The TBAC also published a response to a Treasury Department charge that has drawn a lot of interest from the Street – whether the Treasury should consider lending excess TGA balances into the repo market, allowing the ever-larger TGA to earn interest for the government. While TBAC ultimately found that the operational challenges would likely outweigh the potential economic benefits, they also found that there might be some room for Treasury to earn relatively modest positive returns under certain reserve regimes (in instances where repo – specifically the triparty general collateral rate, or TGCR – exceeds IORB). The analysis found that the fewer reserves there were in the system, the higher the repo returns would be. We think this has meaningful implications for Treasury if indeed the Fed’s balance sheet were to contract in coming years – as incoming Fed Chair Kevin Warsh has expressed an interest in doing.

For this idea to be worthwhile, TGCR must exceed IORB, rather than simply be positive, due to the theory behind the Treasury–Fed consolidated balance sheet. That is, every dollar that Treasury lends into the repo market from the TGA would create a reserve held by the banking system and be paid IORB – money that would then not be remitted back to Treasury. While this would be essentially neutral for Treasury from an accounting standpoint, this would weigh on Fed profitability, which could worsen the Fed’s deferred asset and potentially carry political–economy ramifications. Furthermore, the mere prospect of such an arrangement – and even it is only a suggestion at this stage – hints at the potential contours of a “new accord” between the Fed and Treasury, as Warsh has frequently suggested.

TBAC used different assumptions of “excess cash” to gauge how much Treasury could deploy, which could lead to meaningfully different totals. Its analysis (on slide 4) shows a very large and highly volatile deployable balance of generally around $200bn – exceeding $700bn in some cases – and often $0. The question is obviously central to any profitability analysis, but we also think it highlights a key second-order consequence: the effect that a large and potentially volatile additional source of cash might have in overnight triparty repo markets. We can imagine repo dealers might be hesitant to devote precious balance sheet to a client with volatile balances rather than a more predictable cash lender.

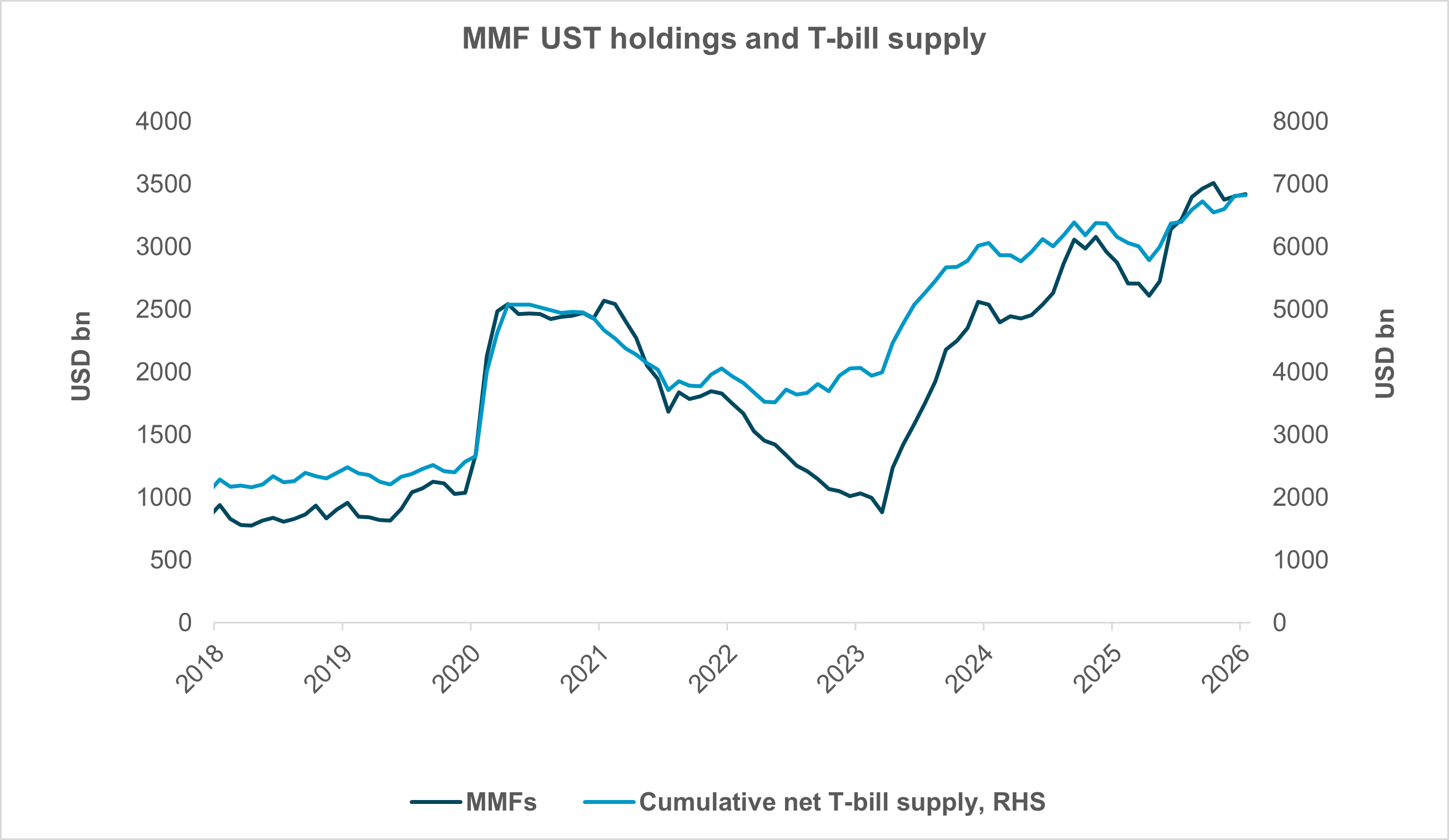

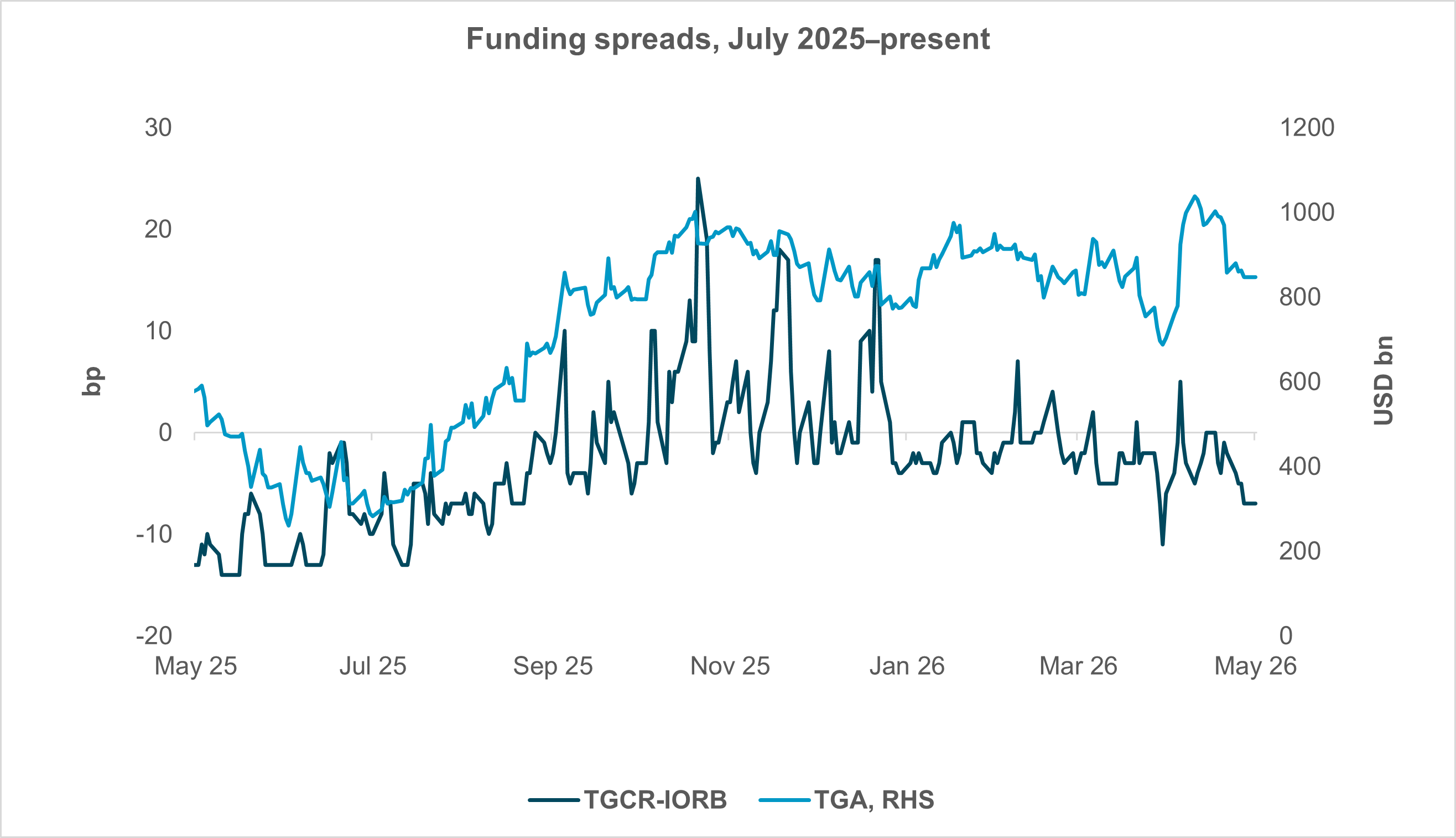

Exhibit #3 shows that last autumn, with TGA balances rising above $800bn and nearing $1tn, repo rates were indeed volatile and elevated. With TGCR rates frequently over IORB, this would have represented an opportune time for TGA excess balances to be offered in repo markets. Note however, this period coincided with the balance sheet’s transition from an abundant reserve regime to a merely ample one. It’s likely that in ample regimes such as at present, a growing TGA would almost axiomatically imply elevated money market rates, creating conditions for Treasury to deploy the TGA into repo. This is somewhat circular, but we can imagine a regime in which excess cash would still earn interest through such an arrangement.

Another interesting thing to note is that excess cash balances are often negative during debt ceiling episodes, which of course makes sense. With the debt ceiling a binding constraint on issuance, Treasury has often spent down the TGA to meet ongoing fiscal needs. One could imagine the response of a Treasury empowered to lend into the repo market: it would simply step out of the market until the debt ceiling had been lifted or suspended and the TGA had replenished its cash. But the net impact on the market is more unpredictable. Triparty repo rates are typically low during debt ceiling periods, as the relative absence of collateral alters the supply–demand dynamic.

In a world in which Treasury is an active repo lender, the equilibrium would be rather different. Treasury would be both a source of demand (TGA cash lending) and supply (bill collateral) and stepping out of both sides simultaneously would have an unpredictable and cross-cutting impact on the new equilibrium. Would the removal of TGA cash – which would otherwise tamp down funding market volatility – outweigh the more benign effects of less collateral in the system? Would dealers be able to price this into the new equilibrium? For the time being, these questions remain hypothetical, with TBAC concluding that after a “healthy debate,” “further study” would be needed before making a recommendation.