Tariffs and the Fed

Get in-depth macro data and insightful charts in our Bi-Weekly Macro & Charting, published every two weeks on Tuesdays.

Get in-depth macro data and insightful charts in our Bi-Weekly Macro & Charting, published every two weeks on Tuesdays.

John Velis

Time to Read: 4 minutes

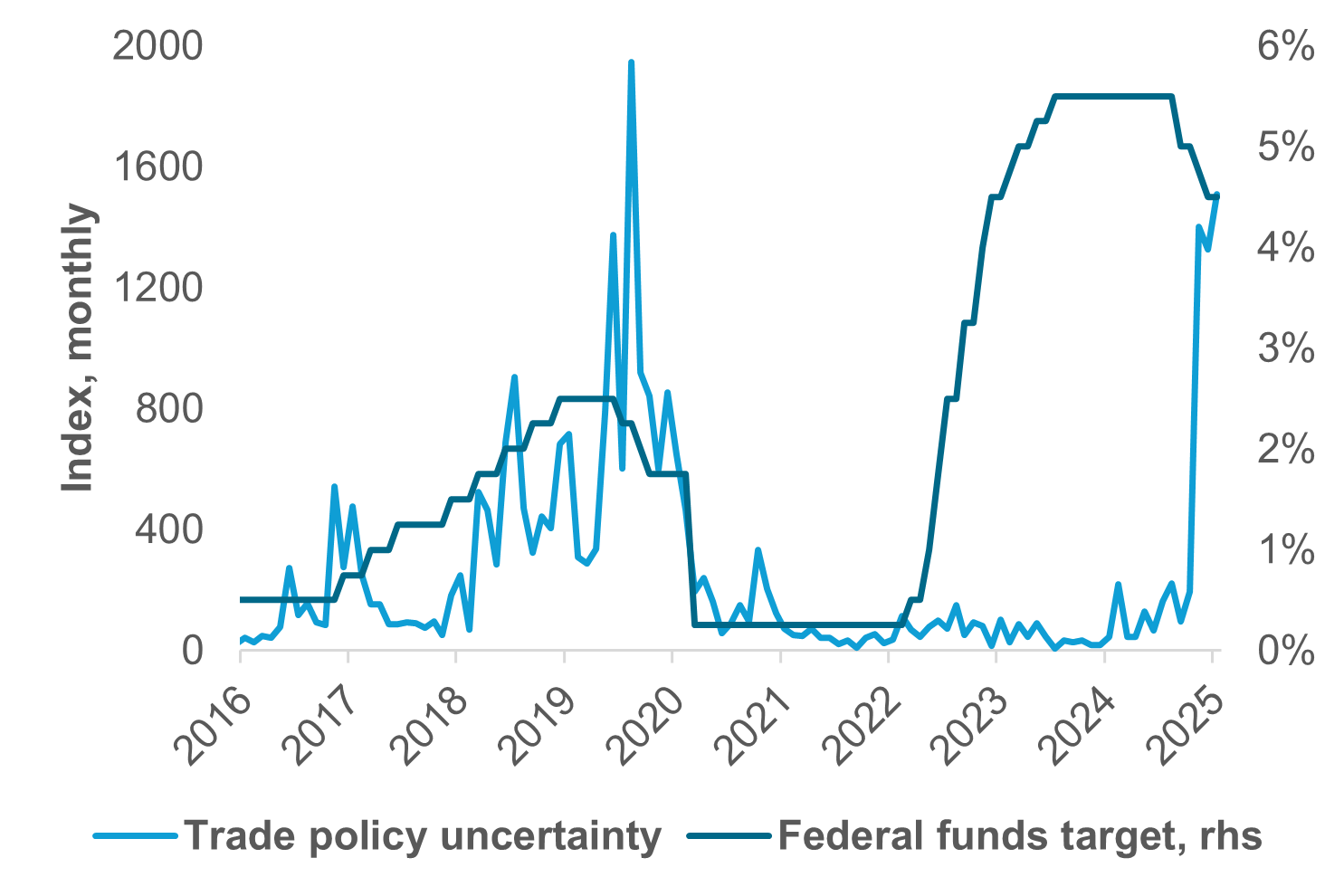

EXHIBIT 1: TRADE POLICY UNCERTAINTY REIGNS

Source: Bloomberg, Federal Reserve Board of Governors

Our take

Tariff news dominates the market, which expects a 25% tariff on Canadian and Mexican imports (and “just” 10% on Mexican oil) and a 10% rate on all Chinese goods. The EU could see a significant tariff increase as well. It’s understood that this broad import tax regime will raise domestic prices, not only for imported goods subject to duties, but also potentially for domestically produced goods that compete with them. What will the Fed do when the tariffs go into effect?

In early January, Fed Governor Waller raised eyebrows during a Q&A when he said tariffs “are unlikely to affect my view of appropriate monetary policy.” We should be circumspect when we consider his remarks. Central banks generally view tariffs as a tax hike more than a source of inflation, causing a one-time price increase that monetary policy is relatively powerless to stop. These shifts in prices from higher import taxes are not akin to an unsustainable increase in aggregate demand which puts upward pressure on inflation over time. In other words, they are not a process within the general equilibrium of the economy which would be driving prices higher. It’s a tax shock.

Exhibit #1 shows the behavior of the federal funds rate over the last decade, including the first Trump administration, when trade policy uncertainty (as measured by textual analysis of news stories) started to increase significantly. While the Fed was raising rates at that time, this was not in response to potential tariff risks. Rather, the Fed was beginning to normalize rates after years of extraordinary monetary policy and potential inflationary outcomes from the 2017 tax cuts. It’s not clear that rates went higher due to tariffs, and inflation generally remained under control over that period. However, the economy was starting to slow in 2019 (pre-Covid), in part responding to the decline in trade caused by the first round of Trump tariffs.

Forward look

If the tariffs go forward, as is likely at present, the Federal Reserve will look through the impact of what is effectively a tax hike and could place more weight on potential output losses and labor market weakness. Estimates are that GDP will fall around a full percentage point – especially if targeted countries retaliate. Inflation could climb 0.5% or more. Should inflation expectations – which have barely budged of late and remain below levels in most of 2024 – spike, the Fed would likely react. Otherwise, we don’t see monetary policy being calibrated to one-time price shifts.

With the “blackout” period associated with the January 31 FOMC meeting now over, we should hear more on the relationship between tariffs, inflation and monetary policy. The growth impact of higher tariffs and retaliation should dominate Fed thinking more than the one-time inflationary impact of the tariffs themselves, but this will take some time. We don’t expect a rate cut in March, but by then the market will have more information on the exact nature of tariffs and some indication of the administration’s fiscal policies put forward – so the March Summary of Economic Projections will be interesting reading across all the major macro variables.

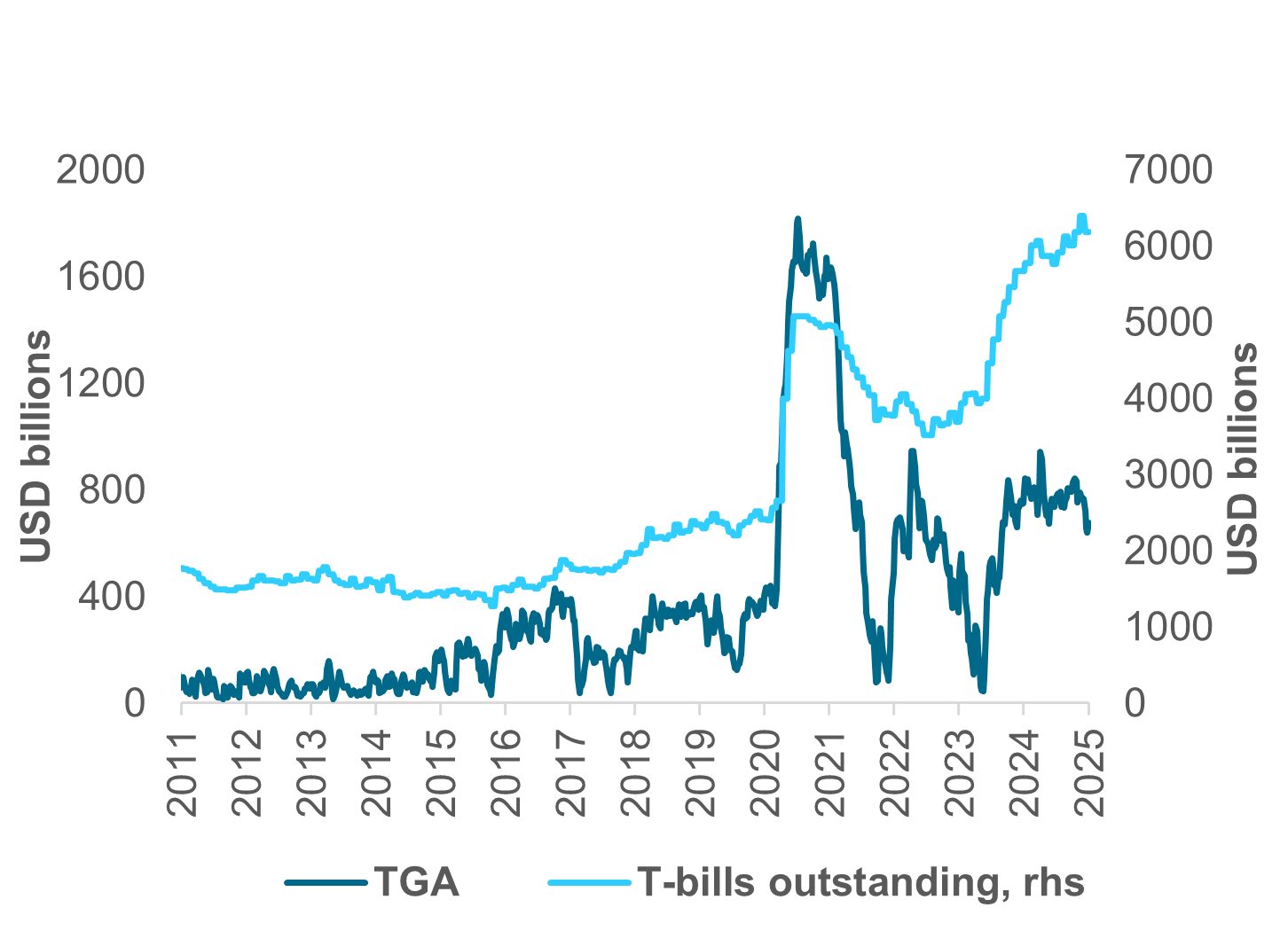

EXHIBIT 2: TREASURY GENERAL ACCOUNT AND T-BILLS OUTSTANDING

Source: United States Department of the Treasury

Our take

We have written a few times recently about the interplay between the Treasury General Account (TGA) and bank reserves against the background of the debt ceiling. Treasury is already engaging in extraordinary measures to avoid hitting the debt limit. Furthermore, due to the devastating fires there California – which pays 16% of all US personal income tax – has been granted a reprieve until later in the year, which will reduce revenues to the Treasury just when it could use them the most.

We have argued that the eventual decline in the TGA would result in increased reserves as the Treasury spends out of what is essentially its checking account. Much of these outlays will lead to rising reserves, giving the appearance of abundant system-wide liquidity. Then assuming the debt ceiling is eventually dealt with, the TGA would rise as it’s rebuilt following extraordinary measures. This would cause the opposite reaction in reserves, bringing them down. How fast the TGA is rebuilt – it had been fairly quick in recent debt ceiling episodes – would determine how fast reserves would fall. Our fear was that the fall in reserves could be so abrupt that it could expose liquidity scarcity in funding markets.

There is, however, another possible outcome. The TGA, which had been well north of $400bn under normal (i.e., non-debt ceiling periods) circumstances since the pandemic – and often higher than that – may not be rebuilt to such levels under the new administration. Particularly if new Treasury Secretary Bessent chooses to emit US debt at longer maturities rather than rely heavily on bill issuance as has been the norm since 2017. A 3- to 5-day buffer for accounts payable might be the target level, i.e., under $300bn.

Exhibit #2 shows the evolution of the TGA and daily T-bill supply. Before the pandemic, the first Trump administration and Biden’s term, it was as low as less than $100bn on many occasions, and T-bill supply was not nearly as heavy during this time. If we return to this now, we could see the concerns we expressed recently obviated.

Forward look

Much remains to be seen as developments play out. The ultimate outcome depends on the debt ceiling and the fiscal package expected later this month. Debt issuance and maturity distribution need to be clarified well. We’ll continue to monitor the debt ceiling and budget reconciliation process for details about target TGA levels.