Market Movers: Second Verses

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

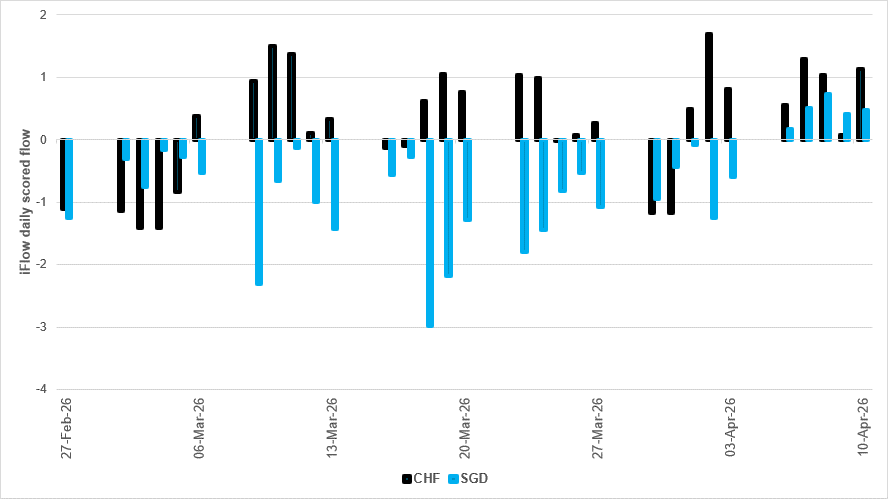

Safe haven flows of CHF and SGD since start of U.S./Iran conflict

Source: BNY

Flows into CHF since the war began have outstripped those into SGD. The ceasefire has seen both currencies gain inflows, despite hopes that the talks will lead to an extended truce.

Today’s decision by the Monetary Authority of Singapore (MAS) reflects the softening in Q1 GDP from 5.7% to 4.6%. Manufacturing growth slowed sharply, while construction accelerated, helped by public projects. The ongoing war concerns clearly show up in the shift in the MAS outlook, as it warned of downside growth and upside inflation risks. The MAS slightly increased the slope of the S$NEER policy band, while keeping the width and center unchanged. The move reflects recent SGD strength and rising inflation risks, despite a softer growth outlook.

SNB policy shifts are likely to be much the same, but with more concern about CHF appreciation. The hopes of a resolution have brought more, not less, SGD and CHF buying.

The shift in the U.S./Iran conflict from missiles to words leaves markets hoping for a beginning to the end of the war. Market reactions were dominated by hopes of more truce talks on Thursday, coupled with a significant bounce in tech shares in Asia. Taiwan’s TAIEX index rose 1.7% to set a new record high, while the South Korean KOSPI gained 2.7%, taking it back above February 27 levels and testing the 6,000 mark. Equities in Europe continued to rally, while U.S. futures are up, led by technology shares. The key to keeping the “turnaround Tuesday” rally intact will once again be whether oil prices hold, with Brent below $100/barrel. Further U.S. Q1 bank earnings announcements will also be key to keeping robust expectations intact. Bond yields are lower, as is USD, with KRW, CHF and ILS leading.

Bottom line: Markets are unwinding the war effect on prices, with the S&P 500 back to pre-war levels, along with USD. What has not changed are the correlations between USD and oil, stocks and bonds. The market risk persists in turnarounds and off-key second verses, as the music of diplomacy requires more effort. Investors’ patience will be tested today by earnings, PPI and further searches for new safe havens.

RBA Deputy Governor Andrew Hauser has warned of stagflation risks for Australia amid persistently high inflation and constrained supply capacity. Elevated inflation and supply constraints are limiting the scope for policy easing, despite mounting downside risks to growth. Energy price surges linked to the Middle East conflict are causing a significant income shock, eroding household purchasing power and raising business costs. Hauser described this as a central bank “nightmare” scenario, in which inflation rises while economic activity weakens, complicating policy decisions. The RBA remains focused on preventing a rise in medium-term inflation expectations, reinforcing a hawkish bias. ASX +0.29% to 5670, AUDUSD +0.695% to 0.7099, 10y ACGB -6.8bp to 4.95%.

South Korea’s National Pension Service (NPS), which manages $1tn in assets, is removing its longstanding 15% cap on foreign exchange hedging to allow greater flexibility amid won volatility. The 15% figure will now serve as a baseline, adjustable based on market conditions. The NPS will adopt a currency-neutral performance framework and may issue foreign currency bonds, signaling a more active market role in response to won weakness. This move aims to stabilize KRW, which has weakened due to heavy dollar demand from retail investors and overseas investments. As of March, the NPS held $603.2bn in foreign exchange assets, with $13.2bn tactically hedged. KOSPI +2.74% to 5968, USDKRW +0.386% to 1476.65, 10y KTB +2.7bp to 3.712%.

China’s state-backed iron ore buyer, China Mineral Resources Group Co. (CMRG), has allowed several steel mills to resume bidding for some BHP Group iron ore cargoes denominated in U.S. dollars, easing a months-long dispute. This follows a visit by BHP’s incoming CEO Brandon Craig, who met with leaders from China Baowu Steel Group and CMRG. While physical deliveries from Chinese ports are not yet permitted, a notice is expected. The move signals a potential shift in iron ore contract negotiations after CMRG had imposed broad restrictions, in place since last September. Iron ore futures have fallen since the report. CSI 300 +1.19% to 4701, USDCNY +0.2% to 6.8166, 10y CGB -1.3bp to 1.785%.

Chinese President Xi Jinping has met UAE Abu Dhabi Crown Prince Khalid in Beijing. Xi emphasized the comprehensive strategic partnership between China and the UAE, highlighting deepening political trust, steady cooperation in energy, investment, trade and technology, and enriched cultural exchanges. Both sides agreed to strengthen high-level contacts, support each other’s core interests and enhance multilateral coordination in platforms such as the UN and BRICS. Xi outlined four principles for Middle East peace: peaceful coexistence, respect for sovereignty, adherence to international law and balancing development with security. The UAE expressed commitment to deepening ties and supporting regional stability and security.

Canada’s Liberal Party, led by Prime Minister Mark Carney, has secured a majority government following projected wins in the University-Rosedale and Scarborough Southwest byelections, bringing its total to 173 seats in the House of Commons. This majority will enable the Liberals to control parliamentary committees and advance legislation more freely without opposition compromises. The result marks a significant political shift, as Carney was a private citizen 16 months ago and the Liberals were at one stage trailing the Conservatives by 20 points. TSX 60 Future +0.07% to 1970, USDCAD +0.538% to 1.3768, 10y CGB -0.4bp to 3.465%.

Singapore’s MAS has raised the slope of the SGD nominal effective exchange rate (S$NEER) policy band, keeping its width and center unchanged, to address rising inflation risks. The 2026 headline and core CPI forecasts were raised to 1.5-2.5% (from 1.0-2.0%), driven by elevated global energy prices. The MAS highlighted considerable risks around inflation and growth, with downside growth risks and upside inflation risks balanced against the earlier views expressed in January. Q1 GDP contracted by 0.3% q/q (+4.6% y/y, down from 5.7% in Q4 2025), weighed down by energy costs but supported by electronics and AI-related capex. STI +0.61% to 5015, USDSGD +0.276% to 1.272, 10y SGB -2.5bp to 2.043%.

The European Union Chamber of Commerce in China has warned that China’s expanding export control regime is evolving into a strategic tool affecting global supply chains, particularly for rare earth elements (REEs) and related technologies. In 2025, China tightened controls on REEs, lithium-ion battery tech and superhard materials, with extraterritorial provisions introduced but suspended until November 2026 following an agreement with the U.S. These measures risk disrupting European companies and global trade, increasing uncertainty and fragmentation. The chamber is urging China to implement targeted controls that prevent military misuse without harming legitimate civilian trade, to safeguard EU economic security and maintain stable sourcing of critical goods. Euro Stoxx 50 +0.8% to 5952, EURUSD +0.821% to 1.179, BBG AGG Euro Government High Grade EUR 0bp to 3.334%.

U.S. March PPI final demand is forecast higher at 1.1% m/m, 4.6% y/y vs. 0.7% m/m, 3.4% y/y in February, with the ex food and energy measure expected at 0.40% m/m, 4.10% y/y vs. 0.50% m/m, 3.90% y/y in February.

Central bank speakers: The ECB’s Gabriel Makhlouf speaks in Washington, DC, at Semafor World Economy – The Future of Global Finance; the ECB’s Philip Lane speaks at the University of Virginia in Charlottesville; the Fed’s Austan Goolsbee speaks at Semafor World Economy 2026; the Fed’s Michael Barr speaks on rural economic development; the Fed’s Anna Paulson, Susan Collins, Tom Barkin and Michael Barr participate in a fireside chat.

U.S. Treasury sells $50bn in 52-week bills and $70bn in 6-week bills.

Mood: Positive sentiment persists, with continued equity inflows and selling of core sovereign bonds. iFlow Mood has risen to 0.178, reflecting sustained investor optimism.

FX: Mixed G10 flows: USD and EUR saw outflows, while CHF, NOK and CAD attracted inflows. Broad EM inflows were led by INR, CLP, CHF and NOK, with outflows in BRL, COP, PHP and IDR. EUR scored holdings moved deeper into underheld territory.

FI: Strong demand for government bonds from Hungary, Poland, the Eurozone and LatAm, while outflows were seen in Australia, the Philippines and India.

Equities: Flows were mixed and generally light across the G10, EMEA and APAC, with stronger demand in LatAm. Sweden, Türkiye, Taiwan and Australia led inflows. Within emerging markets, IT, financials and consumer staples saw the most buying.

“You can’t go back and change the beginning, but you can start where you are and change the ending.” – Carl Sandburg

“We have two lives, and the second begins when we realize we only have one.” – Confucius

Germany’s wholesale prices rose by 4.1% y/y in March, up from +1.2% in each month from December 2025 to February 2026. Prices were 2.7% higher m/m. The surge was mainly driven by higher prices for mineral oil products (+17.8% y/y; +18.8% m/m) and non-ferrous ores, metals and semi-finished metal products (+48.4% y/y). Price increases were also seen in sugar, confectionery and bakery products (+6.1%) and tobacco (+5.9%). Conversely, prices fell for coffee, tea, cocoa and spices (-8.9%), milk products (-8.3%), flour and cereals (-5.8%) and grain and animal feeds (-3.4%). The conflict in Iran and the Middle East largely influenced energy and raw material costs. DAX +0.99% to 23978, EURUSD +0.821% to 1.179, 10y Bund -5bp to 3.042%.

Spain’s annual CPI inflation rose to 3.4% y/y in March (February: 3.3% y/y), with core inflation rising to 2.9% (February: 2.7% y/y). Monthly CPI rose 1.2%, driven by transport (+4.5% on higher fuel prices), clothing and footwear (+6.5% thanks to the new spring-summer season) and restaurants/accommodation (+0.8%). Key annual contributors were transport (5.3%), housing (3.7%, influenced by electricity and fuel prices) and clothing (2.6%). The annual HICP rate also reached 3.4%, up 0.9 percentage points from February, with a 1.7% monthly increase. IBEX 35 +0.74% to 18152, EURUSD +0.821% to 1.179, 10y Bono -6.5bp to 3.487%.

U.K. BRC retail sales growth accelerated to 3.6% y/y in March, boosted by an early Easter. Food sales rose 6.8% y/y, while in-store non-food sales increased by 1.4% y/y. BRC same-store sales were up 3.1% y/y from 0.7% y/y in February. However, online non-food sales growth slowed to 0.1% y/y. The online penetration rate for non-food items edged down to 37.6% from 38.1% last year. Demand was strong for computers, toys and homeware, but clothing and footwear struggled. Supply chain disruptions and rising costs continue to pressure retailers. FTSE 100 +0.24% to 10608, GBPUSD +0.76% to 1.3537, 10y gilt -5.3bp to 4.816%.

Swedish CPI inflation remained at 0.5% y/y in March, unchanged from February, with a 0.6% m/m decline. CPIF inflation eased to 1.6% y/y from 1.7%. Fuel prices surged by some 20% m/m, the largest increase since the 1990s, mainly driven by diesel (+28%) and petrol (+15%), contributing significantly to inflation. Electricity prices fell sharply (-19.3% m/m), offsetting fuel impacts. Food prices were down (-1.0% m/m), mainly due to lower dairy prices. Rents rose 4% y/y, while interest expenses continued to dampen inflation. Core inflation (CPIF-XE) eased to 1.1% y/y from 1.4%. OMX +0.79% to 3127, EURSEK +0.871% to 10.7938, 10y Swedish GB -2.6bp to 2.851%.

Australia’s Westpac-Melbourne Institute Consumer Sentiment Index for April plunged 12.5% to 80.1 from 91.6 in March, in the largest m/m drop since COVID. Rising fuel prices, driven by the U.S.-Israeli war on Iran, and a 25bp interest rate hike intensified cost of living pressures. Job loss fears hit a 5.5-year high, and consumer confidence in the housing market weakened. The “family finances vs. a year ago” sub-index fell 16.7% to 66.8, impacted by a historic 37 cents/liter fuel price surge to $2.40, despite a temporary fuel excise tax cut. Overall, consumers are braced for renewed economic weakness. ASX +0.29% to 5670, AUDUSD +0.695% to 0.7099, 10y ACGB -6.8bp to 4.95%.

Australian business confidence plunged 29 points in March to -29. This was the second-largest monthly fall in NAB survey history, comparable with declines during the global financial crisis and the onset of COVID. This sharp drop followed the Middle East conflict, reflecting heightened global uncertainty. Despite this, business conditions eased only slightly to +6, near the long-run average, indicating resilient economic momentum. Forward orders fell six points to -1, signaling rising caution, while capacity utilization rose to 83.1%, which is above average. Purchase cost growth more than doubled q/q to 3%, and product price growth increased to 1.1%.

Japanese industrial production for February showed a 2.0% m/m contraction in seasonally adjusted production, with a small 0.4% y/y increase, vs. -2.1% m/m, 0.3% y/y in January 2026. Shipments fell by 1.5% m/m and 0.1% y/y. Inventories rose 0.3% m/m, but shrank by 3.4% y/y. The inventory ratio increased by 2.0% m/m but decreased by 1.3% y/y. Production capacity edged down by 0.1% m/m and by 1.1% y/y. The operating ratio was down marginally m/m (-0.1%) to 105.0 (seasonally adjusted) but up 1.7% y/y. Nikkei +2.43% to 57877, USDJPY +0.434% to 159, 10y JGB -5.2bp to 2.415%.

China’s export growth slowed sharply to 2.5% y/y in March, falling short of the 8.3% forecast, as the Iran conflict triggered an energy shock, raising fuel and transport costs and disrupting earlier AI-driven momentum. Imports surged 27.8% y/y in the strongest rise since November 2021, likely reflecting higher energy prices and front-loaded demand. The trade surplus narrowed to $51.1bn in March, with the Q1 surplus at $265bn (vs. $271bn in 2025). YTD export growth is 14.7% y/y, outpaced by imports at 22.7% y/y. By destination, exports to the U.S. lagged sharply (-16.3% YTD y/y), while growth in exports bound for Hong Kong (+40%), South Korea (+24.5%), the EU (+21.1%) and ASEAN (+20.9%) remained strong. CSI 300 +1.19% to 4701, USDCNY +0.2% to 6.8166, 10y CGB -1.3bp to 1.785%.

Singapore’s GDP grew by 4.6% y/y in Q1, softening from 5.7% in Q4 2025. On a q/q seasonally adjusted basis, the economy contracted by 0.3%, reversing the previous quarter’s 1.3% expansion. Manufacturing growth slowed to 5.0% y/y (from 11.4% in Q4 2025), driven by electronics, transport engineering and precision engineering, despite declines in biomedical and chemicals. Construction accelerated to 9.0% y/y (Q4: 4.6%), supported by public and private projects. Wholesale, retail trade and transportation grew 6.7% y/y (Q4: 6.8% y/y), while information, finance and professional services expanded by 3.9% y/y but contracted by 4.0% q/q. The U.S./Israel/Iran conflict may impact future growth. STI +0.61% to 5015, USDSGD +0.276% to 1.272, 10y SGB -2.5bp to 2.043%.