Less Isn't Enough

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

The best and worst of times continue to play out for markets, as the economic data point to a slowdown while equities rally back near record highs. Our mood index is now at extremes, as investors catch up in equities and put cash to work.

Nevertheless, the November price action clearly signaled risk ahead. The rotation out of technology sets up December with ongoing doubts about AI earnings, which are expected to slow into 2026. Bitcoin entered a bear market – down 30% from its peak – and its connection to equities became clearer through ETF outflows and a souring view of the “Digital Asset Treasury” boom. U.S. equity indices fell, as did those in Japan, China and Australia. The break in seasonality raises the question of whether 2025 ends like 2018 – with a whimper, not a bang.

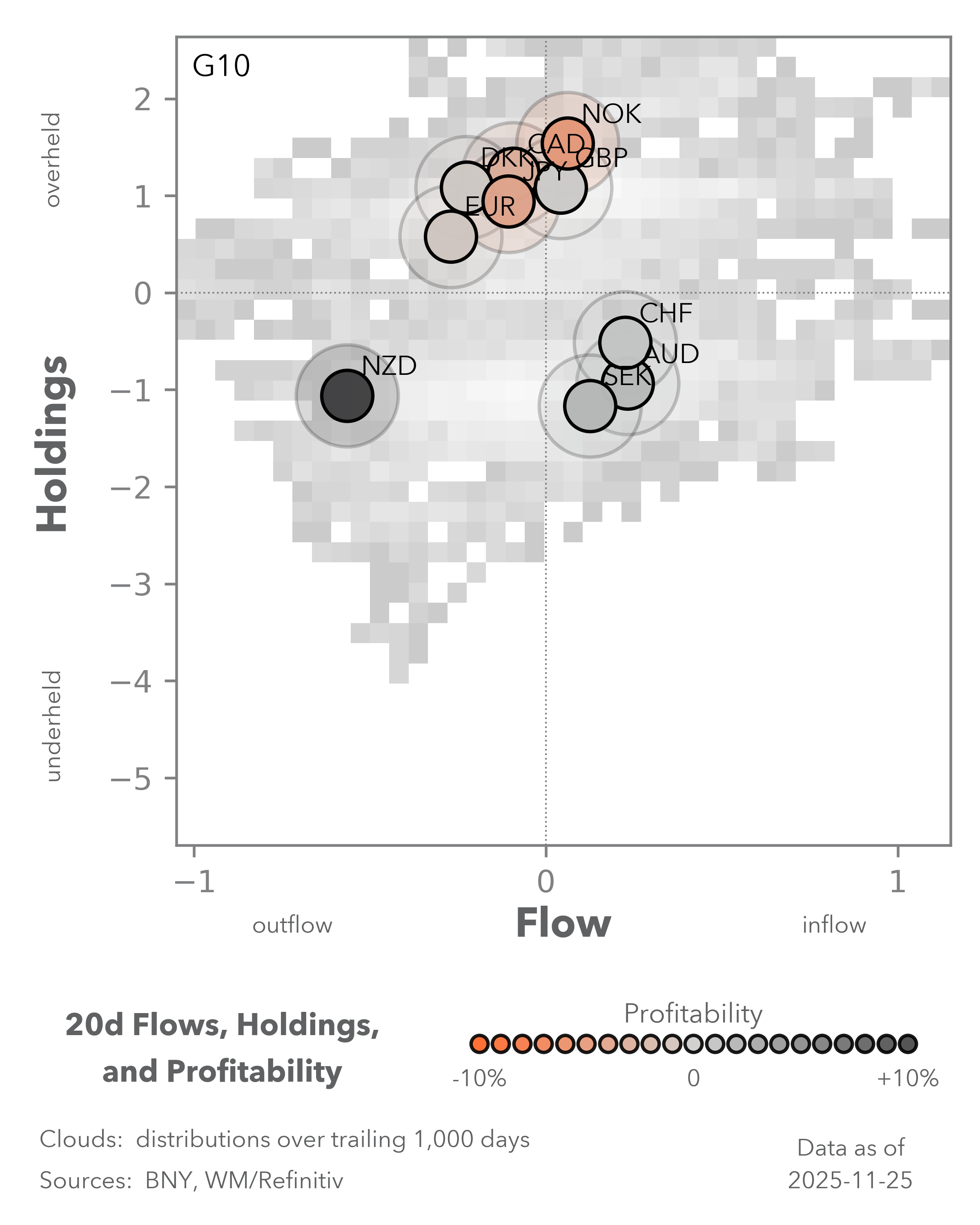

USD stability, despite the odds of a December rate cut, also dominates views that the U.S. may again lead growth into 2026, even amid political and policy concerns. The November byword is affordability, as the Trump administration shifts focus from trade and peace talks to cheaper food and lower health care costs.

December begins with a focus on data. Growth and inflation serve as domestic anchors, keeping investors wary as they climb the wall of worry into the usual Santa Claus rally. Any surprise that shifts FOMC rate cut expectations may matter more than disappointment in consumer data or earnings.

Will Black Friday sales set the tone for year-end risk?

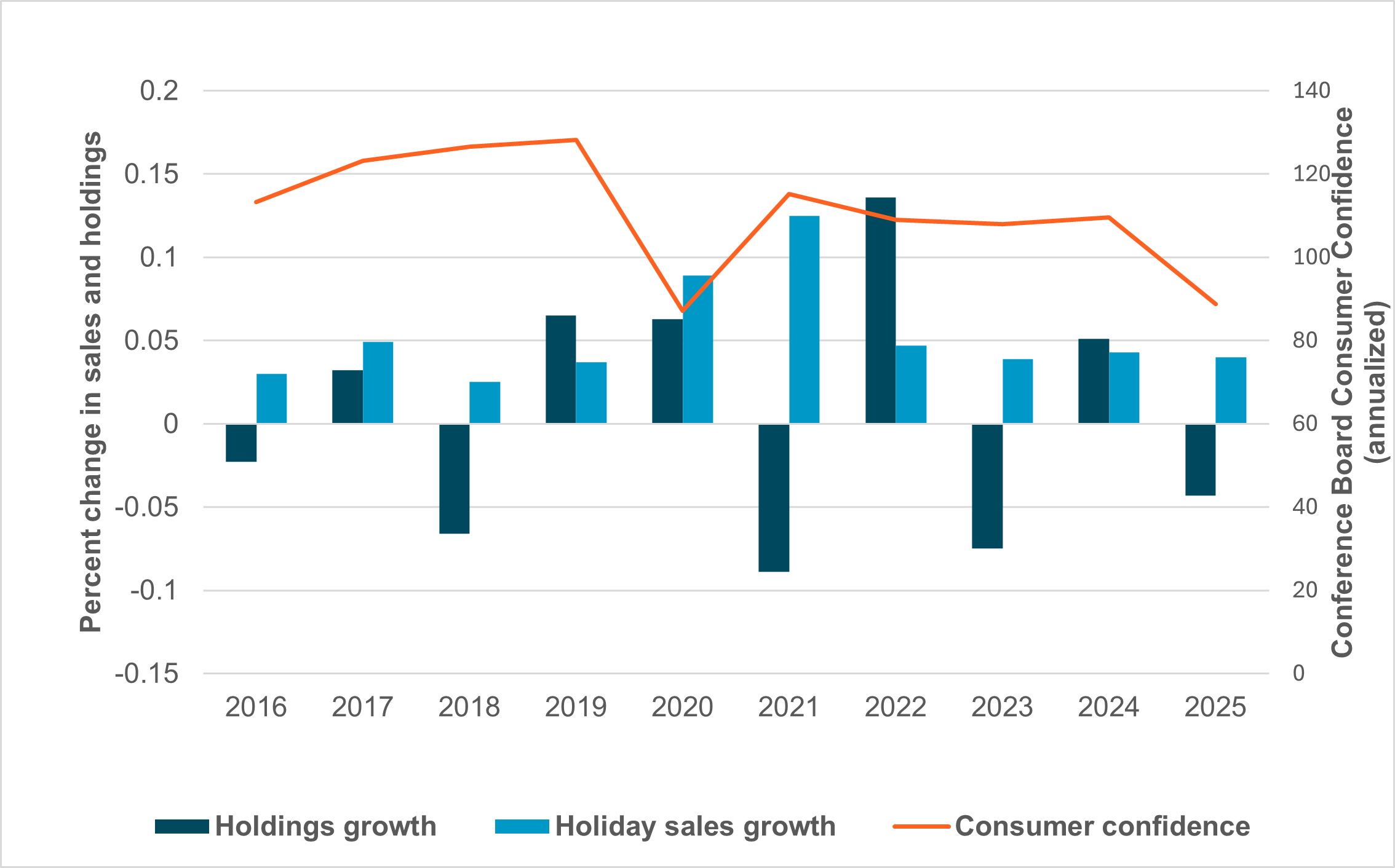

EXHIBIT #1: U.S. HOLIDAY SALES AND IFLOW RETAIL INDUSTRY HOLDINGS CHANGE

Source: BNY, NRF, Bloomberg

Our take: The National Retail Federation (NRF) estimates that 2025 holiday sales will grow 4% y/y to a record $1.015tn. The history of holiday sales and actual retail industry stock holdings is uneven. As Exhibit #1 highlights, consumer spending doesn’t necessarily translate into retail stock price gains or investor buying. What does seem to matter is consumer confidence. In the past three instances when growth outlooks were upbeat but didn’t match holdings, consumer confidence was higher. Our iFlow holdings data show that investors are more pessimistic than retail companies about 2025, and this time most consumer sentiment surveys agree.

Forward look: The risk for 2025 has been described as a repeat of 2018, where the year ends with equity selling, not buying. The question for investors now is whether Cyber Monday and additional retail guidance will lead to a downside surprise. This divergence matters, and it’s driving volatility across all markets.

U.S. economic data still insufficient to call 2026

EXHIBIT #2: CORE PCE INDEX COMPONENTS

Source: BNY, Bloomberg

Our take: We are finally starting to get some government data, but the flow remains more of a trickle than a flood. The rooster of this week’s economic events remains somewhat limited ahead of the December 10 FOMC meeting. Most of this week’s insights will come from non-official sources, but they remain meaningful for gauging where the economy is heading into the rate decision.

The Institute for Supply Management (ISM) produces its manufacturing PMI on Monday. Given the mixed regional PMIs so far, expectations for the ISM survey are similarly divided. Most observers expect the headline print to remain below 50, indicating contraction, but the subindices matter just as much. Prices, employment and new orders will help frame the inflation, labor market and production pictures as we head into 2026. The ISM services PMI follows on Wednesday, with expectations pointing to a mildly expansionary topline number. September’s PCE deflator, due Friday, will likely be too moderate and too stale to influence FOMC votes.

Forward look: This week’s ADP and jobless claims are unlikely to sway the FOMC undecideds. Weekly jobs data had been weakening through late October. Would another poor print increase the odds of a Fed rate cut? After last week’s downbeat – but not decisively weak – Beige Book, it would likely take a significantly soft ADP print to shift any of the hawks. However, it could provide enough cover for undecided members to support a rate cut.

EMEA: ECB’s hawkish tilt amid stubborn inflation

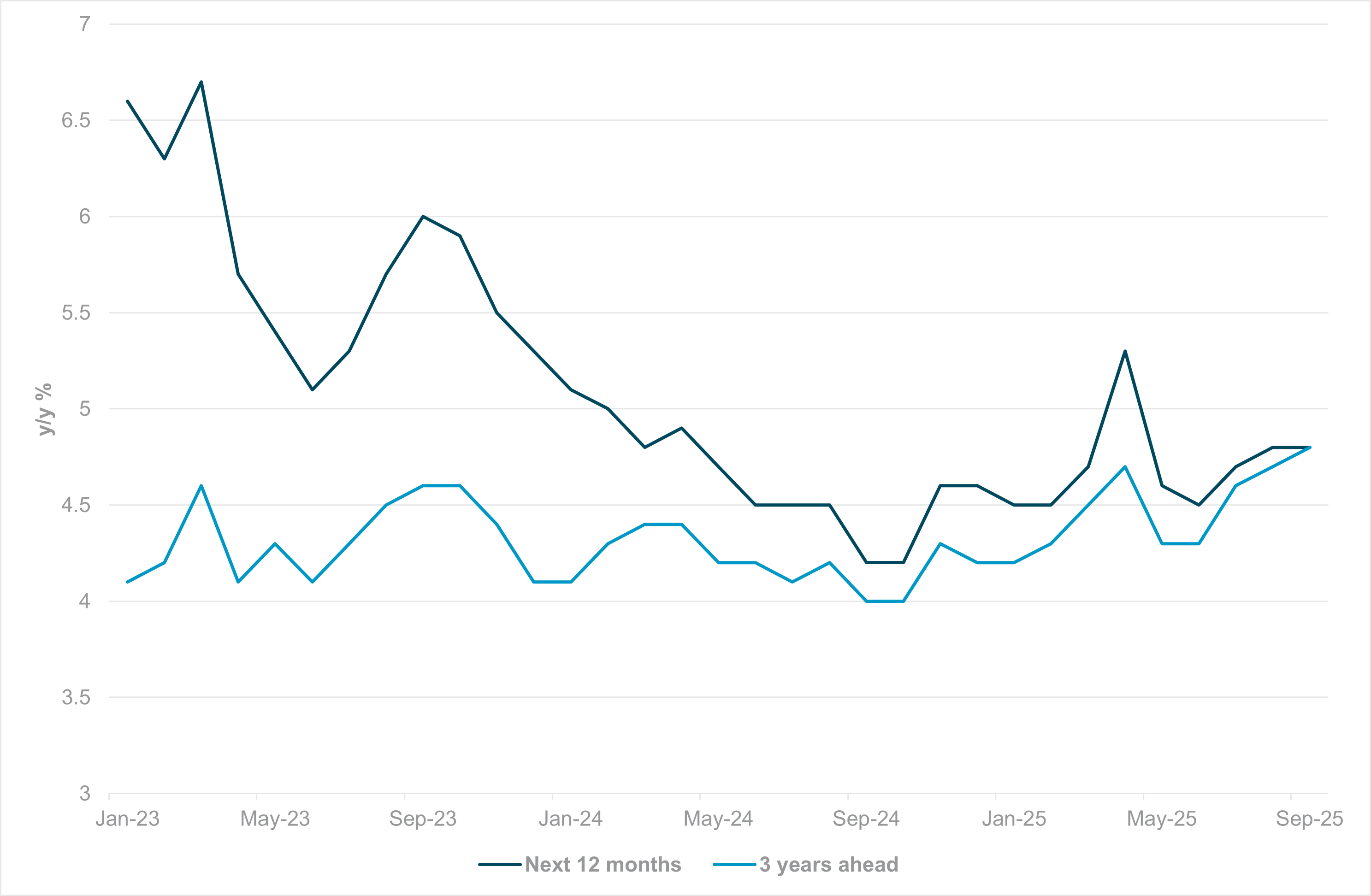

EXHIBIT #3: EUROZONE HOUSEHOLD INFLATION EXPECTATIONS, NEXT 12 MONTHS AND 3 YEARS

Source: BNY

Our take: Preliminary November inflation figures are due this week, and European Central Bank (ECB) hawks appear increasingly confident of vindication. Governing Council member Gabriel Makhlouf recently signaled that if the ECB were to revise the balance of risks, it could be to the upside, citing services inflation as “higher than it should be” and expressing concern about food inflation. Furthermore, the ECB is no longer alone in this respect, as more G10 central banks are on the cusp of changing their bias, given that inflation is no longer materially declining.

Crucially, non-tradables are driving the shift, while the Eurozone itself is seeking more public investment. Any productivity gains are likely to be backloaded or limited in size. As a result, the ECB will likely err on the side of upside inflation risk, even as activity data, particularly in production, continues to deteriorate. There are also signs of de-anchoring, with a notable rise in forward inflation expectations among Eurozone households. In the near term, a peace deal in Ukraine could help reduce asset risk premia, but we doubt energy links will be re-established soon, if ever. Therefore, any hope for a supply-based disinflationary shock is misplaced.

The National Bank of Poland (NBP) decision is the only EMEA central bank meeting this week, and we expect a pause, as policy tensions grow between the central bank and the government. The IMF has even called for 4% of GDP in fiscal consolidation, but this will likely run counter to the government’s program, thereby restricting policy space.

On the positive side, wage growth is falling materially, though still above inflation, and recent activity data point to accelerating demand. Following earlier easing and renewed fears of price growth due to fiscal spending, Poland’s real rates outlook has deteriorated, putting pressure on currency holdings. High underlying asset holdings have only increased hedging interest – though on the positive side, there appears to be little liquidation risk for now. A hawkish message risks a political backlash, but we expect the NBP to stand firm on price stability and hold below 4.25.

Forward look: The ECB’s Governing Council members will continue speech rounds in the coming days, and we expect broad affirmation of unchanged policy settings at the December meeting, barring major inflation surprises.

In the U.K., the market will continue to absorb the budget’s impact, but we caution against overinterpreting its effect on monetary policy. Most of the demand-related measures (i.e., directly impacting household income) are backloaded and won’t affect the Bank of England’s (BoE) immediate outlook. Meanwhile, U.K. data show clear signs of deterioration, so on balance, any fiscal consolidation supports policy easing, even if the BoE would have preferred more active spending cuts.

APAC: Regional PMI, Inflation, Australia’s Q3 GDP, Japan’s household spending & RBI

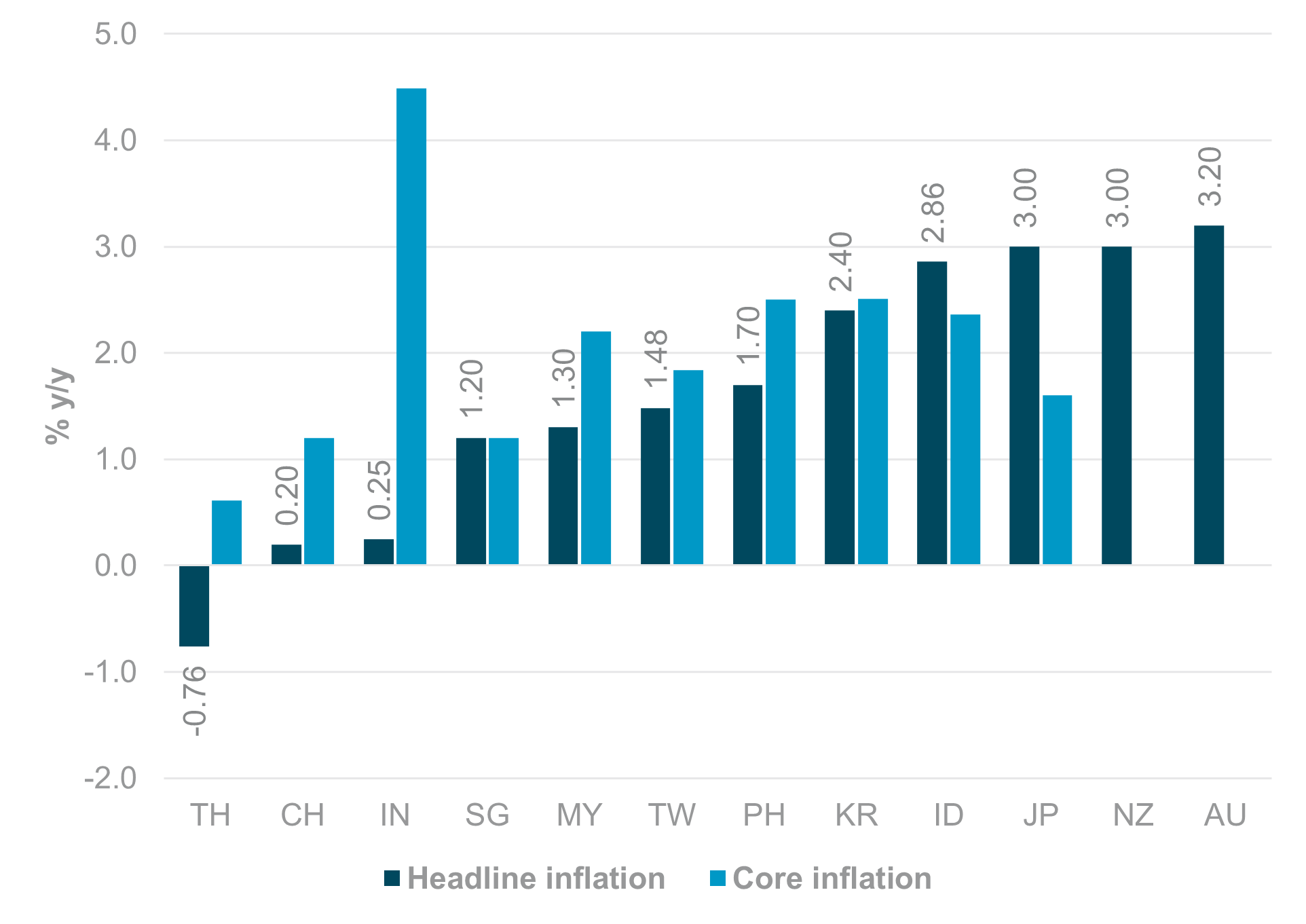

EXHIBIT #4: SHEADLINE AND CORE INFLATION IN APAC

Source: BNY, Bloomberg

Our take: In the Asia-Pacific (APAC) region, key focus areas this week include the release of the November Purchasing Managers’ Index (PMI) figures, regional inflation data, South Korea’s November trade results, and October export numbers from both Indonesia and Australia. Additionally, South Korea and Australia are set to announce Q3 GDP figures, while the Philippines will report October lending data. Singapore will report October retail sales while Japan is scheduled to release both the November consumer confidence survey and October household spending statistics.

Regional November PMI outcomes will serve as effective indicators of market sentiment. Key influences include sustained improvements in global trade – most notably the extension of the one-year U.S.-China trade truce – and recent equity market volatility tied to asset valuation concerns and significant foreign equity outflows. We are closely monitoring whether South Korea’s recent contraction in PMI is an isolated event or signals continued downward momentum. Taiwan and Malaysia are expected to demonstrate further improvement in PMI sentiment, having recorded 47.7 and 49.5, respectively, in prior readings. Overall, we believe that the most challenging period has passed. However, the pace of growth normalization will depend on external factors, such as global trade conditions and domestic policy support.

Regional November CPIs are expected to remain at the lower end of their respective ranges, supporting accommodative policy measures. Notably, India has experienced a sharp decline in food inflation, resulting in near-zero headline inflation but elevated core inflation, producing an unusually wide and divergent inflation profile. The RBI meeting this week is expected to provide further insight into these developments. Across APAC, we do not expect the short-term inflation trajectory to affect the current dovish policy outlook.

In Australia, market response to Q3 GDP data may be asymmetric: a downside surprise could revive expectations of rate cuts, while a positive result is unlikely to shift the current neutral outlook. Finally, Japan’s October household spending and November consumer confidence figures will be closely monitored, as they could support the case for a Bank of Japan rate hike at the December policy meeting.

The Reserve Bank of India is scheduled to meet this week. The evident deceleration in economic growth may prompt the RBI to extend its easing cycle, following its decision to maintain rates at the August and October meetings.

Forward look: Market liquidity is expected to remain thin, making conditions more prone to volatility during the remaining trading weeks of the year. External developments and investor flows dynamics continue to exert significant influence on regional currencies – particularly the South Korean won (KRW) and Taiwan dollar (TWD), which, in our view appear oversold and misaligned. The risk of heightened depreciation expectations is rising for several regional currencies, including the KRW, TWD, Indian rupee (INR) and Philippine peso (PHP). These concerns are being addressed by prompt policy responses, including central bank interventions. The anticipated revival of capital flows into the APAC region – driven by economic recovery, sustained demand for semiconductors and supportive policies – is likely to benefit both domestic equities and currencies. That is, unless the Fed takes an unexpectedly hawkish stance, which could place upward pressure on the USD.

As markets enter the final month of the year, investors face a landscape defined by fading seasonality, diverging global policy paths, and increasingly asymmetric data risks. December will center on whether incoming growth and inflation data can sustain the delicate balance that has supported risk assets despite weakening fundamentals. A shift in Fed rate-cut expectations, whether triggered by softer consumer data or geopolitical catalysts, remains the key swing factor for cross-asset volatility. With liquidity thinning into year-end, even modest surprises may drive outsized market reactions. Institutional investors should position for persistent two-way risk, maintain disciplined diversification, and prepare for an early-2026 environment, where policy direction, earnings resilience, and consumer momentum will shape the next leg of global market performance. USD exceptionalism is evolving into a more relative race – to sustain rather than outshine. Sentiment in APAC and EMEA is stronger than in the Americas, making diversification a clear opportunity for investors.

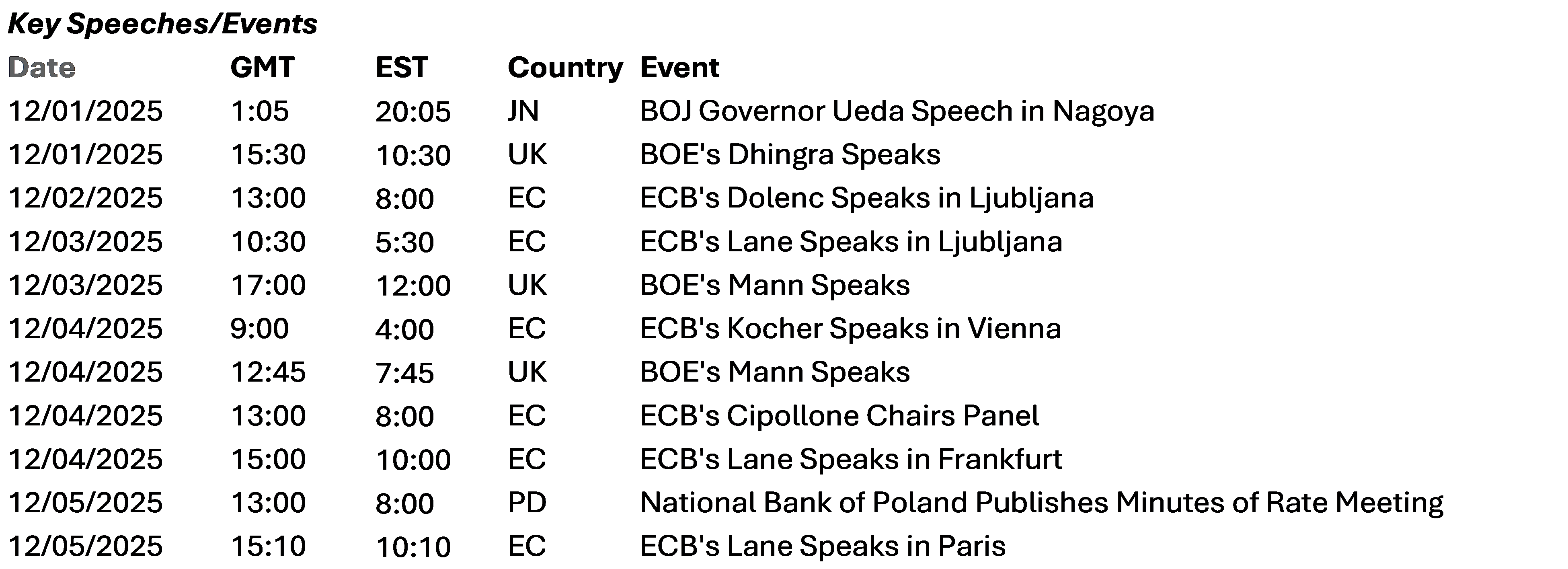

Central bank decisions

India, Reserve Bank of India (RBI) (Friday, December 5): With strong signs that economic growth is slowing, we expect the RBI to lower interest rates by 25bp to 5.25% to help stimulate the economy. The headline inflation rate is low at 0.25% y/y, which supports this move, though rising core inflation is a concern. While a weaker rupee could argue against easing, history suggests otherwise – the RBI reduced rates in February 2025 despite the USDINR reaching a record high of 87.43.

Poland, National Bank of Poland (NBP) (Wednesday, December 3): Fiscal dominance is becoming a key theme in policy expectations, affecting rate trajectories from Japan to Brazil. Central and Eastern Europe is at the forefront of such discussions. Even the IMF has warned that fiscal expansion now threatens Poland’s growth path. While the IMF’s call for 4% of GDP in cumulative fiscal adjustment could lower the terminal rate outlook, the NBP will likely take a more conservative stance and push back where possible. Monetary Policy Council member Wiesław Janczyk said there was room “for a small rate cut” in the near future, but consensus will likely favor a hold.

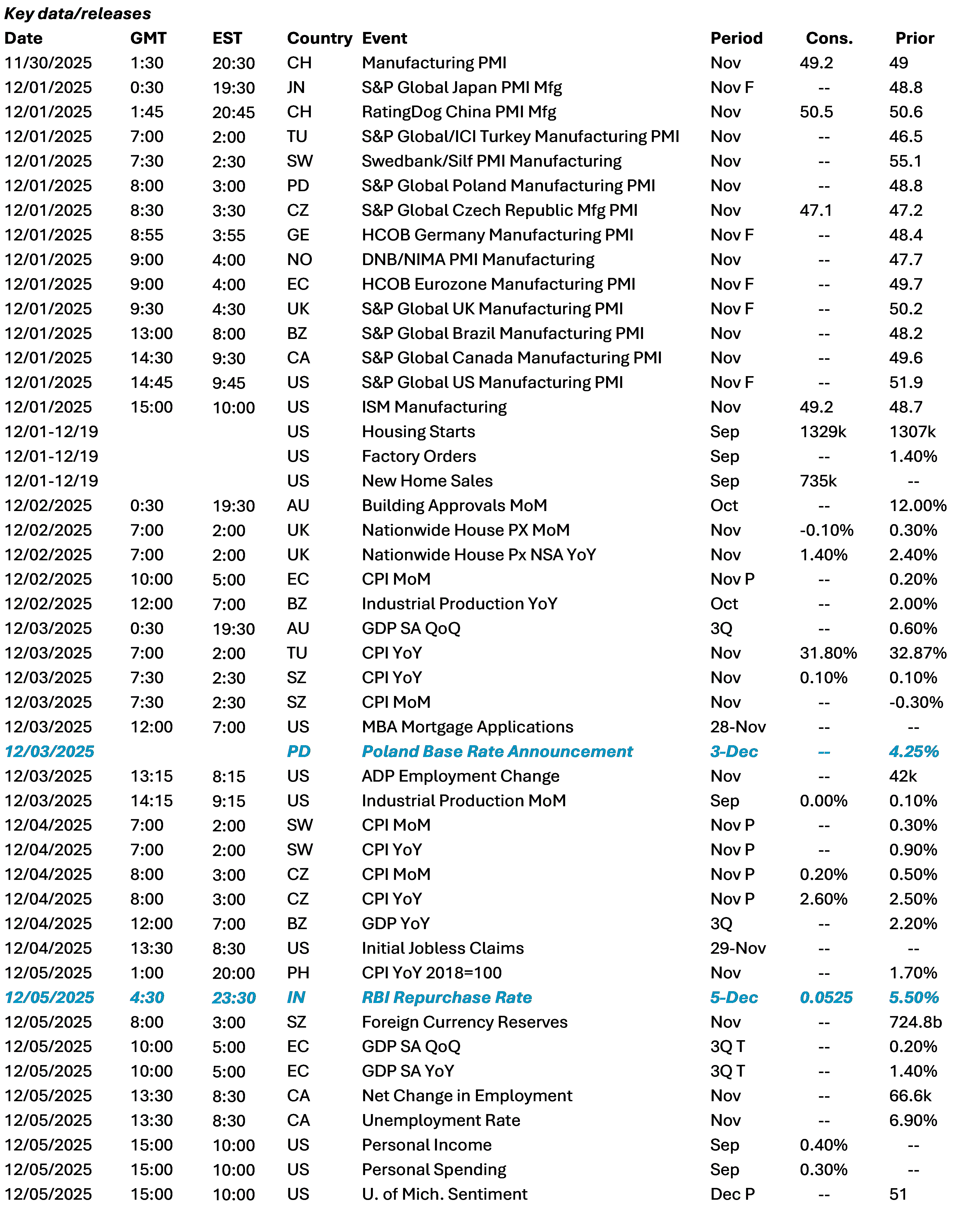

Data Calendar

Event Calendar