Market Movers: Second-Order Effects

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

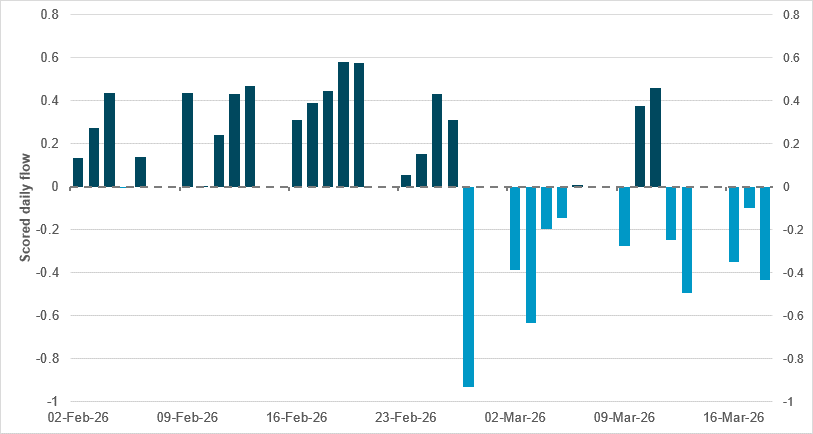

SCORED DAILY FLOWS IN “HAVENS” – AGGREGATION OF CHF, SGD AND JPY

Source: BNY

Yesterday’s BoJ and SNB decisions didn’t indicate any sense of panic among decisionmakers, but priorities for exchange rate management were clear. While both decisions were united in limiting volatility, the current energy crisis has very different implications for the balances of payments in these countries whose currencies have traditionally been considered havens.

For JPY and SGD, the core angle is to limit outflows caused by heavy exposure to imported energy as trade surpluses shrink. The SNB, meanwhile, is being very tactical about limiting inflows: it has signaled that it would be willing to act if safety-driven flows threatened the country’s inflation outlook.

On an aggregate basis, we note that none of the three currencies have benefited from the current environment: SGD is continuing to struggle, while a very early SNB warning at the beginning of the conflict also contributed to selling. After a very strong start to the year for the group, markets have reverted back to dollar safety by default. In addition, we note that overall fixed income interest for Switzerland, Japan and Singapore has converged. Assuming that the declines in Singapore and Japan are largely duration-based, then at least there is not much standing in the way of incremental outflows, and holdings could recover as soon as the inflation and real-rate outlook improves. Meanwhile, Swiss interest has increased; this will largely center on front-end private sector liquidity due to the lack of sovereign or municipal liquidity. Even so, all three currencies remain around 5% below their rolling 12-month averages, in a clear sign that safety interest is lacking due to the combination of balance-of-payment and policy risks.

The start of spring brings holidays, including Eid and other celebrations in Japan, Indonesia, Malaysia and the Philippines. While the sun enjoys an equinox, there is no equivalent for the markets. Friday sees the culmination of secondary effects from the four-week war. Relative calm in the oil markets hasn’t stopped FX volatility in JPY, IDR and ZAR. USD has flipped from a gain of 1% to a fall of 1%, and today is holding near the lower end of its war ranges. Rate decisions yesterday led to significant front-end rate moves, with the BoE moving from expectations of 1-2 rate cuts in 2026 to 2-3 rate hikes. Similar flips in EU rates have left GBP and EUR moves on the front lines of focus. Bond yields are higher, equities are mixed and other commodities, such as gold, are bid.

Bottom line: There are secondary war effects in markets that are starting to show up and affect how risk management is working across investor portfolios. The rise in cross-asset volatility is one example, as the extreme volatility of energy mixes with the front end of rate markets in developed nations. FX remains a shock absorber and logically will be the snap measure of sentiment on the day ahead, with the search for safe havens ongoing.

The Trump administration is considering options to seize or blockade Iran’s Kharg Island, a key oil export hub, as part of efforts to pressure Tehran to reopen the Strait of Hormuz, though no final decision has been made. The move would mark a significant escalation, potentially requiring additional troop deployments and exposing U.S. forces to heightened risk, with preparations including recent airstrikes aimed at weakening Iran’s military presence on the island. While some officials argue such action could strengthen U.S. leverage in negotiations, others warn it may not achieve the desired outcome and could provoke further disruption. Alternative strategies, including naval escorts for tankers, are also under discussion as the conflict continues. S&P Mini -0.08% to 6655, DXY +0.153% to 99.383, 10y UST +4.4bp to 4.293%.

The Pentagon is considering deploying additional troops to the Middle East as the conflict with Iran intensifies, signaling a potential escalation beyond current U.S. involvement. Discussions remain ongoing regarding the scale and scope of any deployment, but the move would expand on the roughly 50,000 troops already stationed in the region and could increase the likelihood of direct engagement, including operations involving Iran itself. The deliberations come amid heightened tensions following Iran’s efforts to disrupt the Strait of Hormuz, a critical global oil transit route, and as U.S. allies show reluctance to deepen involvement. Any troop increase would add to existing naval and air operations already underway.

The ECB’s François Villeroy de Galhau has stated that the central bank remains fully committed to returning inflation to its 2% target, emphasizing policy effectiveness since the 2022 inflation shock and readiness to act further if required. He framed the current rate pause as a response to heightened uncertainty, particularly from the Middle East conflict, rather than inaction, noting that multiple scenarios are being used and can be updated more frequently if conditions evolve. Villeroy also stressed that policy decisions will not be driven by short-term oil price fluctuations but by the medium-term outlook. However, Bundesbank President Joachim Nagel warned that an April hike should be considered if the inflation outlook deteriorates, a view echoed by Bank of Estonia Governor Madis Mueller. Euro Stoxx 50 +0.86% to 5662, EURUSD -0.208% to 1.1565, BBG AGG Euro Government High Grade EUR +4.6bp to 3.194%.

Asian LNG markets are tightening after Qatar announced that two liquefaction trains at Ras Laffan could remain offline for up to five years following missile strikes, forcing QatarEnergy to declare force majeure on some long-term contracts. The disruption, affecting around 12.8 million metric tons of annual capacity, has pushed regional spot prices into the mid-$20s per MMBtu, with bids reaching as high as $28. This has prompted some buyers such as Indian Oil to withdraw from tenders, while others are delaying purchases. Although some countries are reporting adequate inventories and alternative supply options, importers are increasingly turning to U.S. suppliers. Analysts estimate that the outage has shifted the market from surplus to a 4% deficit, with elevated prices expected to persist. HH natural gas -1.169% to 3.129, Dutch TTF natural gas +0.151% to 61.945.

President Trump and Japanese Prime Minister Sanae Takaichi have announced initiatives to strengthen the U.S.-Japan alliance, focusing on economic security, supply chain resilience and defense cooperation. Key highlights include accelerated Japanese investments in U.S. energy projects totaling up to $109bn, enhanced cooperation on critical minerals and technology innovation, and expanded space and biotech partnerships. Both nations have committed to bolstering their defense capabilities, including missile production and advanced systems deployment. They have emphasized regional security, supporting peace across the Taiwan Strait, denuclearization of North Korea and coordinated responses to strategic competitors. Nikkei -3.38% to 53373, USDJPY +0.584% to 158.65, 10y JGB 0bp to 2.277%.

Fed speakers: Governor Christopher Waller speaks on CNBC at 8.30 ET, while Governor Michelle Bowman speaks on Fox Business at 8.00 ET.

Canadian February retail sales are forecast at -0.3% m/m after +1.5% m/m. Consumer behavior before the war will represent an important baseline for the BoC.

Mexican Q4 aggregate demand expected up 1% q/q, 1.8% y/y after 1.1% y/y, with private spending up 1.6% q/q after 1.0% q/q. Further Banxico rate cuts are in doubt, and growth data will be key.

Mood: Risk sentiment remains fragile, with iFlow Mood at -0.142, reflecting continued allocation away from equities into core sovereign bonds.

FX: G10 flows were mixed and light. USD and JPY saw inflows, while EUR and GBP were sold. Elsewhere, significant outflows were recorded in IDR, SGD, TRY and ILS, offset by strong buying in CLP.

FI: Broad demand for sovereign bonds across the G10 and LatAm, led by Eurozone and Japanese government bonds. EMEA and EM APAC saw outflows, notably in Israeli, Chinese and Indonesian government bonds.

Equities: G10 equities were broadly sold, while the rest of the iFlow universe saw better buying interest. Strong inflows were observed in Poland, Thailand and Norway, contrasting with outflows in Colombia, India and the U.S.

“Second-order effects, such as belief in belief, makes fanaticism” – Alfred Korzybski

“Consider the totality of risk and effect; look always at potential second-order and higher-level impacts.” – Charles T. Munger

The euro area’s current account surplus widened to €38bn in January from €13bn the previous month. This was driven by surpluses in goods, services and primary income, and partly offset by a secondary income deficit. Over the 12 months to January, the surplus narrowed to €261bn (1.6% of GDP) from €377bn (2.5%), reflecting a shift in primary income to deficit and a smaller services surplus, despite a larger goods surplus. Within the financial account, euro area investors increased their purchases of foreign debt securities, while non-residents continued strong buying of euro area assets. Reserve assets rose sharply to €1.99tn, largely due to higher gold prices, with Bulgaria’s euro adoption having limited aggregate impact. Euro Stoxx 50 +0.86% to 5662, EURUSD -0.208% to 1.1565, BBG AGG Euro Government High Grade EUR +4.6bp to 3.194%.

The euro area current account surplus widened to €38bn in January, up from €13bn in the previous month. This was driven by surpluses in goods (€33bn), services (€16bn) and primary income (€4bn), partly offset by a €15bn secondary income deficit. In the 12 months to January, the current account surplus narrowed to €261bn (1.6% of GDP) from €377bn (2.5%) a year earlier, reflecting a shift in primary income to deficit and a smaller services surplus and despite a larger goods surplus. In the financial account, euro area residents’ net purchases of non-euro area portfolio securities reached €786bn, while non-residents acquired €914bn of euro area securities.

German producer prices fell by 3.3% y/y and 0.5% m/m in February, driven primarily by lower energy costs. Energy prices dropped 12.5% y/y and 1.8% m/m, with sizable falls for natural gas (-14.3%) and electricity (-13.4%), while mineral oil products fell 7.0% y/y despite a m/m increase. Excluding energy, producer prices rose 1.0% y/y and 0.2% m/m. Among components, investment goods prices increased by 1.7% y/y and intermediate goods by 1.1%, supported by higher metals prices, while consumer goods prices decreased by 0.6% y/y, led by falling food prices. Public sector data indicated no impact from late February’s Middle East conflict developments on pricing trends for the month. DAX +0.88% to 23040, EURUSD -0.208% to 1.1565, 10y Bund +1.1bp to 2.973%.

France’s basic monthly wage index rose 0.2% q/q in Q4, with y/y growth at 1.7% from 2.0% previously; the hourly wage index for workers and employees increased by 0.2% q/q and 1.6% y/y. By sector, q/q wage growth was 0.2% in services and 0.1% in both industry and construction, with y/y increases of 1.7% in services and construction and 2.0% in industry. Adjusted for inflation, which rose 0.7% y/y, real wages increased by 1.0% for the monthly index and 0.8% for the hourly index. By category, annual wage growth ranged from 1.5% for employees to 2.0% for managers, with real-terms gains across all groups. CAC 40 +0.59% to 7854, EURUSD -0.208% to 1.1565, 10y OAT +0.8bp to 3.65%.

French retail sales volumes fell by 0.3% m/m in February, reversing a 1.3% increase in January, driven by a 1.6% m/m decline in manufactured goods, while food sales rose by 1.3%. Within manufactured goods, sharp decreases were recorded in footwear (-9.5%) and textiles (-5.7%) following strong rebounds in the prior month, whereas sales of games and toys (+5.8%) and bicycles and motorcycles (+5.5%) increased. By distribution channel, sales were down across most segments, including hypermarkets (-0.1%), supermarkets (-0.3%), small retail (-0.8%) and department stores (-10.6%). Over the three months to February, retail sales were flat, as a 0.9% rise in food sales offset a 0.6% decline in manufactured goods.

Italian exports fell by 4.6% y/y in value terms and 5.8% y/y in volume terms in January, while imports were down 7.4% y/y by value and 2.9% y/y by volume, with exports broadly flat m/m (-0.1%) and imports 1.3% m/m lower. Export weakness was broad-based, led by sharp drops for refined petroleum (-38.2%), machinery (-7.3%) and food products (-9.2%), partly offset by gains in metals (+17.1%) and pharmaceuticals (+5.9%). The trade balance recorded a surplus of €1.1bn, with a narrower energy deficit and a higher non-energy surplus. Import prices rose 0.2% m/m but fell 3.3% y/y, reflecting easing external cost pressures despite some m/m increases in intermediate goods. The current account registered a deficit of €1.785bn for January. FTSE MIB +0.89% to 44089, EURUSD -0.208% to 1.1565, 10y BTP +2.9bp to 3.806%.

U.K. February public sector borrowing was £14.3bn, £2.2bn higher y/y and the second-highest February on record, largely reflecting the timing of central government debt interest payments. Borrowing in the financial year to February totaled £125.9bn, down £11.9bn y/y and equivalent to 4.1% of GDP. This was 0.6 percentage points lower than in the same period a year earlier. The current budget deficit stood at £5.1bn in February, bringing the YTD total to £62.1bn, which is £16.7bn smaller than a year earlier. Public sector net debt was estimated at 93.1% of GDP, while net financial liabilities were 82.5%. The central government net cash requirement was £9.1bn, up £0.6bn y/y. FTSE 100 +0.39% to 10102, GBPUSD -0.201% to 1.3404, 10y gilt +5.3bp to 4.896%.

China has kept its loan prime rate (LPR) remained unchanged, with the 1y rate at 3.0% and the 5y rate at 3.5%, marking a tenth consecutive month of stability. The unchanged setting reflects a steady policy rate environment, as the central bank’s 7-day reverse repo rate has held constant, alongside limited incentives for banks to lower LPR spreads. Market rates, including AAA interbank certificates of deposit yields, have edged slightly lower following earlier liquidity injections, while narrowing net interest margins in Q1 have constrained pricing adjustments. The authorities have reiterated a moderately accommodative monetary policy stance, signaling potential policy rate cuts later in the year that could guide LPR lower. CSI 300 -0.35% to 4567, USDCNY +0.125% to 6.8823, 10y CGB -0.1bp to 1.839%.

China’s central bank and foreign exchange regulator has introduced updated rules governing domestic firms’ overseas lending. These are aimed at unifying previously fragmented RMB and foreign currency frameworks and better supporting companies’ cross-border financing needs. The policy brings such lending under a macroprudential framework, linking limits to firms’ net assets while raising the adjustment coefficient to expand capacity and encouraging greater use of RMB. It also strengthens risk controls through clearer requirements on fund management, reporting and regulatory oversight. The authorities outlined standardized registration procedures based on firms’ financial conditions and compliance history, while allowing existing lending arrangements to continue under current terms during a transition period.

Taiwan’s export orders in February 2026, measured in USD, totaled $63.88bn, down 16.9% m/m but up 23.8% y/y (January: $77.91bn). The January-February cumulative reached $140.78bn, up 41.3% YTD y/y. Key sectors driving growth included information and communication products (+55.2% y/y) and electronic products (+26.2% y/y), supported by strong demand for AI, high-performance computing and cloud services. Major export destinations were the U.S. (+45.1% y/y), ASEAN (+33.8% y/y), China/HK (flat y/y), Europe (-5.6% y/y) and Japan (+17.8% y/y). Overseas production accounted for 47.3% of orders, rising 2 percentage points y/y. The outlook for March is positive, with order growth expected. TAIEX -0.43% to 33544, USDTWD -0.054% to 31.97, 10y TGB +0.1bp to 1.415%.

Hong Kong recorded a balance of payments surplus of HK$46.5bn (5.3% of GDP) in Q4, reversing a HK$136.5bn deficit in Q3. Meanwhile, the current account surplus narrowed to HK$93.9bn (10.6% of GDP) due to a shift in the goods balance to a deficit, partly offset by stronger services and primary income inflows. For 2025, the BoP deficit stood at HK$69.9bn (2.1% of GDP), which was smaller than in 2024, while the current account surplus was HK$406.6bn (12.2% of GDP). The international investment position showed net external assets of HK$19.510tn (5.9 times GDP). Gross external debt rose to HK$16.054tn (4.8 times GDP), driven mainly by the banking sector. Hang Seng -0.88% to 25277, USDHK$ -0.057% to 7.8379, 10y HKGB -1.2bp to 1.417%.

Hong Kong’s Consumer Price Index (CPI) for February 2026 rose by 1.7% y/y, up from 1.1% in January 2026. Underlying inflation, excluding government relief measures, increased by 1.6% y/y (January: 1.0%). The rise was mainly driven by higher charges for package tours and transport fares during the Lunar New Year, which fell in February this year versus January last year. Key contributors included miscellaneous services (+4.9%), transport (+4.3%) and utilities (+3.5%), while clothing and durable goods prices decreased. The government noted modest inflation early in 2026 but flagged rising fuel import costs due to geopolitical tensions.