Selective risk rally cannot be ruled out

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

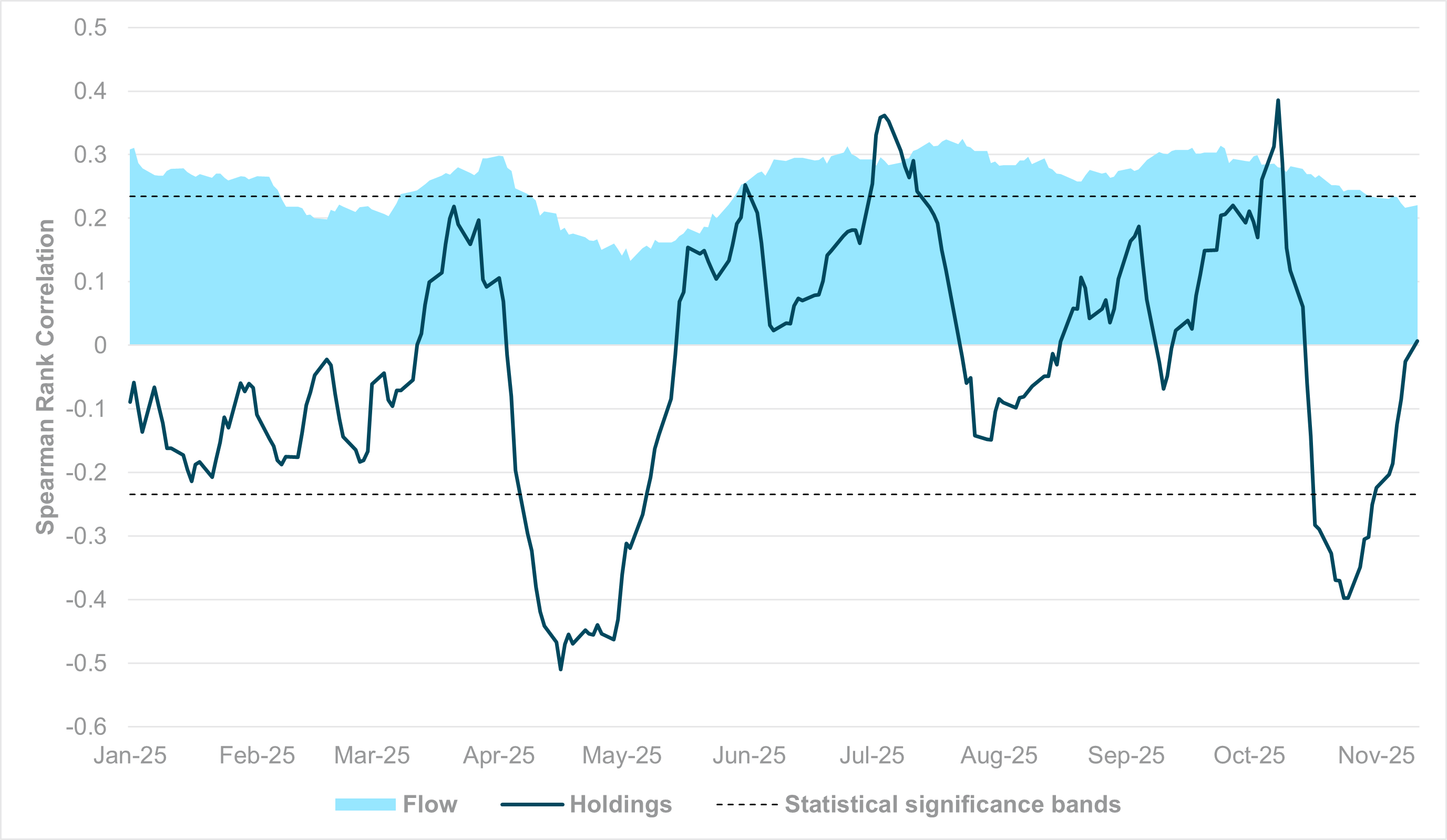

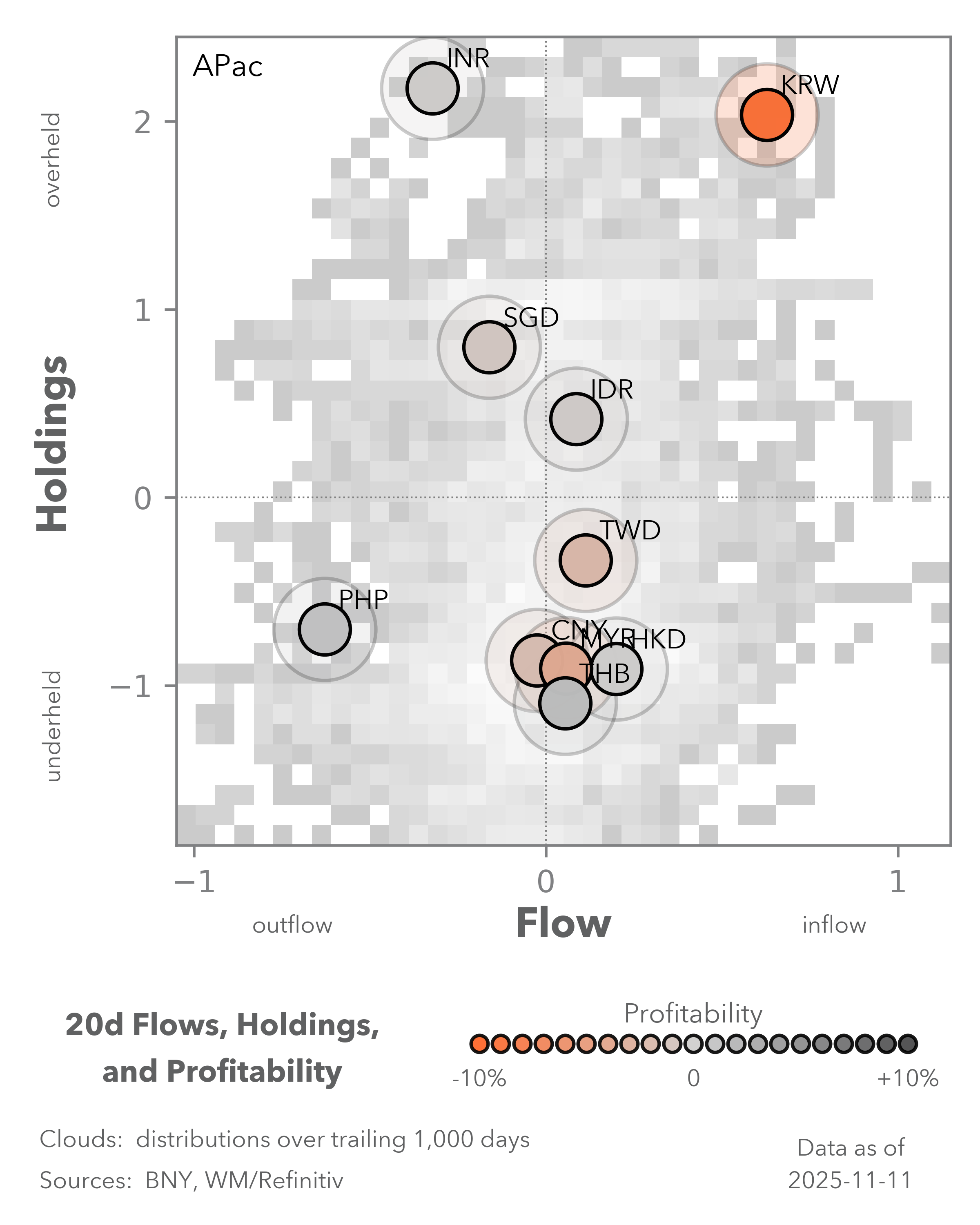

EXHIBIT #1: IFLOW CARRY, HOLDINGS AND FLOW INDEX

Source: BNY

Our take

Market reaction to the end of the U.S. government shutdown has not been straightforward for risk appetite. Equity valuations remain in focus, and the signals from FX are similarly inconsistent. For example, after only the second material round of carry unwinding this year, seen in October, carry trades based on the alignment between currency yields and flows have recovered in a risk-positive direction. High-yielder flows are normalizing, while safety names are again under pressure. We should not rule out a “Santa rally” in FX carry trades before year end.

More importantly, reduced holdings resistance is in play, as October sales undermined high-yielders. Our iFlow Carry holdings index has now fallen to neutral for the first time in six months. This development is significant: Unlike flows, the “normal” level for carry holdings is positive. By definition, not owning high-yielders, or not being under-held in low-yielders, incurs a cost of carry. Consequently, FX markets have approached the end of the shutdown and year end in a defensive position, yet the path for carry recovery is relatively clear. The bigger question is how to define the carry trade into the year end or even 2026, especially with most traditional emerging market (EM) high-yielders still in their respective easing cycles.

Forward Look

We continue to be confident in the central bank credibility of EM countries, which normally constitute the high-carry group. However, we are increasingly concerned about government fiscal outcomes and the pressure on central banks to apply additional easing measures.

Although this is a widespread phenomenon across developed and emerging markets, flow sensitivity to lower real yields is far greater among EM economies. We expect any carry flow to be cautious and selective, given that some of the strongest pressure is now in Latin America and EMEA, while even APAC central banks are leaning dovish. In other words, while low-yielders will continue to struggle and drive one leg of carry interest, flow distribution into high-carry names will be very narrow.

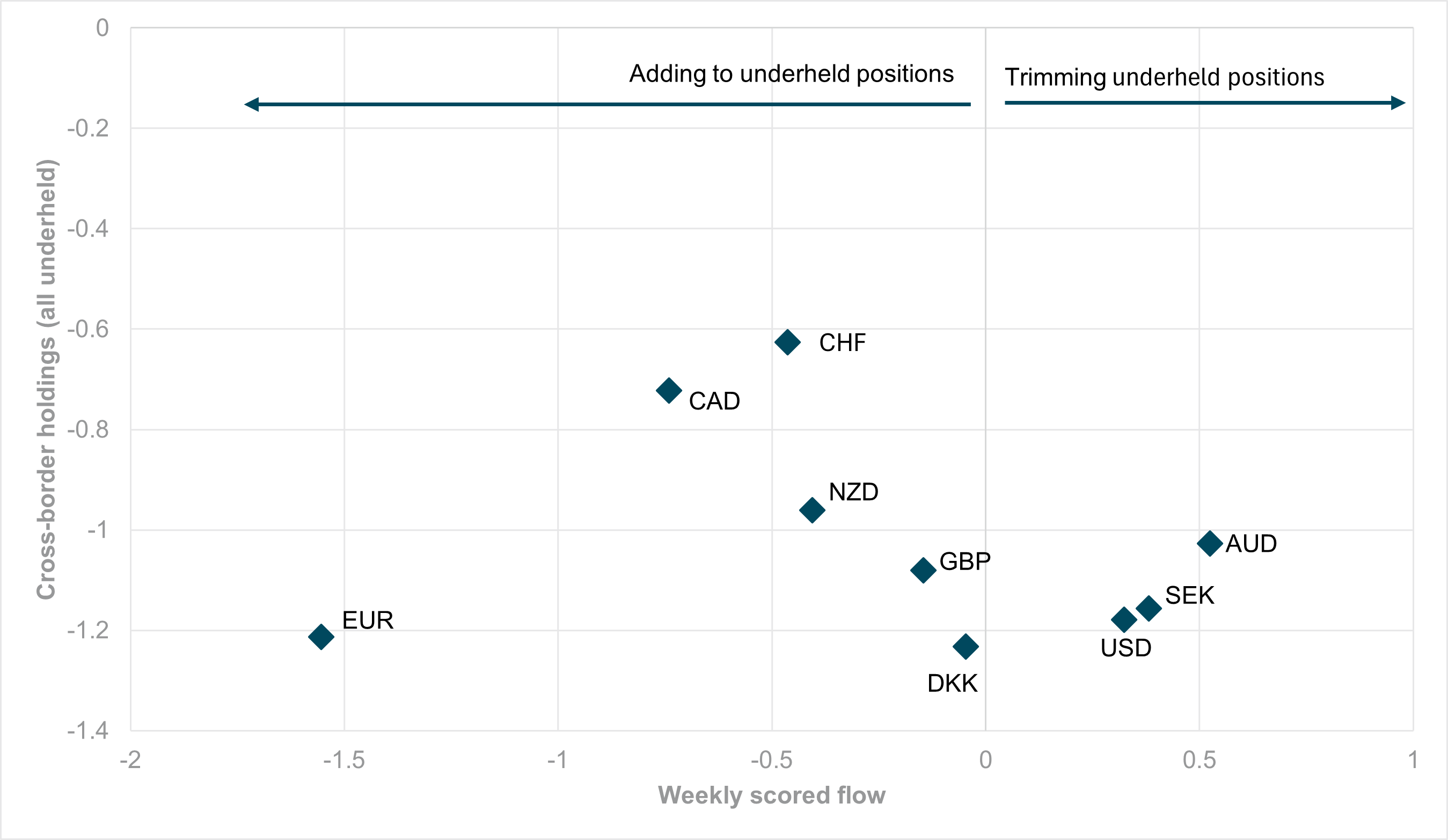

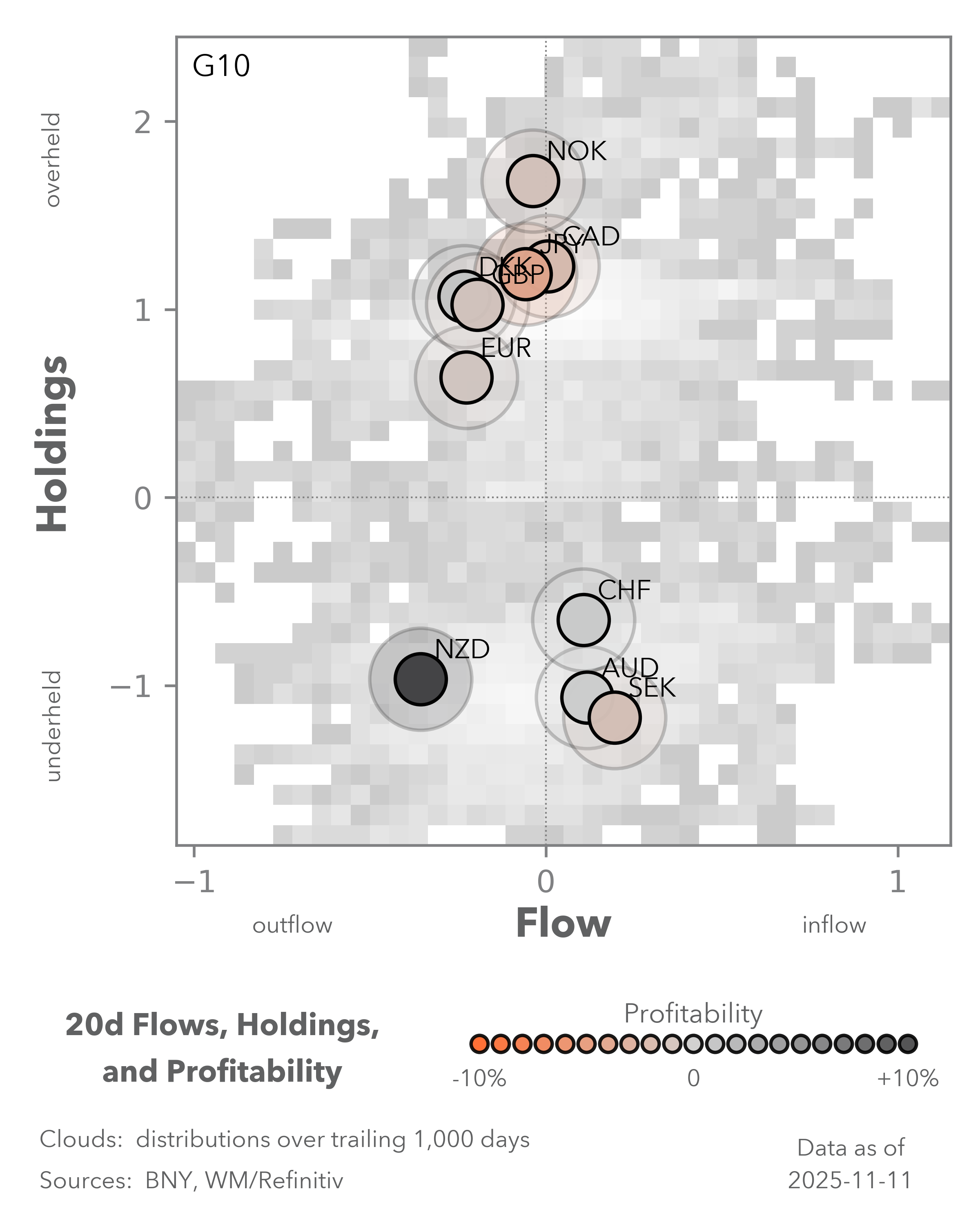

EXHIBIT #2: G10 CROSS-BORDER HOLDINGS VS. FLOW, ONE-WEEK BASIS

Source: BNY

Our take

Risk appetite may be slowly emerging in EM carry, but the same cannot be said for G10 holdings. Despite the U.S. government reopening being priced back into markets, iFlow cross-border flows for underheld currencies – typically current hedges on underlying assets – have continued to show additional selling. The dollar has found some recovery flow, even as U.S. growth and policy outlooks face their own challenges.

The distribution of currency flow, however, continues to point to the importance of policy divergence. For example, the market sees only limited scope for easing by Australia’s central bank, while the Fed has pivoted back to a stance that left a December cut open. At the same time, Sweden’s Riksbank no longer sees potential for easing, already at very low levels. The Norwegian krone and Japanese yen (JPY) remain overheld, which is unsurprising given that Norges Bank and the Bank of Japan (BoJ) hold among the most hawkish policy stances in the G10.

Forward look

Flow divergence within the G10 supports the carry-recovery narrative, though no central bank in this group ranks highly enough in yield to drive it in either flow or holdings. However, increased hedging in the euro (EUR) and British pound (GBP) by cross-border investors and rising position sizes suggest that Europe’s growth outlook is becoming even more challenging. The franc (CHF) is far less underheld for safety purposes, but even with news of an impending U.S. trade deal, it is struggling to regain a favorable position.

We expect G10 hedging interest to remain relatively strong into year end, as no currency’s current hedging levels are materially above changes in asset holdings. However, the scope for policy surprises in a dovish direction remains high for many, and asset allocators clearly do not wish to be caught offside any pivots.

EXHIBIT #3: JGB AND JPY FLOWS, WEEKLY SMOOTHED BASIS

Source: BNY, Office for Budget Responsibility

Our take

Japan’s Finance Minister Satsuki Katayama’s comments on the JPY this week led to noticeable strength in the currency. As the U.S. dollar (USD) to JPY exchange rate moves through 155 – well above Katayama’s now disavowed “fair value” estimates of 120–130 – the risk of a renewed round of imported inflation is high. The Federal Reserve’s outlook doesn’t point to any interest rate favors into year-end.

However, Japan’s new government still faces difficulties reconciling a strong fiscal package with market unease over increased issuance. Liberal Democratic Party (LDP) policy chief Takayuki Kobayashi stated that “there is still quite a gap” between the government’s view and that of Ministry of Finance officials. The market does not expect a smooth fiscal path or ongoing attempts to delay BoJ hikes. These factors undermine interest in Japanese assets, but the weak performance of the JPY and Japanese government bonds (JGBs) since the LDP leadership election may have already created a sufficiently large holdings gap for Japanese assets. Our data show that recent JPY flow is now at its best level since late September, and JGB flows have also firmed up since late October, suggesting that the worst is over for now.

Forward look

The lack of additional selling does not imply that return flows will pick up, especially in a slightly more carry-friendly environment. We noted last week that JPY crosses are no longer a factor in the yen’s overall holdings, and USDJPY will have to contend with a more favorable dollar environment. Nonetheless, the bar is now lower for a tactical flow recovery in Japanese assets. Key assumptions include one more BoJ hike this year and a credible fiscal package. The JPY remains overheld in iFlow on an aggregate basis, suggesting cross-border positioning for hikes and valuation improvements remain intact. The LDP should seize this window of opportunity for a balanced package and help Japan’s asset holdings consolidate.