Market Movers: Guarded Optimism

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 6 minutes

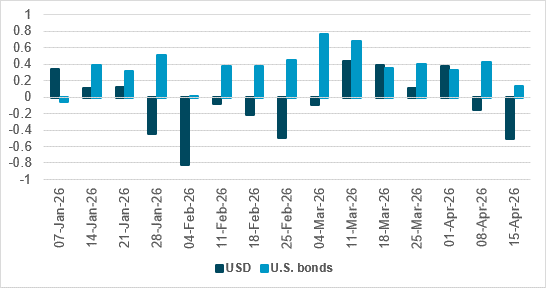

USD and U.S. bond flows in 2026

Source: BNY

The buying of U.S. bonds and USD since the war started stands out in our flow data. The market shift since the ceasefire appears to be a return to normal. Bonds are being bought and hedged again. The role of the dollar as a safe haven in the conflict has been linked to many factors, but the energy supply shock creating a need for USD to pay for oil is the most prominent. This is the conundrum for asset allocation and risk, as higher oil prices are adding to inflation concerns globally, and the relief today with oil still over $90/barrel will keep inflation above target.

The USD hedge and the intervention by other central banks to cap USD gains are clearly part of the ongoing narrative and key consequences of the war – as are the hopes of a sustainable peace.

The third week of equity gains is drawing to a close, led by ongoing hopes of a deal to end the conflict between the U.S. and Iran. President Trump’s optimism was not sufficient for APAC shares, which saw sizable profit-taking; meanwhile EU shares have notched up tepid gains, as have U.S. futures. Weekend risk worries are dominating another Friday of light-conviction trading. Falls for oil, USD and bond yields all support a modest risk-on move in equities, with the wrapper of earnings supporting the ongoing rally.

Bottom line: Friday trading rules apply, as investors have seen another great week for equities, with technology back as a key driver. Bond yields have been steady, and FX markets have been tame. The surge of volatility in commodities has eased. All these factors support modest risk-taking as we head into the unknown of weekend news wrapped around geopolitics. However, there are a host of central bank speakers and more meetings to go today that could shift the focus on this return to normal, leaving profit-taking and rest more important than chasing momentum trades. Optimism about the future will be guarded, given the events of the last month and their effect on all assets.

Former U.S. Treasury Secretary Henry Paulson has urged authorities to prepare an emergency “break-glass” plan to prevent a potential collapse in demand for U.S. Treasurys, warning of severe consequences. He highlighted that a debt crisis would differ from the 2008 financial crisis, with limited fiscal firepower to intervene. Paulson emphasized the need to address the fiscal deficit through increased revenues, tax reforms and an overhaul of social security and healthcare. He noted the challenge of gaining congressional support before a crisis hits. The U.S. debt-to-GDP ratio is projected to reach a record 108% by 2030, raising concerns over market stability. S&P Mini +0.13% to 7087, DXY -0.02% to 98.196, 10y UST -0.8bp to 4.303%.

Israel and Lebanon have agreed a ten-day ceasefire starting at 5 p.m. ET on April 16. The truce aims to foster lasting peace, mutual recognition of sovereignty and security along their shared border. President Trump has expressed optimism about Lebanon dealing with Hezbollah, the Iran-backed militia. The ceasefire follows recent heavy Israeli strikes on Lebanon and ongoing U.S.-Iran tensions. Trump plans to host Israeli Prime Minister Benjamin Netanyahu and Lebanese President Joseph Aoun for peace talks, the first since 1983. U.S. officials, including Vice President JD Vance and Secretary of State Marco Rubio, will support efforts to secure lasting peace. TA-35 +0.99% to 4422, EURILS +0.067% to 2.9905, 10y IGB -3.1bp to 3.92%.

Bank of Japan Governor Kazuo Ueda has emphasized that Japan’s low real interest rates must be considered when deciding the timing of rate hikes. He noted that inflation is being driven by a “negative supply shock,” which is harder to control than demand-driven inflation. Ueda highlighted Japan’s accommodative financial environment and low real rates up to the medium-term zone. He acknowledged uncertainties from the Middle East conflict and rising crude oil prices, which could increase inflationary pressures, while robust corporate profits and government stimulus should support growth. Policy decisions will be data-dependent and made at each meeting accordingly. Nikkei -1.75% to 58476, USDJPY -0.157% to 159.27, 10y JGB +1bp to 2.424%.

The Reserve Bank of India has instructed state-run oil refiners to reduce spot dollar purchases and instead use a special credit line accessed via State Bank of India to meet their foreign exchange needs. This measure, previously used during the Ukraine war, aims to ease pressure on the rupee, which has depreciated by more than 3% this year to record lows, making it Asia’s worst-performing major currency. The credit line is available to Indian Oil Corp, Hindustan Petroleum and Bharat Petroleum, which together refine about half of India’s 5.2 million barrels/day of capacity. The move seeks to lower dollar demand from refiners and stabilize the rupee amid rising oil prices and foreign outflows. SENSEX +0.46% to 78347, USDINR +0.375% to 92.85, 10y INGB +3.4bp to 6.922%.

Australia is set to sign a multibillion-dollar contract with Japan to purchase 11 advanced Mogami-class naval frigates. The first three ships, costing A$15-20bn ($10.75bn), will be built in Japan and the remainder in Western Australia. The deal aims to modernize Australia’s navy and strengthen security ties with Japan. The first vessel is expected by 2029, entering into service in 2030. Mitsubishi Heavy Industries is leading the project. This contract reflects Japan’s push to expand its defense exports amid rising global military spending and deepening Australia-Japan defense cooperation. ASX -0.09% to 5666, AUDUSD +0.056% to 0.7171, 10y ACGB +4bp to 4.995%.

Central bank speakers: The Fed’s Christopher Waller speaks on the economic outlook; Fed President Tom Barkin speaks on the economic outlook. Fed President Mary Daly participates in a moderated conversation.

Mood: Optimism has strengthened, with iFlow Mood rising to 0.237, driven by an acceleration in equity buying alongside continued selling of core sovereign bonds.

FX: G10 currencies saw inflows, against broad USD selling. Flows were mixed across regions, with inflows in CLP, ZAR, INR and MYR, versus outflows in PLN, IDR, PHP, BRL and COP.

FI: Strong demand for Eurozone, Hungarian and Chinese government bonds, contrasting with selling in Australian, Chilean and Philippine sovereigns.

Equities: Broad-based global buying, led by Australia, Sweden, Brazil, Chile, Hungary, Türkiye, China and Taiwan, with selective outflows in Canada, Israel and the Philippines. Within EM America, the healthcare sector was sold against buying elsewhere, above all in the consumer discretionary, consumer staples and communication services sectors.

“Push the needle into some middle range of guarded optimism.” – Ron Suskind

“Optimism is essential to achievement and it is also the foundation of courage and true progress.” – Nicholas Butler

Food prices in New Zealand rose 3.4% y/y in March, down from 4.5% in February, driven mainly by a 7.3% increase in meat, poultry and fish. Food prices were down 0.6% m/m, led by a 2.9% drop in fruit and vegetables. Elsewhere, petrol prices rose 18.6% m/m and diesel prices surged 42.6% m/m, in the largest monthly increase since July 2011. Petrol prices rose by 13.9% y/y and diesel by 36.9% y/y. Domestic airfares fell 14.4% m/m, while international airfares rose 3.5% m/m. NZX 50 -1.23% to 12906, NZDUSD -0.051% to 0.5886, 10y NZGB +3.6bp to 4.681%.

New Zealand’s electronic card transactions in March 2026 rose by 1.3% m/m to NZ$10bn, with 182 million transactions averaging NZ$55 each. Retail spending increased by 0.7% m/m, driven by fuel (+17.3%), consumables (+1.1%), durables (+1.2%) and motor vehicles (+1.9%), while apparel (-4.2%) and hospitality (-2.4%) declined. Non-retail spending (excluding services) rose 2.5%, and services edged up 0.1%. For Q1, retail spending grew by 1.0% q/q, led by consumables (+0.5%) and hospitality (+0.7%), with apparel down 0.4%. Total electronic card spending increased by 0.4% q/q.

Türkiye’s new house sales rose 1.3% y/y in March to 35,725, while existing house sales fell 3.6% y/y to 77,642 (from 35,281 and 80,507, respectively). Mortgaged house sales surged 35.9% y/y to 25,978, offset by a 9.6% y/y decline in other sales. Calendar-adjusted new and existing house sales decreased by 1.8% and 6.2% y/y, respectively. House sales to foreign buyers dropped 20.0% y/y to 1,353, with Russia, Iran and Germany providing the most purchasers. New and existing commercial property sales declined by 5.4% and 12.3% y/y to 3,787 and 9,712, respectively, with mortgaged sales up 60.1% y/y. BI 100 +0.39% to 14257, USDTRY -0.227% to 44.8655, 10y TGB +7bp to 32.38%.

Türkiye’s April 2026 Market Participants Survey saw the 2026 year-end CPI expectation increase to 27.53% (from 25.38%). The 12-month-ahead expectation climbed to 23.39% (from 22.17%), with the 24-month-ahead measure up to 18.02% (from 17.30%). Average 12-month inflation is mostly expected at between 22.00% and 24.99%, and 24-month inflation at 16.00-19.99%. The year-end USD/TRY exchange rate expectation rose slightly, to 51.23 from 50.97. GDP growth expectations for 2026 and 2027 dipped to 3.5% (from 3.8%) and 4.1% (from 4.3%), respectively. The policy rate expectation for the April MPC meeting is 37.75%.

China’s Q1 GDP breakdown by industry showed 5.0% y/y growth to ¥33.419tn. The primary sector rose by 3.8%, the secondary sector by 4.9% and the tertiary sector by 5.2%. Key contributors included manufacturing (+6.3%), industrial output (+6.1%), financial services (+6.5%), information technology (+10.6%) and leasing/business services (+12.2%). Sizable decreases were recorded in construction (-3.8%) and real estate (-0.1%). Other sectors such as wholesale/retail (+4.1%) and transportation (+4.3%) also recorded moderate growth. CSI 300 -0.17% to 4729, USDCNY -0.066% to 6.8271, 10y CGB -1.6bp to 1.765%.

Singapore’s March non-oil domestic exports (NODX) were up 15.3% y/y, accelerating from 4.0% in February, driven by electronics (+74.0%) including integrated circuits (+113.8%), PCs (+57.3%) and disk media products (+78.3). Non-electronic NODX declined by 0.6%. There were increases in NODX to Hong Kong (99.4% y/y), Taiwan (63.1% y/y), South Korea (44.1% y/y) and China (20.3% y/y), while exports to Indonesia (-56.8% y/y), the EU27 (-11.9% y/y), U.S. (-44.8% m/m, -2.7% y/y) and Thailand fell. Non-oil re-exports (NORX) surged by 61.4% y/y, buoyed by rises for both electronics (+90.4%) and non-electronics (+24.9%). Total merchandise trade grew by 38.5% y/y, with exports up 41.2% and imports up 35.5%, supported by both non-oil (+47.6%) and oil (+6.9%) exports. STI -0.13% to 5001, USDSGD -0.04% to 1.2726, 10y SGB -1.1bp to 2.015%.

Malaysia’s advance GDP estimate for Q1 showed 5.3% y/y growth, down from 6.3% in Q4 2025. The economy contracted by 4.4% q/q, reversing the 3.3% q/q growth in the previous quarter. Growth was driven by services (+5.4%), manufacturing (+5.8%), construction (+7.8%) and agriculture (+2.8%) sectors, though all showed slower expansion compared with Q4 2025. The mining and quarrying sector shrank by 1.1% y/y, impacted by lower crude oil and natural gas production. Key contributors included wholesale and retail trade, information and communication, and transportation and storage, classed within services. KLCI +0.36% to 1696, USDMYR -0.056% to 3.9567, 10y MGB +0.8bp to 3.577%.

Malaysian inflation rose to 1.7% y/y in March, up from 1.6% in February, driven mainly by transport (1.6% y/y vs. 0.7% in February). Core inflation rose to 2.1% from 2.0% y/y. Other contributors included personal care and social protection (7.0%), insurance and financial services (4.9%) and alcoholic beverages and tobacco (2.7%). Food and beverages (1.1%) and education (2.5%) recorded softer inflation, while clothing and footwear declined slightly (-0.1%). Monthly inflation increased to 0.3% m/m in March from 0.2% in February. Q1 inflation came in at 1.6% y/y (from 1.3% in Q4 2025) and 0.6% q/q (Q4: 0.2%).