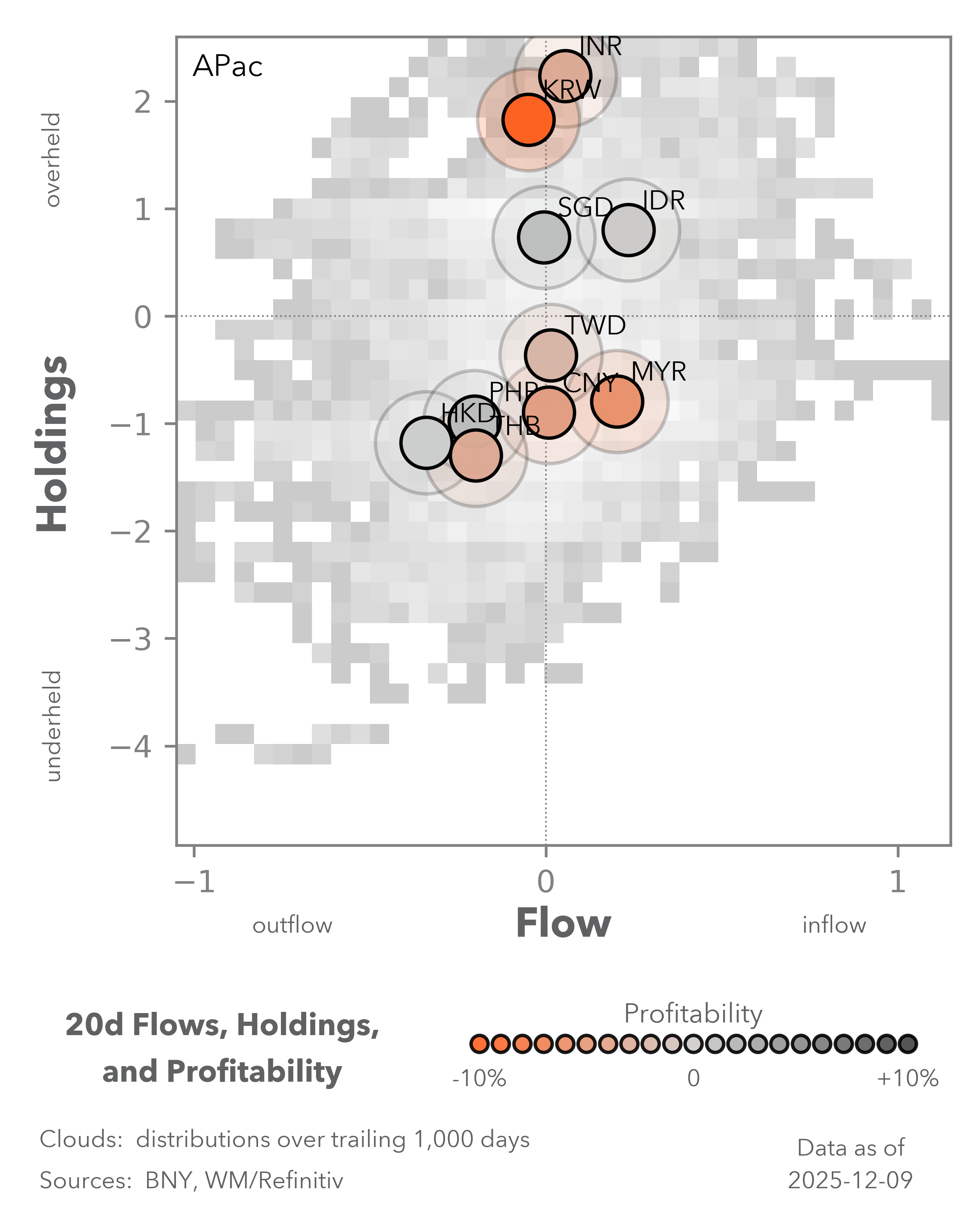

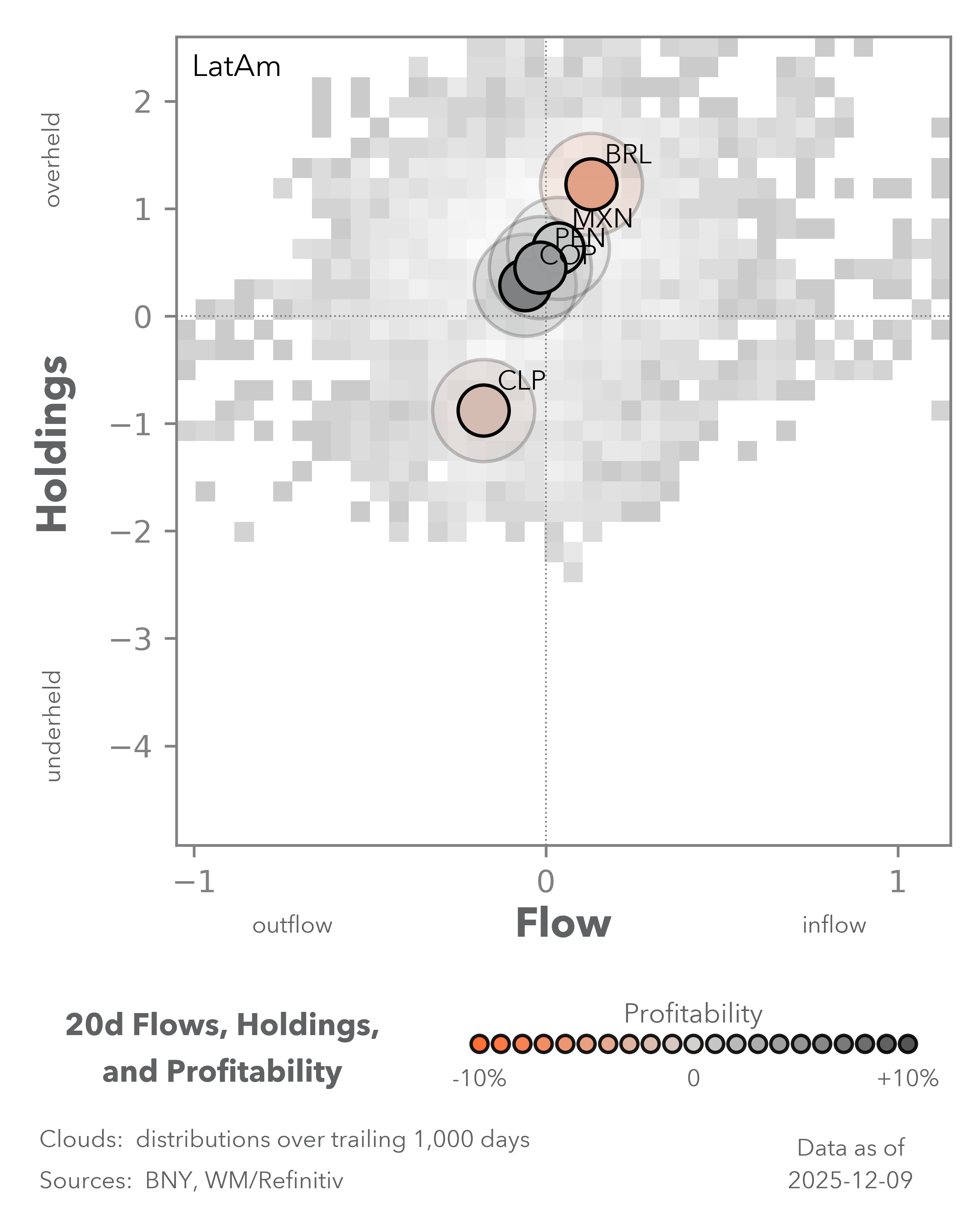

Inflation and Reflation Fuel APAC, Europe Flows

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

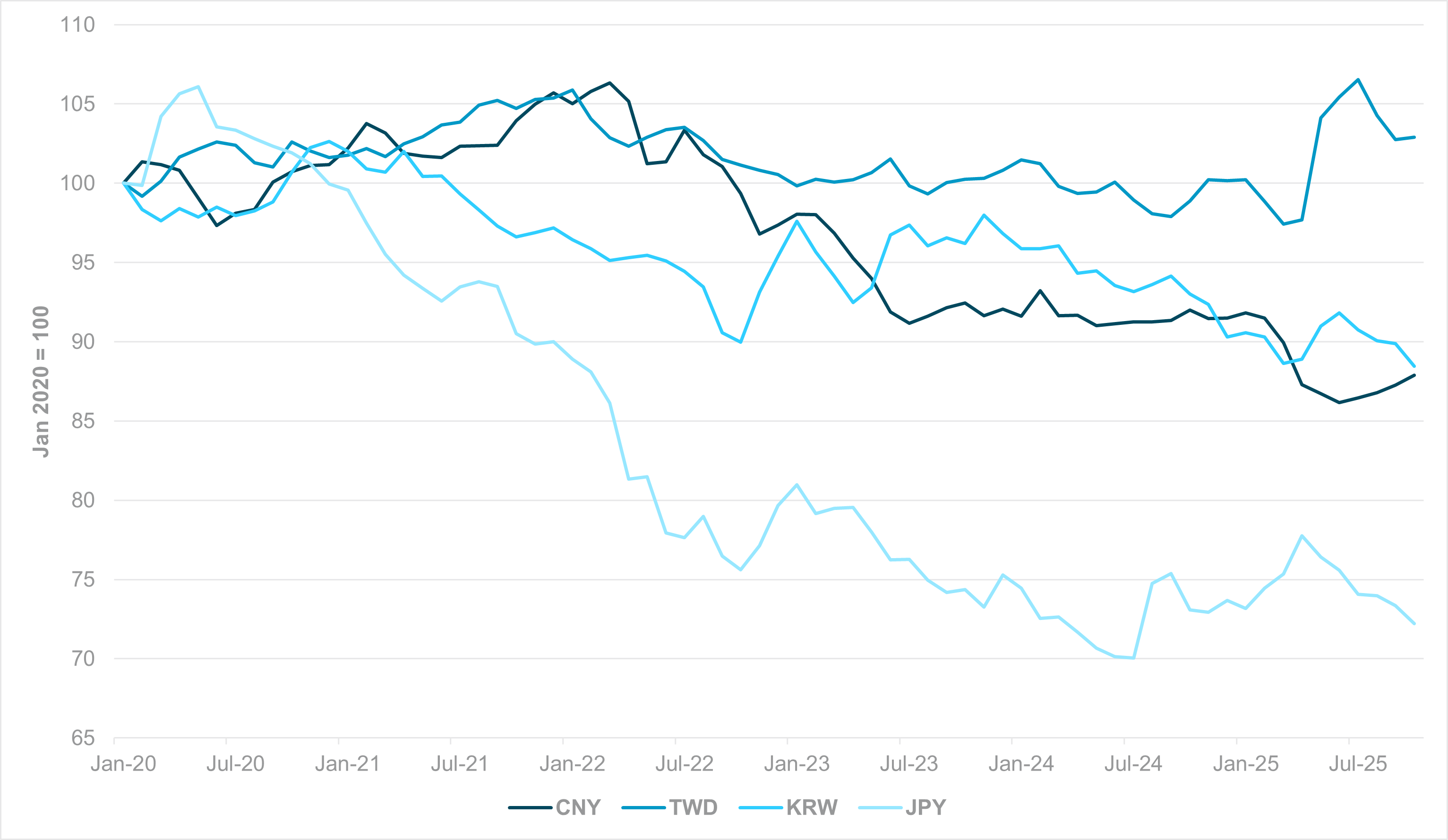

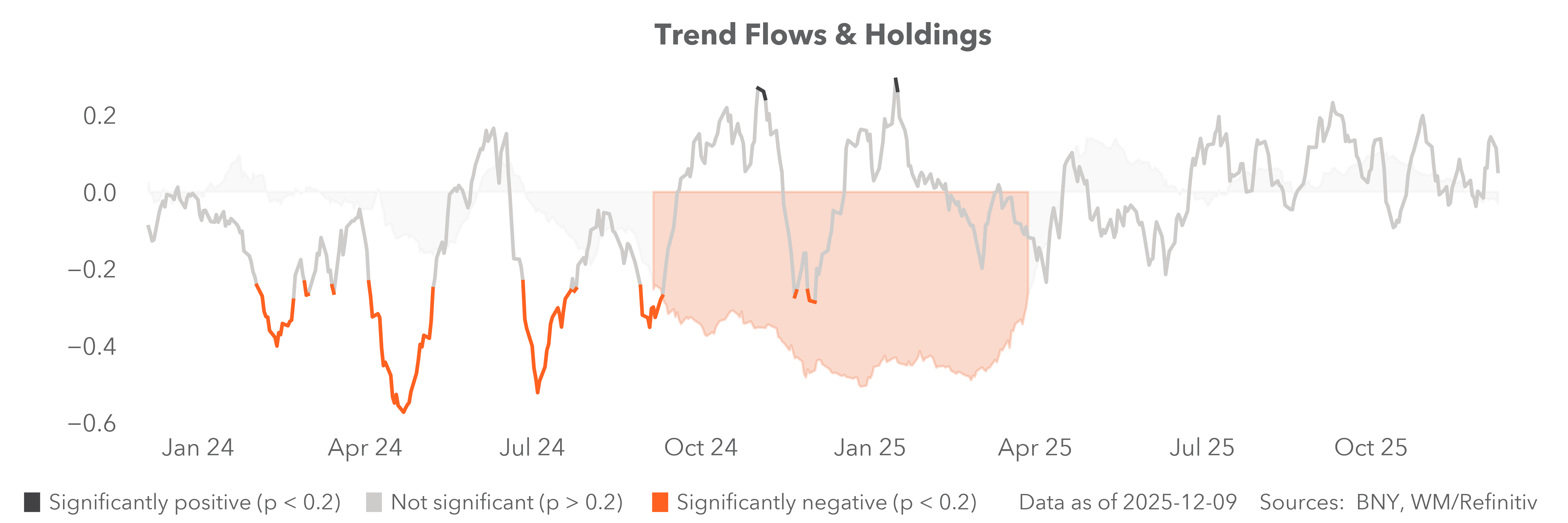

EXHIBIT #1: REER, PAST FIVE YEARS

Source: BNY, BIS

Our take

The IMF concluded its Article IV assessment on China this week and called on Beijing to fix economic “imbalances.” Part of the process would be a “more flexible” FX rate, and Managing Director Kristalina Georgieva implied that some strength would be warranted. At a press briefing in Beijing, she said that China is simply “too big” to generate additional growth from exports and warned that such a growth approach risks “furthering global trade tensions.” We believe China is attentive to such risks and now shows greater tolerance for a stronger renminbi (CNY) as part of its rebalancing process. However, the pace and channel of currency strength will remain at China’s own choosing. We believe the burden of renminbi appreciation in real terms will fall heavily on the inflation channel, considering the ongoing risks surrounding international trade and the domestic need to gradually boost demand and counter involution.

China is not alone in this regard: the South Korean won’s (KRW) real effective exchange rate (REER) depreciation since 2020 is nearly identical to that of the CNY (Exhibit #1), based on Bank for International Settlements (BIS) exchange rate indices. Had the Taiwan dollar (TWD) not endured the May round of nominal gains, its real value would also remain below the same starting point. Taiwan’s export-driven imbalances are arguably far more severe compared to peers. Only the Japanese yen (JPY) has faced greater downside pressure through the nominal channel, but at least inflation has proven strong enough to offset it.

Forward Look

Even if there is clear scope for inflation-based REER gains, the inflation channel itself will be important for global trade relations. The latest release of China’s inflation numbers underscores the issue: CPI is now showing clearer signs of a rebound, but PPI remains materially weak.

From the IMF’s point of view, avoiding trade tensions suggests that PPI-based REER gains are far more desirable. However, domestic efforts to boost household demand, and ultimately wages, point to better prospects for CPI. Furthermore, China’s demand distribution has shifted such that higher disposable income and spending power do not necessarily translate into increased goods imports or reduced global trade tensions. We continue to see strong prospects for EM APAC assets in the year ahead, though FX is unlikely to be a major driver of total returns.

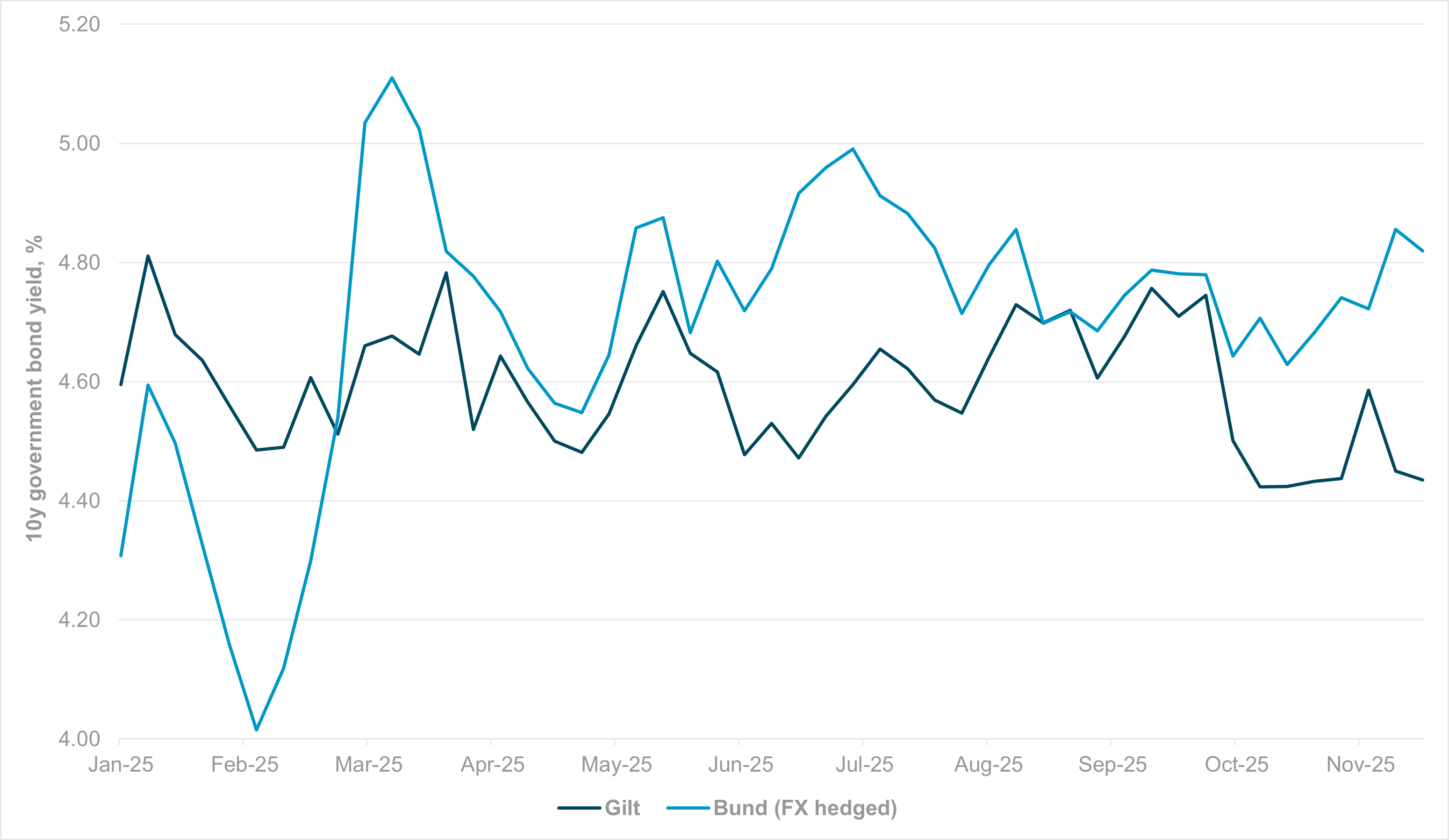

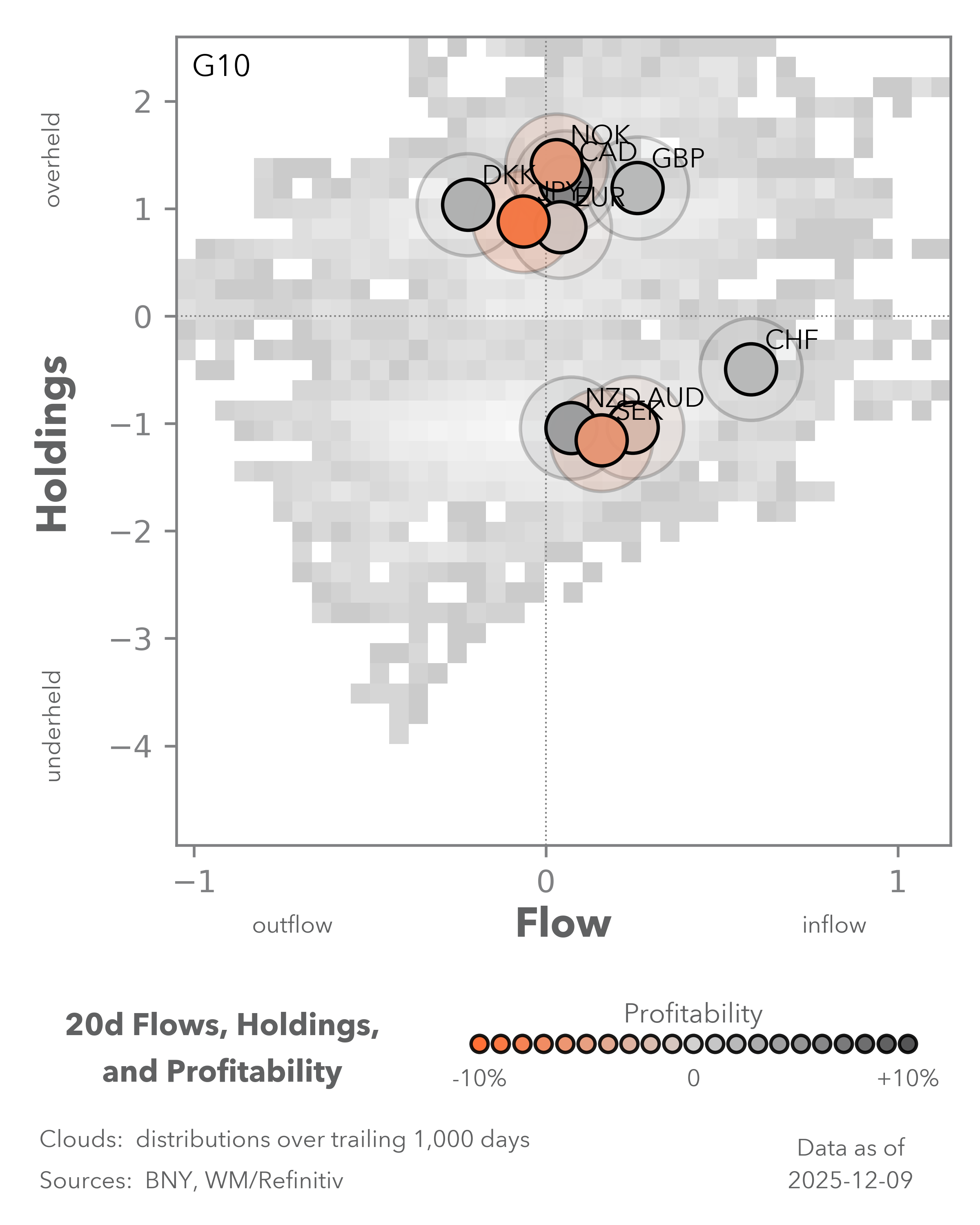

EXHIBIT #2: FISCAL IMPULSE BACK FOR BUNDS, GILTS REFLECT CONSOLIDATION

Source: BNY, Bloomberg

Our take

The past few days have seen a material shift in the European Central Bank’s (ECB) rhetoric, and we now acknowledge that our base case for further easing is unlikely to materialize in 2026. Banque de France Governor François Villeroy and ECB President Christine Lagarde have indicated upward revisions to growth. Governing Council hawks are now more comfortable asserting upside inflation risk, though the prospect of a rate hike remains some way off.

Crucially for the Eurozone and the broader EU, markets are now returning to the pricing of “healthy” reflation, which was the Q1 2025 narrative that drove a jump in Eurozone bond yields and a large-scale rotation into European equities. Faced with an increasingly challenging geostrategic position, there are signs that Germany’s public investment and fiscal narrative is gaining traction once again. This could ultimately boost competitiveness and help the Eurozone avoid stagflation.

Ten-year Bund yields are once again approaching the levels seen in early Q1, and a move to 3% cannot be ruled out. Crucially, the gains reflect productivity rather than inflation, and fiscal sustainability in Germany is not in question.

Forward look

Renewed vigor in Bunds stands in sharp contrast to the U.K., where markets have pushed 10-year gilt yields to YTD lows. This followed material fiscal consolidation and weaker data, finally giving the Bank of England enough confidence to cut rates.

Yesterday, U.K. Chancellor Rachel Reeves did not rule out further fiscal tightening, stating that she reserved the right to act “at any point” to support public finances. However, markets continue to question the broader growth strategy.

Non-inflationary Eurozone growth and fears of ongoing U.K. stagflation are materially changing the risk-reward outlook for fixed income investors with a relative value mandate. This week’s moves in Bund yields mean that, on a hedged basis (calculated using annualized one-month forward points in the EURGBP rate), U.K. investors can now pick up an additional 40bp relative to gilts in nominal terms.

Factoring in inflation differentials, real yields for German and Eurozone sovereign bonds are even more attractive. For unconstrained European fixed income allocators, continued rotation away from the U.K. and into the Eurozone presents additional upside risk to the EURGBP.

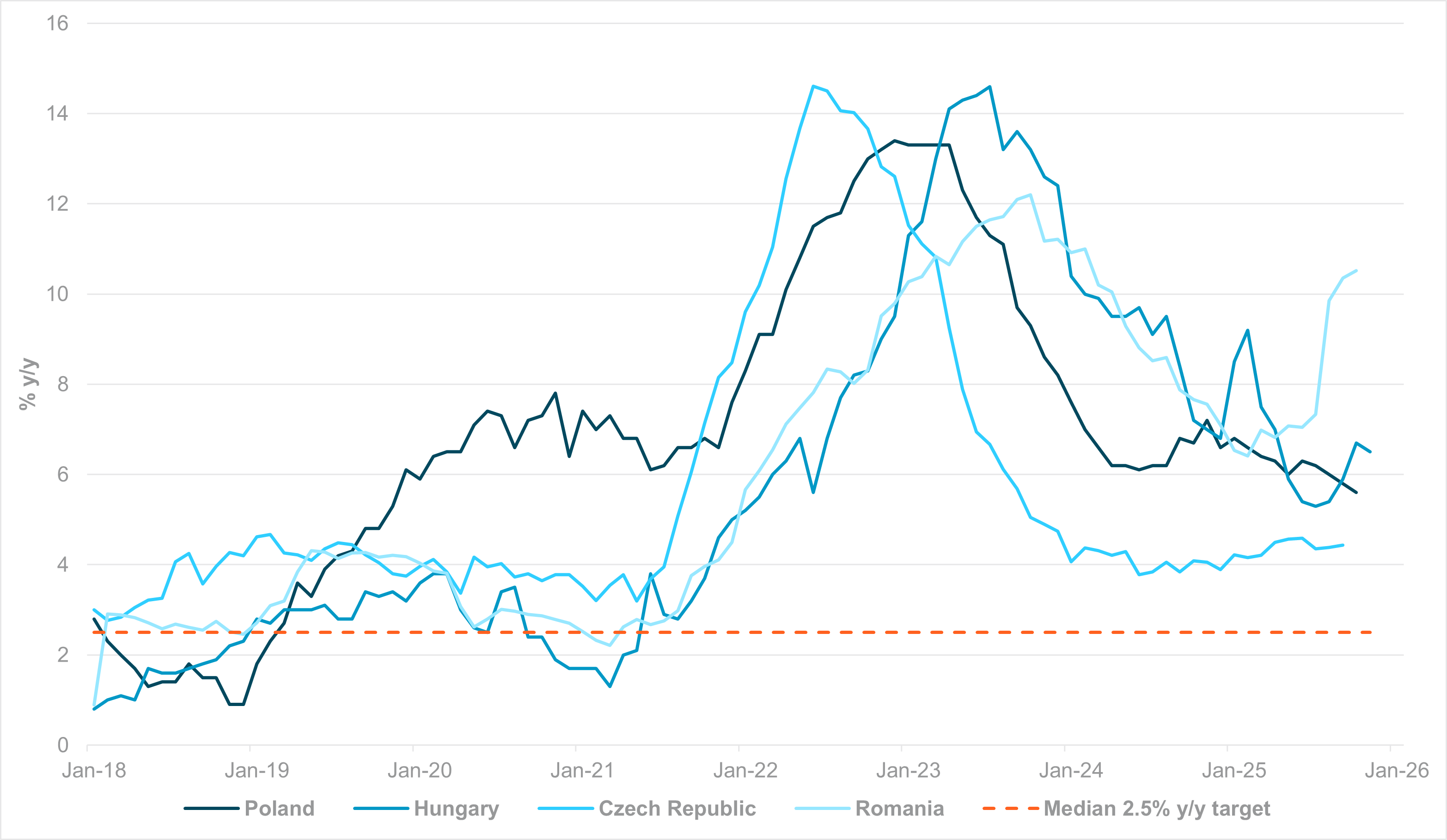

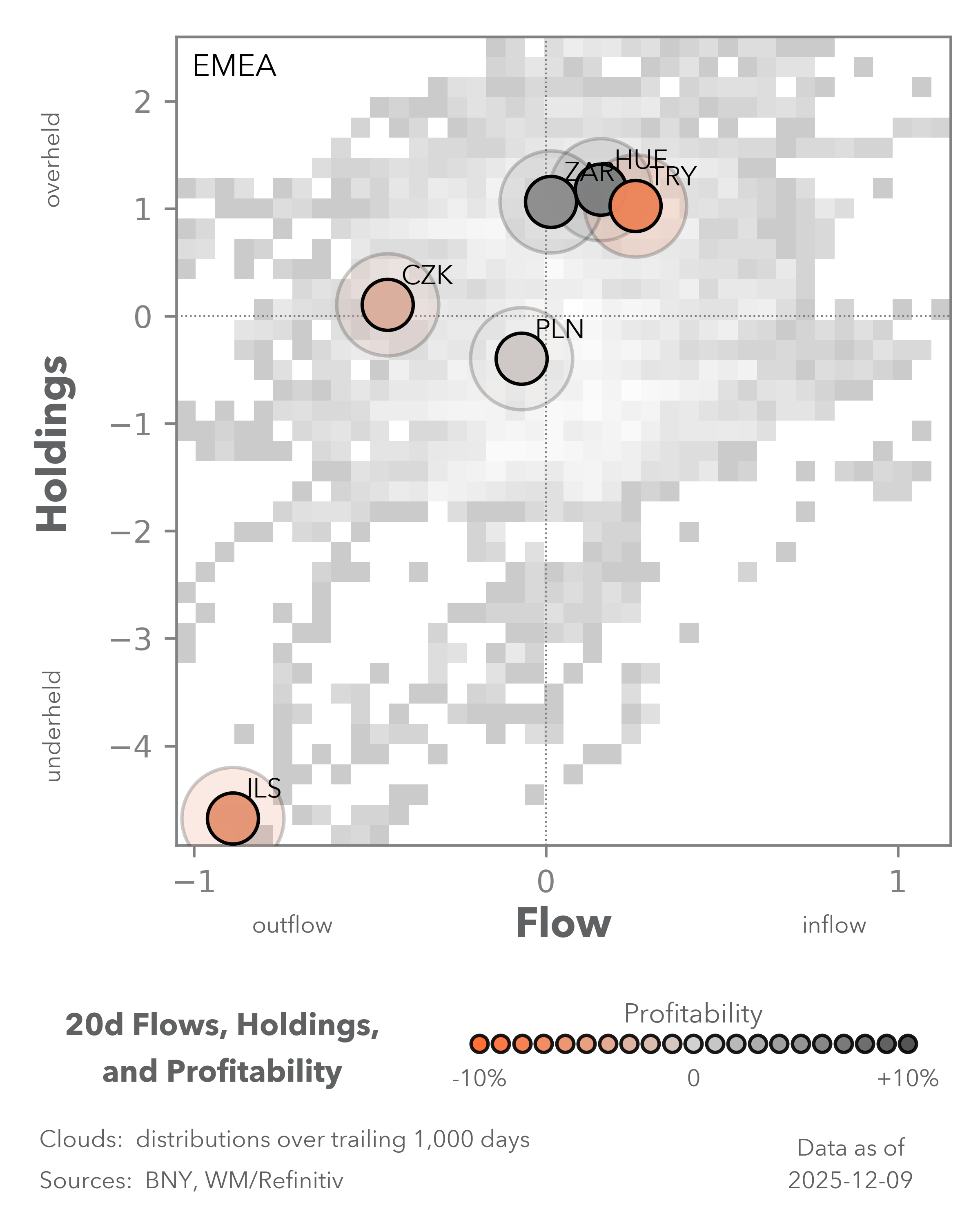

EXHIBIT #3: SERVICES INFLATION, CEE ECONOMIES

Source: BNY, Macrobond

Our take

iFlow indicates that Central and Eastern European (CEE) currencies are facing their most severe round of selling since Q3 2024, as the public spending concerns are now leading to material revisions to the outlook for real rates. The region was already at risk due to heavy holdings of various assets, and FX hedging is now picking up materially.

CEE’s labor supply problem is well-documented, and one reason central banks in the region moved early on rates – helping their currencies appreciate – was to restrain demand driven by very high real wage growth. We highlight that services inflation – which is largely driven by wage growth – moved into double-digits in all four countries (Exhibit #3) between 2022 and 2023. By early this year, signs had finally emerged that tight policy was having an effect.

However, due to domestic needs, government spending plans are being sharply revised higher, and this directly risks a strong rebound in services inflation, where the transmission channel is most prominent. Services inflation is already rising materially in Romania and Hungary. In the Czech Republic, it is also slowly moving higher, even though headline CPI is negative. Only Poland’s services inflation downtrend appears to remain intact, which partially explains why the its central bank was able to push through an additional cut this month.

Forward look

The growth and investment case for CEE remains strong as defense- and industrial supply chains continue to favor the region. This was a key source of wage inflation in the first place, but additional government spending is simply adding to capacity constraints.

Central banks in the region have not yet indicated a shift in their policy stance, and even the ECB is arguably further along this respect. However, services inflation across the region is running well above target. If there is any sign that monetary policy is behind the curve, currency weakness will swiftly follow, especially with the EUR now in a healthier position.

President Trump’s denial of liquidity support for Hungary underscores financing risks. The fact that such support was even discussed reflects broader concerns about the country’s financial account. We expect CEE central banks to remain on hold indefinitely, though a hawkish turn cannot be ruled out.