Tax week and the funding markets

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 4 minutes

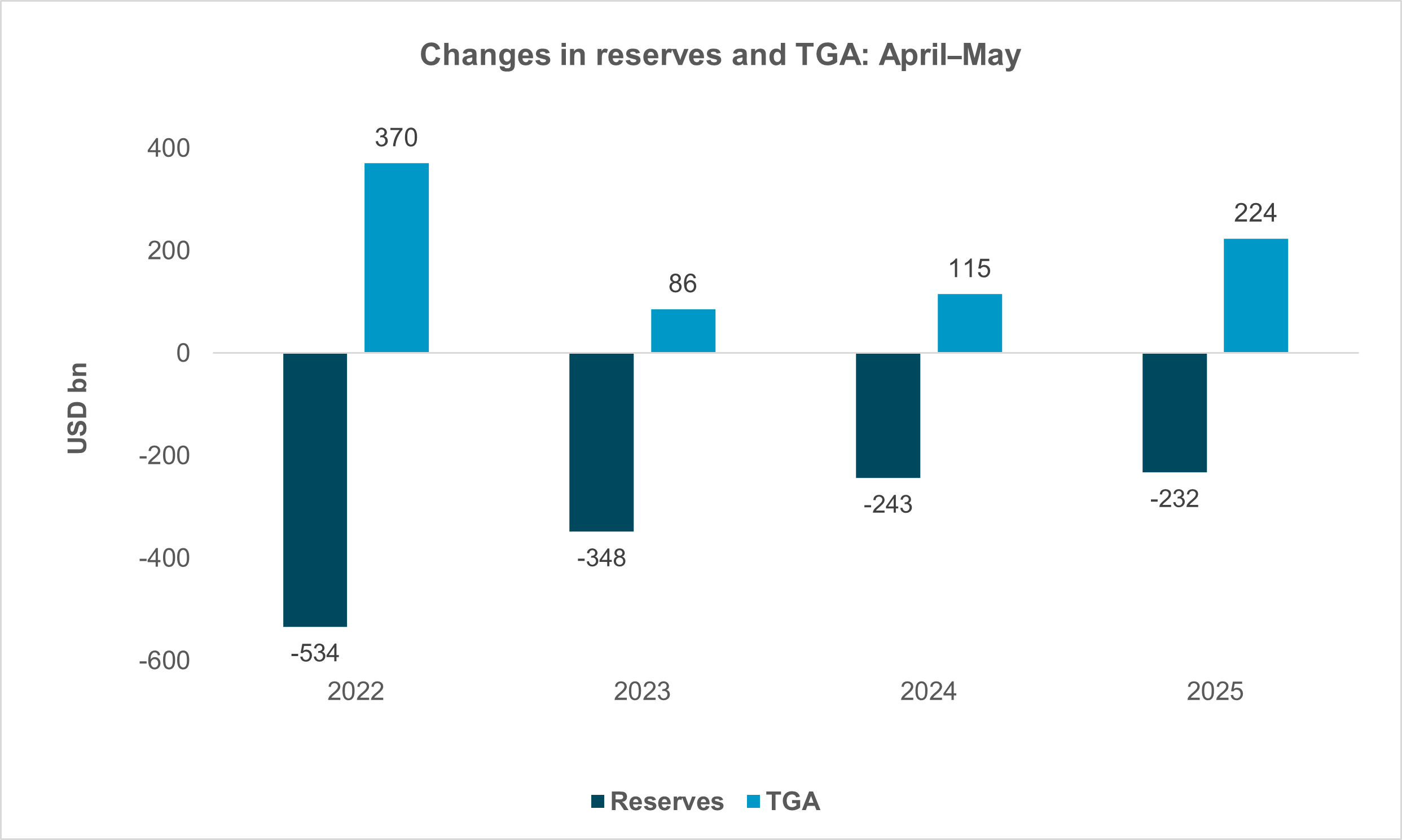

EXHIBIT #1: APRIL MEANS FALLING RESERVES AND A RISING TGA

Source: BNY Markets, Federal Reserve Board of Governors

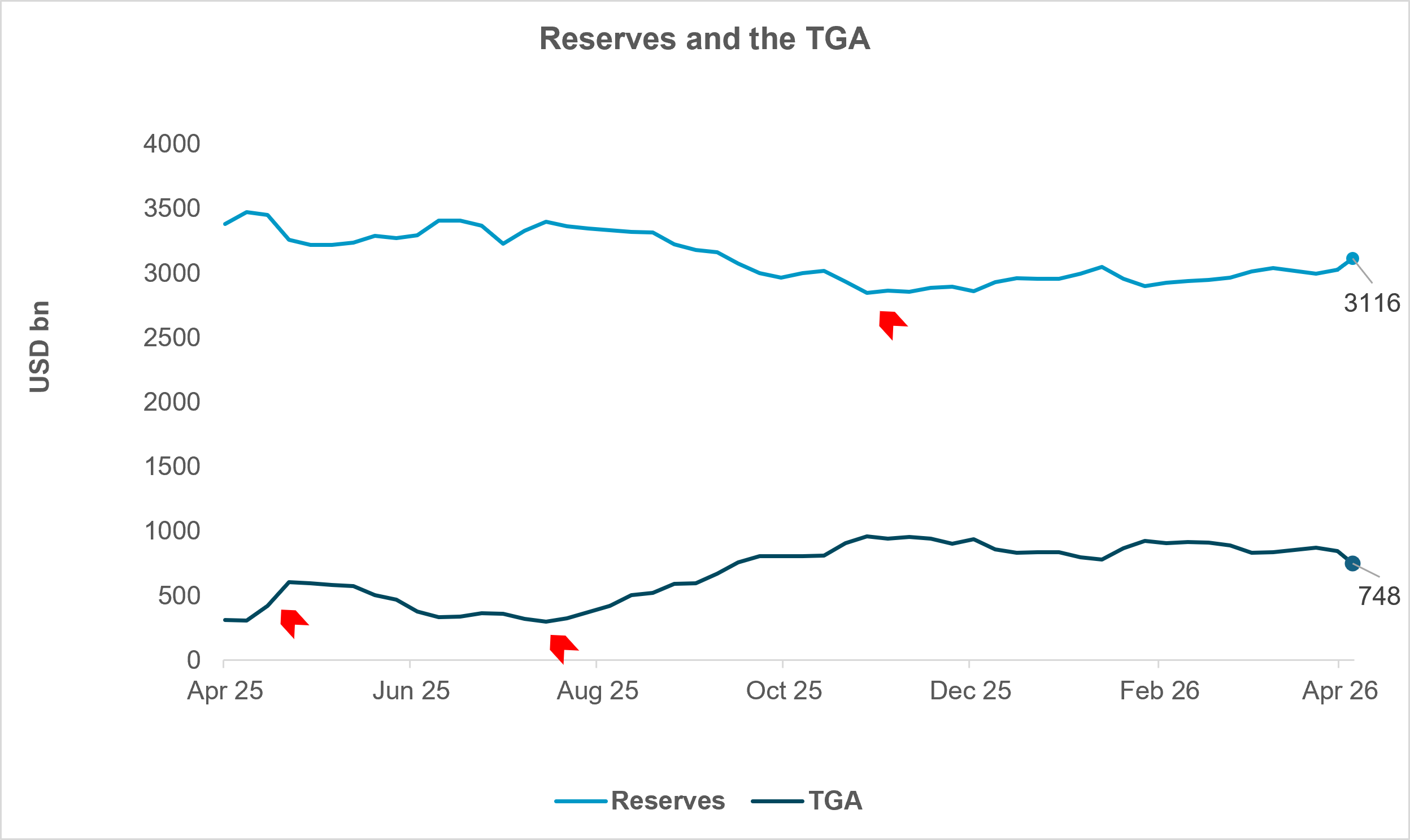

EXHIBIT #2: FED LIABILITIES HAVE BEEN STEADY LATELY

Source: BNY Markets, Federal Reserve Board of Governors

Tomorrow is Tax Day, as if our readers needed reminding. For money markets, this means the Treasury General Account (TGA) will swell as it collects revenues, and reserves will fall over the week and into the rest of the month. Exhibit #1 shows the behavior of these two Fed liabilities between the last week of March and the first week of May, for each of the last four years. Movements can be large – as much as $350bn in either direction. Will system liquidity be tested? We remain optimistic that the season will be managed with minimal disruption.

As of last Wednesday, total reserves were $3.1tn, the highest they have been since September 2025. At the same time, the TGA was $748bn, not coincidentally the lowest it’s been since the same period. With reserves comfortably above $3tn and room for the TGA to grow, both factors could be crucial for the days ahead.

Exhibit #2 shows the weekly movement of these two aggregates over the last year. Note the three arrows on the graph: the end of April last year, when the TGA jumped $200bn as coffers were filled around tax day; midsummer 2025, when the debt ceiling forced the TGA down to just $360bn, bottoming out in the last week of June; and the end of October, when reserves hit a low of $2.85tn, leading to QT curtailment and the eventual initiation of reserve management purchases (RMPs).

Since then, reserves have been relatively steady at $3tn, with RMPs continuing at approximately $40bn per month. Today, the New York Fed announced that RMPs for the next four weeks will be just $25bn, representing a meaningful tapering of these purchases. This was not entirely surprising. From the March FOMC minutes, the System Open Market Account (SOMA) manager noted “that after April, the monthly pace of RMPs was likely to be reduced significantly as swings in nonreserve liabilities were expected to moderate; the adjustment was likely to be somewhat gradual.” Between December 2025 and April 12, the NY Fed purchased over $200bn in T-bills through RMPs and portfolio reinvestments. We expect the pace of RMPs to roughly halve through the rest of the year, assuming money markets remain stable.

We think that the April tax season can be managed. One reason: as the SOMA manager notes, recent heavy usage of standing repo at the NY Fed suggests “a greater willingness of at least some counterparties to use the operations when economically sensible following the changes to standing repo operations implemented in December.” The April 15 tax deadline is sandwiched between two chunky bill settlements, but we still expect limited disruption in funding markets.

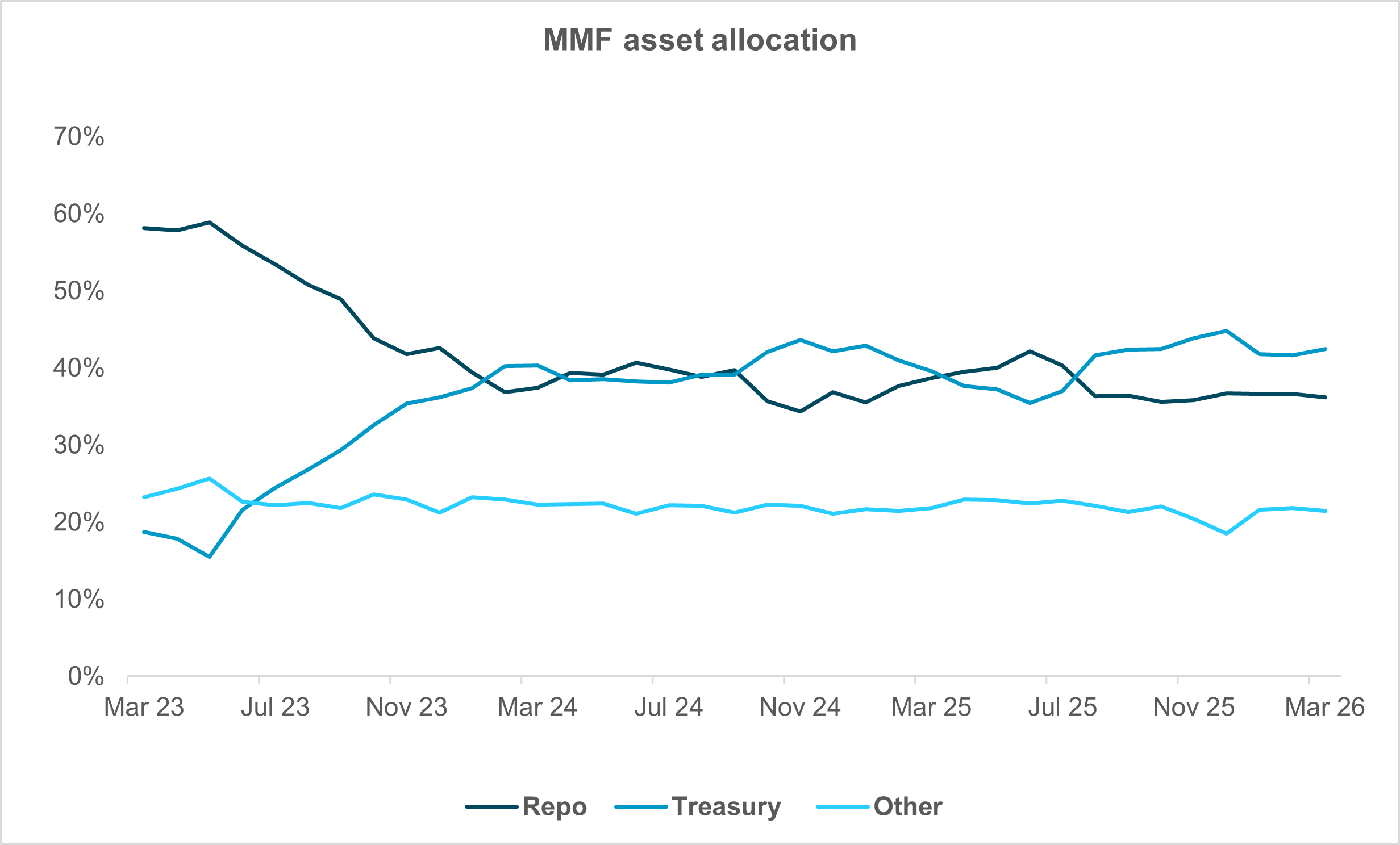

EXHIBIT #3: RELATIVELY STEADY MMF ASSET ALLOCATIONS

Source: BNY Markets, Crane Data

Money market funds (MMFs) currently hold near-record levels of assets – close to $8.2tn according to Crane Data. Investment Company Institute data put last week’s MMF AUM at $7.8tn, near the all-time high set just weeks earlier. Note that ICI data doesn’t include the same universe Crane does, but the results generally support each other; cash levels are high.

Exhibit #3 shows asset allocation of the MMF pie through the end of March. Note that repo comprises 36.2% of MMF assets, while T-bill holdings are just above 42%. Currently, funds are more allocated to bills than to repo, though both levels are close to where they have been for most of the past 18 months. Funds’ weighted average maturities are somewhat extended, with the average money fund at 43 days. This reflects funds’ desire to lock in higher rates on bills before expected Fed rate cuts are transmitted into lower T-bill yields. We think MMFs have ample capacity to keep supplying cash into repo as money market liquidity faces seasonal pressure.

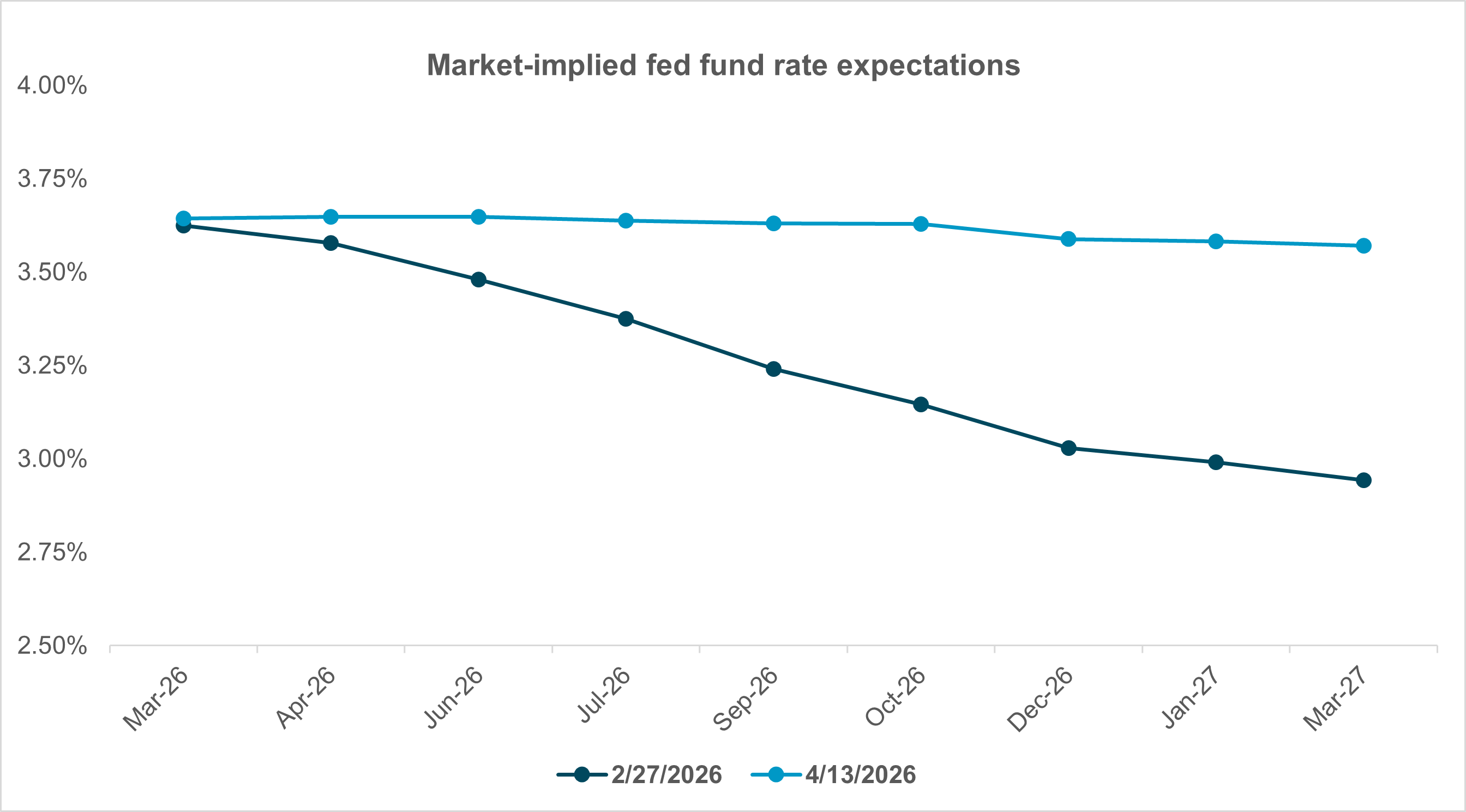

EXHIBIT #4: FLAT RATE CURVE

Source: BNY Markets, Bloomberg

The market-implied path of policy rates is virtually flat through end-2026 and into early 2027. Given uncertainties surrounding the growth and inflation outlook as the war drags on, current expectations seem reasonable; the duration and impact of the conflict remain impossible to gauge, and the market is probably correct to be similarly agnostic.

Last week, the March FOMC Minutes were published, and much like the meeting and press conference afterward, firm prescriptions were elusive. Perhaps the clearest expression of the two-sided risk confronting all central banks appeared near the end of the penultimate section, where the Committee addresses the policy action and outlook. The paragraph opens with the following (obvious) assertion: “With regard to the outlook for monetary policy, in light of the heightened degree of economic uncertainty, participants emphasized the importance of being nimble in adjusting the stance of policy in response to incoming data, the evolving outlook, and the balance of risks.” This is unassailable at present. Later, we learn that “many participants” expected rate cuts “if inflation were to decline in line with their expectations.” This is where we sit as well. Assuming the conflict ends with even a partial resumption of crude oil supply, the war’s economic damage will weigh on an already weak labor market, leading to rate cuts – as long as oil prices have peaked and are declining – even if crude is unlikely to return to prewar pricing.

FOMC participants who expect lower rates eventually, like ourselves, are counting on an eventual cooling of the conflict and a related easing of inflationary expectations. To be sure, as the same paragraph in the minutes points out, “some participants judged that there was a strong case for a two-sided description of the Committee’s future interest rate decisions in the post-meeting statement, reflecting the possibility that upward adjustments to the target range for the federal funds rate could be appropriate if inflation were to remain at above-target levels.” The dual mandate is experiencing tension, and the market is averaging those tensions to keep its rate forecast steady for now.