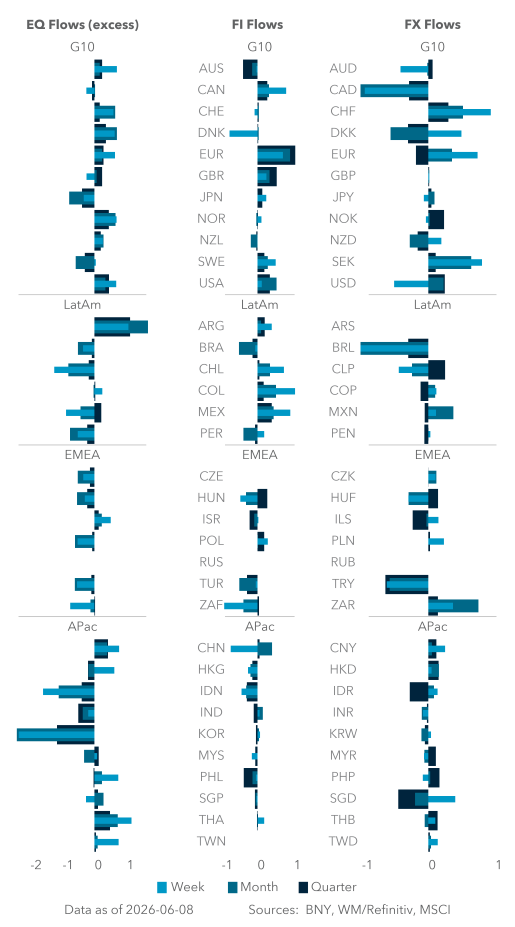

Cross-border confidence can only go so far

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 4 minutes

EXHIBIT #1: EUR AGGREGATE AND CROSS-BORDER HOLDINGS, YTD

Source: BNY

Our take

Last week we highlighted how the ECB decision is finally generating positive rate-differential flows on EUR crosses. Even EURUSD is finding its footing ahead of the decision, and this has helped the currency recover its holdings to flat for the first time in over two months. USD strength has probably added to hedging interest by EUR-based investors on the margins, but we can see that the most significant move has been from cross-border investors and/or non-EUR-denominated accounts. This investor group is naturally underheld in EURs, and for much of the year, hedges were quite large due to fears over the eurozone economy, hitting 50% above the 12-month average hedging level. However, there’s been clear improvement since the ceasefire, even when aggregate EUR positions were still declining. This group’s hedging is now back to “flat” on the rolling 12-month average.

Forward look

Even with a hawkish ECB relative to peers, we believe it’ll be difficult for cross-border investors to reduce hedges further due to nominal differentials, unless there is surge in flows into underlying assets without a commensurate gain in hedging (forward EUR sales). This means that the marginal demand in EUR holdings will have to come from onshore investors or EUR-denominated accounts. In turn, assuming overseas assets aren’t yet being liquidated, hedging relative to underlying asset levels will have to rise sharply. This will only happen if USD strength hits extremes and/or rate differentials move sharply in favor of the EUR. We find both hard to achieve in the near future based on current fundamentals. For the eurozone economy, we still believe the best approach is for the ECB to signal that aggressive tightening is not the base case, allowing some easing in financial conditions through rates and even the currency.

EXHIBIT #2: RETAIL VS. INSTITUTIONAL FLOWS INTO EM APAC SEMICONDUCTORS

Source: BNY

Our take

South Korean and Taiwanese equity markets will likely remain volatile in the near term as the global AI/tech theme continues to struggle with valuations and positioning ahead of key IPOs and share sales. Over the past month, we have been tracking the divergence between retail (ETF-driven) and institutional flow and how it impacted index performance. During the ascendancy phase in April and May, institutional investors struggled to maintain flow momentum due to single-stock ownership limits and other governance restrictions. However, severe underperformance of passive funds risked client outflows and at points may have forced institutional buying where opportunities arose. However, with Fed expectations moving and a permanent conflict deal still elusive, there are early signs retail investors are buckling. Our flow figures across the EM APAC Semiconductor Industry Group (GICS Level 2) show that purchase peaks for retail investors are well below levels seen in February and April, while institutional flows have not seen active buyers since the end of April.

Forward look

Much can still happen in the near term due to various dynamics in place. For cross-border investors (retail or otherwise), the strength of the dollar has helped further widen valuation gaps for EM APAC AI/Tech equities, whose multiples remain attractive relative to U.S. peers. However, given the position of the relevant Asian companies in the AI/Tech supply/product chain, performance will be at risk if capex intentions by global firms (especially in the U.S.) soften. Consequently, U.S. financial conditions remain the key variable in global assets with a high-beta to the AI theme. Recent developments suggest institutional caution, willingly adopted or otherwise, is more justified.

EXHIBIT #3: CANADIAN GOVERNMENT BOND HOLDINGS, TOTAL VS. CROSS-BORDER

Source: BNY

Our take

The Bank of Canada is among the few central banks where easing expectations dominate, but until recently this has not exactly translated into demand for government bonds, whether on a domestic or cross-border basis. Given near-term supply-based inflation expectations are high globally, no amount of domestic weakness can offset the move in breakevens, which in turn undermines real rates. The Canadian five-year breakeven has jumped from 1.9% from the end of February to around 2.25% at present; coupled with divergence against the U.S. in rate expectations, the combination is not a great environment for duration performance.

However, as we head into today’s policy decision, it appears that cross-border investors are now taking a different view. Total holdings into Canadian government bonds, which is largely driven by domestic investors, remains mostly unchanged. In contrast, cross-border investors have seen their holdings gain by close to 12% of the rolling 12-month average. Their current holdings level is at its strongest point relative to domestic flows this year (Exhibit 3).

Forward look

The split has also extended into currencies where cross-border CAD interest is performing well, though not enough to offset outflows by domestic investors. From a cross-border perspective, given asset inflows into Canada as well, there’s potentially greater interest in adding to exposures while CAD remains soft. If valuations can recover from these levels, breakevens can start declining due to FX passthrough. On the margins, Canada may even benefit from terms-of-trade improvement due to developments in energy and commodity markets. Coupled with a more benign core inflation profile, duration looks increasingly attractive. As domestic investors do not have the benefit for USD or FX-conversion to capture CAD valuations, holdings are likely range-bound. Nonetheless, Canadian and wider global duration will remain at risk if the market materially reprices Fed expectations.