Market Movers: Blockades

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 6 minutes

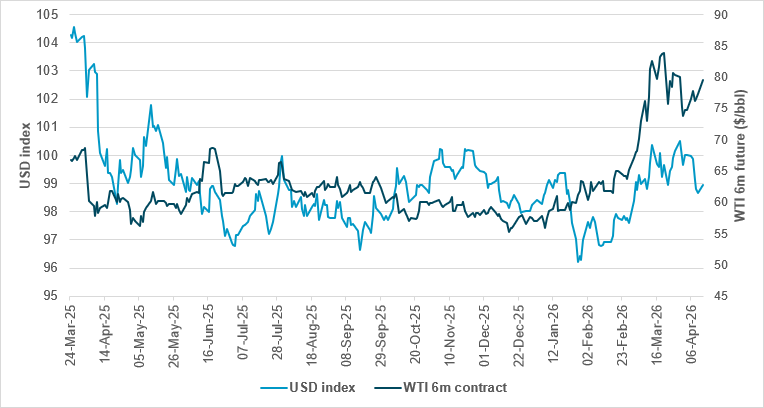

WTI 6m futures vs. USD index

Source: BNY, Bloomberg

The failure of weekend talks between the U.S. and Iran to produce further talks and a deal for peace leaves markets starting the week ahead in risk aversion mode. Stocks, bonds and most FX are all lower. The relationship between oil and USD has looked steady over the last year, with correlations significant at 0.45 or more. However, the April ceasefire shifted that relationship.

The key question for today revolves around whether the divergent moves in oil and the USD that started then will fill the gap back. We will see either sharp gains for USD or some WTI price relief. The problem is not just about today, but about future supply expectations. Oil backwardation is continuing and problematic for measuring the ongoing impact of higher energy prices on the global economy, something that will come under the spotlight in the IMF week ahead.

Hopes for a quick set of U.S./Iran talks and a peace deal have been dealt a setback, and with this came increased risk across markets. The war between Israel and Hezbollah continues in Lebanon. The election in Hungary saw the opposition sweep into power, with Viktor Orbán conceding defeat, complicating U.S. and EU relationships further. USD is up 0.3%, oil is up 8%, bond yields are up 2-4bp and stocks are down 0.5-1.0%. The reaction has been muted compared with other Mondays, as the U.S. blockade plan is seen as less of an escalation than other actions.

Bottom line: Markets are interpreting the blockade as a middle-ground reaction to the failed talks, and consequently as less of a reason to fully unwind risk assets. The problem for today rests in the knock-on effects from higher oil prices and the fragility of global supplies. Chinese reactions to President Trump’s plan will also be key, with the May 14-15 trip seen as important to both nations. The ongoing pressure of geopolitics shows up clearly today in Europe with the Hungarian election. How markets deal with the influence of inflation at the ballot box everywhere will be key in the months ahead. For today, however, USD remains the barometer for trading risk – and its bounce suggests more trouble ahead.

The U.S. Central Command (CENTCOM) will enforce a blockade on all maritime traffic entering or exiting Iranian ports from 10 a.m. ET on April 13, following a proclamation by President Trump. The blockade applies to vessels of all nations at Iranian ports along the Arabian Gulf and Gulf of Oman but will not affect navigation through the Strait of Hormuz to non-Iranian ports. Mariners will receive formal notices and are advised to monitor broadcasts and communicate with U.S. naval forces when operating near the Gulf of Oman and Strait of Hormuz. S&P Mini -0.53% to 6819, DXY +0.299% to 98.944, 10y UST +1.6bp to 4.333%.

Iran’s armed forces have warned that if security at the country’s ports in the Persian Gulf and Sea of Oman is threatened, no port in these regions will be safe. They emphasized that port security must be collective, condemning U.S. restrictions on vessel movements in international waters as illegal and piracy. Iran plans to enforce a permanent mechanism to control the Strait of Hormuz, barring enemy-affiliated vessels from passage while allowing others under Iranian regulations. This statement signals heightened tensions amid U.S.-Iran conflicts over maritime control and follows failed peace talks and U.S. threats of a blockade.

Hungary’s parliamentary election ended Viktor Orbán’s 16-year rule. Opposition leader Péter Magyar’s center-right Tisza party won a two-thirds majority, securing 53.6% of the vote and 138 out of 199 seats. Voter turnout was nearly 80%, a record in post-Communist Hungary. Magyar pledged national unity and constitutional reforms, while Orbán conceded defeat and vowed to serve from opposition. The result signals a shift toward closer alignment with the EU, potentially unlocking suspended EU funds and supporting a €90bn loan to Ukraine. The election marks a significant political realignment in Hungary and the wider region. Budapest SI +2.92% to 136766, EURHUF +2.33% to 366.23, 10y HGB -10bp to 6.55%.

Germany’s coalition government, led by Chancellor Friedrich Merz, has agreed €1.6bn of measures to mitigate rising fuel prices. Key steps include a 17-cent/liter gasoline tax cut for two months and a €1,000 tax-free employer bonus for 2026. These short-term relief efforts are aimed at easing consumer burdens amid the global uncertainties while broader reforms and budget cuts are negotiated to address the stagnating economy. Additional proposals under consideration include enhanced commuter tax breaks and reduced energy levies. The measures reflect the government’s balancing act between immediate support and long-term fiscal adjustments. DAX -0.92% to 23585, EURUSD -0.265% to 1.1692, 10y Bund +0.6bp to 3.064%.

BoJ Governor Kazuo Ueda has highlighted the need for vigilance amid rising crude oil prices and global financial market instability caused by the escalating Middle East conflict. While Japan’s economic and price developments remain roughly on forecast, Ueda warned that a prolonged war could disrupt supply chains and factory output, impacting the economy. He noted that higher oil costs may have mixed effects on underlying inflation, depending on output gaps and inflation expectations. Ueda emphasized close monitoring of the situation’s impact on the economy, prices and financial conditions ahead of the BoJ’s April 27-28 policy meeting. Nikkei -0.74% to 56503, USDJPY -0.257% to 159.68, 10y JGB +2.9bp to 2.467%.

China’s social financing stock reached ¥14.83tn YTD in March, with a m/m jump of ¥5.23tn and 7.9% y/y growth (down from 8.2% y/y in February). Growth was driven by corporate, central and local government bonds. Total loans from financial institutions rose to ¥8.6tn YTD, or ¥2.99tn m/m, up 5.7% y/y (from 6.01% y/y in February), supported by a broad-based increase including ¥491bn in household loans and ¥295bn in medium to long-term loans, indicating housing market stabilization. Foreign currency deposits increased by $6bn to $1.13tn. M2 money supply growth slowed to 8.5% y/y from 9.0% y/y. CSI 300 +0.21% to 4646, USD¥-0.066% to 6.8337, 10y CGB -1.6bp to 1.795%.

Former PBoC governor Zhou Xiaochuan has highlighted a “golden window of opportunity” for the yuan’s internationalization amid declining U.S. dollar credibility, driven by U.S. tariffs, sanctions and geopolitical tensions. Zhou noted appreciation pressure on the yuan due to capital inflows and stressed that China’s trade surplus does not hinder yuan global use. He called for an improved supply of safe, liquid assets and enhancements to yuan convertibility and cross-border financial infrastructure. Zhou urged steady reforms to align yuan internationalization with China’s economic strength, citing recent updates to the Cross-border Interbank Payment System (CIPS) as supportive steps.

U.S. March existing home sales are expected to ease by 0.8% m/m to 4.05 million, from +1.7% m/m to 4.09 million.

Central bank speakers: The ECB’s Luis de Guindos speaks in Madrid.

U.S. Treasury sells $89bn in 13-week bills and $77bn in 26-week bills.

Mood: Risk sentiment improved further, with iFlow Mood rising to 0.155 – the highest since late February (pre-Iran conflict). Equity demand strengthened, while core sovereign bonds saw continued selling.

FX: Broad-based inflows into CHF, NOK, CLP, CZK, INR and THB. Outflows were concentrated in USD, EUR, COP and BRL.

FI: Flows remained light with a mild buying bias, led by Polish, Hungarian and Eurozone government bonds and U.K. gilts.

Equities: Strong buying across G10, LatAm and EMEA; APAC mixed. Sweden, Australia, Peru, Türkiye and Taiwan led inflows, while Singapore, the Philippines and Poland saw the most selling.

“Intelligence is the capacity to receive, decode and transmit information efficiently. Stupidity is blockage of this process at any point…” Robert Anton Wilson

“The defensive power of a pinned piece is only imaginary.” – Aron Nimzowitsch

German producers of building materials (glass, ceramics, stones and earth) reported a significant deterioration in business sentiment in March 2026. The business climate index was down to -23.5 points from -17.9 in February. High energy prices, which represent a large share of production costs in this sector, are weighing on sentiment. More companies are planning price increases, with the price expectation indicator rising to 22.2 points from 8.4. Production cutbacks increased (-9.9 from -5.3), though order books improved compared with last year (-43.5 vs. -63.7). The sector is slowly recovering but faces setbacks due to the impact of the Middle East conflict. DAX -0.92% to 23585, EURUSD -0.265% to 1.1692, 10y Bund +0.6bp to 3.064%.

The Netherlands’ volume of goods exports rose by 1.6% y/y in February, driven by increased exports of machinery, minerals and transport equipment (1.4% in January). Imports declined by 0.3% y/y, mainly due to lower imports of minerals and transport equipment. Export conditions in April have improved compared with February, supported by a less adverse real exchange rate and better producer confidence in Germany. Goods represent about 75% of total exports. AEX -0.34% to 1007, EURUSD -0.265% to 1.1692, 10y NGB +0.9bp to 3.188%.

Dutch corporate bankruptcies rose by 12% y/y in March to 301 cases, 32 more than in March 2025, but fell 3% vs. February 2026. The bankruptcy rate increased to 8.1 per 100,000 businesses, from 7.4 a year earlier. The accommodation and food services sector recorded the highest bankruptcy rate, at 30.6, down from 38.5 in March 2025. Since peaking at 24.8 in March 2015, the bankruptcy rate had declined to a record low of 3.4 in August 2021. It then gradually increased until stabilizing in 2024 and then embarking on a slight downward trend.

Türkiye’s February 2026 trade sales volume increased by 4.0% y/y, while the retail sales volume rose by 15.6% y/y. On a m/m basis, the trade sales volume declined by 0.6%, with the retail sales volume down 0.2%. The volume in wholesale and retail trade and repair of motor vehicles and motorcycles fell 1.5% y/y and 5.5% m/m. The wholesale trade sales volume decreased by 0.1% y/y but increased by 0.2% m/m. The retail trade sales volume showed strong y/y growth but a slight m/m decline. BI 100 -1.44% to 13871, USDTRY -0.208% to 44.7228, 10y TGB +70bp to 32.57%.

Japan’s preliminary money stock data for March 2026 show M2 and M3 increasing by 2.0% y/y and 3.7% y/y, respectively, up from 1.7% and 2.0% in February. Broadly defined liquidity (L) rose 1.4% y/y, slightly down from 2.0% in February. Average outstanding amounts in March were ¥1.280qn for M2 and ¥1.286qn yen for M3. Components of broadly defined liquidity showed mixed trends, with pecuniary trusts up 4.0% y/y and bank debentures rising sharply by 536.2%. These figures reflect moderate growth in Japan’s money supply and liquidity conditions compared with previous months. Nikkei -0.74% to 56503, USDJPY -0.257% to 159.68, 10y JGB +2.9bp to 2.467%.

New Zealand’s services sector struggled in March, with the BusinessNZ Performance of Services Index (PSI) in contraction, falling to 46.0, down 1.6 points from February. This is well below the historical average of 52.8. All five sub-indexes were below 50, with the activity/sales sub-index weakest at 44.6. The sector is being impacted by the conflict in Iran, particularly in discretionary spending areas such as accommodation, cafes, restaurants and cultural services. Employment came in at 46.4, new orders at 45.7, stocks and inventories at 46.2 and supplier deliveries at 47.3. Negative sentiment rose to 69.1% of comments. The poor PSI suggests potential economic contraction, prompting a downgrade in 2026 growth forecasts. NZX 50 -1.22% to 13020, NZDUSD -0.086% to 0.5833, 10y NZGB +5.1bp to 4.756%.

Indonesia’s retail sales for March are projected to have grown by 2.4% y/y, supported by sales in spare parts and accessories; food, beverages and tobacco; and cultural and recreational goods. Retail sales rose 9.3% m/m in March, up from 4.1% in February 2026, driven by information and communication equipment, motor vehicle fuel and clothing, as household demand increased during Ramadan and Eid al-Fitr. February retail sales were up 6.5% y/y (5.7% in January) and 4.1% m/m (from -2.7% in January). Inflation expectations for May rose, while August is expected to be stable. JCI +0.59% to 7502, USDIDR -0.03% to 17103, 10y IDGB +2.7bp to 6.596%.