Our take

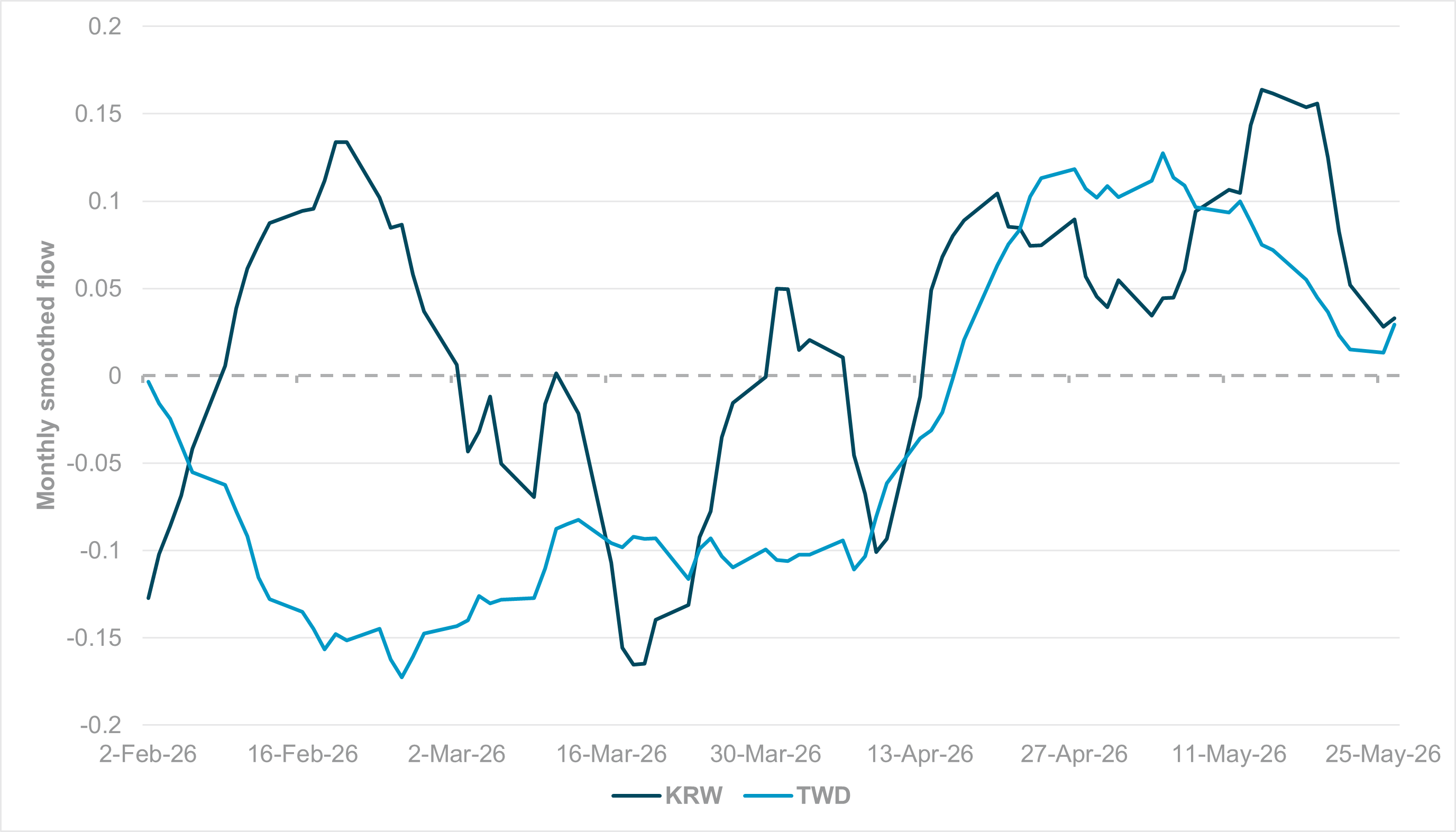

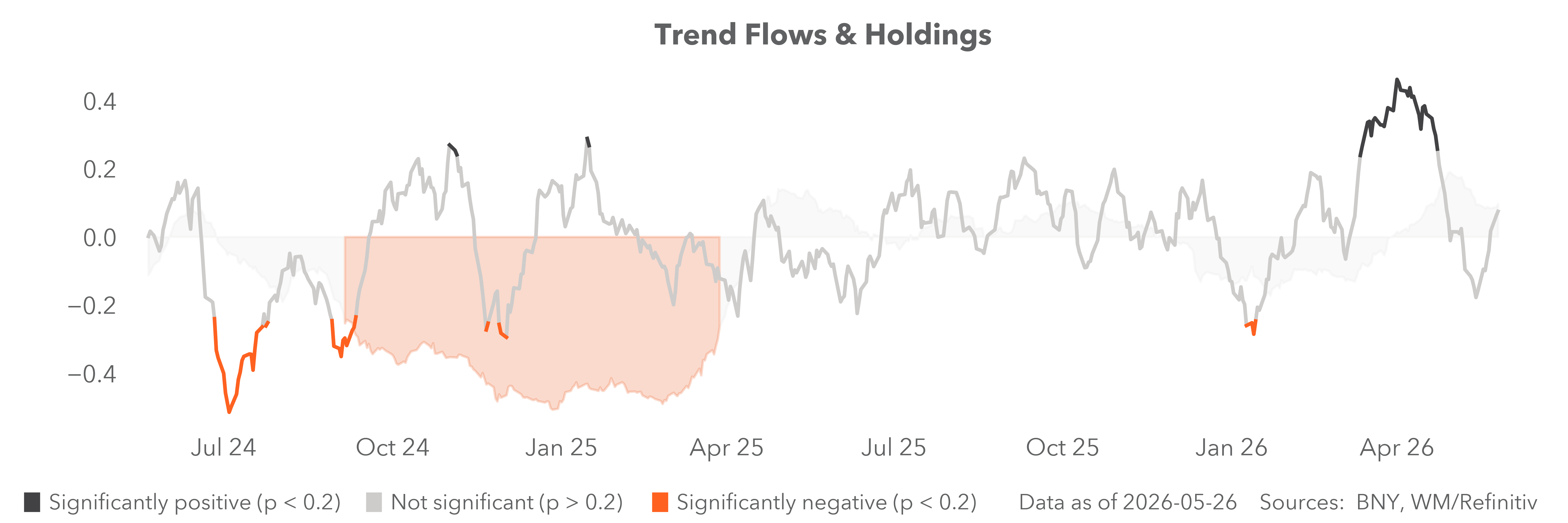

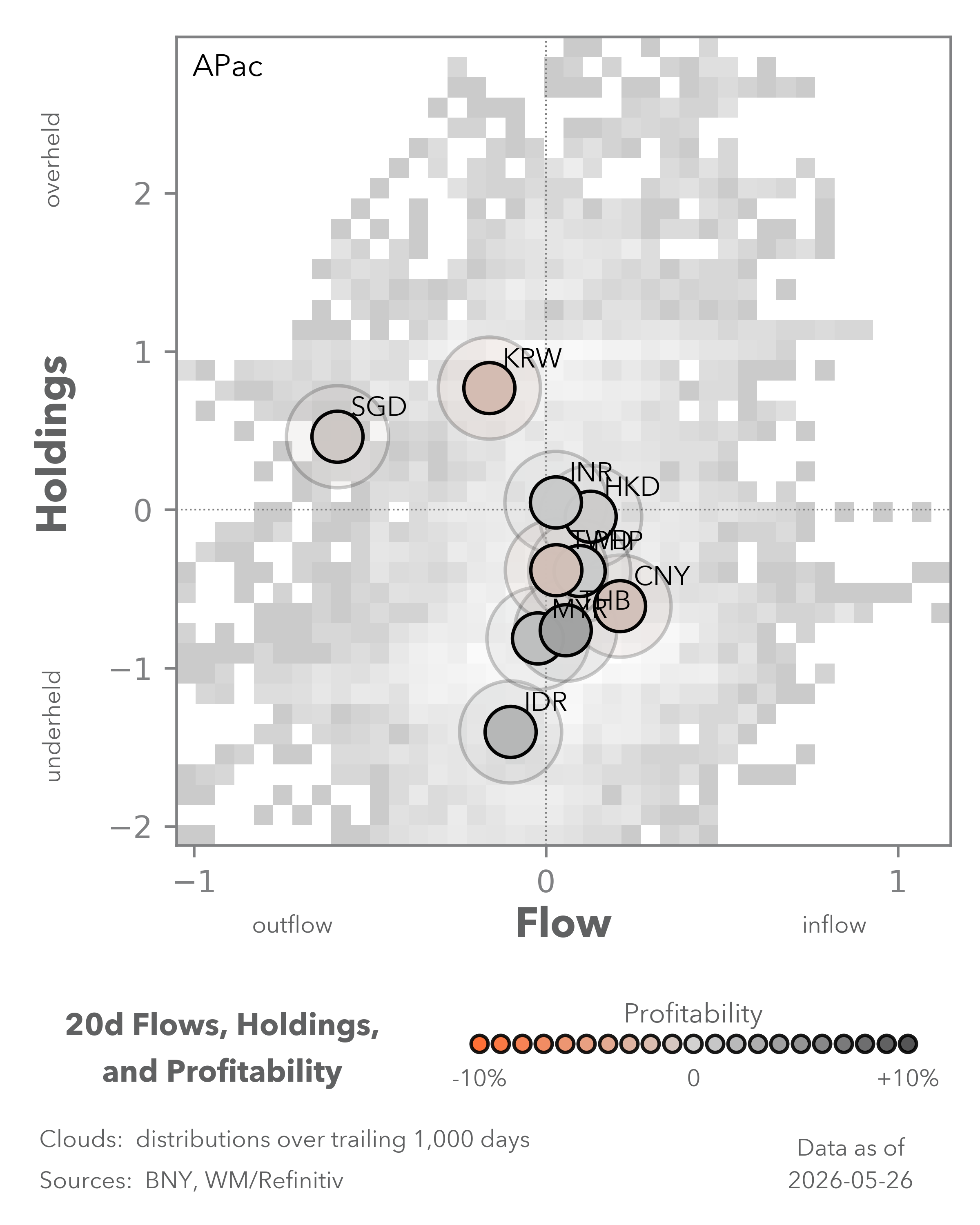

KRW and TWD are not part of general rebalancing calculations, mainly due to very weak international participation in fixed income markets, but the alignment between FX and equity performance is now material. As of Wednesday, KOSPI’s year-to-date gains are tracking 100%, while the TAIEX is also above a healthy 50%. Even though extreme equity gains should generate some hedging/rebalancing interest, we have seen how cross-border investors are almost “forced-in” into re-rating markets (South Africa last year being a recent example). Our flows indicate that as sentiment recovered with the ceasefire in April, there were some signs of outflows materializing through mid-May, as total exposures had begun to look excessive. However, on a monthly smoothed basis, neither KRW nor TWD have fallen back to net selling, and performance is well aligned.

Forward look

Extreme growth and surpluses generated through the semiconductor sector will require a policy offset – either through outright tightening or allowing gains in the real effective exchange rate. Both factors will strongly support the need to reduce hedge ratios, while leaving currency exposures more exposed to equity market factors rather than domestic fundamentals – such as inflation driven by higher import costs and energy supply. The two are linked, of course, as problems with the latter will cause production difficulties in the companies involved.

However, for the same reason that “U.S. exceptionalism” is returning, the market is viewing trends as secular, and any short-term pullbacks might find dip-buyers. The client breakdown of flows into South Korea, as we expected, indicates heavy institutional recovery flows heading into month end. The strong retail presence in KOSPI during the more volatile months around mid-May appears to have succeeded in attracting underperforming institutional flows back into the market.