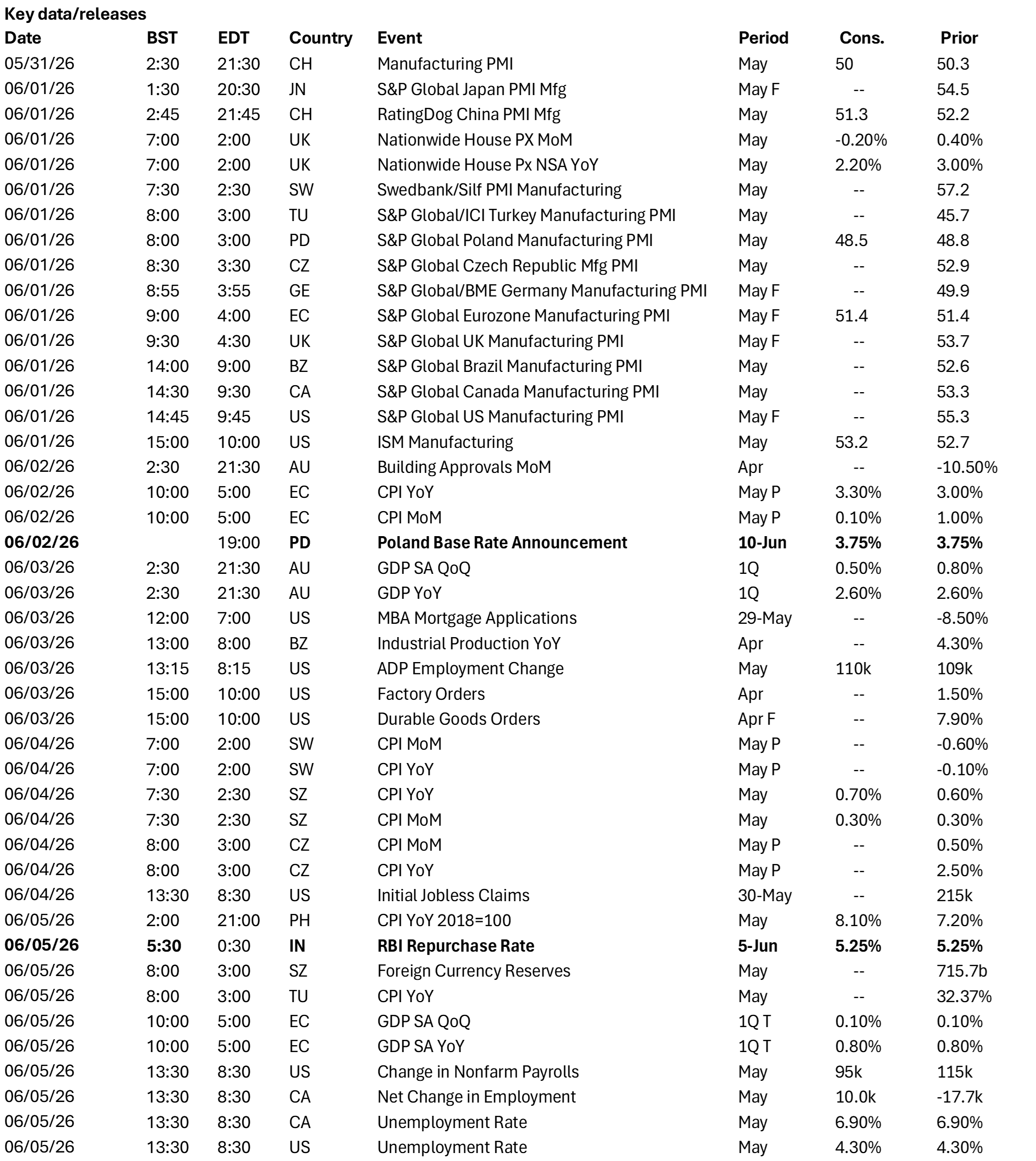

North America: Labor data and the Fed outlook

EXHIBIT #2: U.S. JOLTS VS. NFP, M/M CHANGE

Source: BNY, Bloomberg

Our take: With month-end behind us, this week will feature a considerable number of data releases in the U.S., highlighted by NFP on Friday. The week kicks off with insight into the manufacturing sector: S&P Manufacturing PMI and ISM Manufacturing on Monday, JOLTS on Tuesday, and ISM Services and Durable Goods midweek.

Canadian data will feature Manufacturing PMI and some employment data later in the week.

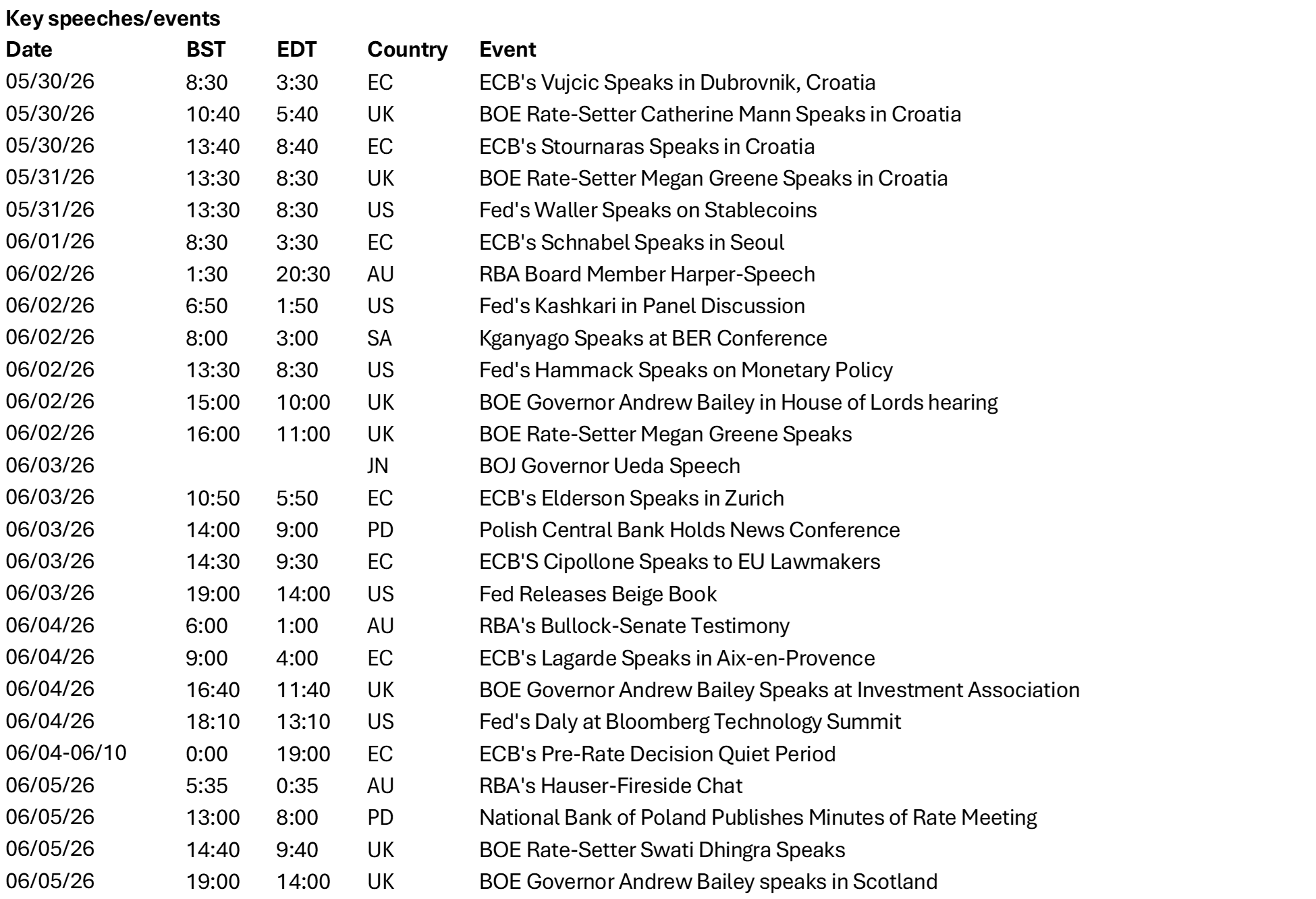

The Fed speaker calendar should be lighter this week. While we’ll have appearances by Presidents Beth Hammack (Cleveland), Neel Kashkari (Minneapolis), and Lorrie Logan (Dallas), we don’t expect meaningfully different messaging from what they have consistently been communicating since their dissents at the April FOMC.

Forward look: The NFP print at the end of the week will be most in focus for U.S. markets. Median forecasts put May at 93,000, slightly below the surprisingly strong 115,000 in April.

After a poor Q1 GDP print, Canada has entered a technical recession for the first time since Covid. While recessions are always headline-grabbing, net change to employment is projected to be modestly positive, and Manufacturing PMI for May might come in positive after a 53.3 print for April. The contrast to the U.S. will be watched closely.

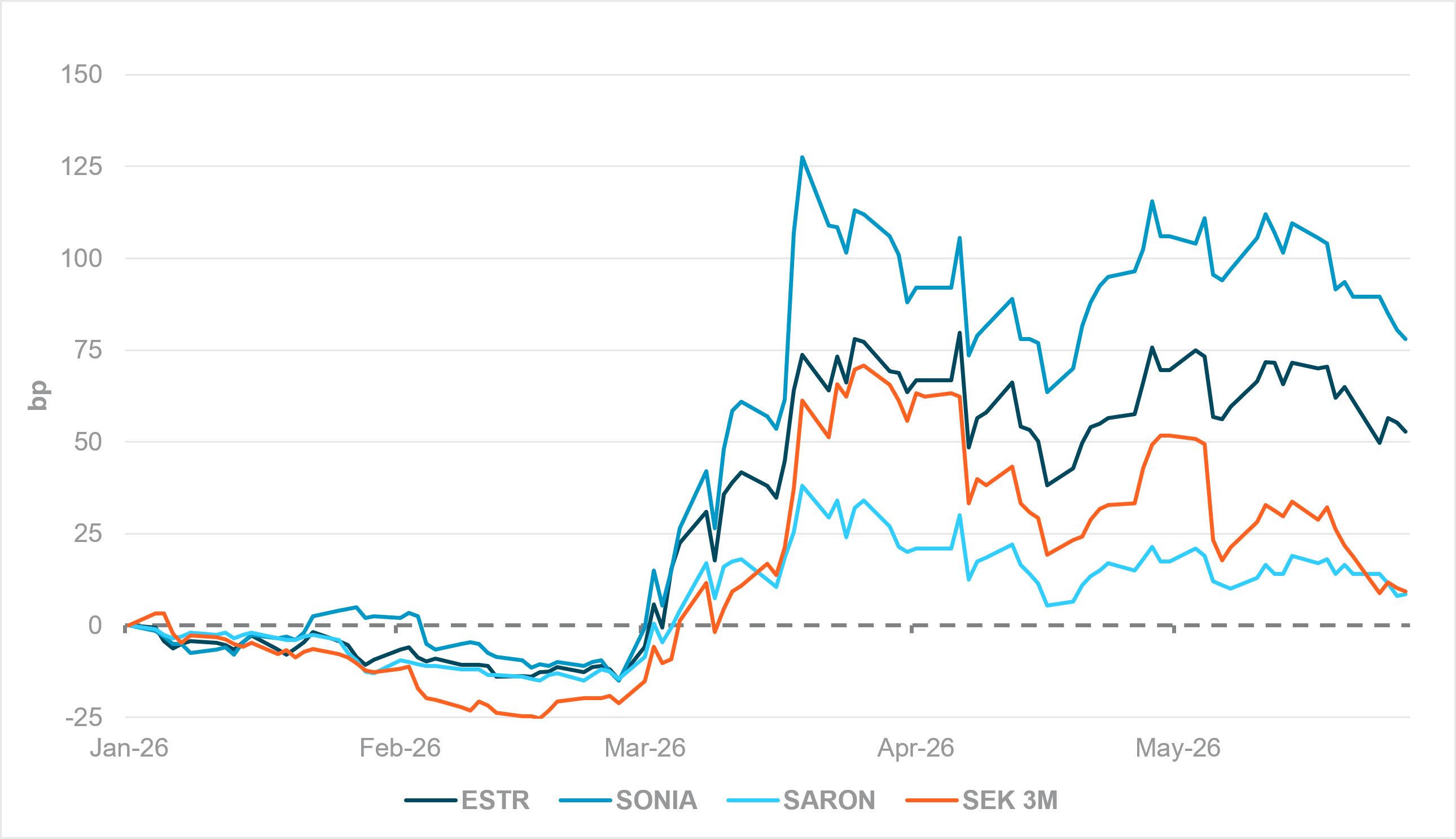

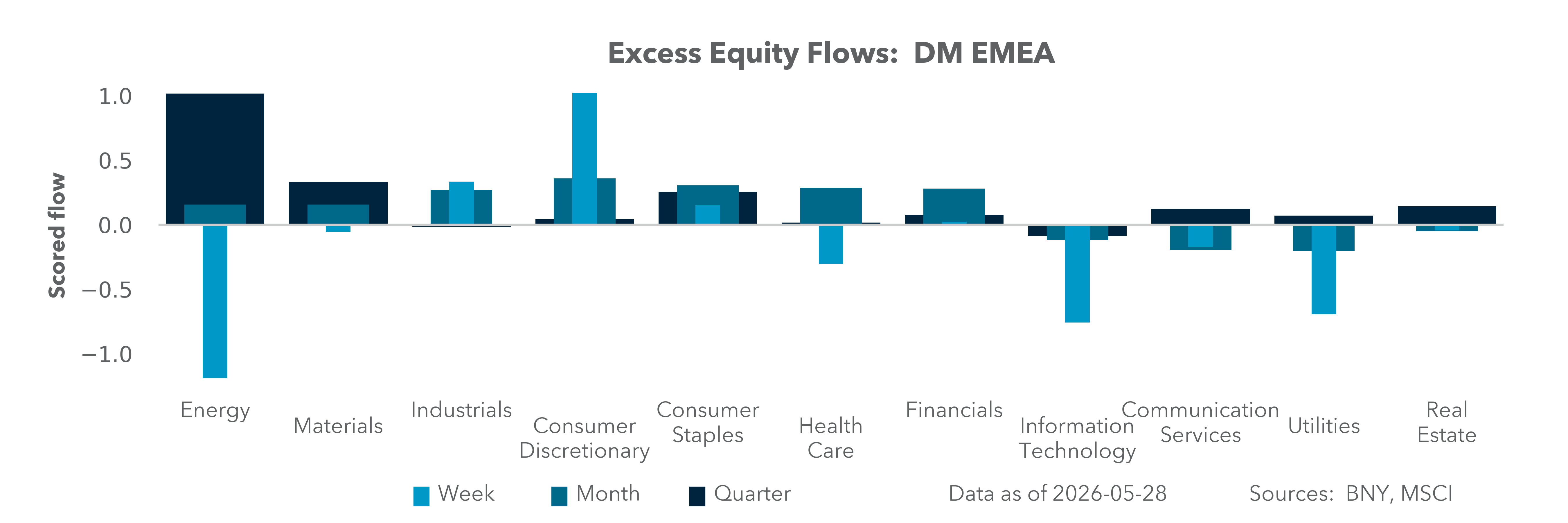

EMEA: ECB and other central bank guidance

EXHIBIT #3: CHANGE IN YEAR-END RATE EXPECTATIONS

Source: BNY

Our take: Preliminary May inflation prints across the Eurozone have broadly come in softer than expected, including a material 0.2% m/m contraction in Germany and subdued sequential figures for France and Spain. Only Italy’s headline inflation in May surprised strongly to the upside. While the aggregate figure is most likely to hold below 3%, ECB officials have only stepped up warnings of a June move, to the extent that Bank of Lithuania Governor Gediminas Šimkus is discussing the prospect of a second hike, pending inflation prints. Current pricing of year-end rates shows that when measured against “peak pricing” during the height of the conflict, ECB expectations have come off the least, which is broadly consistent with the policy outlook.

The Governing Council’s mandate is narrower, which allows some discounting of the labor market looseness prevailing elsewhere. Ahead of the ECB’s pre-decision blackout period this week, communication will likely point to “maximum divergence” from European peers, but weak momentum in EUR performance suggests that the gap may prove difficult to sustain. The direction of convergence remains to be seen. The base case remains for improving supply pressures, and once the growth “cost” from the ECB’s tightening becomes clear, policy reversals this year cannot be ruled out. On the other hand, the ECB may be displaying foresight. Given the growing ranks of hawkish surprises in APAC, we cannot rule out that the more hesitant European central banks may be forced to revisit their position.

Forward look: The Narodowy Bank Polski (NBP) decision on Tuesday is not expected to yield any major surprises, and most CEE central banks appear comfortable with their current policy approaches. Hungary’s central bank, for example, was sufficiently comfortable with the inflation outlook such that a dovish bias was still in place, but the key point of divergence is that the new government is explicit about fiscal consolidation (subject to additional budgetary support from the EU), which opens some additional monetary space.

Poland is in a different situation; we believe that keeping the status quo for the NBP requires taking a view on the situation in the Middle East and government spending priorities. The problem is that geopolitical deterioration and fiscal pressure are currently too closely linked – any lack of improvement on the former is likely to force higher government spending, given the political necessity of addressing cost-of-living concerns.

Unless there’s a major policy surprise, central banks in Europe will also need to contend with transmission effects from the upcoming ECB hike. The CEE countries with floating exchange rates – yet an integral part of the continent’s industrial supply chain – could face additional balance-of-payments pressures on a macro level, while corporate margins will face additional erosion as FX costs add to supply stress.

As PMIs are released across the region this week, the gap between input and output indices will provide a clear indication of the distribution of price pressures. In some sense, it would be preferable for output prices to register slower gains compared to inputs. If this is the case, headline inflation is more contained through finished goods, but narrowing margins would feed through into broader weakness in income growth. Although far from ideal in a growth context, voluntary restraint is preferable to politically painful spending cuts aimed at curtailing demand.

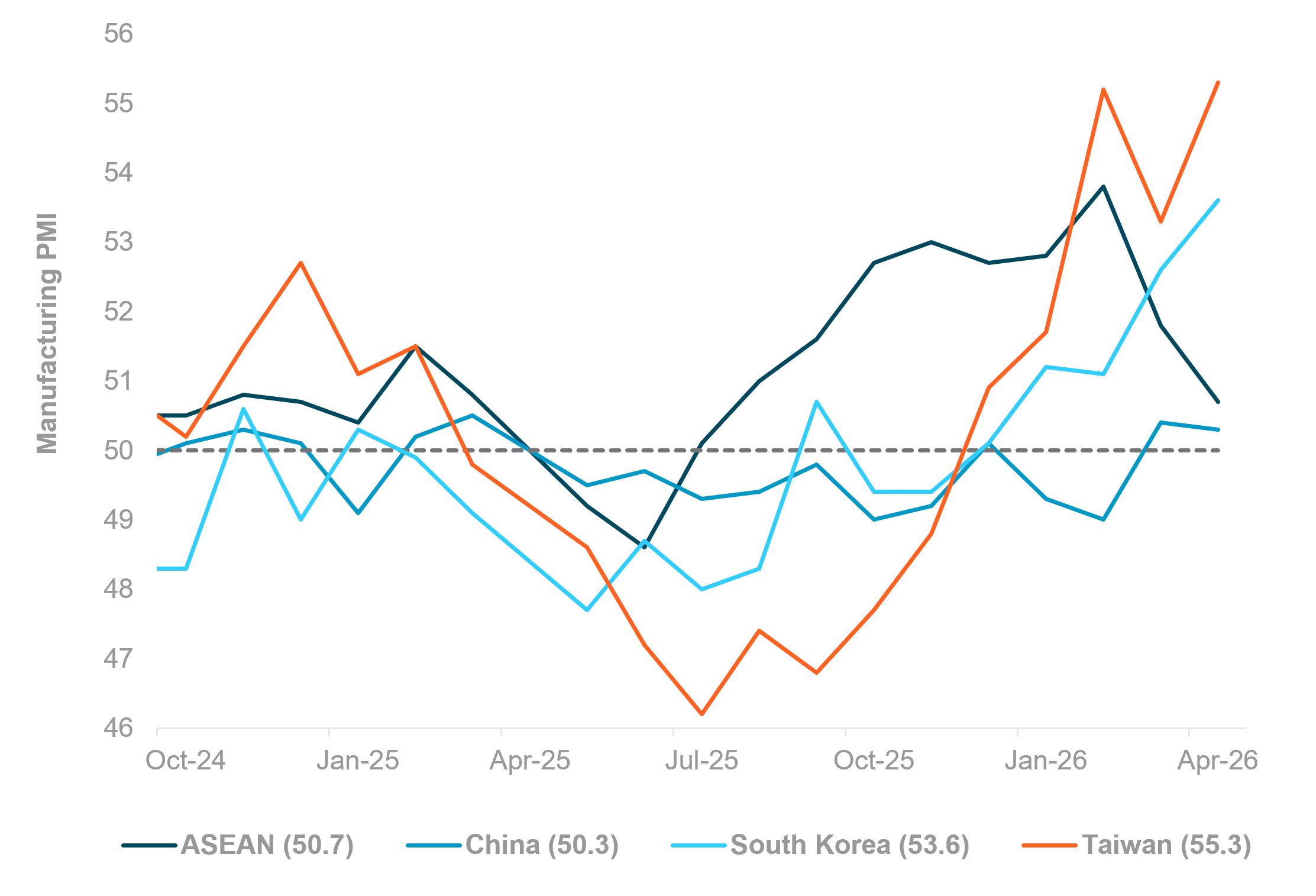

APAC: Growth momentum and FX differentiation

EXHIBIT #4: SOUTH KOREA AND TAIWAN PMI SURGE WHILE ASEAN WEAKENS

Source: BNY, Bloomberg

Our take: China PMIs, the Reserve Bank of India (RBI) meeting and Australia’s Q1 GDP dominate the week, with markets focused on how elevated oil prices are affecting regional business sentiment, trade and tech momentum, and inflation pressures. China’s official May PMIs, particularly services, and PMI for Indonesia, Thailand and the Philippines will be closely watched for signs of softer sentiment following sharp April deteriorations. South Korea’s exports and trade data remain a key gauge of the global tech cycle. Regional CPI releases from South Korea, Taiwan, Thailand, the Philippines and Indonesia will also shape expectations for policy easing and FX stability across Asia.

In South Asia, India’s Q1 GDP, current account balance and RBI decision are in focus, as investors assess whether an uncertain growth outlook keeps the RBI cautious despite rising inflation pressures. Elsewhere, Indonesia’s trade data, Singapore’s retail sales and FX reserves, and Japan’s Q1 corporate profits and capital spending will provide further signals on domestic demand and investment trends.

Australia’s Q1 GDP, April exports and trade balance will be central to Reserve Bank of Australia expectations, alongside speeches from Michele Bullock, Ian Harper and Andrew Hauser. Meanwhile, Bank of Japan Governor Kazuo Ueda’s comments will be scrutinized for policy signals ahead of the mid-June BOJ meeting.

Forward look: The fluid Middle East backdrop, insatiable demand for compute power, semiconductors and AI-related assets, alongside the evolving monetary policy cycle, remain the key drivers and differentiators for the near-term APAC FX outlook. Lower oil prices provide some relief for net oil-importing currencies, but it’s still premature to turn constructive as adverse terms-of-trade dynamics continue to weigh. Rising stagflation risks add further pressure, particularly for the INR, IDR and PHP. The RBI will remain closely watched following a series of largely ineffective measures to curb INR depreciation.

Meanwhile, KRW valuation appears deeply depressed. We see a high probability of near-term reversal – supported by strong economic recovery momentum and tentative signs of easing foreign equity outflow pressure – mirroring the pattern recently observed in Taiwan.

Our constructive thesis on medium-term CNY appreciation remains intact, underpinned by persistent foreign capital inflows. However, we are monitoring potential policy spillover risks to sentiment following the recent aggressive campaign targeting cross-border stock trading and reported travel restrictions on senior AI talent at private firms.

Overall, differentiation and relative value remain the dominant themes across APAC FX markets.

June will test whether markets have correctly priced the combination of easing geopolitical tensions, resilient growth, and persistent inflation risks. Equity investors continue to reward AI-related earnings growth and the prospect of lower energy costs, yet bond markets remain more skeptical, with flows increasingly favoring duration and defensive positioning. This divergence suggests investors are not fully convinced that the recent decline in oil prices will translate into a sustained easing of broader inflation pressures without a more dramatic growth drop.

The next phase of the market narrative will likely depend on labor market data, manufacturing activity, and central bank reactions to shifting inflation expectations. While the extension of Middle East ceasefire negotiations has reduced immediate tail risks, confidence remains fragile and vulnerable to renewed supply disruptions. Across regions, policymakers face the challenge of balancing slowing growth with inflation that remains above target. The result is likely to be greater differentiation across assets, currencies, and regions, making relative value and earnings durability increasingly important drivers of returns.

Central bank decisions

Poland, Narodowy Bank Polski (Monday, June 2): No change is expected, though – as with many peers – the NBP will need to assess how much room remains in real rates to prevent any un-anchoring in inflation expectations. Much will depend on progress toward resolving the conflict, but the market is also keeping an eye on fiscal stress, where Poland is underperforming and a monetary offset may be required at some point. For now, we would expect most CEE central banks to wait for the ECB decision and Middle East developments to play out before committing to their next moves.

India, Reserve Bank of India (Friday, June 5): We expect RBI to stay on hold at 5.25%, though the risk of a rate hike grows as policymakers attempt to curb currency weakness and anchor inflation expectations. Tighter monetary policy is unlikely to address supply-driven inflation or stabilize the INR – and could undermine growth momentum in the process. Further macroprudential and liquidity measures are the more likely path ahead.

Source: BNY

Source: BNY