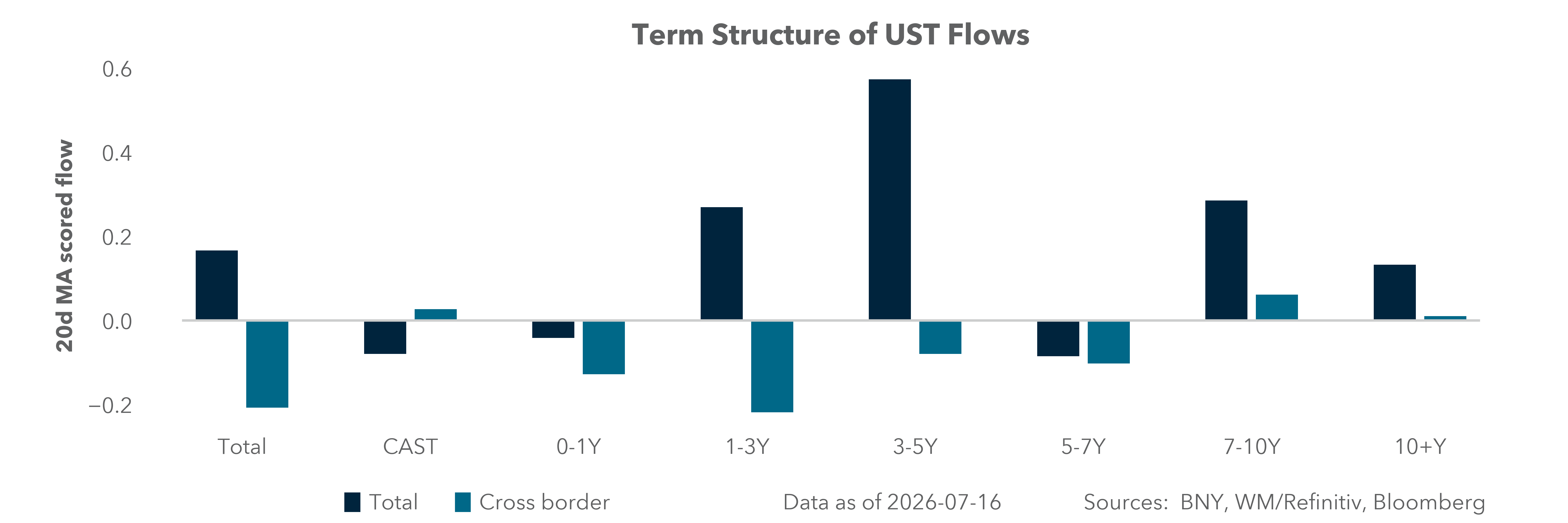

Central bank caution steadies tech volatility

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Geoff Yu

Time to Read: 9 minutes

Validation test: The week ahead tests whether data can stabilize markets before rotation turns into liquidation. The ECB stays on hold, with lower inflation reducing the urgency around further tightening, but European PMIs now carry the signal. The question is not whether Europe is strong but whether activity is stable enough to support the emerging value case in euro assets.

The U.S. faces the same test through Friday’s S&P PMIs, with manufacturing expected at 54.4. Markets need evidence that activity is holding up as inflation cools. Canada CPI matters for the Bank of Canada (BOC) pause story, but the U.S. growth signal is the cleaner global catalyst.

Carry vs. stress: Carry remains the main support. Rate differentials still work, LatAm balance-of-payments buffers remain solid, and Mexico’s retail sales, IGAE and bi-weekly CPI can reinforce the easing-with-carry setup. But carry needs calm markets.

Asia is the weak link. Inflation prints from Japan, New Zealand and Singapore, policy decisions at Bank Indonesia (BI) and on China’s LPR, trade data from South Korea and Taiwan, alongside regional PMIs, will test whether Asia’s export engine can offset softer domestic demand. Any break in technology flows turns Asia from a growth support into the transmission channel for global de-risking.

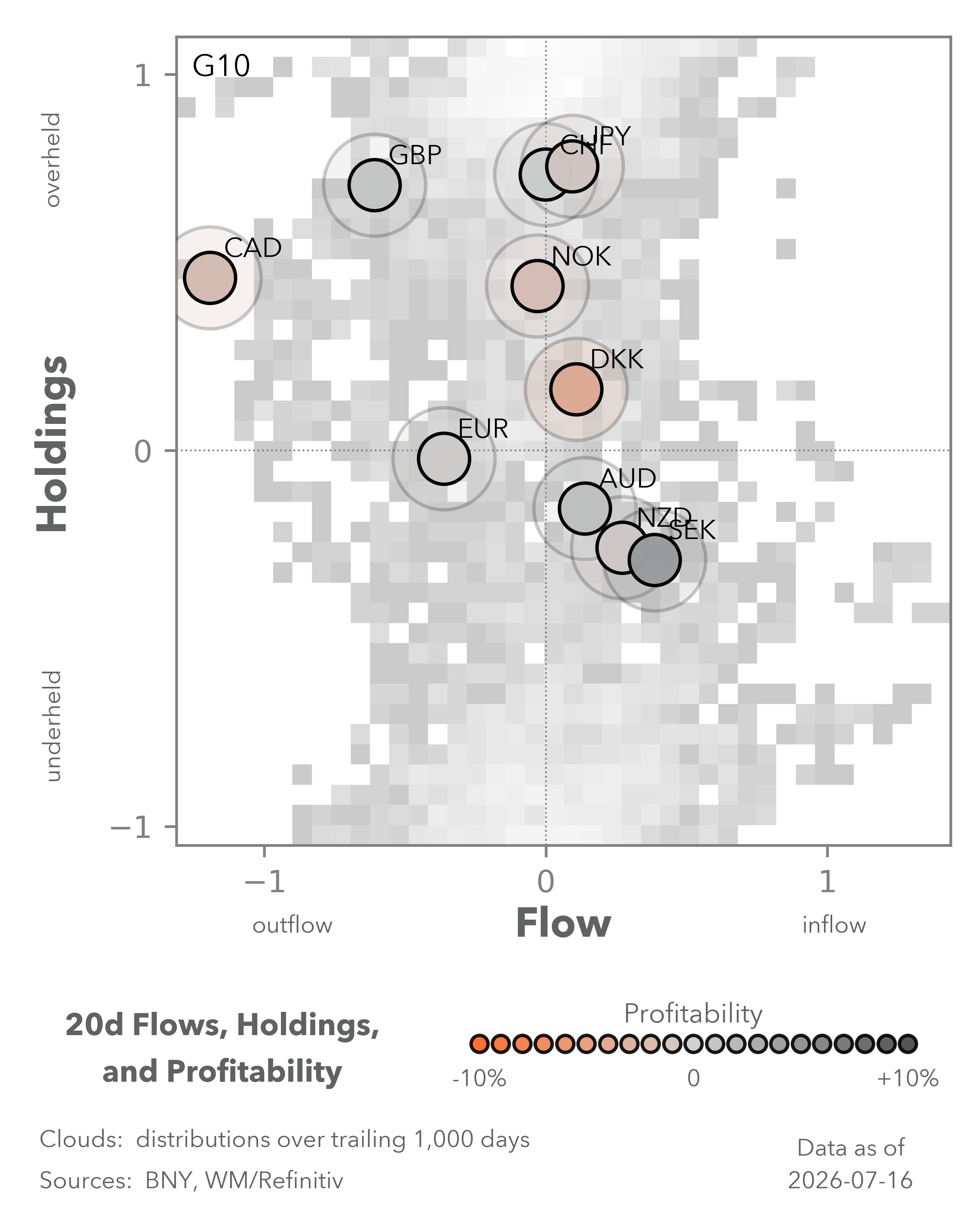

Tail risks: The Gulf remains the global inflation risk. Oil is already higher, and any supply or shipping shock quickly revives the energy channel. The U.K. adds a local credibility test as Andy Burnham takes office and cabinet appointments land, with the chancellor role central for sterling and gilts.

Turkey and South Africa rate decisions also matter for EMEA high-yield FX, but the larger issue is market tolerance for shocks when the Fed is in blackout and policy commentary is absent.

Bottom line: Orderly rotation remains the base case. Carry, an ECB hold and tentative European stabilization help. But the burden of proof has shifted. Markets need growth confirmation from PMIs and earnings; without it, Asia volatility, higher oil, U.K. political risk and Fed silence turn rotation into liquidation risk.

North America: U.S. inflation eases, markets turn to growth signals

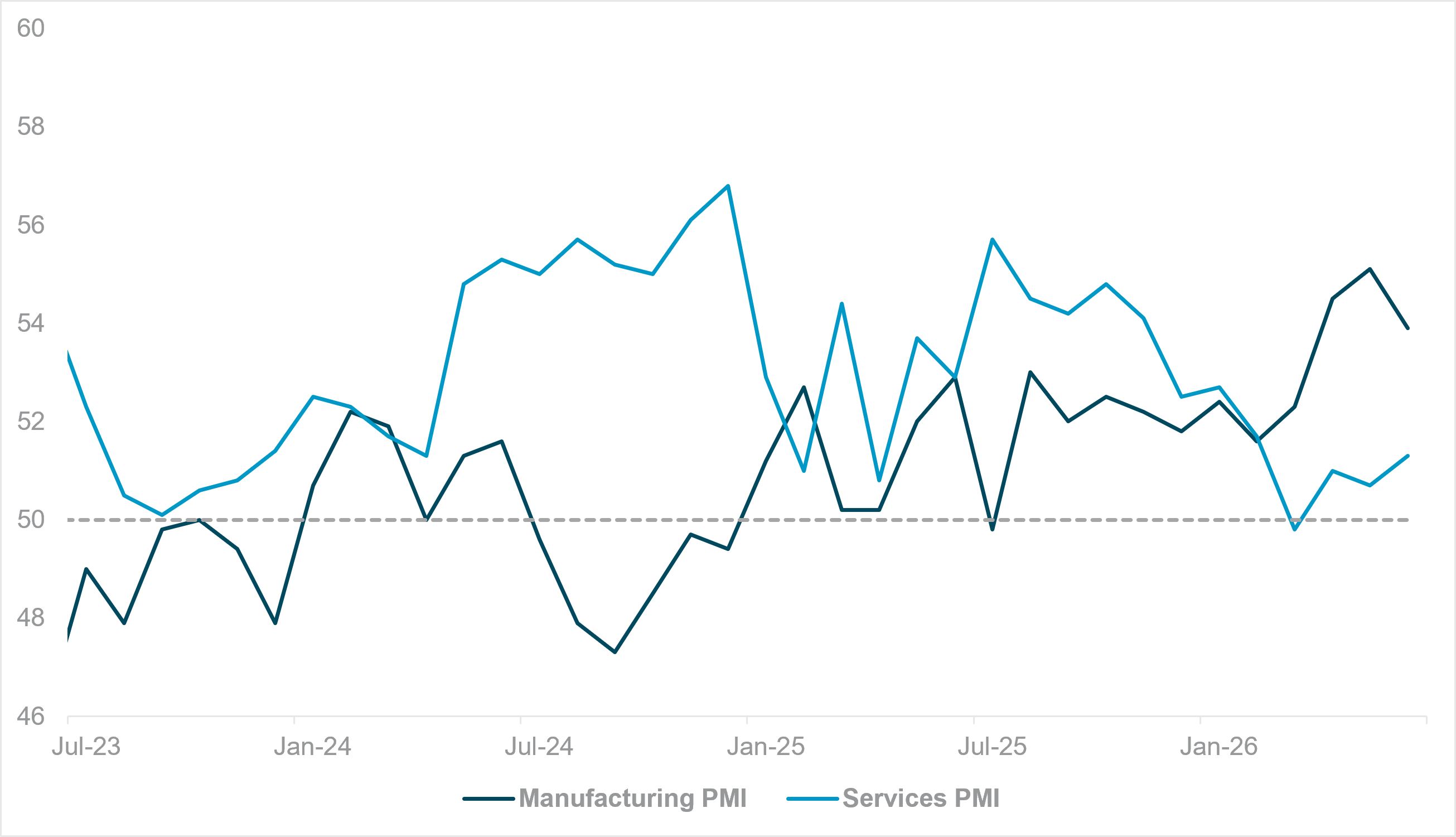

EXHIBIT #1: U.S. MANUFACTURING AND SERVICES PMIS

Source: BNY, Bloomberg

Our take: Last week’s softer-than-expected core CPI reinforced the view that U.S. inflation is cooling at the margin, easing some of the pressure on markets to price a more hawkish Fed path. Fed communication was active before the blackout period, but the speakers did not materially shift the policy backdrop. The BOC’s decision to hold rates steady kept the Canadian policy outlook on pause as well.

This week’s North American calendar is comparatively light. The main U.S. release is Friday’s S&P PMIs for manufacturing, services, and the composite, with manufacturing expected at 54.4. In Canada, CPI is the key print and is also expected to come in lower.

With the Fed now in a communications blackout after last week’s speaker-heavy schedule, there is limited scope for policy repricing from central bank commentary alone.

Forward look: The most important data point this week is likely the U.S. PMI suite – not because it will supersede inflation in market importance, but because it offers a timely read on whether activity is holding up alongside easing price pressures. A Manufacturing PMI print around the expected 54.4 would point to continued expansion and help confirm that growth remains resilient even as inflation moderates. That combination could be constructive for risk sentiment but could leave rates markets caught between softer inflation and still-firm activity.

Canada’s CPI will matter primarily for its implications for the BOC’s reaction function. Another downside surprise would reinforce the case that policy is already restrictive enough, supporting duration and reducing pressure for further tightening.

Overall, this week will likely be quieter, with the broader rates narrative still anchored by the softer U.S. inflation tone established last week.

EMEA: The ECB isn’t back “where we started"

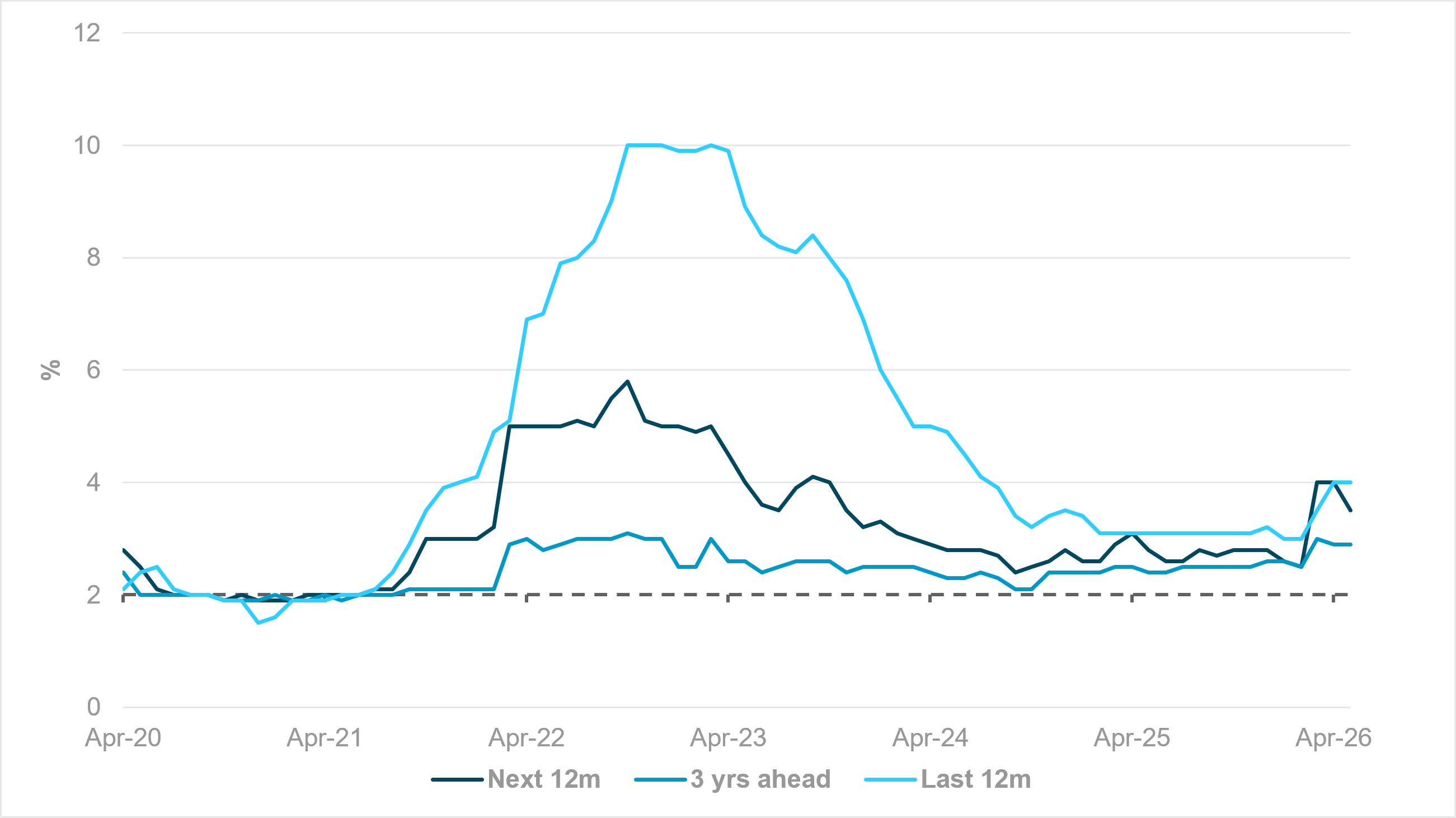

EXHIBIT #2: ECB INFLATION EXPECTATIONS SURVEY

Source: BNY, ECB

Our take: Expectations for the upcoming ECB decision have been extremely volatile since the June hike, but now it’s no longer considered live. Despite the best efforts of hawks such as Bundesbank President Joachim Nagel to elevate vigilance, commentary has clearly shifted toward the lack of second-round effects, especially through wages. Nagel’s comment after the recent round of escalation – suggesting that the ECB was “back where we started” in March – has very limited merit based on energy prices and inflation expectations. The 5y5y inflation forward has only increased by 5bp since the ceasefire “ended,” while survey-based figures are also manageable. Although only released officially after the decision, the ECB’s own inflation survey is expected to show three-year CPI expectations well anchored at 2.9%, unchanged from May.

The ECB’s communication will remain closely tied to its scenarios. The “severe” scenario remains the tail risk, while the status quo lies somewhere between “mild” and “adverse,” based on the criteria established in March. We see the direction of travel still heading toward “mild,” but it will likely take until September for confirmation as the Governing Council will need to see the next set of forecasts pushing CPI to below 3% for the year. This remains achievable, but the question is at what cost to growth. If the cost is too high, setting expectations for easing or at least a reversal of the precautionary hike in June is essential. There is a value argument emerging in favor of euro assets, but growth and earnings confirmation is required. Current financial conditions don’t support this case, and we have highlighted in iFlow that Eurozone assets do not face extreme holdings stress.

Forward look: This week’s European data calendar is light. Preliminary PMI results are due and broadly expected to show stability to slight expansion across Europe, notwithstanding upside inflation risk through input and output prices. Turkey’s central bank decision is expected to show unchanged rates at 37%, but current sequential inflation remains well above target, and real rates need to move higher to justify the recent improvement in the country’s financial account. Rates are also expected to rise in South Africa, but we expect the SARB to signal that 7.25% marks the end of insurance hikes.

The main political event is in the U.K., where Burnham is expected to officially start his term as prime minister after an audience with the king. Cabinet appointments will continue through Monday afternoon, with investors awaiting confirmation that current Home Secretary Shabana Mahmood will be named chancellor. In his acceptance speech as U.K. Labour Party leader on Friday, Burnham warned that he had not settled on his appointments, indicating there is tail risk of disappointments for the crucial role. Sterling’s recent run looks excessive given the country’s challenging fundamentals, and risk management on the currency and gilt markets is needed.

We expect European low-yielders to struggle in the current environment. While there is value in high-yield FX and perceived growth assets, it’s difficult to make a strong case for rotation away from APAC and the U.S. until stagflation risk recedes.

APAC: Trade and inflation data test Asia’s export engine

EXHIBIT #3: CHINA’S ACTIVITY, INVESTMENT AND CONSUMPTION NOT YET STABILIZING

Source: BNY, Bloomberg

Our take: Asia’s macro calendar is centered on inflation, trade and policy, with inflation data from Japan, New Zealand and Singapore, alongside the BI meeting, likely to be the key market catalysts.

Japan’s CPI will be closely watched for fresh clues on the Bank of Japan’s policy path amid persistent underlying inflation, while exports and PMIs will indicate whether external demand remains resilient. New Zealand’s Q2 CPI will shape expectations for the Reserve Bank of New Zealand’s easing cycle, while Singapore‘s CPI, following stronger-than-expected Q2 advance GDP growth, will be the final key input ahead of the Monetary Authority of Singapore’s July policy decision. In China, the July Loan Prime Rate is expected to remain unchanged as policymakers continue to prioritize targeted support and ample liquidity. We expect BI to deliver another rate hike to reinforce its commitment to rupiah stability.

Trade remains the dominant regional macro theme. South Korea’s early-July exports, Taiwan’s export orders and industrial production, Malaysia’s exports and Thailand’s customs exports will provide the latest read on the technology and manufacturing cycle.

Elsewhere, Australia’s labor market and July PMIs will be important for the August Reserve Bank of Australia meeting, while India’s flash PMIs and infrastructure output should reveal whether recent signs of slowing growth are stabilizing.

Overall, the week’s releases will determine whether Asia’s export engine continues to offset softer domestic demand, shaping both regional central bank expectations and market sentiment.

Forward look: Asia’s risk backdrop is deteriorating. A correction in technology shares, a stronger U.S. dollar, elevated crude oil prices and persistent geopolitical tensions all argue for further downside. The main offset is that investor positioning has yet to capitulate. iFlow continues to show resilient cross-asset flows, suggesting conviction remains intact despite weaker price action. That resilience is most visible in technology. Despite a near 10% month-to-date decline in the MSCI Asia ex-Japan Information Technology Index, iFlow shows only limited outflows from the sector, while investors continue rotating into Financials, Consumer Staples and Consumer Discretionary. Whether investors continue defending technology will be a key test of market conviction. A meaningful deterioration in tech flows would reinforce the broader bearish outlook.

The South Korean won remains an outlier. Its recent strength continues to diverge from fundamentals, with foreign equity outflows, persistent outbound investment and looser fiscal policy all pointing in the opposite direction. We continue to view SK Hynix’s ADR repatriation as the dominant driver. As these technical flows fade, KRW appreciation should lose momentum unless foreign portfolio inflows recover materially.

The Chinese yuan remains the region’s anchor, and we stay constructive over the medium term. However, near-term risks are rising as foreign equity inflows have flattened, and domestic investors have started reducing risk. A deeper correction in Chinese equities could trigger renewed FX hedging demand and temporarily push USDCNH higher before the medium-term appreciation trend resumes.

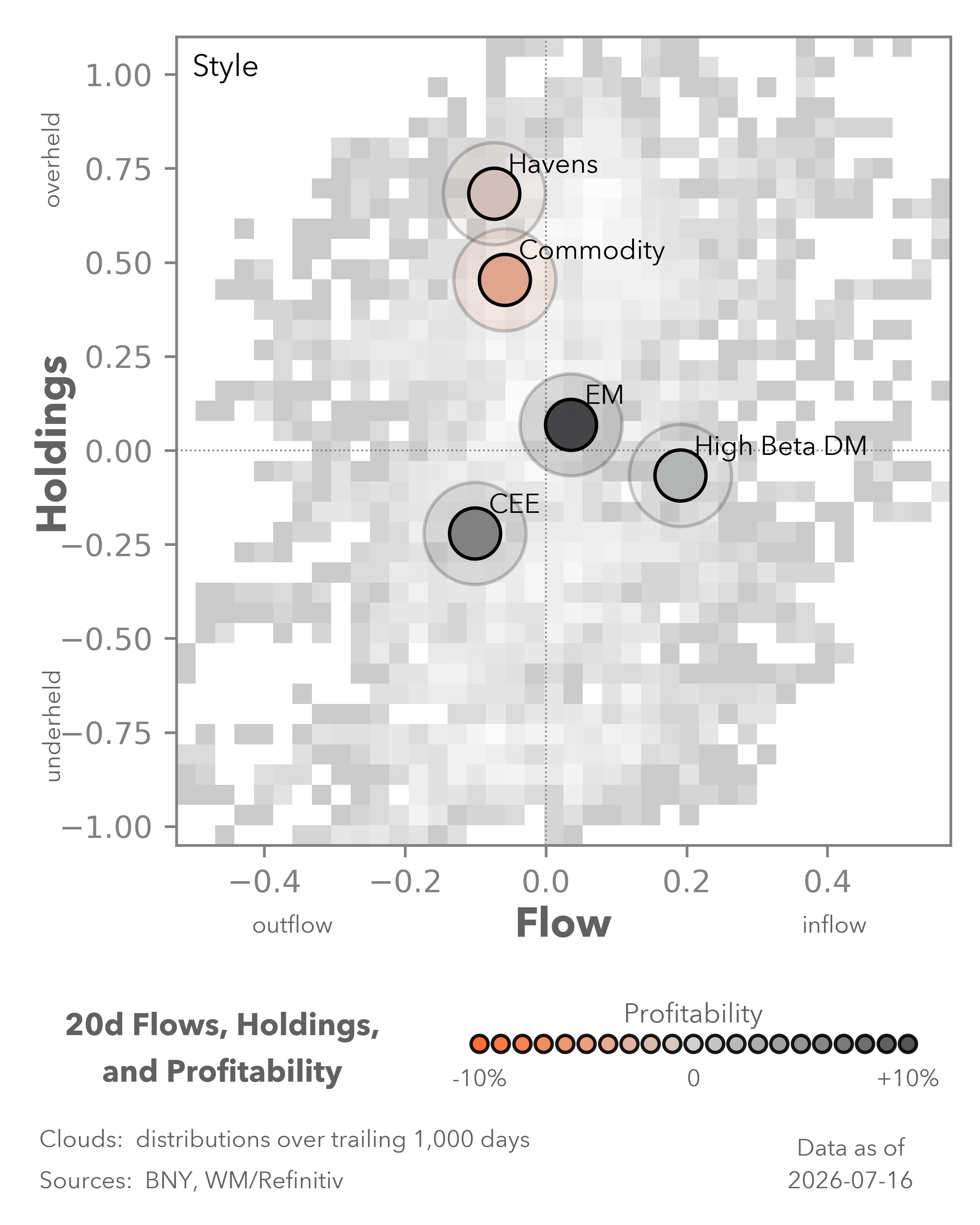

Latin America: Conflict-era inflows leave a solid balance-of-payments buffer

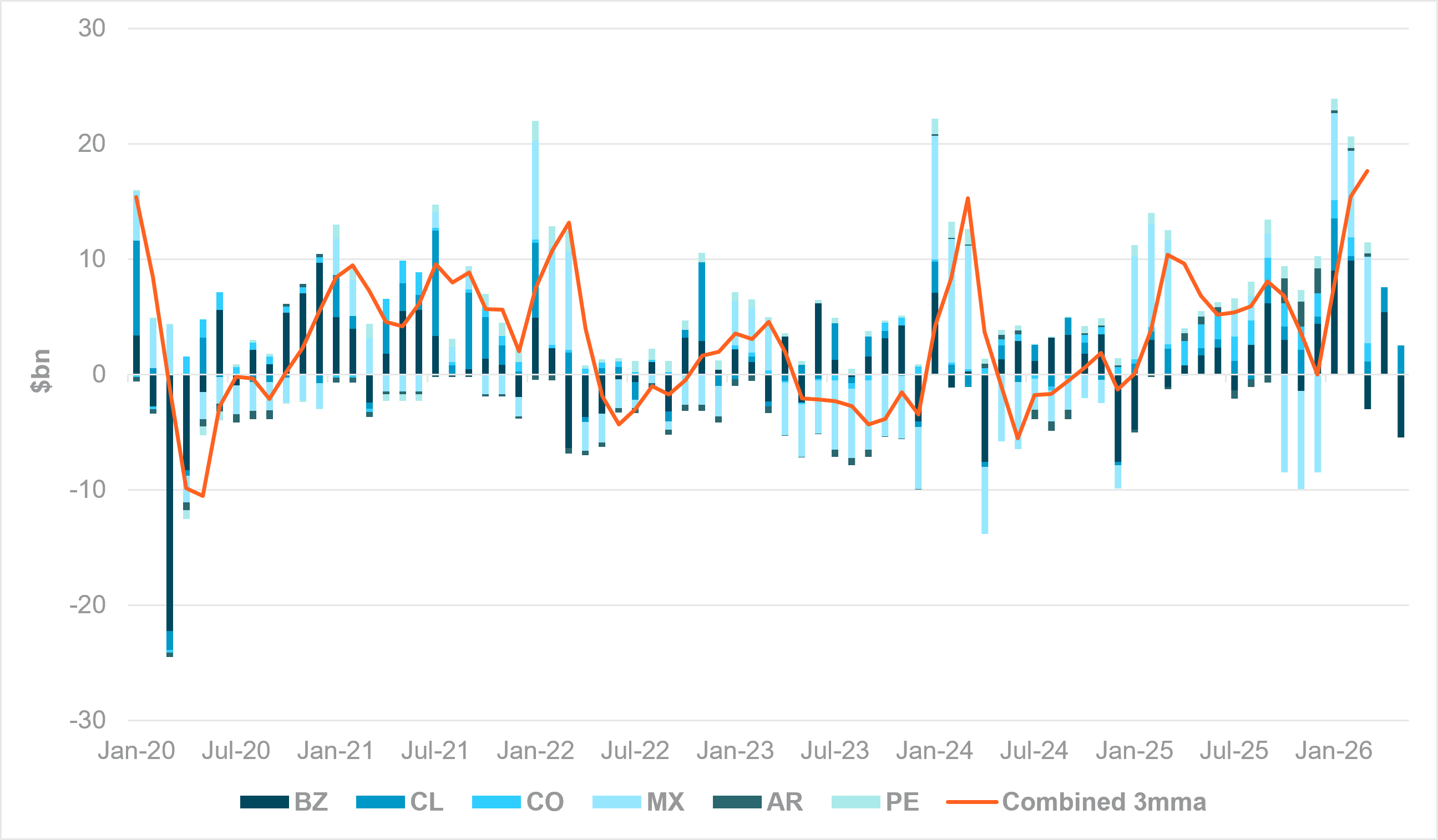

EXHIBIT #4: COMBINED FINANCIAL ACCOUNT LIABILITY INCURRENCE, LATIN AMERICA

Source: BNY, Macrobond

Our take: We continue to see improvement in the carry environment despite increasing nervousness in equity markets. Given the current positioning profiles in equities, risk profiles in standard carry trades – especially dollar-funded – look even more attractive. Nonetheless, Latin America remains well-positioned in FX, and it’s easy to see why.

Although not by design, the latest balance-of-payments data highlight that combined financial account for the region is in its healthiest state this decade. Between December 2025 and February 2026, all six major economies had positive incurrence of portfolio liabilities for three straight months: the same number as the entire period between January 2020 and April 2025. A further three occurred between May 2025 and November 2025. Rolling three-month inflows into the region also hit their highest levels since before the pandemic. In March, Latin America was seen as a “safe haven” and even benefited from temporary terms-of-trade improvements due to the supply shock arising from the Middle East conflict.

On the one hand, the strength of the financial account in the region means that even with a less dovish Fed (unlikely at present), the region has a significant buffer for potential outflows should dollar preference rise. Considering current elevated dollar positioning, we see such risks as low in any case. However, the surprise in the current setup is that despite dollar hedges also being at their lowest level this decade, it hasn’t come at the expense of Latin American currencies, so the holdings case for the region isn’t strong either. Currency hedges will likely rise, subject to the dollar’s trajectory, but overall return expectations for Latin America need managing unless a clear re-rating case emerges.

Forward look: Mexican retail sales (Tuesday) and IGAE (Thursday) activity data are expected to show moderate gains in domestic demand, but nothing to detract from Banxico’s easing path as real rates remain high relative to price risks. Biweekly CPI is expected to come in at 3.25% y/y with barely any sequential growth in headline and core components. If U.S. inflation figures continue to surprise to the downside, Banxico can rightly question whether a real rate buffer of 3% is necessary in a softer growth environment with trade risks looming in the background. However, the market is not yet convinced, with the 1y1y still close to 100bp above the current overnight rate.

We continue to see a positive carry setup. The Fed is on the defensive against price risks, and inflation can surprise to the downside in Mexico if greater pass-through materializes at current USDMXN levels. Even so, we note that PEN is the only clearly underheld currency in Latin America, so direct risk reward for total return in Latin American FX is weaker than EMEA or APAC high-yielding peers. The biggest holdings gap remains in fixed income and equities in the region.

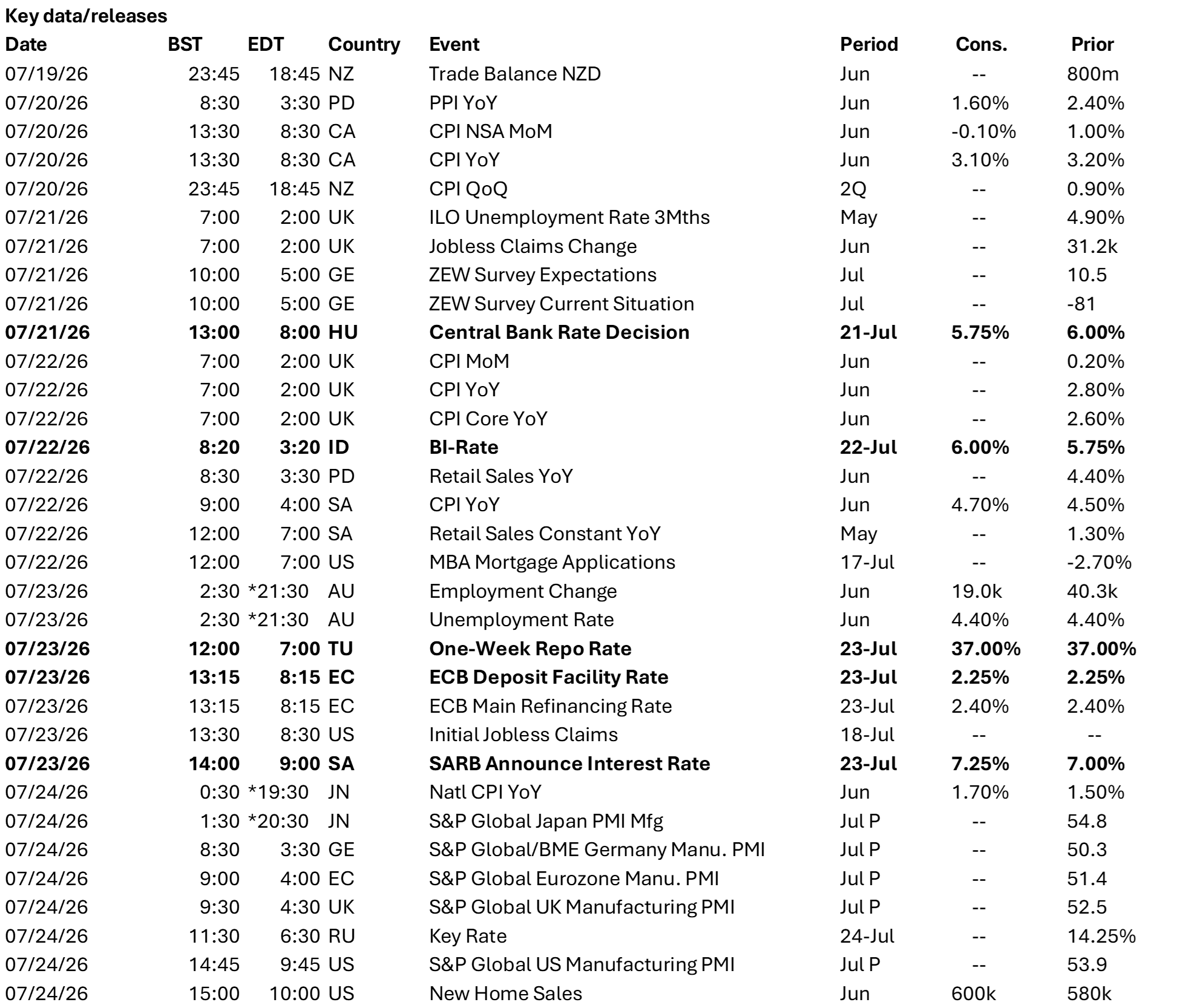

Central bank decisions

Hungary, Magyar Nemzeti Bank (MNB) (Tuesday, July 21): The MNB is expected to cut rates further to 5.75% as June inflation surprised further to the downside at 1.7%. Other activity numbers remain robust, but with real rates at 4% and further fiscal restraint due, there is plenty of scope for easing in financial conditions. Real rates in Hungary are now clearly outpacing the rest of Europe, and with the ECB dialing back rhetoric, there is more room for the MNB to ease without the risk of major HUF weakness.

Indonesia, Bank Indonesia (BI) (Tuesday, July 21): We expect BI to raise the policy rate by 25bp to 6.00%, reinforcing its commitment to go “all out” to defend the rupiah. Renewed geopolitical tensions, persistent foreign equity outflows and renewed IDR depreciation leave BI with little choice but to tighten further, even if higher rates have only limited success in attracting capital inflows. Beyond the rate decision, attention will turn to BI’s updated macroeconomic projections after the government raised its 2026 fiscal deficit target to 2.85% of GDP from 2.68%.

Türkiye, Türkiye Cumhuriyet Merkez Bankası (TCMB) (Thursday, July 23): No change is expected in the TCMB’s benchmark repo rate, but progress toward lowering inflation remains slow – core inflation for June managed to fall below 30% y/y and sequential growth fell below 1% m/m for the first time this year, but the annualized run rate in 2026 remains close to 40%, mandating a hawkish stance. Our flows show improved interest in duration, but it requires policy confirmation.

Eurozone, European Central Bank, ECB (Thursday, July 23): The Governing Council is no longer showing a unified front on the outlook as more members doubt whether second-round effects are present. However, Bundesbank President Joachim Nagel warned that the current tension in the Strait of Hormuz was essentially a return to March conditions. Vigilance remains, but if the ECB doesn’t signal a clear risk of a severe scenario, the risk of further hikes is low.

South Africa, South African Reserve Bank (SARB) (Thursday, July 23): The SARB is expected to raise rates to 7.25%, but the market’s base case is that this hike will be the last of the recent cycle, barring material escalation in the Gulf and sharp rises in global energy prices. Inflation figures for June are due the day before the SARB meeting and core CPI is expected to stay below 4%, but sequential price growth is expected to remain high, mandating “insurance” moves. Weakness in manufacturing and industrial production limits economic tolerance for further tightening.

Source: BNY

Source: BNY