Falling Behind

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

Clocks in the U.S. were turned back this weekend, but markets leaped forward. Technology shares led after a week of big events, including the U.S.-China trade détente, another FOMC rate cut and Nvidia achieving a market capitalization of $5tn. Hanging over all these events like a cloud was a month-end funding squeeze. Companies continued to borrow significantly, with $80bn in investment grade issuance in the United States in the last week of October, led by Meta’s jumbo $30bn six-tranche deal to help fund AI capex spending.

We expect issuance to be a healthy $55bn this week and $120bn for the month of November. This puts the spotlight back on U.S. markets as the Supreme Court hears arguments on the legality of Trump’s tariffs and the implications for the U.S. deficit. Interest rates around the globe are being influenced by a number of events. These include ongoing budget discussions in the U.K. and France, the U.S. government shutdown and the possible end of the Senate filibuster, as well as central bank decisions from Australia, Brazil, the U.K., Mexico and Sweden.

The key market themes revolve around secular AI Investments and their role in driving valuations, conflicts with easier monetary policy and fiscal spending. Corporate layoffs, sticky global inflation, ongoing supply chain and commodity tightness and significant political uncertainty in the month ahead are tempering expectations of a buoyant equity market as we move into the end of 2025. The risk this year may be how financial conditions impact consumers. Usually, trouble has a way of making itself known when no one is worried about. The circular relationship between stocks and the real economy may be the key factor as we approach year-end.

Will the market rally on Fed cuts or reduce leverage?

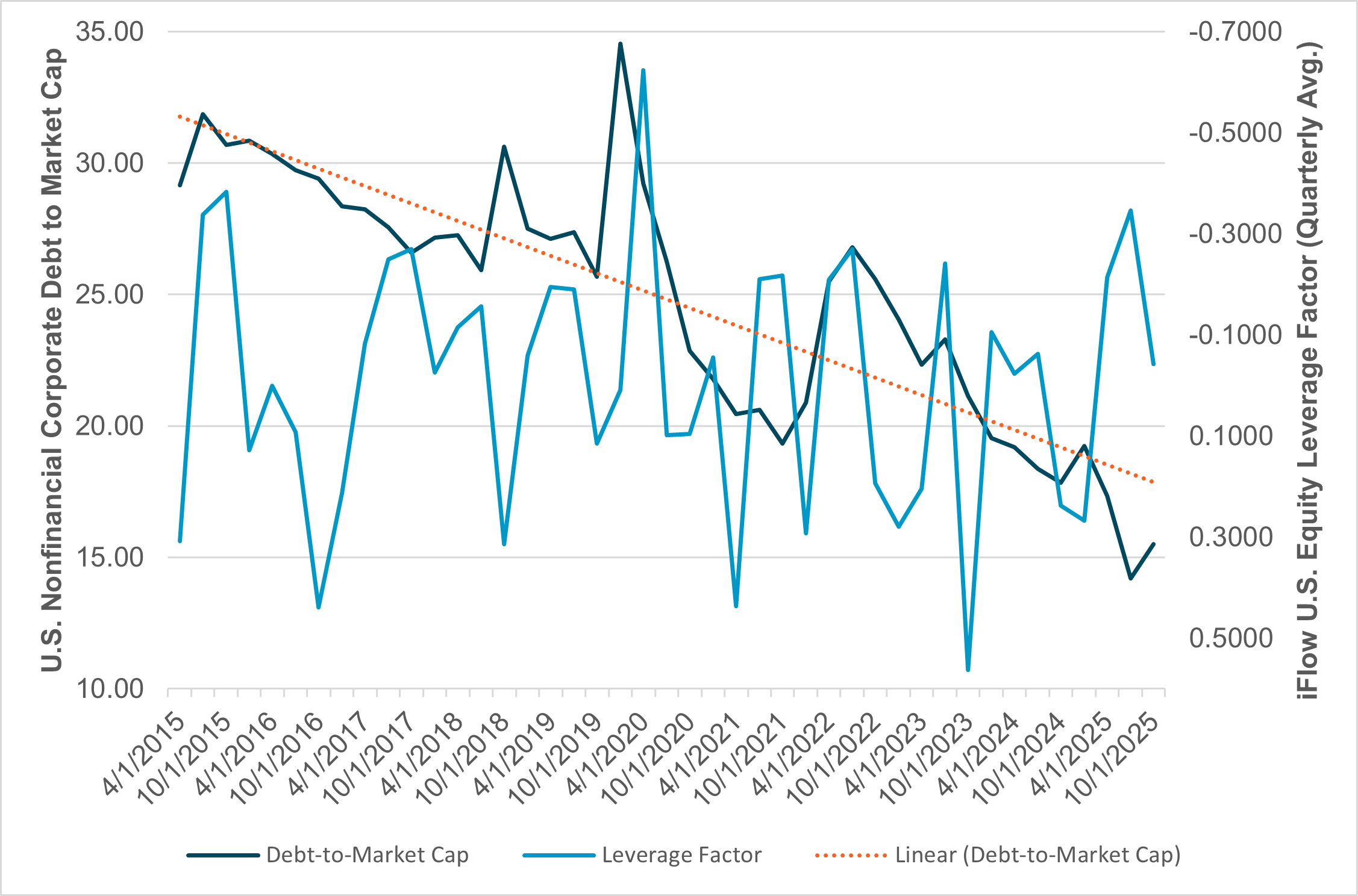

EXHIBIT #1: RATIO OF U.S. CORPORATE LEVERAGE TO IFLOW EQUITY LEVERAGE FACTOR

Source: BNY, FRED

Our take: Investors remain concerned about a market bubble, but our iFlow data suggest there is still room to run. The leverage ratio is near the long-term average, while nonfinancial corporate debt-to-market capitalization, a measure used by the Fed and others, is bottoming out. Concerns about risk are being driven by the surge in repo and other borrowing costs in the U.K., EU and U.S. markets in 2025. Are rising debt burdens sustainable if markets continue to melt up?

The correlation of our leverage factors to the overall corporate leverage trend is significant but not sufficient to necessitate a larger move. Historically, extremely low leverage ratios point to a stock market bubble, which usually leads to a recession, while high ratios indicate stagnant growth and inflation. On average, the ratio of corporate leverage to market capitalization was 77% from 1970 to 1990.

Forward look: Leverage concerns as companies borrow to grow may risk a squeeze-out of government borrowing, driving up borrowing costs. While fiscal dominance concerns are normal in emerging markets, they are not common in developed ones. Credit markets show that investment-grade spreads remain immune to such turning points, but that does not mean there are no doubts about credit. The more immediate concern for stocks and bonds revolves around cash.

Liquidity could be the key issue for unfettered leverage in Q4, as revealed by month-end rates, but this will be a greater concern in the financial sector than in high-tech. As the Fed recognized when it decided to end quantitative tightening (QT), reserves have gone from abundant to ample. For now, concerns about borrowing to invest in AI capex is seen as a secular rather than a cyclical one. Given the strength of Magnificent Seven earnings in the third quarter, the path ahead for November trading should be about normalizing risk as investors shift from defensive to normal positioning. For the week ahead, U.S. exceptionalism could once again be a theme, with a stable USD, higher rates and even higher U.S. equities.

U.S. focus on the economy and government shutdown key

EXHIBIT #2: U.S. ADP DATA AND NONFARM PRIVATE (NFP) PAYROLLS

Source: BNY, Bloomberg

Our take: We would normally expect jobs data at the end of the week, but if the government does not reopen we will be looking elsewhere for economic clues. The Institute for Supply Management produces its manufacturing and services PMIs on Monday and Wednesday, respectively, and these surveys have a plethora of information on business sentiment, inflation at the firm level and employment intentions. The University of Michigan Sentiment Survey on Friday will provide similar insights from the household perspective.

The ADP private payrolls data out on Wednesday, having been cited by Fed Chair Powell in his post-FOMC press conference last week, will be one of the more watched labor indicators. Exhibit #2 shows that a 4-month moving average of the ADP monthly data gives comparable results to the official NFP data for private jobs growth, and the most recent indications have confirmed our concerns about labor market weakness.

Forward look: Regarding the shutdown, Senate Republicans last week discussed the possibility of ending the filibuster so they can pass their continuing resolution with a simple majority. This could happen during the week, but even if it did it would not allow the data releases to start flowing right away. Also on the government docket next week, the U.S. Supreme Court hears arguments on the Trump Administration’s tariff policy. Although a decision is not likely to come until the end of the year, markets could get a taste of the Supreme Court’s orientation on the matter.

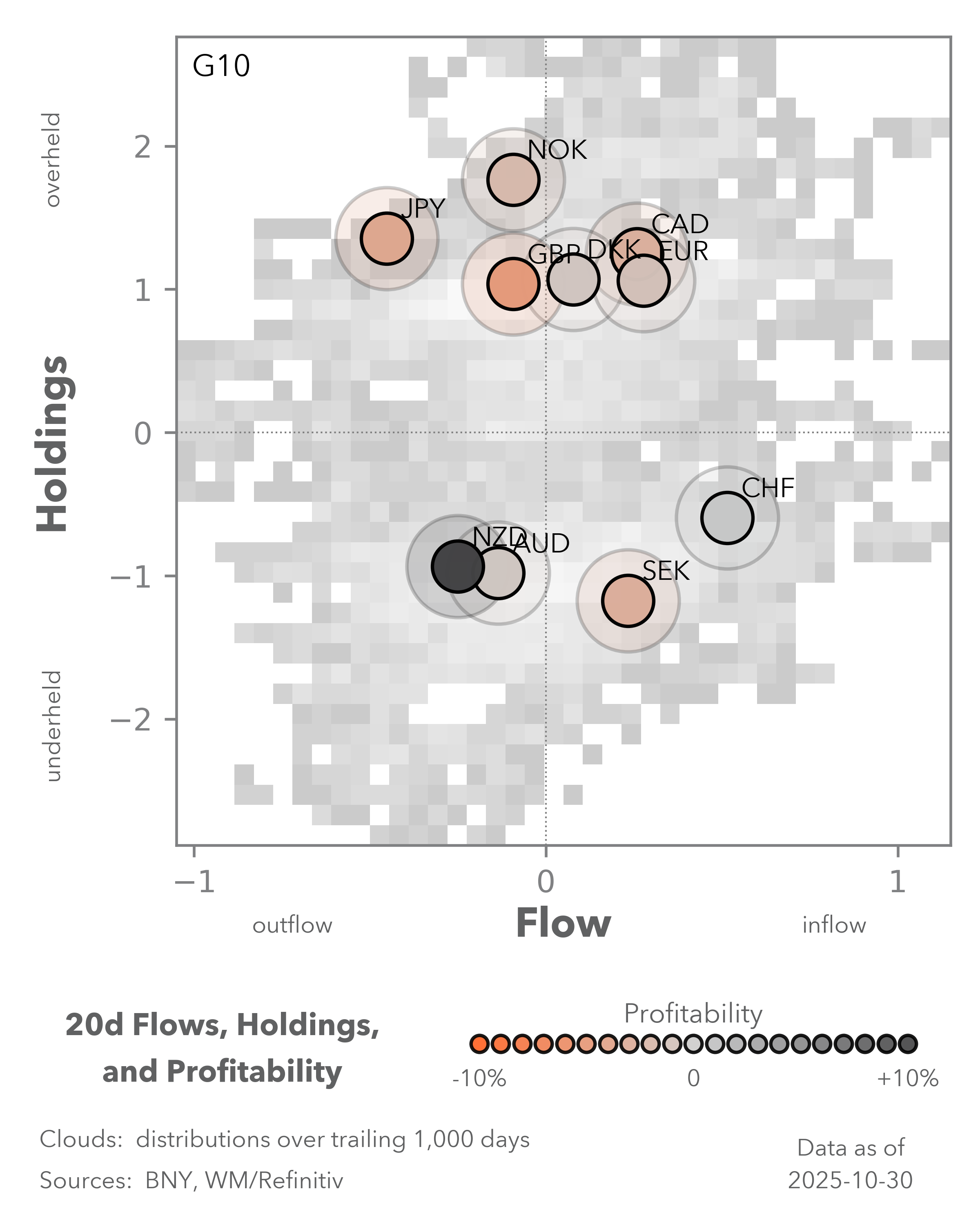

EMEA: Riksbank, Norges Bank and BoE to take stock of domestic conditions

EXHIBIT #3: CROSS-BORDER HOLDINGS OF GBP, SEK AND NOK

Source: BNY

Our take: Any lingering hope for the ECB’s doves to make their case for a December cut have been dashed by the preliminary October PMI prints. The reported noted that growth was recorded across both key sectors, and led by services where the latest increase in business activity was the strongest since August 2024. However, the inflation outlook was mixed: input price growth softened for both goods and services, while “manufacturers increased their selling prices for the first time in six months, joining the services sector in recording inflation. Service providers raised charges at a solid pace that was sharper than seen in September.” This would be seen as a good environment for corporate earnings, as lower costs, but increased output prices can help with ongoing margin expansion. The ECB will clearly take the output view more seriously and stress the need to anchor price expectations. Meanwhile, if input costs are also falling or not registering strong growth, central bankers may also argue that there is little need for relief through easier financial conditions via the interest rate channel. President Lagarde’s post-decision press conference will likely reiterate the notion of the Eurozone being in “a good place,” but for now there is only a need to pay some lip service to downside risks from supply shocks and domestic demand.As the global economy attempts to look forward to a more sustained period of trade calm, there is no guarantee that Europe can benefit much from its own preferential trade deals with the U.S. and more benign global conditions. The EU looks set to step up its talks with China over bilateral issues surrounding supply chains and there is a clear risk of material damage to output in the automotive sector, which has finally managed to show some signs of stability this year as it moves to boost competitiveness in the face of relentless Chinese competition uncertainty over the investment and market outlook for electric vehicles.

However, on a domestic basis the central banks of Sweden, Norway and the U.K., all of which will decide next week, esoteric issues continue to frustrate. Norway and the U.K. now have rates that match the Fed’s but there is little sign that there will be convergence in trajectories given stubborn domestic inflation figures. Sweden is in a different position, with inflation comfortably below target, but pushing aggressively below ECB levels is also a gamble for the Riksbank, which remains uncomfortable with SEK valuations despite the year’s gains. The surprising strength of the Eurozone economy will only consolidate ECB expectations in this context.

Forward look: All three central banks will remain on hold but signal that further easing is possible and even desirable, even though markets expect all three to stay on hold for the rest of the year. For now, our data indicate that asset allocators remain most comfortable with NOK holdings. SEK’s current yields preclude a material reduction of hedges, whereas the BoE will cut aggressively at the earliest possible opportunity, not just for domestic growth purposes but also to ensure that the impending market challenges to the country’s fiscal outlook take place with front-end rates and liquidity conditions as accommodative as possible.

Otherwise, ECB members will be active, with the blackout over and the latest growth prints will affirm the “good place” refrain from Governing Council members. With preliminary October CPI numbers also showing no sign of a downward drift in prices and leading indicators only pointing to marginal contraction up ahead, the case for easing is very limited, but Governing Council members will likely retain optionality to avoid the impression that the central bank judges Eurozone’s growth cycle to be decoupling from global conditions and sees policy cycles diverging accordingly.

APAC: Summits galore but asset allocation stays defensive

EXHIBIT #4: RESILIENT CHINESE EXPORTS SUPPORTED BY ASEAN TRADES

Source: BNY

Our take: The focus in APAC this week will be on October exports and regional manufacturing PMI releases, inflation and FX reserves data. We will also see data on Indonesia’s Q3 GDP, Taiwan’s October exports, Thai consumer confidence and bank lending in the Philippines.

There are broad expectations of a slowdown in regional exports after heavy front-loading activity failed to materialize in the first half of the year. China and APAC as a whole continued to see strong export growth in the third quarter, and export data releases from China, Taiwan and Indonesia this week should provide confirmation of this trend. As Exhibit #4 shows, Chinese exports to the U.S. have declined significantly since April following renewed tariff tensions and are down –27% y/y as of September, following an increase of 12.4% at the beginning of the year.

Meanwhile, exports to ASEAN countries have picked up sharply, climbing by 15.8% y/y (14.7% year-to-date y/y as of September). Regional October PMI manufacturing sentiment may be dampened by October market volatility, as revealed by the sharper-than-expected decline in China’s October PMI at 49.0. That said, our view is that Taiwan, the Philippines and Malaysia will eventually drift back into expansionary territory. As for inflation, the overall disinflationary trend, driven primarily by lower crude oil prices, will likely continue. However, low inflation is no longer the primary factor for domestic monetary policy-setting. Regional central banks are increasingly focusing on financial market stability, as demonstrated by high levels of household debt and the need to curb excessive currency depreciation. Elsewhere, Australia will release its September household spending and trade data. While such data is useful, it will be overshadowed by Reserve Bank of Australia’s policy meeting. New Zealand’s Q3 unemployment rates and average hourly earnings will be closely watched ahead of RBNZ’s policy meeting at the end of the month. Japan’s real cash earnings should provide ongoing motivation for BoJ to keep its tightening stance even though it left its target rate unchanged at 0.5% in October.

On the monetary policy front, the Reserve Bank of Australia is widely expected to keep rates unchanged at 3.6% following last week’s higher-than-expected inflation print. Bank Negara Malaysia (BNM) will hold its last policy meeting for the year this week. Steady growth momentum and a normalization of CPI suggest BNM will keep rates on hold for a considerable period.

Forward look: Overall, we are positive on APAC risks, especially in the equity complex, supported by the trade agreements and deals between the U.S. and countries in the region at the ASEAN and APEC Summit last week, solid sentiment in regional equity markets fueled by overall optimism in the tech and AI space, foreign equity inflow momentum in the region, except for China and India and ongoing government efforts to stimulate growth via monetary and fiscal easing and regulatory changes. China has unveiled a plan to streamline qualified foreign investments by easing access requirements, improving efficiency and expanding investment options to attract more long-term foreign capital. However, there are some residual headwinds, such as the ongoing U.S. government shutdown and near-term market volatility given the reassessment of the Federal Reserve’s interest rate outlook.

Further trimming of rate cut expectations could lead to a rebound of the U.S. dollar and U.S. Treasury bond yields and thus raise overall global funding costs, which are negative for APAC. Within EM APAC, differentiation is in play. We are negative on INR (tariff concerns), MYR (fiscal concerns), PHP (aggressive easing bias) and THB (expensive valuation), but positive on CNY, KRW and TWD on potential capital inflows, and IDR on its attractive valuation and government commitment to keeping the deficit in check.

As markets transition into year-end, investors face a delicate balance between optimism over secular AI-driven growth and caution surrounding tightening liquidity and persistent inflation pressures. The interplay between corporate leverage, government borrowing and central bank policies will be pivotal in shaping returns through early 2026. While U.S. exceptionalism – anchored by robust earnings and strong consumer demand – continues to attract capital, the sustainability of this rally depends on liquidity dynamics and confidence in fiscal discipline.

In Europe, policy divergence underscores uneven growth trajectories, while Asia’s export resilience and deepening trade partnerships offer a potential counterweight to global headwinds. For investment professionals, positioning for 2026 means recognizing that markets are shifting from liquidity-driven expansion to fundamentals-led differentiation. Maintaining flexibility across asset classes, managing duration risk and identifying companies with strong balance sheets and credible AI-linked growth strategies may provide the best defense – and opportunity – in an increasingly asymmetric global landscape.

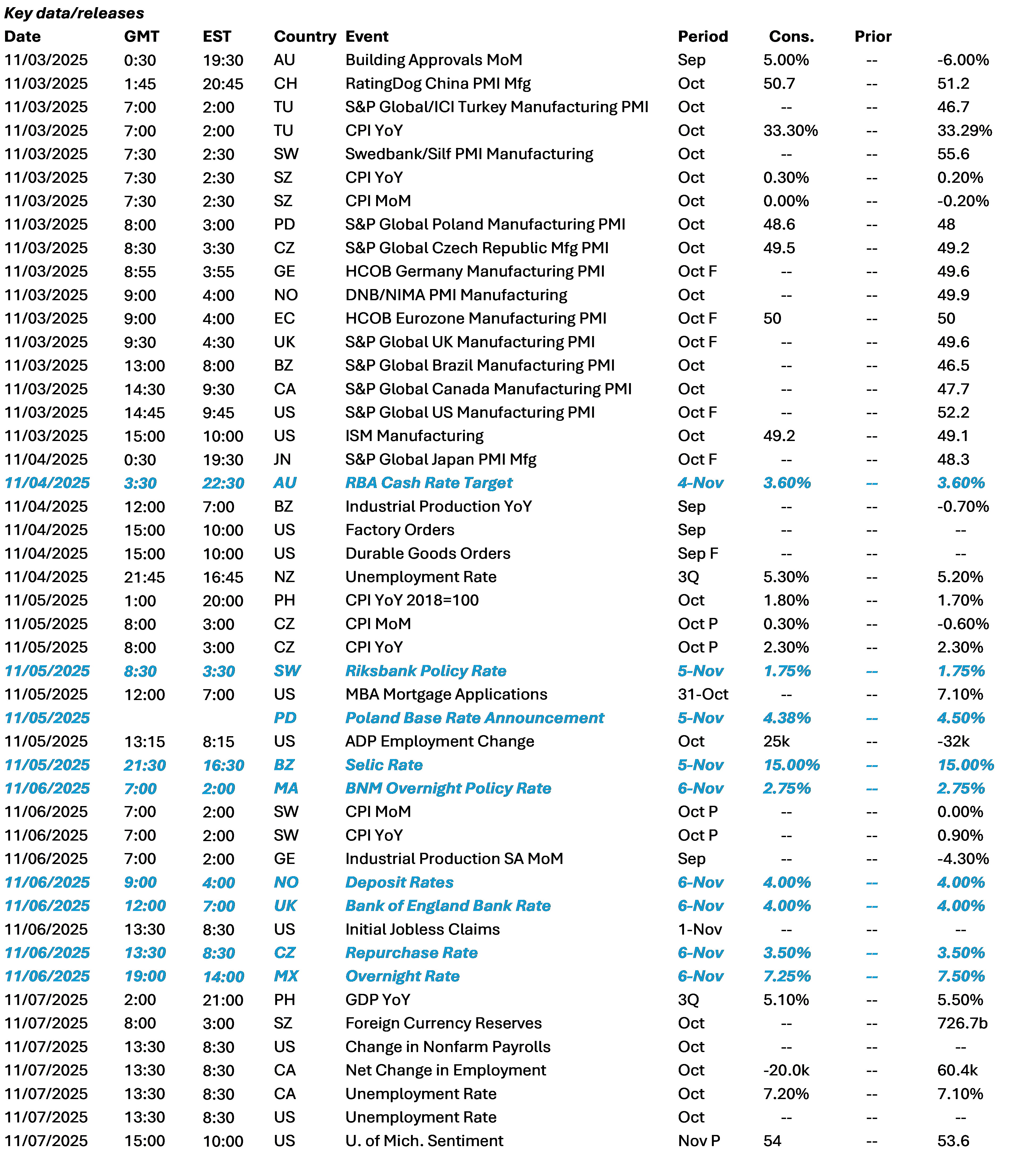

Central bank decisions

Central Bank Decisions

Australia, RBA (November 4, Tuesday) – The RBA is expected to keep its cash rate unchanged at 3.60%. While the labor market has shown clear signs of incremental weakness which would require additional policy support, inflation surprised to the upside in September and the Q3 print remains above 3.2%, with the quarterly 1% gain clearly risking a de-anchoring of expectations. Adding restraint to non-tradable sectors remains a policy priority in the near term, and we believe this should be better reflected in AUD valuations as well. Given the level of Australian asset holdings by cross-border investors, hedge ratios are still quite aggressive and there is scope for some relief, especially as policy differentials vs. the Fed continue to gain.

Sweden, Riksbank (November 5, Wednesday) – The market is not looking for any additional cuts by the Riksbank for the rest of the year, which was the broad message from the central bank at the previous decision. There may also be the sense that as policy divergence versus the ECB will be maintained or even widened ahead. Additional easing will come through the FX channel, despite Riksbank’s consistent view that the currency itself remains undervalued. Recent risk-aversion has helped the market view low-yielding funders more favorably, but with inflation well below target and registering flat changes sequentially, the risks are squarely tilted toward the downside. However, strong activity and leading indicators will support a pause for the November meeting.

Poland, NBP (November 5, Wednesday) – The NBP may ease rates again at its upcoming meeting as price momentum continues to disappoint. Sequential inflation is clearly pointing to target realization and there are obvious signs of wages softening as job losses continue. Retail sales figures also surprised materially to the downside in September, which points to demand retrenchment even though real wage growth is still comfortably positive and any preemptive easing does risk real rates falling too low again relative to economic conditions in the near term. However, our flow figures are picking up clear interest in hedging CEE exposures, and this will also tighten financial conditions at the margin.

Brazil, COPOM (November 5, Wednesday) – The Selic rate is expected to remain unchanged at 15.0% and with Fed Chair Powell signaling a December cut being far from certain, Latin American central banks will continue proceeding with caution as inflation continues to require strong anchoring. On the other hand, Brazil retains plenty of room in real rates – in the double digits based on PGBE and IGP-10 metrics – and where applicable, central banks may choose to optimize policy if growth risks continue to mount. The recent round of carry unwinding, however, is another warning for high-carry EM FX names that the risks remain for overhead names and sustaining FX stability is a necessity for policy as concern over valuations continue to rise.

Malaysia, BNM (November 6, Thursday) – We expect Bank Negara Malaysia to keep rates unchanged at 2.75% at November meeting and maintain an upbeat assessment amid continued growth momentum and normalizing inflation toward 2%. Our view is that BNM is done with easing measures and is unlikely to follow the path of the Federal Reserve. BNM’s latest macro 2025 GDP and CPI forecast are 4%–4.8% GDP (mid 4.4%), and 1.5–2.3% inflation (mid 1.9%), respectively.

Norway, Norges (November 6, Thursday) – Norges Bank will likely end the year with one of the highest rates in G10, if not the highest as capacity for easing remains very restricted and there is no relief whatsoever from inflation, which continues to run closer to 4% even with the global cycle continuing to weaken and terms of trade facing long-term deterioration. The policy outlook also benefits the currency’s strong current holdings status based on our custody figures. As underlying inflation is holding at 3%, there is scope for Norges to retain a dovish outlook, but we do not see much scope for the labor market to weaken and allow demand to adjust lower as well. Current activity levels are mixed but if there is clear deterioration in output we expect Norges to act again.

U.K., BoE (November 6, Thursday) – There will be votes for a rate cut again at the November meeting and despite the improvement in the CPI figure for September, we do not think there is sufficient support for easing to get a cut over the line. If anything, hawkish skeptics such as Mann on the Monetary Policy Committee have voiced alarm at the persistence of inflation and inflation expectations. This decision is also the last before the crucial end-November budget, when additional fiscal measures may also have an impact on price expectations. As a result, the BoE will need to deal with a new set of assumptions for their year-end meeting, at which a cut is more likely as long as inflation numbers are manageable. Some MPC members will argue that the BoE’s inflation focus is becoming too narrow for the needs of the underlying economy, but this will remain a minority view.

Czechia, CNB (November 6, Thursday) – The CNB is expected to keep the repo rate at 3.5% but there will be a tail risk of a cut as September inflation numbers surprised to the downside and showed deep sequential contraction. Given the industrial sector in the broader European Union continues to face critical challenges, the Czech economy will suffer from the aftershocks – the sector is contracting materially based on the latest figures and the CNB will be on standby to offer relief if needed. However, there is no evident sign of output weakness translating into demand softeners yet, and even real wages remain remarkably high by EU standards (5.3%y/y in Q2), so the CNB will need to continue to manage a balancing act.

Mexico, Banxico (November 6, Thursday) – Banxico is expected to cut rates to 7.25% as the contracting economy will require additional support, especially with trade relations with the U.S. still in a state of flux and weakness in the U.S. itself likely to have a knock-on effect. The Fed’s current stance is sufficient enough to give Banxico room to act while inflation continues to run below 4% on a headline basis, though core inflation is still higher at 4.28% for September. On a more favorable note, nominal wage growth fell sharply in September to 3.9% y/y from 7.3% y/y. The figure is one of the lowest in the last five years and should also give Banxico the confidence to act as the labor market is showing signs of softening enough to restrain demand. Conditions for duration remain favorable but additional easing will add to hedging pressures on MXN.

Data Calendar

Event Calendar