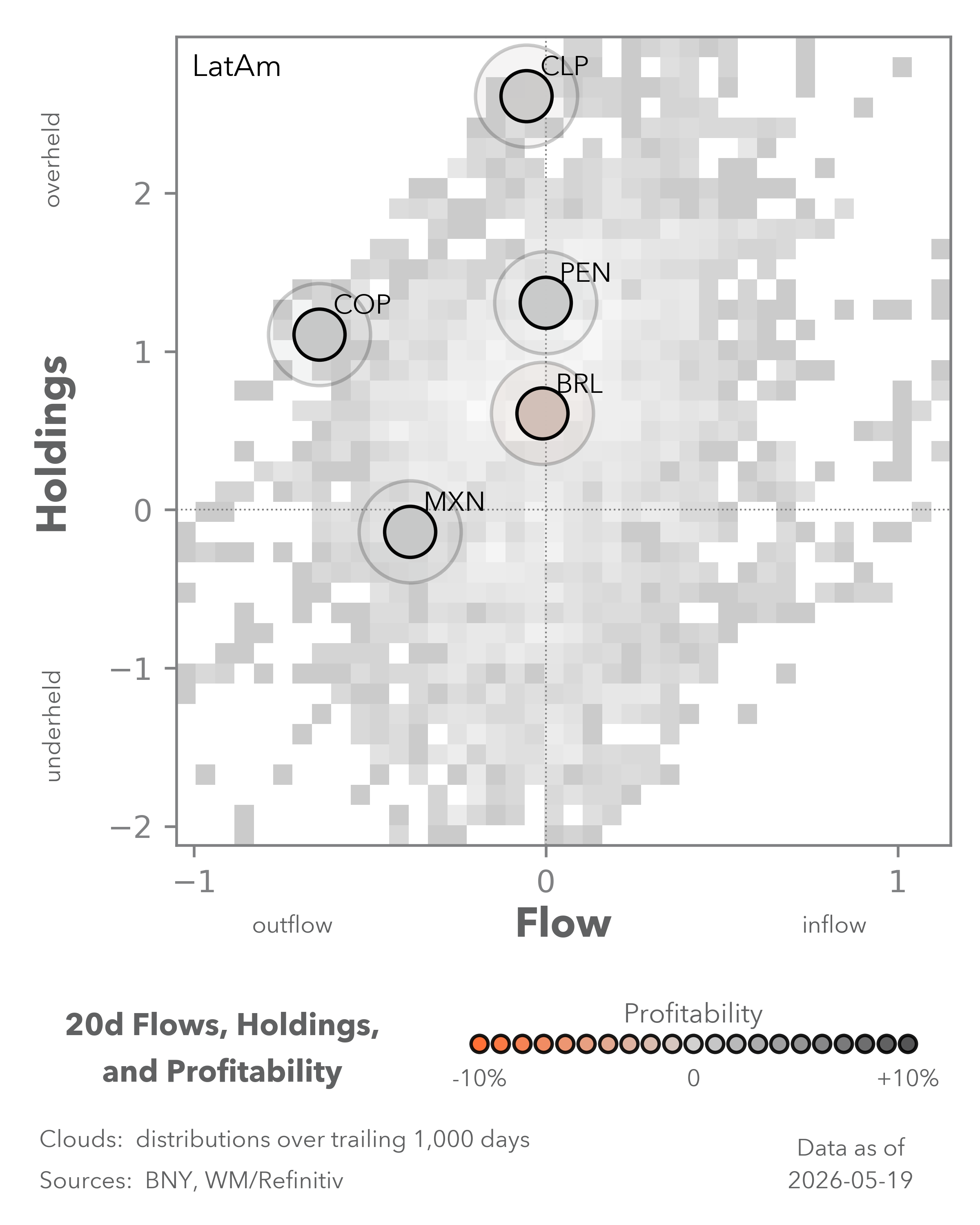

Stress emerges within established themes

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

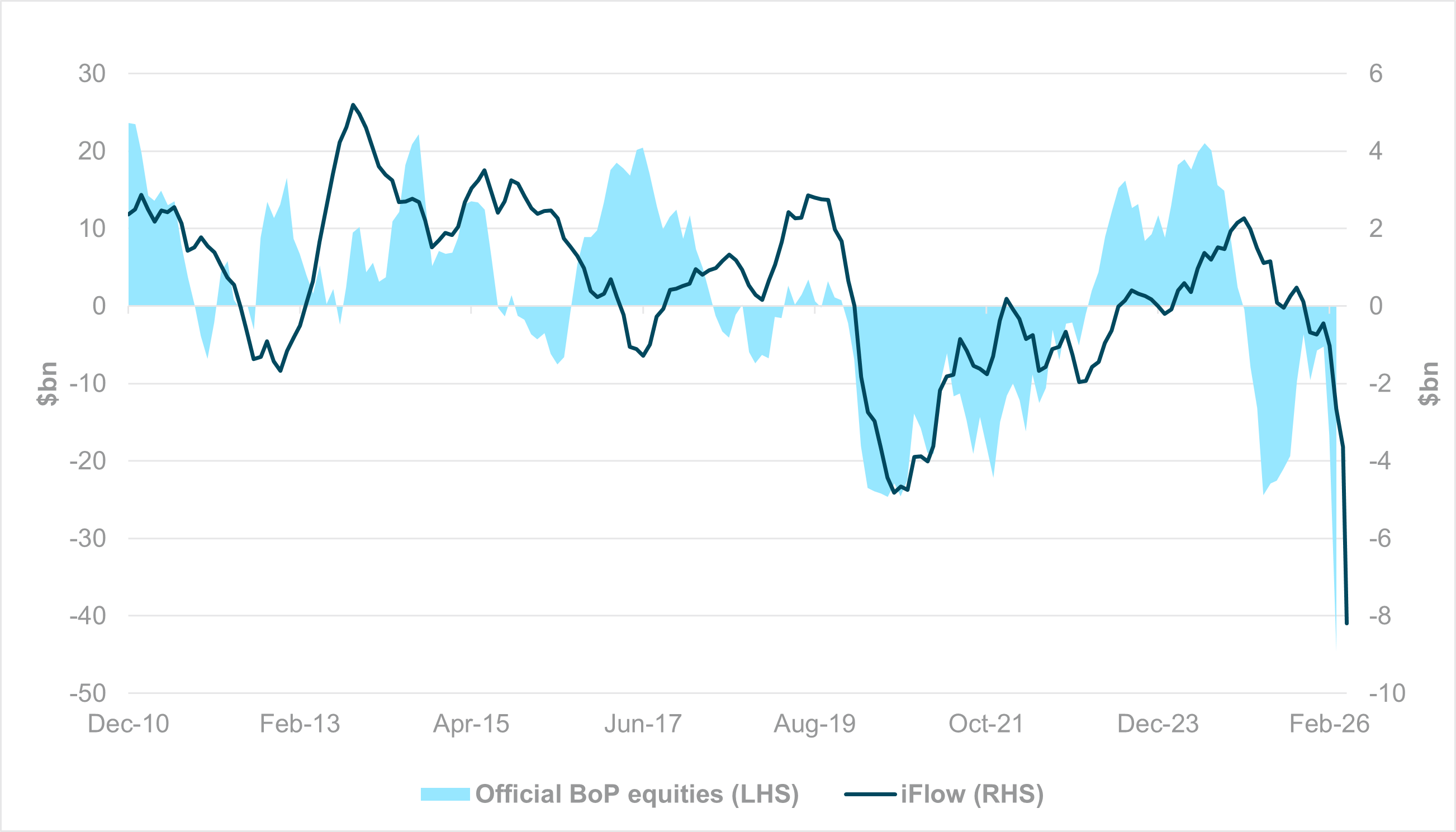

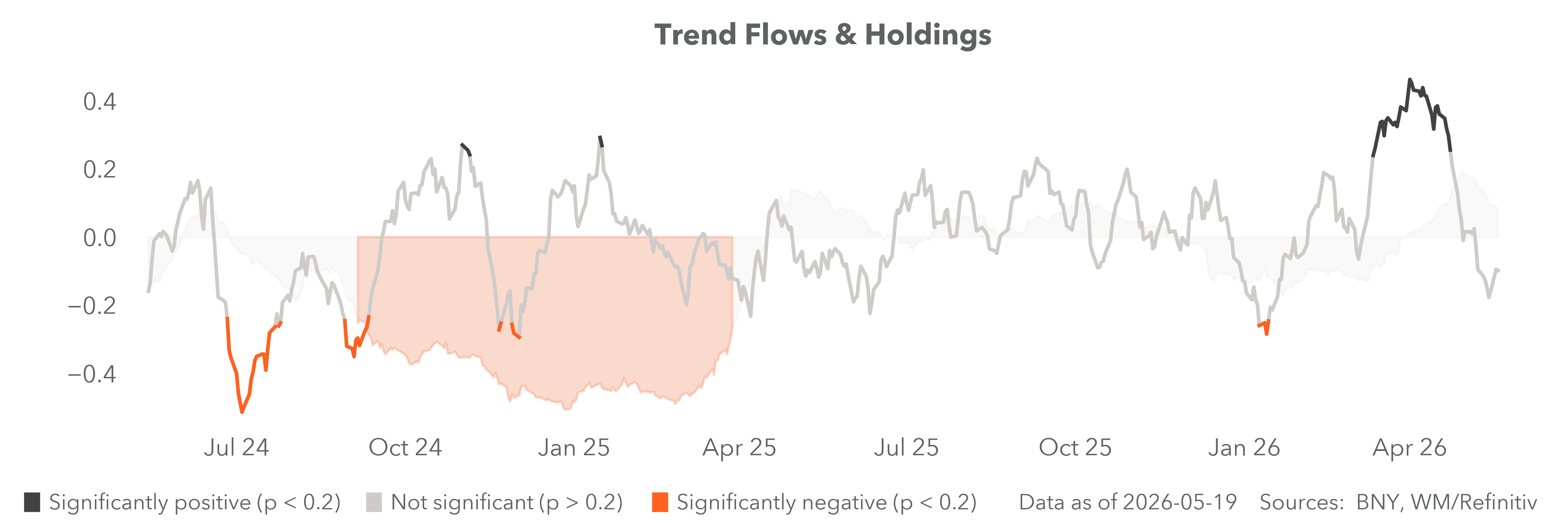

EXHIBIT #1: ROLLING 12-MONTH EQUITY OUTFLOWS FROM SOUTH KOREA

Source: BNY

Our take

Global risk sentiment remains highly sensitive to headline risk surrounding the Iran conflict, but financial conditions will likely continue to tighten as global inflation profiles shift. This is most relevant for the AI/semiconductor theme and the small group of stocks in the U.S., South Korea and Taiwan where positions are concentrated. The KOSPI remains by far the best-performing major market globally, though it saw a significant pick-up in volatility this week. Our flows are now pointing to very heavy institutional selling.

Using our iFlow EM leading indicator, which aggregates daily cross-border security flows and matches them against official data (Exhibit 1), the sharp outflows from outright risk-aversion in March have extended well into April. As iFlow had signaled that flows into South Korea during the rally were increasingly unhedged, renewed outflows could generate the opposite reaction in KRW performance, even though valuations remain attractive due to healthy export trade surpluses.

Forward Look

Clearly, current flows are testing the narrative that the AI/semiconductor theme is secular and can withstand the current supply shock. The original inflow theses rested upon several assumptions relating to the conflict and broader financial conditions. A more permanent ceasefire supports the former – especially if refined products and other downstream Gulf exports such as non-crude mineral fuels and helium gradually resume. The bigger risk is with financial conditions, as even a full end to the conflict in the coming days doesn’t mean full supply chain normalization.

Further, short-term inflation expectations will remain elevated, feeding into yields and heavily positioned equity markets. There will also be a medium-term lift in input costs for Japan, South Korea, Taiwan and most net-energy importers, which will take time to normalize and encumber traditional surpluses. The resulting weakness in currency performance from lower net purchases constitutes a form of tightening onshore, requiring rate hikes to overcome. We’ve already seen preemptive measures in Indonesia on Wednesday and the Philippines earlier this month. The current best-case scenario is for an end to tightening in financial conditions through a policy response to supply risks and inflation – and even then, positioning may need to adjust significantly across the heavily positioned EM markets in APAC.

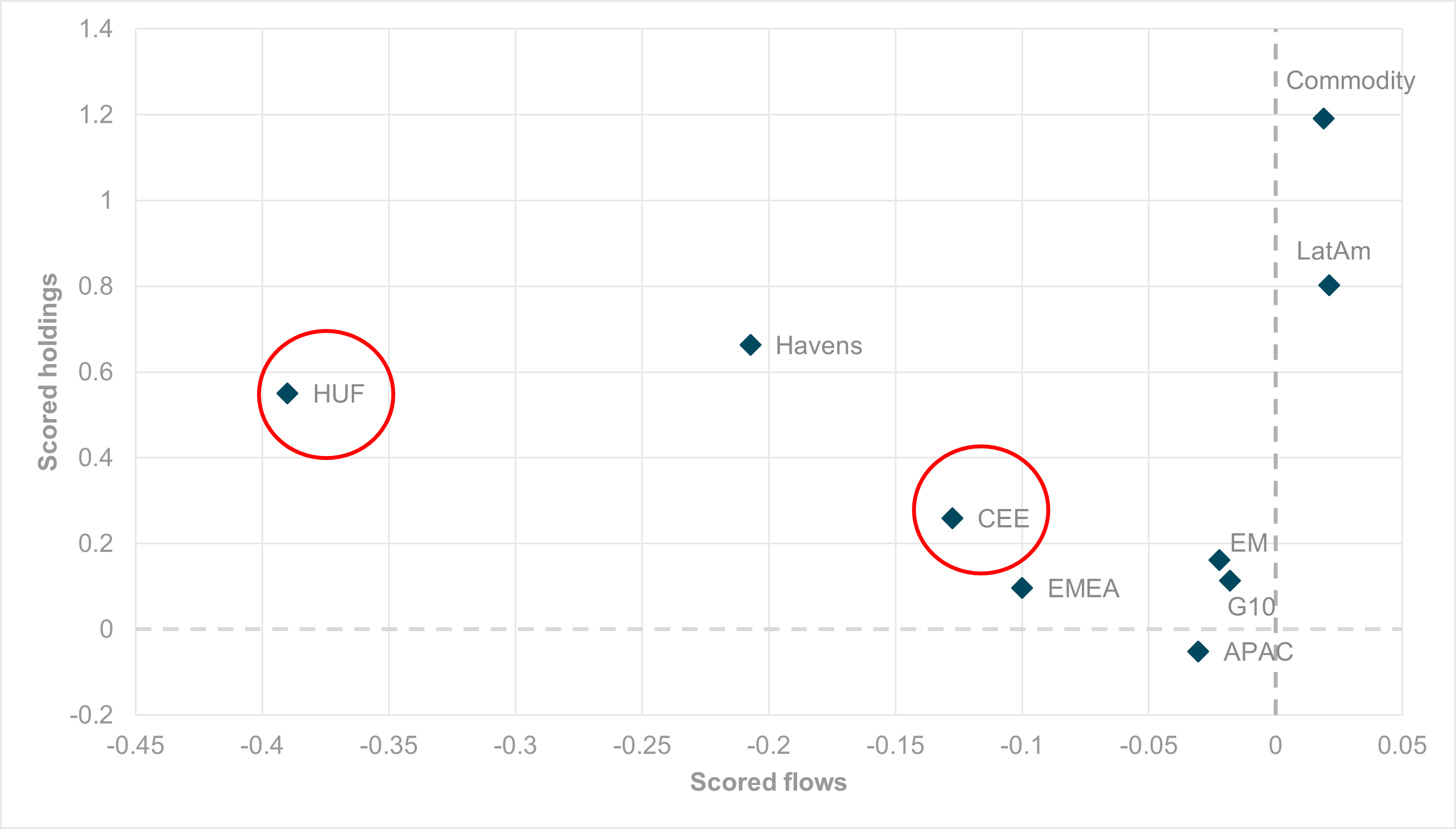

EXHIBIT #2: WEEKLY AVERAGE HOLDINGS AND FLOWS, HUF AND FX AGGREGATES

Source: BNY, Macrobond, BIS

Our take

The National Bank of Hungary (MNB) meeting is the only central bank decision in Europe next week and marks the first meeting since Prime Minister Péter Magyar took office. We maintain that positioning across Hungarian assets hit its limits in the run-up to and wake of the election, as the new government must now deliver on the change it promised. The foreshadowing of a sharp fiscal adjustment due to the previous government’s “budgetary failure” should help obviate the need for additional restraint from the central bank, while a funding deal with the EU is also expected very soon.

Finance Minister András Kármán also laid out fresh criteria for market confidence, stating that “the drop in risk perception should primarily be expressed via a lower cost of debt financing and not necessarily via an excessive forint appreciation.” In this context, the new government is clearly not targeting short-term carry inflows to bring down inflation, but rather a reduction in term premia through greater fiscal prudence. We suspect the view is that if the market believes in fiscal plans and unhedged bond purchases materialize, the currency will take care of itself.

Forward Look

Next week’s decision will test the thesis that markets will gravitate away from short rates and more toward duration. The recent MNB surprise cut on its interest rate on foreign-currency swaps, pointing to an “improving market and liquidity conditions,” suggests the MNB is also more relaxed about FX performance. This points to an unchanged decision, while maintaining vigilance in line with peers globally. In addition, hiking rates so quickly after the FX swap rate move would send inconsistent signals with respect to policy transmission. This doesn’t mean that the FX angle should be abandoned completely – our data indicate that HUF is now leading carry trade unwinding, and CEE is also one of the worst-performing currency aggregates. Holdings are relatively comfortable, but if the global inflation shock is more prolonged, a sufficient front-end real rate buffer remains necessary.

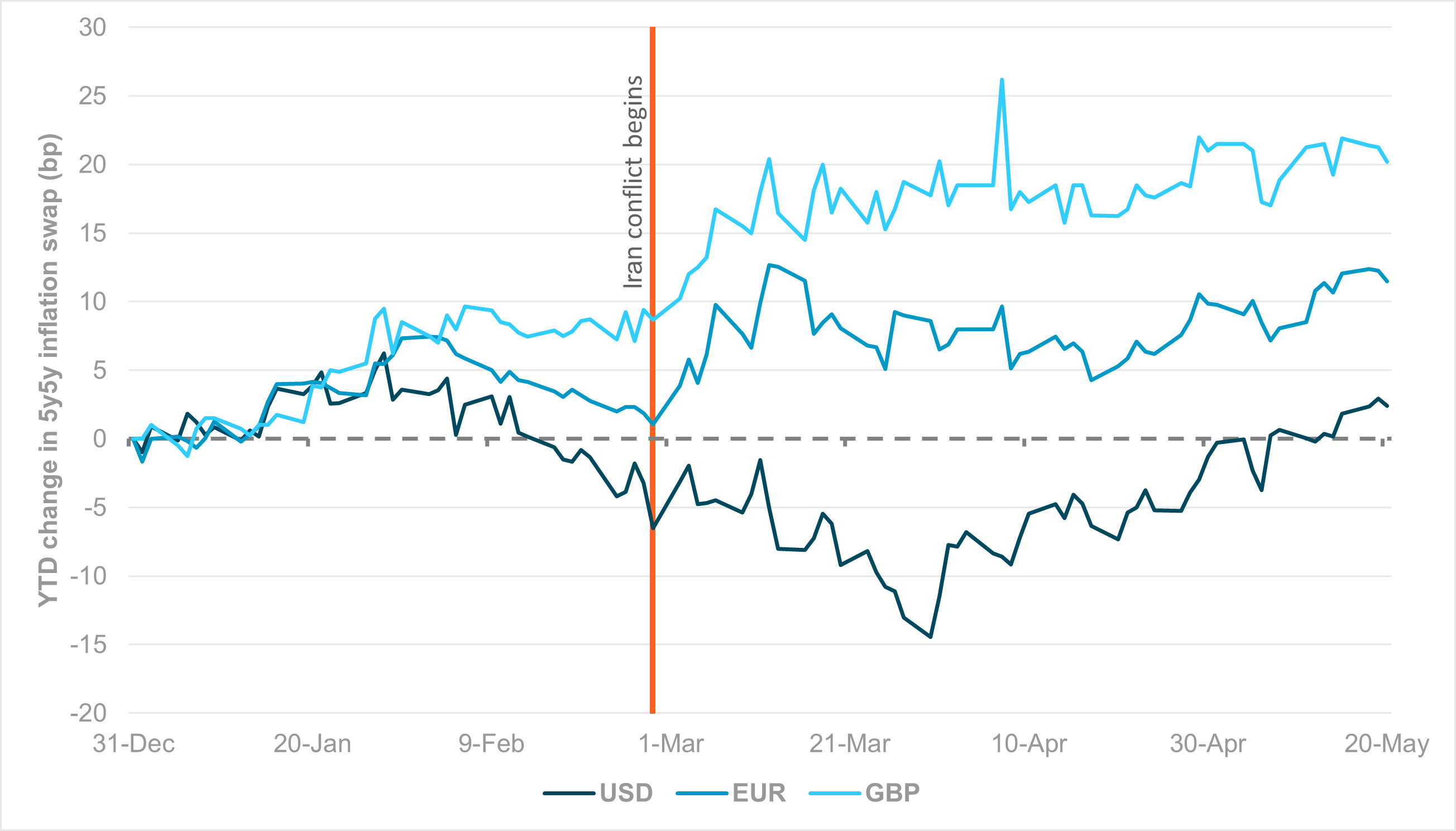

EXHIBIT #3: CHANGE IN 5Y5Y INFLATION SWAP, YTD (BP)

Source: BNY, Bloomberg LP

Our take

Although all sides of the Iran conflict are inching toward a solution, we believe the market is more attuned now to the risks of prolonged disruption and stagflation for economies with poor energy resilience or swift price transmission. This has been Europe’s base case since the beginning of the conflict, but the U.S. is clearly catching up.

Based on 5y5y inflation swaps, even after the first month of the conflict, U.S. long-term inflation expectations were around 15bp below levels seen at the beginning of the conflict, whereas U.K. and Eurozone equivalents had moved materially in the opposite direction, where they have remained even with the prospect of a permanent ceasefire. However, as U.S. data have begun to shift, the disinflation premia have swiftly eroded, and the 5y5y USD inflation swap is back to its levels at the beginning of the year and continues to rise. While there are crucial differences between the U.S. and European economies – being a net energy exporter and lower trade dependency to name a few – the experience of inflation expectations on the other side of the Atlantic justifies strong vigilance. We expect further convergence in inflation expectations through the second half of the year, which means further upside risk of up to 10bp should the change reach Eurozone levels (Exhibit 3).

Forward look

Despite the potential 25bp swing from end-March in the 5y5y, we don’t see such a move undermining the dollar, even if the Fed doesn’t react – nor should it, given its forecast horizon. For onshore investors, the moves in long-dated yields have been far larger than inflation expectations alone, which pushes up real rates across the curve and renders flows far more attractive to onshore bond investors. This has been tracked well in iFlow. The U.S. has also benefited, to the extent that even external bond managers are re-entering the U.S. Treasury market, assuming that savings levels and trade surpluses begin picking up again while long-dated yields remain at a high level. The bigger risk to the U.S. is that real rates remain attractive such that rotation away from equities picks up in earnest and financial conditions tighten more than expected through the equity financing channel. Getting the right balance is essential, and what has worked for flows into the USD and U.S. duration may no longer work for the equity market.